Asia-Pacific Connected Cars Market Outlook to 2030

Region:Asia

Author(s):Abhinav kumar

Product Code:KROD6388

November 2024

98

About the Report

Asia-Pacific Connected Cars Market Overview

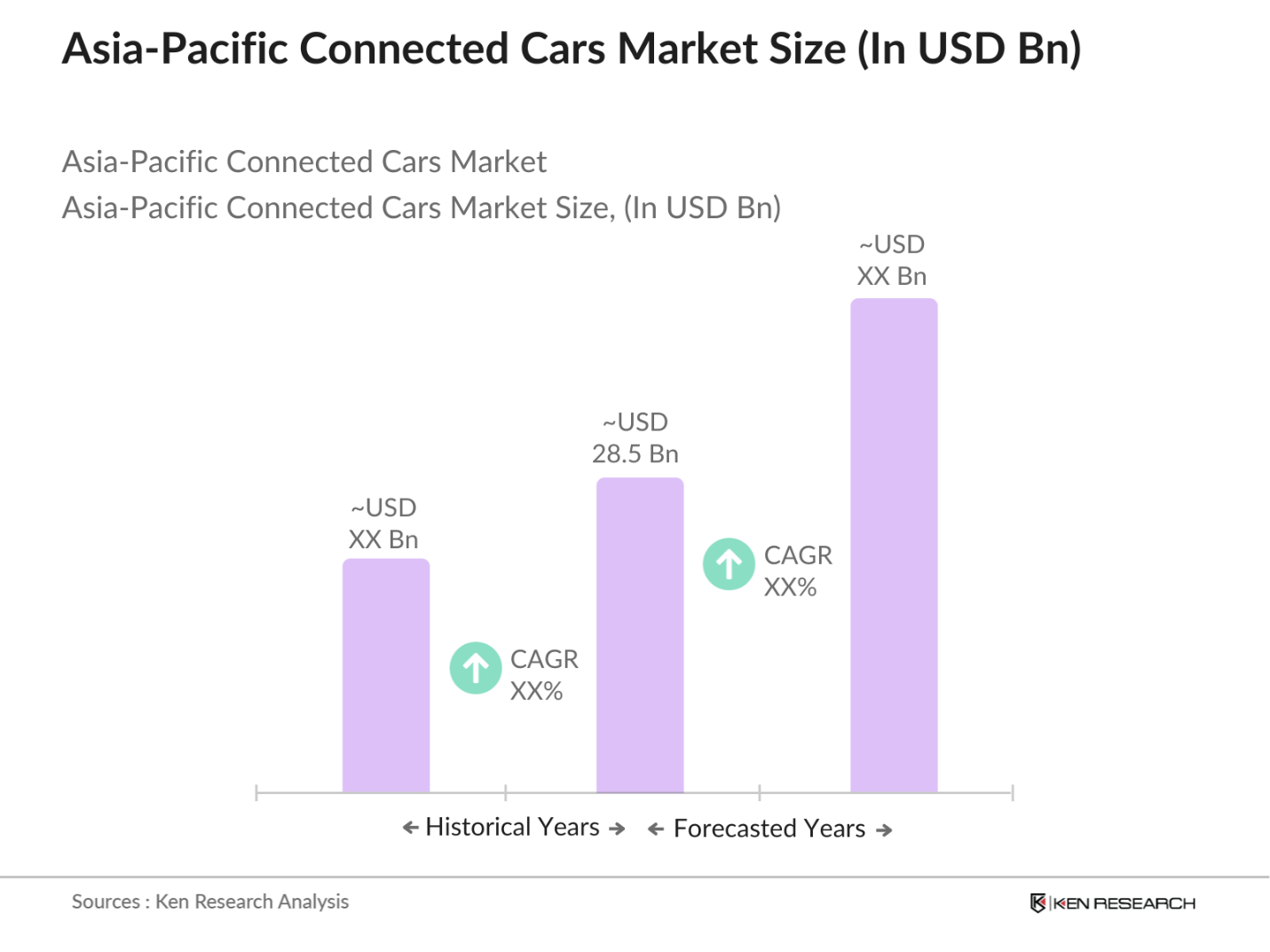

- The Asia-Pacific connected cars market, valued at approximately USD 28.5 billion, is primarily driven by rapid advancements in vehicle connectivity technologies such as V2X (Vehicle-to-Everything) communication and 5G integration. This growth is attributed to increasing consumer demand for safer, more efficient, and tech-enabled vehicles. Additionally, automakers are capitalizing on the region's high vehicle demand to expand their connected solutions portfolios. Increased urbanization and the demand for enhanced in-car experience also contribute to the adoption of connected car technologies in this region.

- Countries like China, Japan, and South Korea lead the Asia-Pacific connected cars market due to their established automotive industries, supportive government policies, and widespread technology adoption. China, for example, has prioritized 5G and smart infrastructure, enabling faster rollout of connected cars. Meanwhile, Japans strong automotive and electronics sectors facilitate rapid technological integration, positioning it as a key market for connected car developments.

- Governmentacific are establishing strict data privacy regulations to protect vehicle users' information. The Personal Data Protection Act in Singapore mandates automakers to comply with stringent data handling standards, impacting approximately 200,000 connected vehicles. Similarly, Japan and South Koreas data privacy laws require connected car data to be encrypted, addressing consumer concerns. These regulations aim to build trust among users by safeguarding their data within connected vehicle networks .

Asia-Pacific Connected Cars Market Segmentation

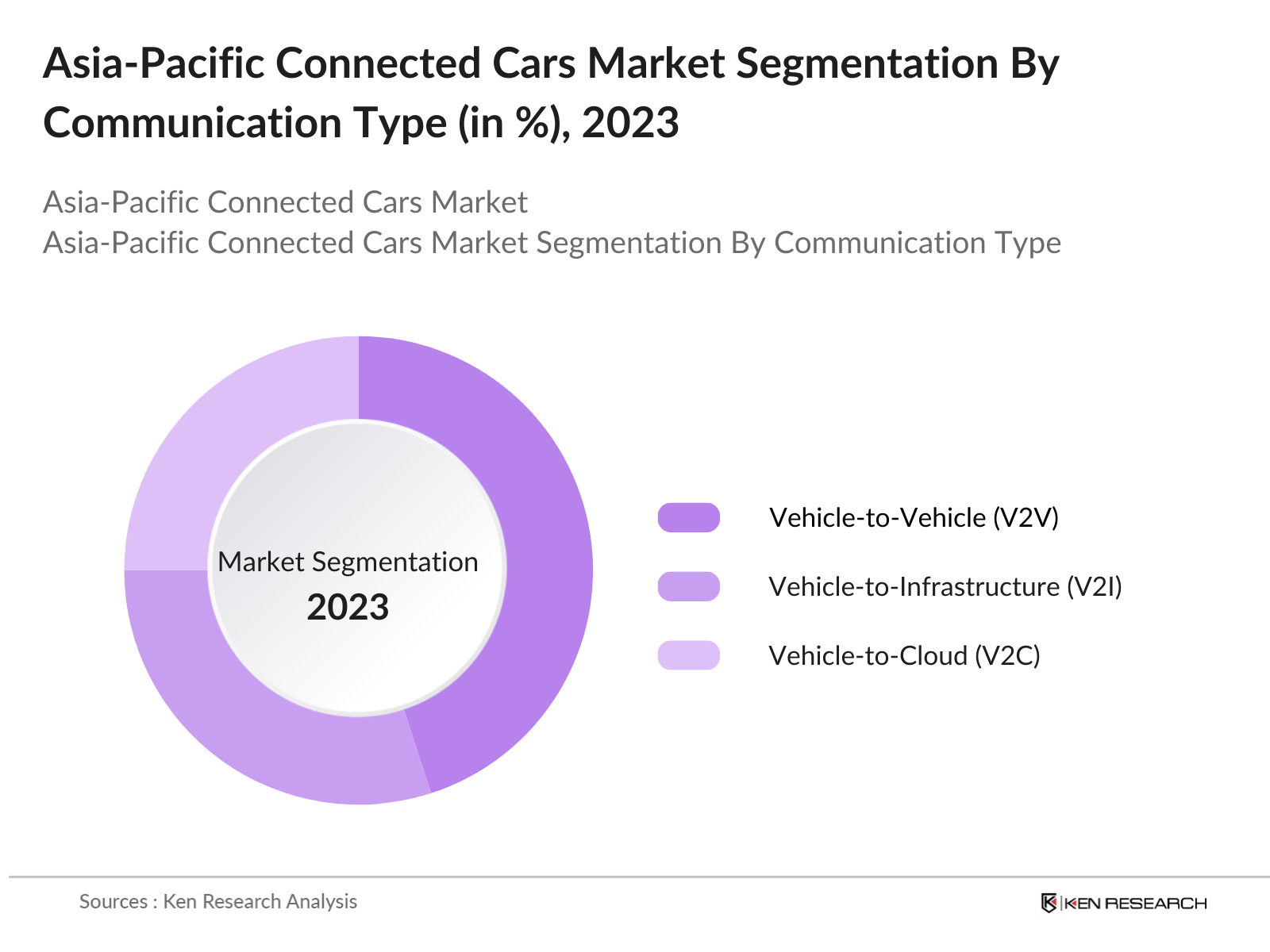

By Communication Type: The Asia-Pacific connected cars market is segmented by communication type into Vehicle-to-Vehicle (V2V), Vehicle-to-Infrastructure (V2I), and Vehicle-to-Cloud (V2C) communications. Recently, V2V communication has dominated the market due to its critical role in ensuring on-road safety through real-time data exchange between vehicles. V2V technologies facilitate collision warnings and cooperative adaptive cruise control, thus enhancing traffic flow and reducing accident risks. The increasing focus on safety standards and the potential for V2V integration into Advanced Driver Assistance Systems (ADAS) bolster the segments dominance.

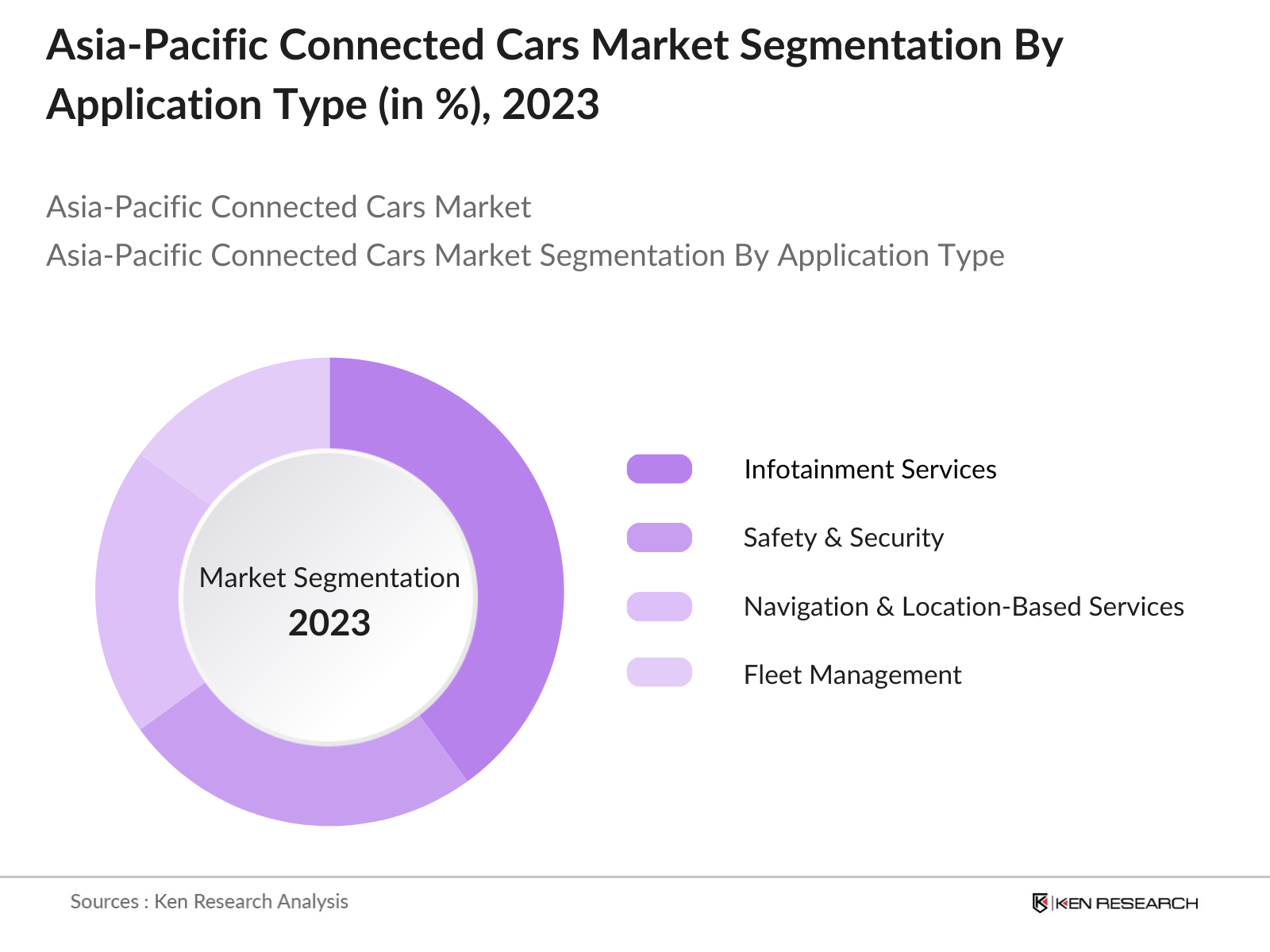

By Application: The market is further segmented by application into Infotainment Services, Safety & Security, Navigation & Location-Based Services, and Fleet Management. Infotainment services hold a significant share in this segment, driven by rising consumer expectations for enhanced in-car digital experiences, including streaming media, gaming, and integrated digital assistant functions. This trend is further supported by growing 5G adoption, which enhances connectivity speed, allowing real-time entertainment and user interaction. Major OEMs are collaborating with tech firms to provide integrated infotainment solutions, underscoring the segments growth.

Asia-Pacific Connected Cars Market Competitive Landscape

The Asia-Pacific connected cars market is dominated by a mix of global automotive giants and local technology firms, creating a robust competitive environment. Major players such as Toyota, Honda, Hyundai, and Nissan are leading market developments, leveraging partnerships and innovation in connected car technologies. The competition highlights the importance of investment in R&D and strategic partnerships with tech firms.

Asia-Pacific Connected Cars Industry Analysis

Growth Drivers

- Vehicle Connectivity Advancements: Vehicle connectivity, primarily through telematics and Vehicle-to-Everything (V2X) communication, is transforming Asia-Pacifics connected cars market. By 2024, the regions transportation infrastructure has seen a significant upgrade, with more than 20,000 intelligent transport systems installed, bolstering V2X communication channels. Notably, in countries like Japan, 40% of newly manufactured vehicles now integrate telematics solutions that aid in navigation, traffic management, and safety alerts. The focus on connectivity has driven manufacturers to invest over $5 billion in V2X and telematics advancements, supported by government incentives in smart transportation

- Adoption of 5G Network: The rollout of 5G across Asia-Pacific plays a pivotal role in enabling connected vehicle functionalities. China has led this movement, deploying more than 2.3 million 5G base stations as of 2023, making real-time data transfer for connected vehicles feasible. In South Korea, 5G-enabled automotive applications contribute to reduced latency in vehicle-to-infrastructure communication, enhancing safety. Japans initiatives to expand 5G coverage to over 90% of the urban population ensure vehicles maintain continuous connectivity, contributing to an increasingly responsive and safe connected vehicle ecosystem .

- Increase Demand for Safety Features: Consumer demand for safety-centric connected features in vehicles is soaring across Asia-Pacific, with nearly 70% of urban car buyers in countries like China and Japan seeking vehicles equipped with ADAS (Advanced Driver Assistance Systems). The focus on safety has led the Japanese government to mandate the integration of lane-keeping assist and automatic braking in new vehicles, aligning with consumer preferences. This increased demand for safety-enhanced vehicles is influencing automakers to integrate advanced connectivity features, strengthening the market for connected cars in Asia-Pacific.

Market Challenges

- Data Privacy Concerns: Data privacy remains a challenge in the connected cars market, as data collection and sharing increase within connected vehicles. The Personal Information Protection Commission (PIPC) in Japan reported that over 50 million vehicles in Asia-Pacific are connected, raising significant privacy concerns among consumers. Consequently, governments, including South Koreas Ministry of Science and ICT, are imposing stricter regulations on data usage in connected vehicles, complicating manufacturers' compliance efforts. Addressing these privacy issues while maintaining data-driven functionality presents a significant hurdle for market participants.

- High Implementation Costs: High Implementation costs associated with implementing connected vehicle technology continue to restrain market expansion. According to the Japanese Ministry of Land, Infrastructure, Transport, and Tourism, advanced telematics and V2X systems require investments exceeding $10,000 per vehicle. Developing economies within Asia-Pacific, such as Thailand and Indonesia, face challenges in adopting these technologies due to budget constraints, creating a divide in market readiness across the region. The substantial financial outlay limits connected vehicle deployment, particularly in cost-sensitive markets.

Asia-Pacific Connected Cars Market Future Outlook

Over the next few years, the Asia-Pacific connected cars market is expected to witness substantial growth driven by increasing vehicle digitization, government support for 5G expansion, and growing demand for advanced driver assistance and safety systems. The push towards sustainable transportation solutions, coupled with the integration of AI in vehicles, is likely to drive significant investments and innovation in connected car technologies.

Opportunities

- Development of Autonomous Vehicles: Autonomous driving, backed by ADAS integration, represents a promising opportunity for connected cars in Asia-Pacific. Japan leads in the adoption of Level 2 and Level 3 autonomous vehicles, with over 2 million such vehicles expected on the roads by the end of 2024. These advancements align with initiatives by the Japanese and South Korean governments, both setting targets to expand autonomous vehicle numbers as part of their transport modernization plans. The synergy between autonomy and connectivity accelerates innovation, offering growth potential in the market.

- Expansion of Fleet Management Solutions: Fleet solutions in Asia-Pacific are increasingly adopting connected vehicle technology. The Australian transport sector reports that over 70% of commercial vehicles utilize telematics for real-time tracking, route optimization, and safety monitoring. Demand for these solutions has surged across logistics-heavy economies like India and China, where fleet management efficiency is crucial. The integration of connectivity and telematics in fleet management solutions offers substantial opportunities for operational optimization, particularly in urban centers.

Scope of the Report

|

By Product Type |

Embedded Systems Tethered Systems Integrated Systems |

|

By Communication Type |

Vehicle-to-Vehicle (V2V) Vehicle-to-Infrastructure (V2I) Vehicle-to-Cloud (V2C) |

|

By Connectivity Solutions |

3G/4G Connectivity 5G Connectivity Dedicated Short Range Communication (DSRC) |

|

By Application |

Infotainment Services Safety & Security Navigation & Location-Based Service Fleet Management |

|

By Region |

China Japan India South Korea Australia |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Automotive OEMs and Manufacturing Companies

Telecommunication Companies

Government and Regulatory Bodies (e.g., Ministry of Industry and Information Technology of China, Road Transport Authority of India)

Connected Car Technology Provider Companies

Autonomous Driving Startup Companies

Investor and Venture Capitalist Firms

Cloud Service Provider Companies

Fleet Management Companies

Companies

Players Mentioned in the Report

Toyota Motor Corporation

Hyundai Motor Company

Honda Motor Co. Ltd.

Nissan Motor Corporation

Tata Motors

Mahindra & Mahindra Ltd.

BYD Auto Co. Ltd.

SAIC Motor Corporation

Changan Automobile

Geely Auto

Table of Contents

1. Asia-Pacific Connected Cars Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Asia-Pacific Connected Cars Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Asia-Pacific Connected Cars Market Analysis

3.1. Growth Drivers

3.1.1. Vehicle Connectivity Advancements (Telematics, V2X Communication)

3.1.2. Adoption of 5G Networks

3.1.3. Government Initiatives (Smart Cities, Infrastructure Improvements)

3.1.4. Increasing Consumer Demand for Safety Features

3.2. Market Challenges

3.2.1. Data Privacy Concerns

3.2.2. High Implementation Costs

3.2.3. Cybersecurity Threats in Connected Vehicles

3.3. Opportunities

3.3.1. Development of Autonomous Vehicles (ADAS Integration)

3.3.2. Expansion of Fleet Management Solutions

3.3.3. Collaborations between Automakers and Tech Giants

3.4. Trends

3.4.1. Integration of AI and Machine Learning

3.4.2. Increased Use of OTA (Over-the-Air) Software Updates

3.4.3. Rise of Subscription-Based Models for Connected Services

3.5. Government Regulations

3.5.1. Regulatory Standards for Vehicle Data Privacy

3.5.2. Government Programs Promoting Electric Vehicles (EVs)

3.5.3. Vehicle Safety Mandates (ADAS Systems)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.7.1. Automotive OEMs (Original Equipment Manufacturers)

3.7.2. Telecommunication Providers

3.7.3. Software Developers (IoT, AI Providers)

3.8. Porters Five Forces

3.9. Competition Ecosystem

4. Asia-Pacific Connected Cars Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Embedded Systems

4.1.2. Tethered Systems

4.1.3. Integrated Systems

4.2. By Communication Type (In Value %)

4.2.1. Vehicle-to-Vehicle (V2V)

4.2.2. Vehicle-to-Infrastructure (V2I)

4.2.3. Vehicle-to-Cloud (V2C)

4.3. By Connectivity Solutions (In Value %)

4.3.1. 3G/4G Connectivity

4.3.2. 5G Connectivity

4.3.3. Dedicated Short Range Communication (DSRC)

4.4. By Application (In Value %)

4.4.1. Infotainment Services

4.4.2. Safety & Security

4.4.3. Navigation & Location-Based Services

4.4.4. Fleet Management

4.5. By Region (In Value %)

4.5.1. China

4.5.2. Japan

4.5.3. India

4.5.4. South Korea

4.5.5. Australia

5. Asia-Pacific Connected Cars Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Continental AG

5.1.2. Denso Corporation

5.1.3. Harman International Industries

5.1.4. Bosch Mobility Solutions

5.1.5. Qualcomm Technologies

5.1.6. Cisco Systems

5.1.7. NXP Semiconductors

5.1.8. Intel Corporation

5.1.9. Panasonic Automotive Systems

5.1.10. LG Electronics

5.1.11. Samsung Electronics

5.1.12. Huawei Technologies Co. Ltd.

5.1.13. Tata Motors

5.1.14. Mahindra & Mahindra Ltd.

5.1.15. BYD Auto Co. Ltd.

5.2. Cross Comparison Parameters (Revenue, Connectivity Solutions Portfolio, R&D Investment, Number of Vehicles Connected, Collaborations)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. Asia-Pacific Connected Cars Market Regulatory Framework

6.1. Vehicle Safety Regulations

6.2. Data Privacy Laws

6.3. EV and Emission Regulations

7. Asia-Pacific Connected Cars Future Market Size (In USD Mn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Asia-Pacific Connected Cars Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Communication Type (In Value %)

8.3. By Connectivity Solutions (In Value %)

8.4. By Application (In Value %)

8.5. By Region (In Value %)

9. Asia-Pacific Connected Cars Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The initial phase involved mapping out the key stakeholders within the Asia-Pacific connected cars ecosystem. This was achieved through extensive desk research utilizing multiple secondary databases and proprietary resources to capture a comprehensive view of the industrys dynamics.

Step 2: Market Analysis and Construction

We gathered and analyzed historical data related to market penetration, focusing on metrics such as vehicle connectivity solutions, communication types, and revenue generation. Additionally, market-specific quality standards were assessed to ensure the accuracy and reliability of revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

We developed market hypotheses, which were validated through in-depth interviews with industry experts representing various automotive, technology, and telecommunication companies. These discussions provided operational and strategic insights crucial for refining market data.

Step 4: Research Synthesis and Final Output

In the final stage, we engaged with connected car OEMs to gather insights into product segments, customer preferences, and sales performance. These findings were used to validate data obtained through bottom-up research, ensuring a well-rounded analysis of the Asia-Pacific connected cars market.

Frequently Asked Questions

01. How big is the Asia-Pacific Connected Cars Market?

The Asia-Pacific connected cars market is valued at approximately USD 28.5 billion, driven by advancements in 5G and V2X communication technologies that enable seamless connectivity and real-time data exchange.

02. What challenges does the Asia-Pacific Connected Cars Market face?

The market encounters challenges such as cybersecurity risks, high implementation costs, and regulatory complexities concerning data privacy, which can hinder the widespread adoption of connected car technologies.

03. Who are the major players in the Asia-Pacific Connected Cars Market?

Major players include Toyota Motor Corporation, Hyundai Motor Company, Honda Motor Co. Ltd., Nissan Motor Corporation, and Tata Motors. These companies dominate due to their extensive portfolios and strong regional presence.

04. What are the growth drivers of the Asia-Pacific Connected Cars Market?

Key drivers include the rise of 5G networks, consumer demand for in-car digital experiences, and government initiatives supporting smart infrastructure and vehicle safety across the region.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.