Asia Pacific Car Audio Market Outlook to 2030

Region:Asia

Author(s):Meenakshi Bisht

Product Code:KROD5020

Region:Asia

Author(s):Meenakshi Bisht

Product Code:KROD5020

December 2024

84

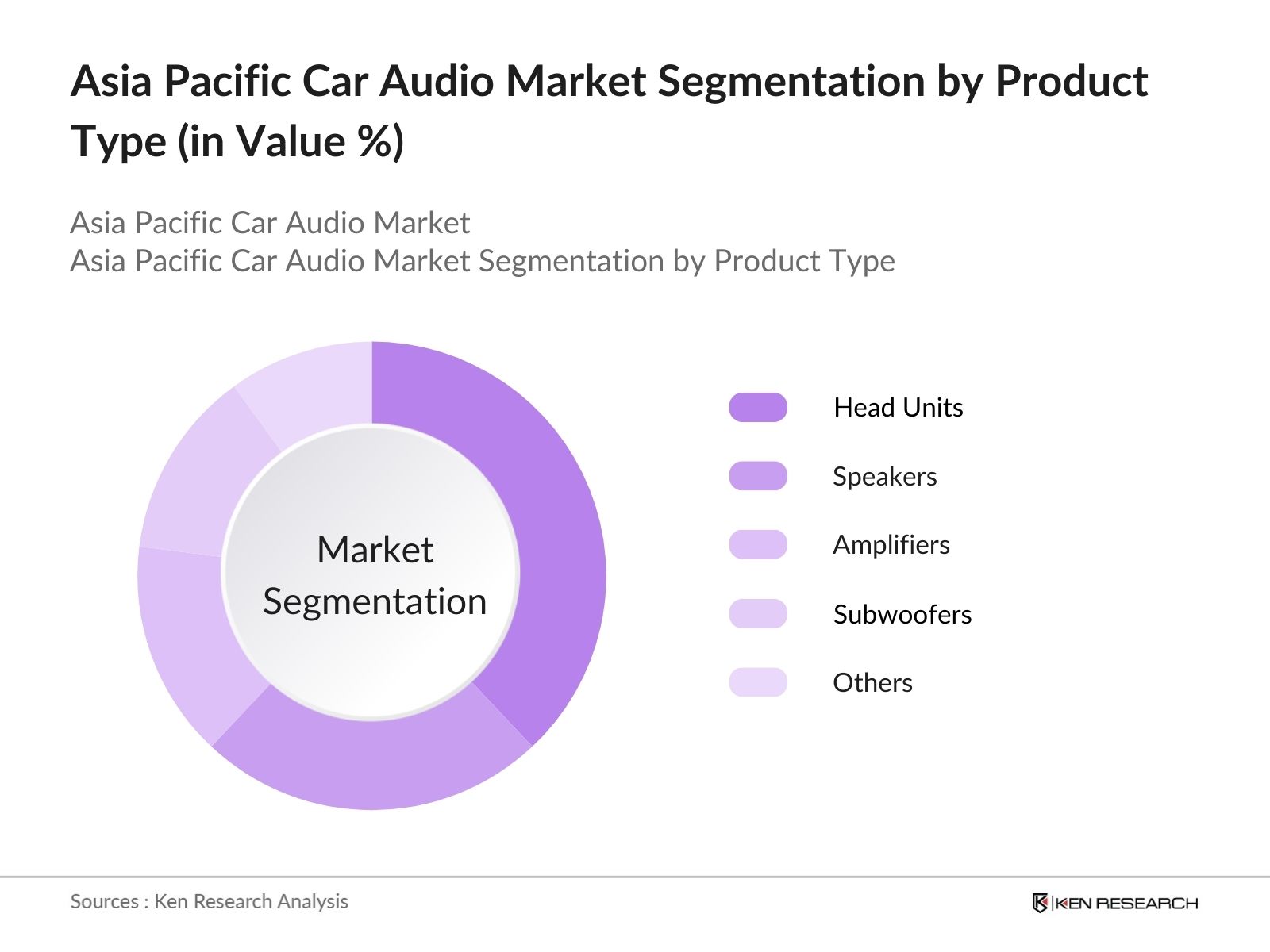

By Product Type: The Asia Pacific car audio market is segmented by product type into head units, speakers, amplifiers, subwoofers, and other components. Recently, head units have held a dominant market share in this segment due to their role as the control center of modern infotainment systems. These units are crucial for integrating wireless connectivity, voice assistants, and advanced navigation systems, making them a key component for both OEMs and aftermarket purchases. The demand for high-end infotainment in luxury and premium cars also contributes to the dominance of this segment.

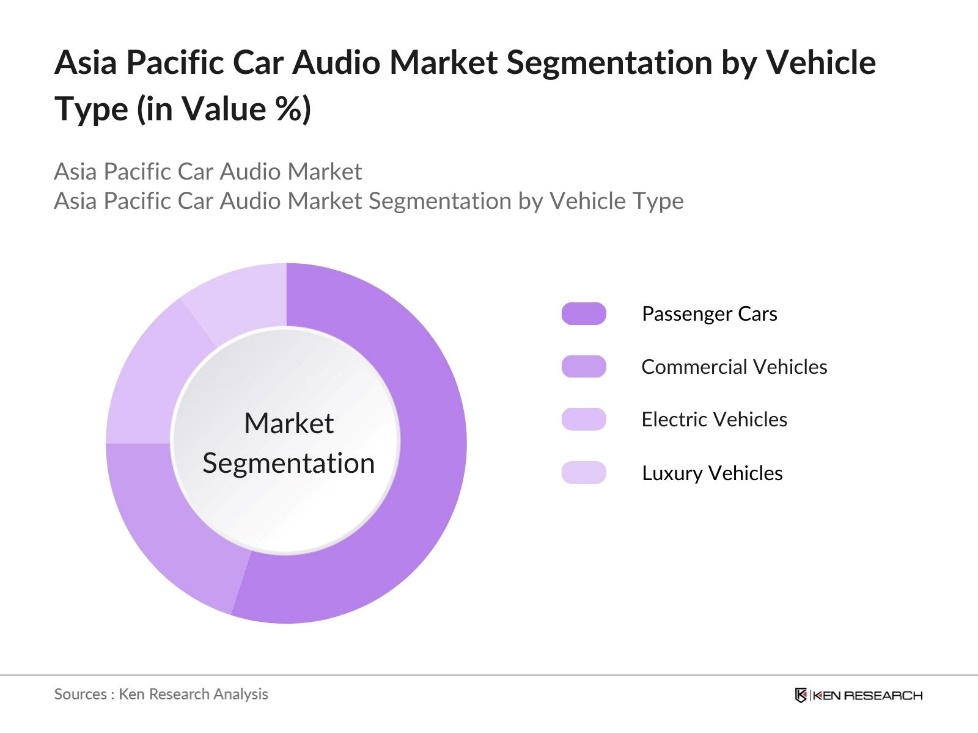

By Vehicle Type: The Asia Pacific car audio market is segmented by vehicle type into passenger cars, commercial vehicles, electric vehicles, and luxury vehicles. Passenger cars hold the dominant market share due to the sheer volume of production and sales across the region. The high rate of automobile ownership, especially in urban areas, and growing consumer interest in customized in-car entertainment drive the demand for car audio systems in this segment. Additionally, the expansion of the middle class in countries like China and India has increased consumer purchasing power, leading to higher demand for premium car audio solutions.

The market is dominated by a few major players, both regional and global. These companies hold significant market shares due to their strong partnerships with original equipment manufacturers (OEMs) and their robust R&D efforts in developing cutting-edge audio technologies. Many of these players have a long-established presence in the market, which has allowed them to build brand loyalty and dominate the industry.

|

Company Name |

Established Year |

Headquarters |

Product Range |

R&D Investment |

OEM Partnerships |

Technological Advancements |

Geographic Presence |

|

Panasonic Corporation |

1918 |

Osaka, Japan |

|||||

|

Pioneer Corporation |

1938 |

Tokyo, Japan |

|||||

|

Sony Corporation |

1946 |

Tokyo, Japan |

|||||

|

Harman International |

1980 |

Stamford, USA |

|||||

|

Alpine Electronics |

1967 |

Iwaki, Japan |

Over the next five years, the Asia Pacific car audio market is expected to witness substantial growth driven by the increased production of electric and autonomous vehicles. As consumer preferences shift towards more connected and personalized in-car experiences, there will be a greater demand for advanced audio systems with features such as 3D sound, voice command integration, and seamless smartphone connectivity.

|

Product Type |

Head Units Speakers Amplifiers Subwoofers Others (Antennas, Equalizers) |

|

Vehicle Type |

Passenger Cars Commercial Vehicles Electric Vehicles (EVs) Luxury Vehicles |

|

Technology |

Standard Audio Systems Premium Audio Systems Smart Audio Systems |

|

Sales Channel |

OEM Aftermarket |

|

Region |

China India Japan Australia South Korea |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers (Passenger vehicle production, Vehicle infotainment trends, Rising consumer demand for premium sound systems)

3.1.1. Increase in Vehicle Production

3.1.2. Rising Adoption of Advanced Infotainment Systems

3.1.3. Technological Advancements in Audio Systems

3.1.4. Consumer Preferences for Customizable Audio Systems

3.2. Market Challenges (Chip shortages, High manufacturing costs, Integration challenges with vehicle architectures)

3.2.1. Chip Supply Constraints

3.2.2. High Cost of Advanced Audio Systems

3.2.3. Complex Integration with Vehicle Electronics

3.3. Opportunities (Electric vehicle integration, Growing aftermarket demand, Rise in connected car technology)

3.3.1. Integration with Electric Vehicles

3.3.2. Aftermarket Opportunities in Emerging Markets

3.3.3. Rise of Connected Car Technologies

3.4. Trends (3D sound systems, Wireless audio solutions, Integration with voice assistants)

3.4.1. 3D Audio and Surround Sound Systems

3.4.2. Wireless and Bluetooth Audio Systems

3.4.3. Integration with AI and Voice-Controlled Systems

3.5. Government Regulation (Safety standards, Emission-related regulations affecting audio integration)

3.5.1. Government Mandates on In-car Audio Safety Features

3.5.2. Emission Regulations Influencing Vehicle Design and Audio System Integration

3.5.3. Standardization of Vehicle Audio Features

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

4.1. By Product Type (In Value %)

4.1.1. Head Units

4.1.2. Speakers

4.1.3. Amplifiers

4.1.4. Subwoofers

4.1.5. Others (Antennas, Equalizers)

4.2. By Vehicle Type (In Value %)

4.2.1. Passenger Cars

4.2.2. Commercial Vehicles

4.2.3. Electric Vehicles (EVs)

4.2.4. Luxury Vehicles

4.3. By Technology (In Value %)

4.3.1. Standard Audio Systems

4.3.2. Premium Audio Systems

4.3.3. Smart Audio Systems

4.4. By Sales Channel (In Value %)

4.4.1. OEM (Original Equipment Manufacturer)

4.4.2. Aftermarket

4.5. By Region (In Value %)

4.5.1. China

4.5.2. India

4.5.3. Japan

4.5.4. Australia

4.5.5. South Korea

5.1. Detailed Profiles of Major Companies

5.1.1. Panasonic Corporation

5.1.2. Pioneer Corporation

5.1.3. Sony Corporation

5.1.4. Harman International Industries

5.1.5. Alpine Electronics

5.1.6. Clarion Co., Ltd.

5.1.7. Kenwood Corporation

5.1.8. JVC

5.1.9. Bose Corporation

5.1.10. Bang & Olufsen Automotive

5.1.11. Continental AG

5.1.12. Voxx International Corporation

5.1.13. Clarion Corporation of America

5.1.14. Denso Corporation

5.1.15. Fujitsu Ten

5.2. Cross Comparison Parameters (Revenue, Employees, Market Share, Product Portfolio, Geographic Presence, Recent Developments, Investments, Technology Focus)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7 Venture Capital Funding

5.8 Private Equity Investments

6.1. Automotive Safety Standards

6.2. Audio System Regulations in Vehicles

6.3. Certification Processes for In-Car Audio Systems

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Product Type (In Value %)

8.2. By Vehicle Type (In Value %)

8.3. By Technology (In Value %)

8.4. By Sales Channel (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

The first step involves mapping the key stakeholders in the Asia Pacific car audio market. This is done through extensive desk research, relying on secondary sources and proprietary databases to gather data on the major influencing factors. Critical variables such as vehicle production rates, consumer spending trends, and technological developments are identified in this phase.

In this step, historical data for the Asia Pacific car audio market is compiled and analyzed. This includes the number of vehicles equipped with advanced audio systems, the ratio of aftermarket versus OEM sales, and the revenue generation within the sector. The analysis helps estimate the current market size.

Market hypotheses are then tested through expert consultations, including interviews with senior executives from leading car audio manufacturers. These interviews help validate the gathered data and provide deeper insights into trends and challenges in the market.

The final phase synthesizes all the data gathered and outputs a comprehensive report that includes detailed analysis of product segments, consumer preferences, and market challenges. This ensures that the final output is accurate and provides actionable insights for market stakeholders.

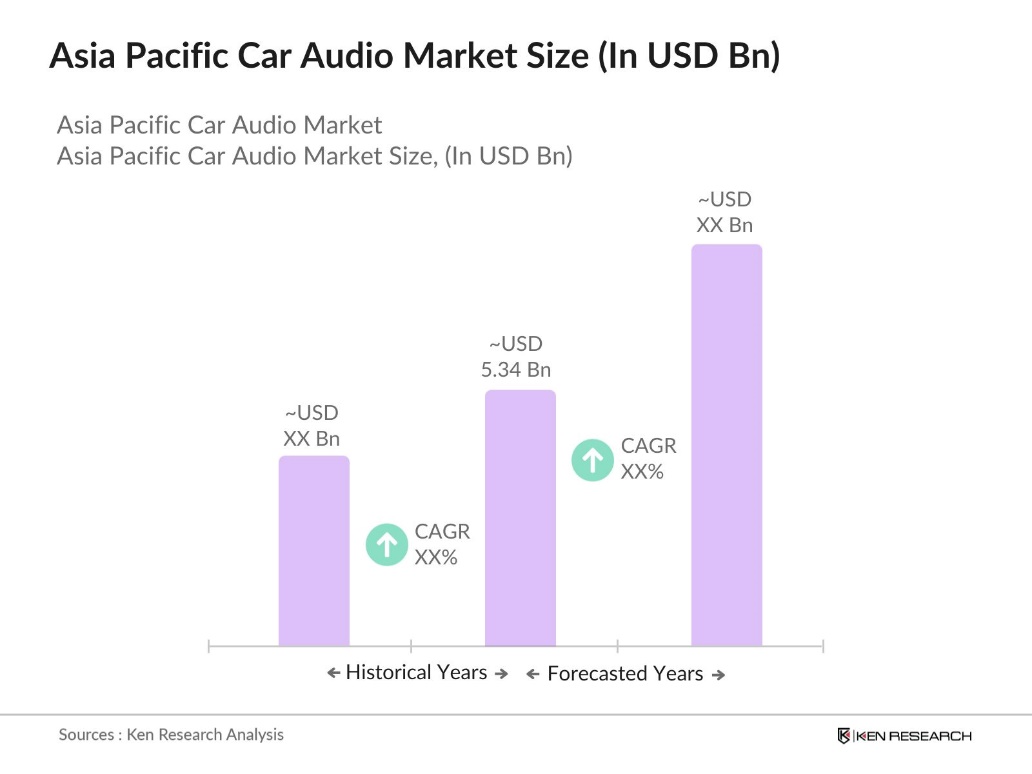

The Asia Pacific Car Audio Market is valued at USD 5.34 billion, driven by increasing vehicle production and consumer demand for high-quality audio systems, particularly in passenger cars and electric vehicles.

Challenges in Asia Pacific Car Audio Market include chip shortages, which have disrupted the supply of key components, and high manufacturing costs for advanced audio systems. Additionally, integrating complex audio systems with modern vehicle electronics remains a hurdle for manufacturers.

Major players in Asia Pacific Car Audio Market include Panasonic Corporation, Pioneer Corporation, Sony Corporation, Harman International, and Alpine Electronics, all of which have established strong partnerships with OEMs and a significant presence in the market.

Growth drivers in Asia Pacific Car Audio Market include the rising production of electric and autonomous vehicles, increasing consumer demand for premium in-car entertainment, and advancements in wireless and AI-based audio technologies.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.