APAC Iron and Steel Market Outlook to 2030

Region:Asia

Author(s):Shubham Kashyap

Product Code:KROD4974

December 2024

92

About the Report

APAC Iron and Steel Market Overview

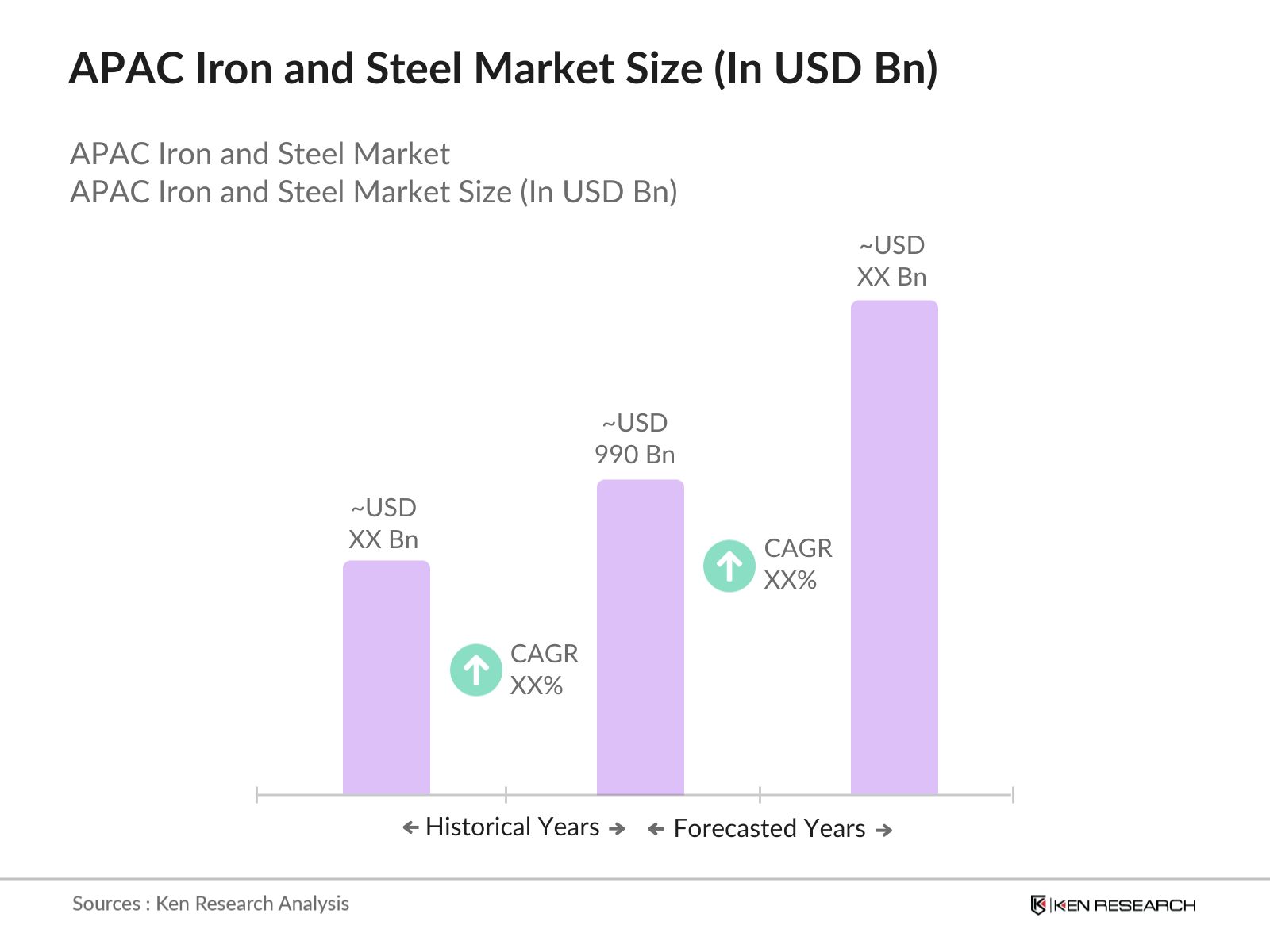

- The APAC Iron and Steel Market is currently valued at USD 990 billion, according to recent analysis. The market is primarily driven by the rapid industrialization, urbanization, and infrastructure development in emerging economies such as China, India, and Southeast Asian nations. These countries account for a significant share of global steel production and consumption, with China alone producing over 50% of the worlds steel output. Increasing demand for steel in construction, automotive, and manufacturing sectors is expected to propel market growth across the APAC region.

- Major markets like China, Japan, and India are leading the iron and steel industry, driven by strong government initiatives to boost infrastructure development. The Belt and Road Initiative (BRI) in China and the Smart Cities Mission in India have led to a surge in demand for steel products in various applications, from construction to transportation. Emerging markets in Southeast Asia, such as Vietnam and Indonesia, are also contributing to market growth, driven by increasing foreign investments in manufacturing and infrastructure sectors.

- Government policies and initiatives play a critical role in shaping the iron and steel market in the APAC region. China has implemented strict capacity reduction policies to eliminate outdated steel plants and promote environmentally friendly steel production. India has launched the National Steel Policy, aiming to increase the countrys steel production capacity to 300 million tons by 2030. These government interventions are likely to strengthen the markets growth trajectory in the coming years.

APAC Iron and Steel Market Segmentation

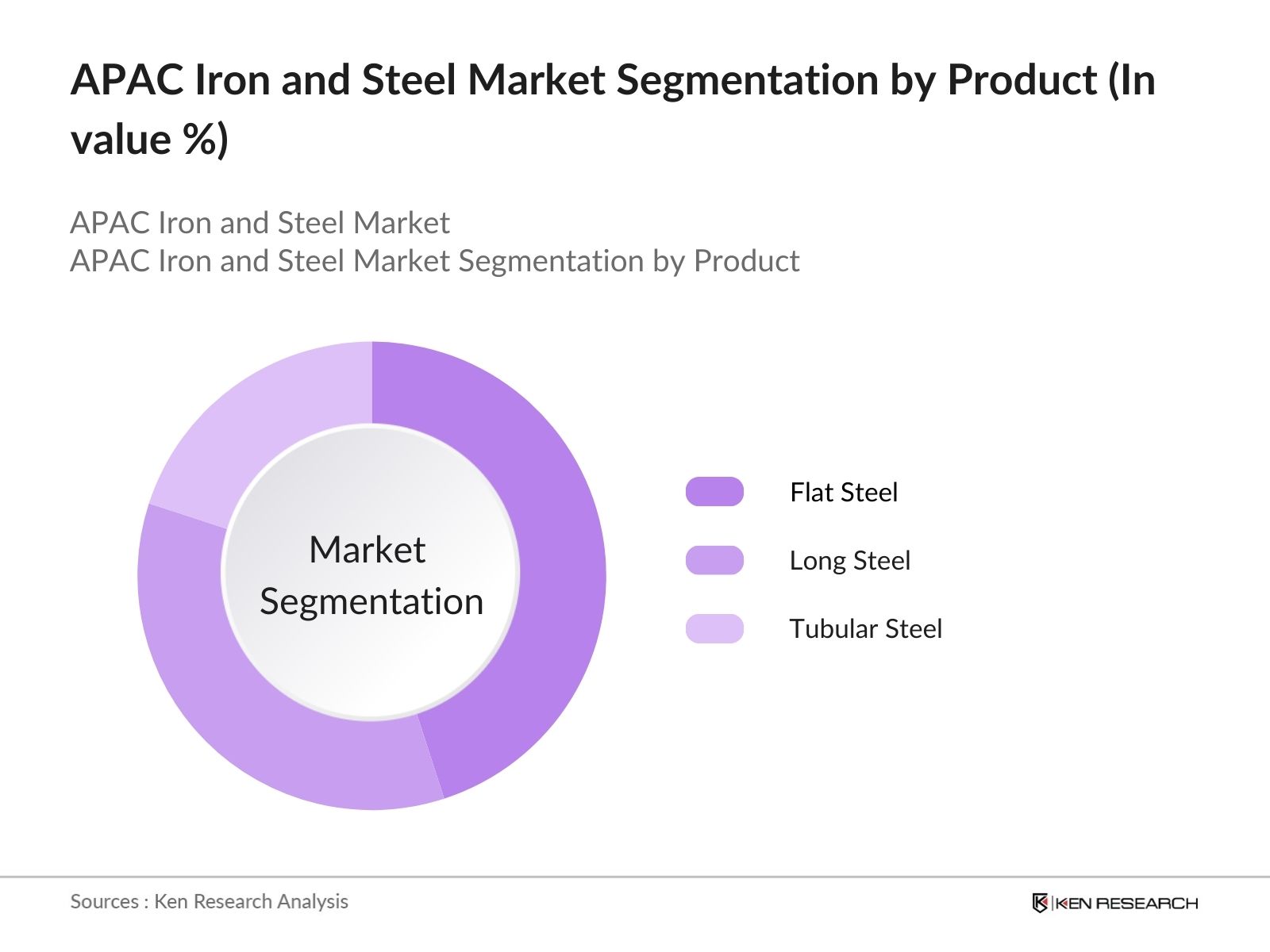

- By Product Type: The market is segmented by product type into flat steel, long steel, and tubular steel. Flat steel holds a dominant position in the market, driven by its extensive applications in automotive manufacturing, construction, and machinery. This segment is particularly strong in markets like China and India, where rapid urbanization and government-backed infrastructure projects are increasing the demand for high-quality steel sheets and plates. Flat steels versatility and durability make it a key product for automotive and construction industries.

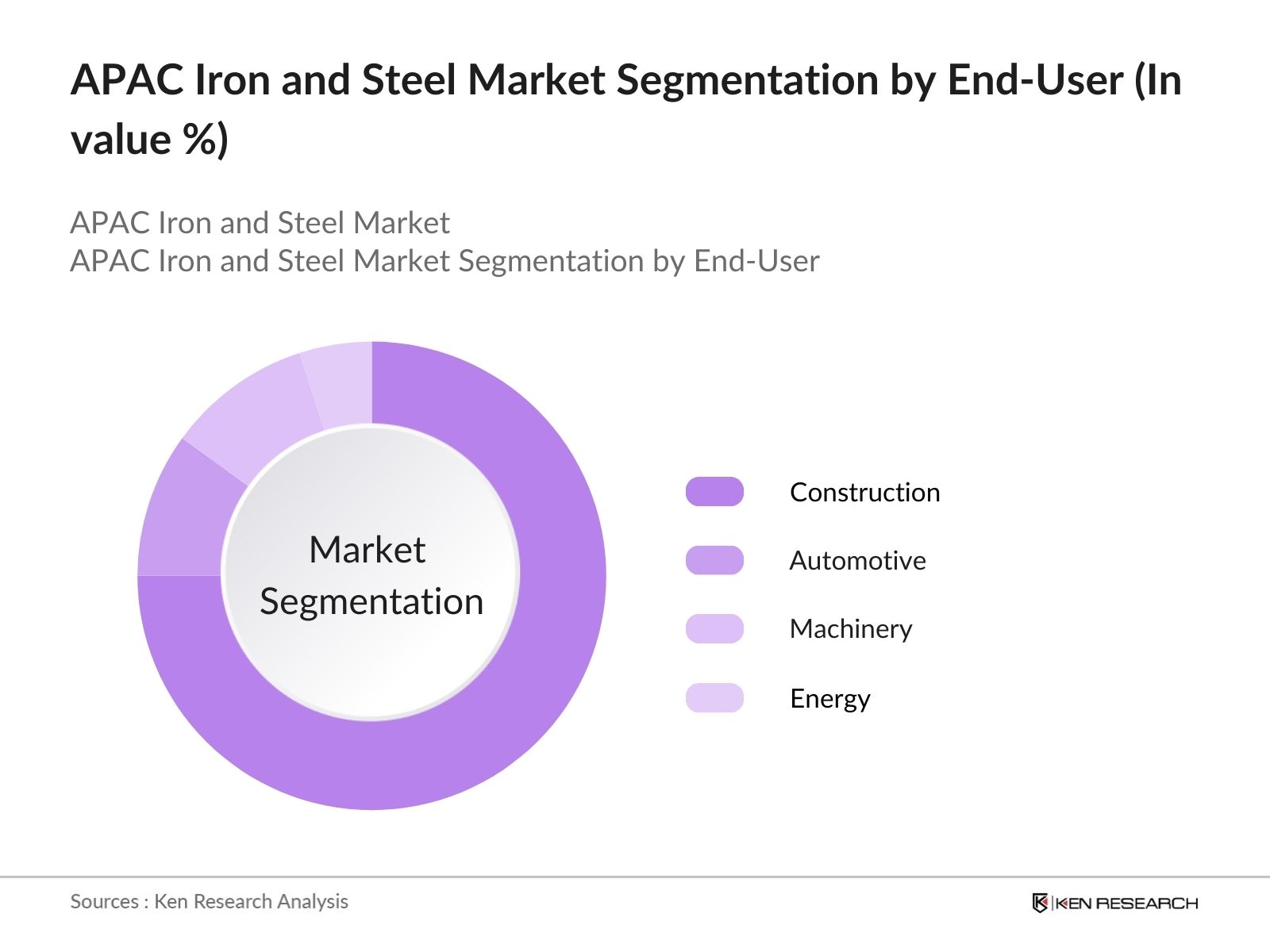

- By End-User: The Market is further segmented by end-user into construction, automotive, machinery, and energy. The construction industry dominates the market, accounting for a significant share due to large-scale infrastructure projects across APAC. Countries like China and India are experiencing a surge in demand for steel products, particularly in building bridges, roads, and residential complexes. The automotive sector is also a substantial contributor to the iron and steel market, with increasing vehicle production across APAC, driving demand for automotive-grade steel.

APAC Iron and Steel Market Competitive Landscape

The APAC Iron and Steel Market is highly competitive, with both global and regional players vying for market share. Major companies such as ArcelorMittal, Nippon Steel Corporation, Tata Steel, and POSCO dominate the market with their extensive production capacities and advanced technological capabilities. These companies are focusing on capacity expansions, mergers, and acquisitions to strengthen their market position.

|

Company Name |

Establishment Year |

Headquarters |

Production Capacity |

Global Footprint |

Sustainability Initiatives |

R&D Investments |

Technology Focus |

Key Markets |

|

ArcelorMittal |

2006 |

Luxembourg |

||||||

|

Nippon Steel Corporation |

1970 |

Tokyo, Japan |

||||||

|

Tata Steel |

1907 |

Mumbai, India |

||||||

|

POSCO |

1968 |

Pohang, South Korea |

||||||

|

China Baowu Steel Group |

1978 |

Shanghai, China |

APAC Iron and Steel Industry Analysis

Growth Drivers

- Increasing Infrastructure Development: Massive infrastructure initiatives across APAC, particularly in India, Indonesia, and the Philippines, drive steel demand. Indias National Infrastructure Pipeline (NIP), which requires over USD 1.5 trillion in investment by 2025, is a prime example of this growth. The ongoing construction of highways, bridges, and railways in the region creates substantial demand for iron and steel products, with an estimated 138 million metric tons of steel used annually in India's construction projects as of 2024.

- Automotive Industry Expansion: The expansion of the automotive sector in countries like Japan, South Korea, and India continues to boost steel demand. According to various sources, including the Society of Indian Automobile Manufacturers (SIAM) and industry reports, the total production of vehicles in India for the fiscal year 2023 (April 2022 to March 2023) was 25.9 million vehicles, with steel being a crucial component in vehicle manufacturing. Japan and South Korea, with production capacities exceeding 9 million vehicles annually, also rely heavily on steel for lightweight and high-strength vehicle parts. The ongoing investments in electric vehicle (EV) manufacturing have further increased the need for specialized steel.

- Rising Steel Production Capacity: APAC is the global leader in steel production, with China alone producing over 1 billion metric tons annually as of 2023. India follows with a production capacity nearing 150 million metric tons. Investments in new steel plants and technology upgrades have bolstered the regions steel production capabilities. For example, Indias Steel Ministry targets 300 million metric tons of capacity by 2030, up from the current level of around 134 million metric tons in 2024, reinforcing APACs dominance in the global steel market.

Market Challenges

- Stringent Environmental Regulations: Stricter environmental regulations across the APAC Ministry of Ecology and Environment have enforced tighter carbon emissions standards on steel plants, pushing companies to adopt cleaner technologies. These regulations require steel manufacturers to invest in advanced emissions-reducing technology, significantly increasing operational costs. Similarly, India's National Clean Air Programme mandates stricter pollution control measures, which also place financial and technological pressures on local steel producers to meet these environmental standards.

- Overcapacity in China: China's steel industry continues to struggle with overcapacity, producing more steel than its domestic market demands. The countrys steel surplus is often exported to other APAC markets at lower prices, disrupting the competitive landscape. This excess production has had significant effects on neighboring countries like India and Vietnam, leading to reduced profitability for local manufacturers and increased competition from cheaper Chinese steel imports. The ripple effect of Chinas overcapacity poses ongoing challenges for the steel industry across the region, with market dynamics shifting frequently.

APAC Iron and Steel Market Future Outlook

The APAC Iron and Steel Market is expected to witness substantial growth over the next five years, driven by increased demand from the construction, automotive, and machinery sectors. Government initiatives aimed at infrastructure development and the adoption of advanced steel production technologies will further propel market growth. However, challenges such as environmental regulations and trade disputes may affect the markets expansion.

Future Market Opportunities

- Green Steel Production: The shift towards green steel production presents significant opportunities for APACs iron and steel market. As of 2024, countries like Japan and South Korea are investing in hydrogen-based steelmaking processes to reduce carbon emissions. Japans steelmakers aim to achieve net-zero emissions by 2050, with major players like Nippon Steel allocating USD 3 billion for green steel production initiatives. India is also exploring green hydrogen technology for steelmaking, presenting new opportunities for eco-friendly production methods.

- Expansion in Southeast Asia: Southeast Asian nations like Vietnam, Thailand, and Indonesia are emerging as key growth markets for iron and steel. The Vietnam Steel Association (VSA) has forecasted a modest growth in steel demand, with an expected increase of about 6.4% in 2024, which translates to 21.6 million metric tons of consumption. Indonesia is building new steel plants with a combined capacity of over 10 million metric tons as of 2023, aiming to reduce its reliance on imports and support local infrastructure development.

Scope of the Report

|

By Product Type |

Flat Steel Products Long Steel Products Stainless Steel Products |

|

By Production Process |

Basic Oxygen Furnace Electric Arc Furnace |

|

By Application |

Construction Automotive Machinery & Equipment Consumer Goods Energy |

|

By End-User Industry |

Residential & Commercial Construction Automotive & Transportation Shipbuilding Industrial Machinery Others |

|

By Region |

China India Japan |

Products

Key Target Audience

Steel Manufacturers

Construction Companies

Automotive Manufacturers

Machinery Producers

Investors and Venture Capitalist Firms

Banks and Financial Institutions

Government Bodies (Ministry of Steel in India, National Development and Reform Commission in China)

Environmental Regulatory Agencies (Ministry of Ecology and Environment in China)

Companies

Major Players Mentioned in the Report

ArcelorMittal

Nippon Steel Corporation

Tata Steel

POSCO

China Baowu Steel Group

JFE Steel

Hyundai Steel

JSW Steel Ltd.

Shougang Group

Nucor Corporation

Severstal

Thyssenkrupp AG

Gerdau SA

Ansteel Group

Hesteel Group

Table of Contents

1. APAC Iron and Steel Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Drivers and Restraints (Steel demand from construction, infrastructure, and automotive industries)

1.4. Market Segmentation Overview (Primary steel production, Secondary steel production, Finished steel products)

2. APAC Iron and Steel Market Size (In USD Bn)

2.1. Historical Market Size (Demand from major economies China, India, Japan)

2.2. Year-On-Year Growth Analysis (Production vs. consumption trends)

2.3. Key Market Developments and Milestones (Major capacity expansions, trade regulations, etc.)

3. APAC Iron and Steel Market Analysis

3.1. Growth Drivers

3.1.1. Rapid Urbanization and Infrastructure Development (Major infrastructure projects in China and India)

3.1.2. Automotive and Machinery Sector Demand (Rising steel usage in EV production)

3.1.3. Government Policies Promoting Steel Production (Subsidies, investment incentives)

3.1.4. Technological Advancements in Steel Manufacturing (Automation, reduction of CO2 emissions)

3.2. Market Challenges

3.2.1. High Energy Consumption in Steel Production (Energy inefficiencies in blast furnaces)

3.2.2. Volatility in Raw Material Prices (Fluctuating prices of iron ore, coking coal)

3.2.3. Environmental Regulations (Stringent emissions control)

3.2.4. Trade Wars and Tariffs (Impact of U.S. tariffs on steel exports)

3.3. Opportunities

3.3.1. Shift Towards Green Steel Production (Hydrogen-based DRI, use of renewables in steelmaking)

3.3.2. Increasing Demand for High-Strength Steels (Automotive, aerospace applications)

3.3.3. Growing Steel Demand in Southeast Asian Economies (Indonesia, Vietnam)

3.4. Trends

3.4.1. Integration of Digital Technologies (AI, IoT, and automation in steel plants)

3.4.2. Adoption of Circular Economy Practices (Steel recycling, use of scrap)

3.4.3. Consolidation of Steel Companies (Mergers and acquisitions in APAC)

3.4.4. Regional Steel Trade Agreements (RCEP and its impact on regional trade)

3.5. Government Regulations

3.5.1. Emissions Standards (Carbon-neutral initiatives in Japan, Chinas 2060 carbon goal)

3.5.2. Incentives for Energy Efficiency (APAC government schemes for green steel production)

3.5.3. Anti-Dumping Regulations (Impact on steel imports and exports)

3.6. SWOT Analysis (Strengths, Weaknesses, Opportunities, Threats)

3.7. Stakeholder Ecosystem (Steel producers, suppliers, logistics partners, etc.)

3.8. Porters Five Forces (Supply chain dynamics, bargaining power of suppliers, threat of new entrants)

3.9. Competition Ecosystem (Regional and global competition, technology adoption among competitors)

4. APAC Iron and Steel Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Flat Steel Products (Sheets, plates, coils)

4.1.2. Long Steel Products (Bars, rods, beams)

4.1.3. Stainless Steel Products (Corrosion-resistant steel)

4.2. By Production Process (In Value %)

4.2.1. Basic Oxygen Furnace (BOF)

4.2.2. Electric Arc Furnace (EAF)

4.3. By Application (In Value %)

4.3.1. Construction

4.3.2. Automotive

4.3.3. Machinery and Equipment

4.3.4. Consumer Goods

4.3.5. Energy (Pipelines, oil rigs, wind turbines)

4.4. By End-User Industry (In Value %)

4.4.1. Residential & Commercial Construction

4.4.2. Automotive & Transportation

4.4.3. Shipbuilding & Offshore Engineering

4.4.4. Industrial Machinery

4.4.5. Others

4.5. By Region (In Value %)

4.5.1. China

4.5.2. India

4.5.3. Japan

4.5.4. Rest of APAC

5. APAC Iron and Steel Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. ArcelorMittal

5.1.2. Nippon Steel Corporation

5.1.3. POSCO

5.1.4. China Baowu Steel Group

5.1.5. Tata Steel

5.1.6. JSW Steel Ltd

5.1.7. JFE Steel Corporation

5.1.8. Hyundai Steel

5.1.9. China Steel Corporation (CSC)

5.1.10. Shougang Group

5.1.11. HBIS Group

5.1.12. United States Steel Corporation

5.1.13. Gerdau SA

5.1.14. Voestalpine Group

5.1.15. Evraz Group

5.2. Cross Comparison Parameters (Production Capacity, Market Share, Technological Adoption, Revenue, Supply Chain Integration, Regional Presence, Mergers & Acquisitions, Sustainability Initiatives)

5.3. Market Share Analysis

5.4. Strategic Initiatives (R&D investments, sustainability projects, expansions)

5.5. Mergers And Acquisitions

5.6. Investment Analysis (Capital expenditure in new plants, green technologies)

5.7. Government Grants and Subsidies

5.8. Private Equity Investments

6. APAC Iron and Steel Market Regulatory Framework

6.1. Environmental Standards (Emissions limits, energy efficiency standards)

6.2. Compliance Requirements (International steel quality standards, environmental compliance)

6.3. Certification Processes (ISO certifications, sustainability certifications)

7. APAC Iron and Steel Future Market Size (In USD Bn)

7.1. Future Market Size Projections (Key factors shaping future demand)

7.2. Key Factors Driving Future Market Growth

8. APAC Iron and Steel Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Production Process (In Value %)

8.3. By Application (In Value %)

8.4. By End-User Industry (In Value %)

8.5. By Region (In Value %)

9. APAC Iron and Steel Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Market Entry Strategies (Geographic regions, partnerships)

9.3. Competitive Positioning (Differentiation, pricing strategies)

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The initial step involved mapping the key stakeholders in the APAC Iron and Steel Market ecosystem, focusing on steel manufacturers, end-user industries, and regulatory bodies. Through comprehensive desk research, industry-level data was gathered using credible secondary sources like government publications and proprietary databases to identify key variables impacting the market.

Step 2: Market Analysis and Construction

This phase involved analyzing historical data related to steel production and consumption in APAC. The analysis considered the influence of key sectors like construction and automotive on the market's revenue generation. Additional emphasis was placed on supply chain dynamics, including raw material availability and price fluctuations.

Step 3: Hypothesis Validation and Expert Consultation

To validate the data, we conducted consultations with industry experts from leading steel manufacturers, such as Tata Steel and POSCO. These discussions were done through telephonic interviews, allowing for the verification of market trends, competitive insights, and future projections, ensuring accuracy in our findings.

Step 4: Research Synthesis and Final Output

In the final stage, the research team synthesized all data and insights obtained from both secondary research and expert consultations. The final report was cross-validated using the bottom-up approach, ensuring that market forecasts, production data, and segmentation insights were accurate and reflective of the actual market conditions.

Frequently Asked Questions

01 How big is the APAC Iron and Steel Market?

The APAC Iron and Steel market is valued at USD 990 billion, driven by large infrastructure projects, rapid urbanization, and the region's strong manufacturing base, particularly in China, India, and Japan.

02 What are the challenges in the APAC Iron and Steel Market?

Key challenges in the APAC Iron and Steel market include environmental regulations, overcapacity issues in China, rising raw material costs, and trade disputes. These factors can potentially slow market growth and impact profitability for steel manufacturers.

03 Who are the major players in the APAC Iron and Steel Market?

Major players in the APAC Iron and Steel market include ArcelorMittal, Nippon Steel Corporation, Tata Steel, POSCO, and China Baowu Steel Group, dominating the market with their strong production capacities and global reach.

04 What are the growth drivers of the APAC Iron and Steel Market?

Growth drivers in the APAC Iron and Steel markets include government-backed infrastructure projects, increasing automotive production, and rising demand for sustainable steel products. These factors are contributing to the market's expansion across key regions in APAC.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.