APAC Aircraft Fuel Market Outlook to 2030

Region:Asia

Author(s):Shubham Kashyap

Product Code:KROD8736

December 2024

96

About the Report

APAC Aircraft Fuel Market Overview

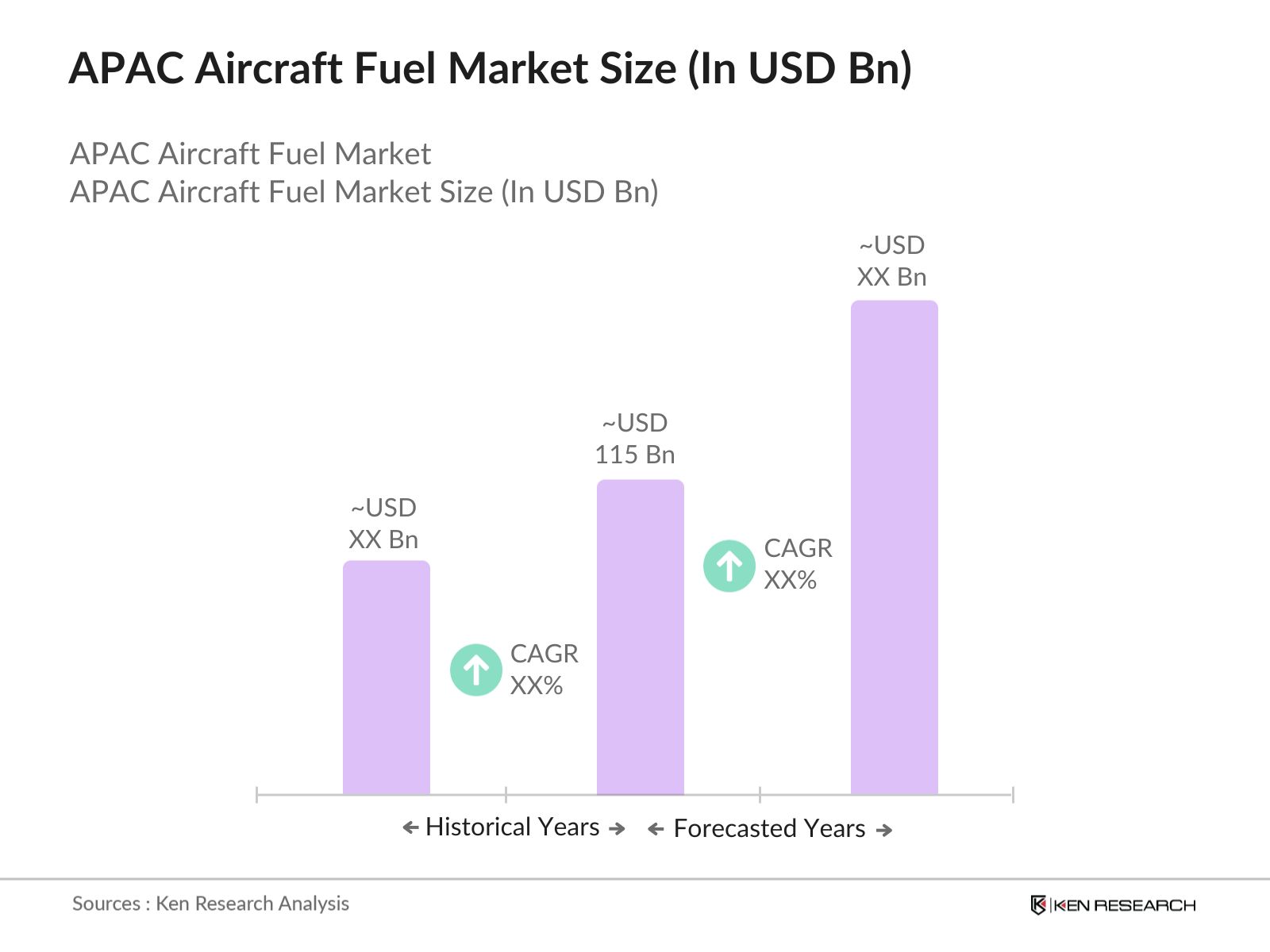

- The APAC aircraft fuel market is valued at USD 115 billion, primarily driven by the rapid growth of the aviation sector, increasing air travel demand, and significant investments in airport infrastructure across the region. The market exhibits steady growth as airlines expand their fleets to cater to rising passenger traffic, while initiatives to improve fuel efficiency and sustainability gain traction. Key factors such as the emergence of low-cost carriers, urbanization, and economic development contribute to the market's stability and long-term expansion, solidifying APAC as a leading market for aviation fuel globally.

- Major demand centers for aircraft fuel in APAC include China, India, and Southeast Asian countries. China dominates due to its robust air traffic growth and substantial investments in aviation infrastructure. India's rapid economic growth and expanding middle class drive increased air travel, further bolstering its position in the market. Southeast Asian nations, particularly Indonesia and Thailand, benefit from thriving tourism industries and strategic geographical locations, enhancing their market presence. The proactive approach to enhancing aviation infrastructure and regulatory support fosters further growth in these countries.

- Governments across the Asia-Pacific (APAC) region have established ambitious emission reduction targets to mitigate aviation's environmental impact. In 2022, the International Civil Aviation Organization (ICAO) adopted a long-term aspirational goal of net-zero carbon dioxide emissions by 2050 for international aviation. Aligning with this, Singapore's Civil Aviation Authority announced in February 2024 a blueprint to achieve net-zero aviation emissions by 2050, emphasizing the adoption of sustainable aviation fuels (SAFs) and operational improvements.

APAC Aircraft Fuel Market Segmentation

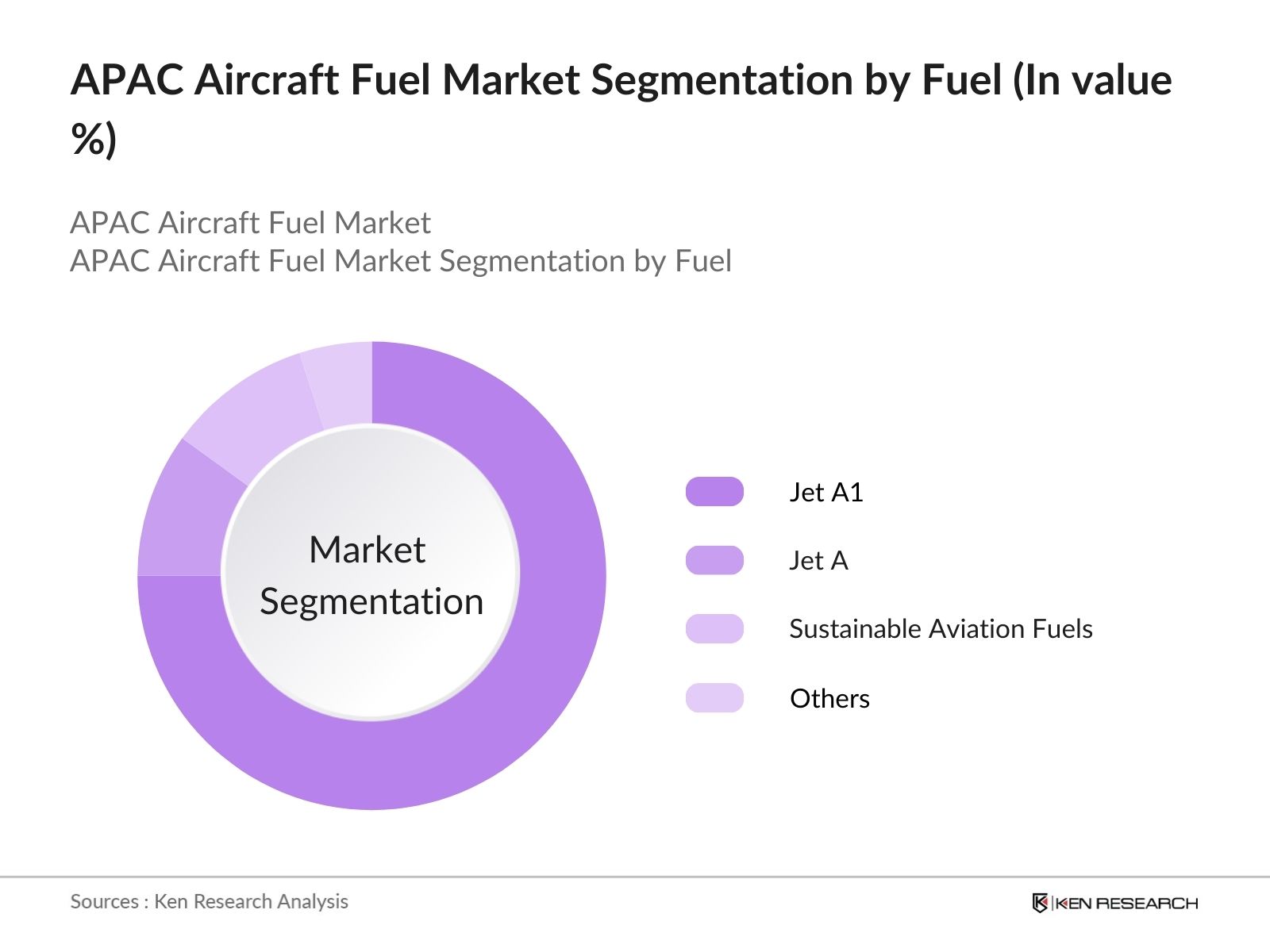

- By Fuel Type: The market is segmented by fuel type into Jet A1, Jet A, Sustainable Aviation Fuels (SAFs), and others. Recently, Jet A1 holds a dominant market share within this segmentation. This trend can be attributed to its widespread availability and compatibility with commercial jet engines, making it the preferred choice for airlines operating both domestic and international routes. The increasing focus on sustainability has also begun to shift attention towards SAFs, but Jet A1 remains the primary fuel source due to its established infrastructure and reliability in meeting the rigorous standards required for aviation fuel.

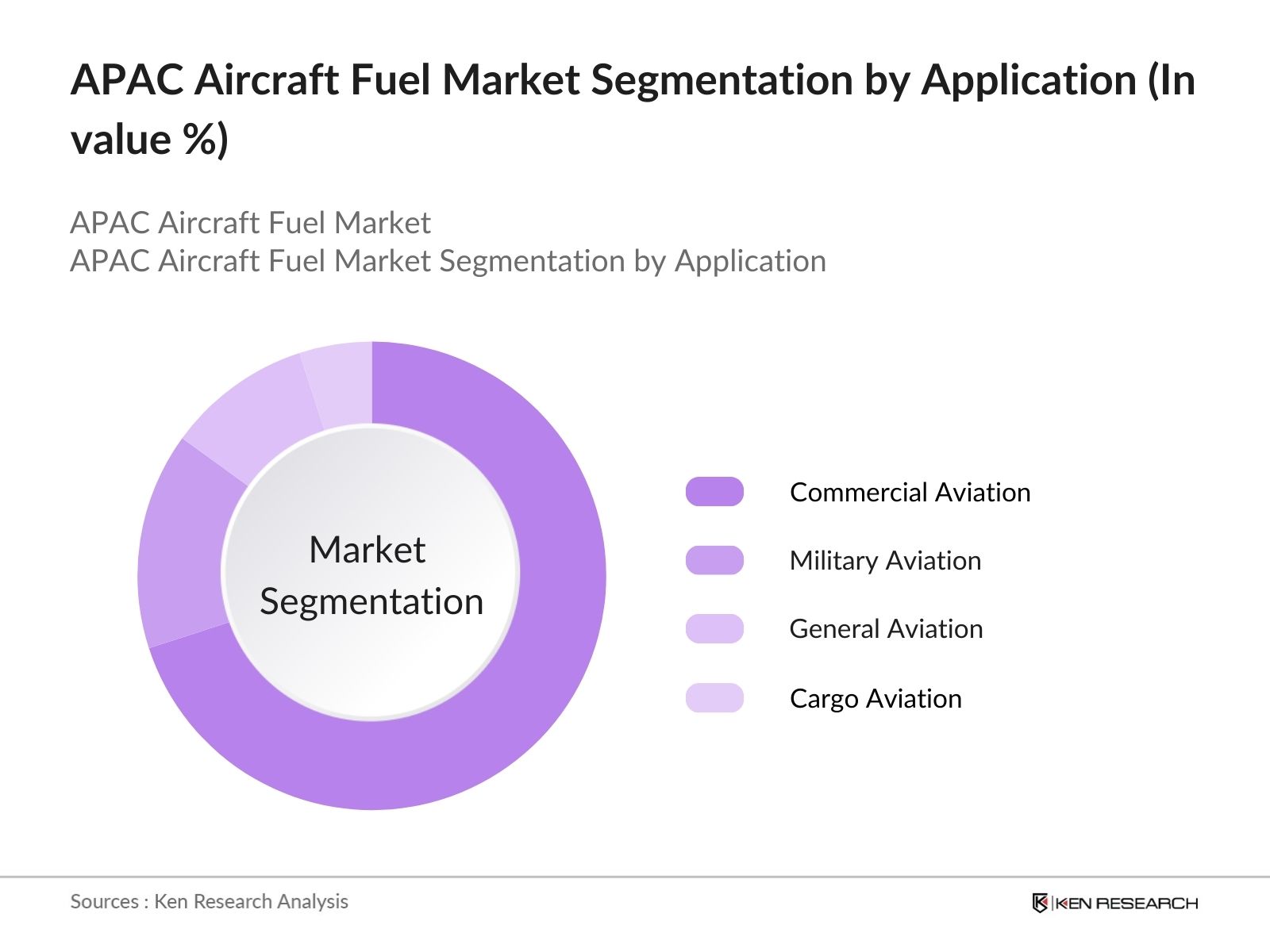

- By Application: The market is segmented by application into commercial aviation, military aviation, general aviation, and cargo aviation. Commercial aviation currently dominates, driven by the exponential growth in passenger numbers and the expansion of airline fleets to meet this demand. The rise in disposable incomes and the growing trend of travel among the middle class further propel the commercial segment, making it a key driver of fuel consumption in the aviation industry. Military and general aviation follow, supported by strategic government investments in defense and private flying operations.

APAC Aircraft Fuel Market Competitive Landscape

The APAC aircraft fuel market is dominated by a few major players, including ExxonMobil Corporation, BP Plc, Royal Dutch Shell Plc, Chevron Corporation, and TotalEnergies SE. These companies leverage their strong brand recognition, extensive distribution networks, and continuous investment in technological innovations to maintain their market leadership positions.

APAC Aircraft Fuel Market Analysis

Growth Drivers

- Expansion of Commercial Aviation: The Asia-Pacific (APAC) region has witnessed a significant expansion in commercial aviation, with the number of scheduled flights increasing from around 7 million in 2019 to over 8 million in 2023. This growth is driven by the emergence of low-cost carriers and the establishment of new routes connecting secondary cities. India's domestic air traffic reached 154 million passengers in 2023, up from 137 million in 2019, indicating a robust recovery and growth trajectory. Similarly, China's domestic air passenger volume surpassed 500 million in 2023, reflecting the region's expanding aviation sector.

- Rising Air Passenger Traffic: Air passenger traffic in the APAC region has been on an upward trajectory, with total passengers carried increasing from 1.5 billion in 2019 to 3 billion in 2023. This surge is attributed to rising disposable incomes, urbanization, and a growing middle class. In Indonesia, air passenger numbers grew from 60 million in 2019 to 69 million in 2023, while Vietnam also saw a noteworthy increase in passengers over the same period. These trends underscore the escalating demand for air travel across the region.

- Government Initiatives for Infrastructure Development: Governments across the APAC region have implemented policies and investments to bolster the aviation sector. China's 14th Five-Year Plan includes the construction of 140 new airports by 2025, aiming to enhance connectivity and support economic development. Similarly, India's National Civil Aviation Policy focuses on increasing regional connectivity and has led to the development of 100 new airports under the UDAN scheme. These initiatives are expected to drive further growth in air travel and, consequently, aviation fuel demand.

Challenges

- Volatility in Crude Oil Prices: The aviation fuel market in the APAC region faces challenges due to fluctuations in crude oil prices. Changes in oil prices directly impact fuel costs, which affects airline profitability and operational planning. To manage these costs, airlines often adjust their ticket prices or implement fuel surcharges. Such measures can influence passenger demand and market dynamics, as travelers may shift preferences in response to fare changes. Price volatility in crude oil thus adds a layer of complexity for airlines in maintaining stable operations and financial performance.

- Environmental Regulations and Emission Norms: Environmental regulations are compelling airlines in the APAC region to adopt cleaner fuels and technologies. The International Civil Aviation Organization's Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) requires airlines to offset emissions that exceed set baseline levels. Additionally, countries like Japan and Singapore have established ambitious emission reduction targets. Compliance with these regulations drives investments in sustainable aviation fuels (SAFs) and fuel-efficient aircraft, presenting financial and operational challenges for airlines as they adapt to increasingly stringent environmental standards.

APAC Aircraft Fuel Market Future Outlook

The APAC aircraft fuel market is poised for robust growth, supported by increasing air travel demand and government initiatives aimed at infrastructure development. The ongoing transition towards Sustainable Aviation Fuels is expected to gain momentum as airlines seek to meet regulatory requirements and address environmental concerns. Additionally, advancements in fuel efficiency technologies will enhance the market's growth trajectory, positioning it favorably for future expansion.

Future Market Opportunities

- Integration of Sustainable Aviation Fuels (SAFs): The APAC region is witnessing a growing adoption of SAFs to meet emission reduction targets. In 2023, Singapore Airlines operated its first flight using SAF, and Japan Airlines committed to using SAF for 10% of its fuel needs by 2030. Additionally, China's Sinopec began producing SAF at its Zhenhai refinery, with an annual capacity of 100,000 tons. These developments present opportunities for fuel producers and suppliers to expand their SAF offerings in the region.

- Technological Innovations in Fuel Efficiency: Advancements in aircraft technology are enhancing fuel efficiency, reducing operational costs, and lowering emissions. The introduction of Boeing 787 Dreamliner and Airbus A350 aircraft, which consume 20% less fuel than previous models, has been adopted by airlines like All Nippon Airways and Cathay Pacific. Such technological progress offers opportunities for airlines to optimize fuel consumption and align with environmental regulations.

Scope of the Report

|

By Fuel Type |

Jet A1 |

|

By Application |

Commercial Aviation |

|

By Distribution Channel |

Direct Sales |

|

By End-User |

Airlines Defense Private Jet Operators Cargo Operators |

|

By Region |

China India Japan Australia South Korea Rest of APAC |

Products

Key Target Audience

Airlines

Aircraft Manufacturers

Fuel Suppliers

Government and Regulatory Bodies (e.g., Civil Aviation Authority of Singapore)

Defense Organizations

Airport Operators

Investors and Venture Capitalist Firms

Banks and Financial Institutions

Companies

Players Mentioned in the Report

ExxonMobil Corporation

Chevron Corporation

Royal Dutch Shell Plc

BP Plc

China Aviation Oil Corporation Ltd

Bharat Petroleum Corporation Ltd

Hindustan Petroleum Corporation Ltd

Indian Oil Corporation Ltd

Petronas

Pertamina

Idemitsu Kosan Co., Ltd.

SK Energy

GS Caltex

Neste Oyj

TotalEnergies SE

Table of Contents

APAC Aircraft Fuel Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

APAC Aircraft Fuel Market Size (In USD Million)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

APAC Aircraft Fuel Market Analysis

3.1. Growth Drivers

3.1.1. Expansion of Commercial Aviation

3.1.2. Rising Air Passenger Traffic

3.1.3. Economic Growth in Emerging Markets

3.1.4. Government Initiatives and Investments

3.2. Market Challenges

3.2.1. Volatility in Crude Oil Prices

3.2.2. Environmental Regulations and Emission Norms

3.2.3. Infrastructure Constraints

3.3. Opportunities

3.3.1. Adoption of Sustainable Aviation Fuels (SAFs)

3.3.2. Technological Advancements in Fuel Efficiency

3.3.3. Strategic Partnerships and Collaborations

3.4. Trends

3.4.1. Shift Towards Biofuels and Alternative Energy Sources

3.4.2. Digitalization in Fuel Management Systems

3.4.3. Integration of AI and IoT in Fuel Monitoring

3.5. Government Regulations

3.5.1. Emission Reduction Targets

3.5.2. Subsidies and Incentives for SAF Adoption

3.5.3. International Aviation Agreements

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competitive Landscape

APAC Aircraft Fuel Market Segmentation

4.1. By Fuel Type (In Value %)

4.1.1. Jet A1

4.1.2. Jet A

4.1.3. Sustainable Aviation Fuels (SAFs)

4.1.4. Others

4.2. By Application (In Value %)

4.2.1. Commercial Aviation

4.2.2. Military Aviation

4.2.3. General Aviation

4.2.4. Cargo Aviation

4.3. By Distribution Channel (In Value %)

4.3.1. Direct Sales

4.3.2. Distributors

4.3.3. Online Platforms

4.4. By End-User (In Value %)

4.4.1. Airlines

4.4.2. Defense Organizations

4.4.3. Private Jet Operators

4.4.4. Cargo Operators

4.5. By Region (In Value %)

4.5.1. China

4.5.2. India

4.5.3. Japan

4.5.4. Australia

4.5.5. South Korea

4.5.6. Rest of APAC

APAC Aircraft Fuel Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. ExxonMobil Corporation

5.1.2. Chevron Corporation

5.1.3. Royal Dutch Shell Plc

5.1.4. BP Plc

5.1.5. TotalEnergies SE

5.1.6. China Aviation Oil Corporation Ltd

5.1.7. Bharat Petroleum Corporation Ltd

5.1.8. Hindustan Petroleum Corporation Ltd

5.1.9. Indian Oil Corporation Ltd

5.1.10. Petronas

5.1.11. Pertamina

5.1.12. Idemitsu Kosan Co., Ltd.

5.1.13. SK Energy

5.1.14. GS Caltex

5.1.15. Neste Oyj

5.2. Cross Comparison Parameters (Revenue, Market Share, Geographic Presence, Product Portfolio, R&D Investment, Strategic Initiatives, Number of Employees, Year of Establishment)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.6.1. Venture Capital Funding

5.6.2. Government Grants

5.6.3. Private Equity Investments

APAC Aircraft Fuel Market Regulatory Framework

6.1. Environmental Standards

6.2. Compliance Requirements

6.3. Certification Processes

APAC Aircraft Fuel Future Market Size (In USD Million)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

APAC Aircraft Fuel Future Market Segmentation

8.1. By Fuel Type (In Value %)

8.2. By Application (In Value %)

8.3. By Distribution Channel (In Value %)

8.4. By End-User (In Value %)

8.5. By Region (In Value %)

APAC Aircraft Fuel Market Analysts Recommendations

9.1. Total Addressable Market (TAM), Serviceable Available Market (SAM), Serviceable Obtainable Market (SOM) Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the APAC aircraft fuel market. This step is grounded in extensive desk research, utilizing secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, we compile and analyze historical data pertaining to the APAC aircraft fuel market, assessing market penetration and the interaction between fuel suppliers and airlines, along with resultant revenue generation. Further, an evaluation of service quality statistics is conducted to ensure the reliability and accuracy of revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed and subsequently validated through computer-assisted telephone interviews (CATIs) with industry experts representing a variety of companies. These consultations provide valuable operational and financial insights directly from industry practitioners, which are instrumental in refining and corroborating the market data.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with multiple aircraft fuel suppliers and airlines to gather detailed insights into product segments, sales performance, consumer preferences, and other pertinent factors. This interaction serves to verify and complement the statistics derived from the bottom-up approach, thereby ensuring a comprehensive, accurate, and validated analysis of the APAC aircraft fuel market.

Frequently Asked Questions

01. How big is the APAC Aircraft Fuel Market?

The APAC aircraft fuel market was valued at USD 115 billion, driven by increasing air travel and demand for efficient fuel management across commercial and cargo aviation sectors.

02. What are the key challenges in the APAC Aircraft Fuel Market?

Challenges in the APAC aircraft fuel market include fluctuating crude oil prices, stringent environmental regulations, and infrastructure limitations in emerging economies, which impact fuel logistics and availability.

03. Who are the major players in the APAC Aircraft Fuel Market?

Major players in the APAC aircraft fuel market include ExxonMobil Corporation, Chevron Corporation, Royal Dutch Shell Plc, BP Plc, and China Aviation Oil Corporation Ltd, dominating through their extensive networks and strategic partnerships.

04. What factors drive the APAC Aircraft Fuel Market?

The APAC aircraft fuel market is propelled by rising air passenger traffic, government investments in aviation infrastructure, and increasing adoption of sustainable aviation fuels to align with emission reduction goals.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.