Asia Pacific Electric Vehicle Charger Market Outlook to 2030

Region:Asia

Author(s):Meenakshi Bisht

Product Code:KROD5832

December 2024

94

About the Report

Asia Pacific Electric Vehicle Charger Market Overview

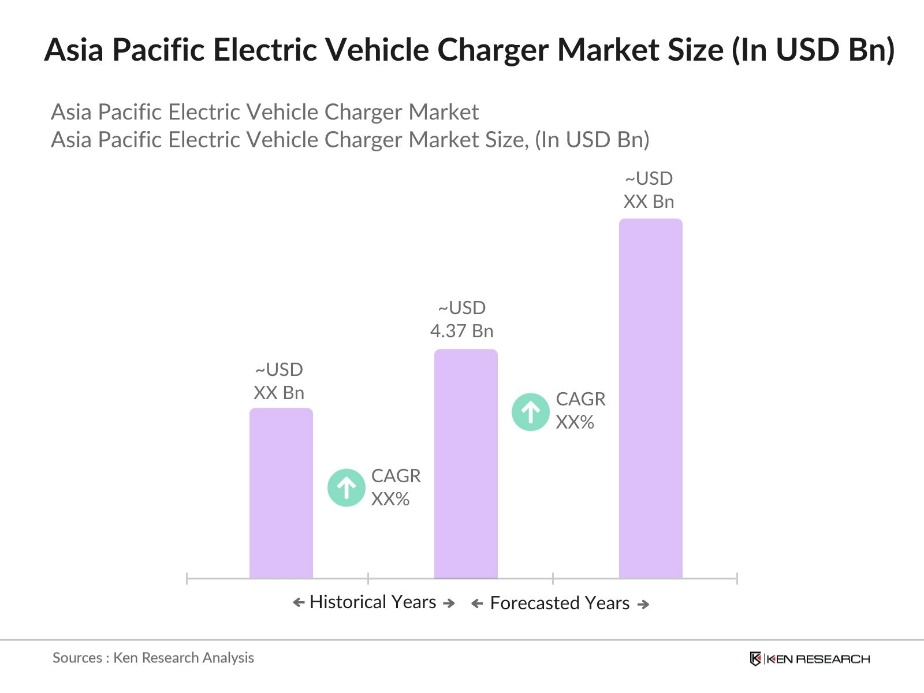

- The Asia Pacific Electric Vehicle (EV) Charger Market is valued at USD 4.37 billion, driven by the rapid growth in electric vehicle adoption and supportive government policies. Several countries in the region have implemented strict emission regulations, offering subsidies and incentives to promote the use of electric vehicles, which in turn propels the demand for charging infrastructure.

- The dominant markets in the Asia Pacific region include China, Japan, and South Korea. China leads the market due to its expansive electric vehicle production capacity, significant government investments in EV infrastructure, and policies encouraging EV adoption. Japans dominance is attributed to its advancements in battery technologies and its established automotive sector. South Korea follows due to substantial investments in R&D and smart city initiatives, making these countries leaders in both EV manufacturing and infrastructure development.

- In 2023, the Australian government partnered with NRMA to build a nationwide EV fast-charging network. The initiative involves setting up 117 fast-charging stations across major highways, including rural areas. This project, supported by a $78.6 million funding commitment, aims to address "black spots" in EV charging availability, ensuring chargers are placed every 150 km on highways. The government allocated $39.3 million to the project, contributing to the larger $500 million "Driving the Nation" program aimed at supporting electric vehicle infrastructure.

Asia Pacific Electric Vehicle Charger Market Segmentation

By Charger Type: The Asia Pacific Electric Vehicle Charger market is segmented by charger type into AC Chargers, DC Fast Chargers, and Wireless Chargers. AC chargers hold a dominant market share due to their lower costs and extensive use in residential applications. These chargers are preferred for home installations as they are easy to install and provide a cost-effective solution for consumers who typically charge their EVs overnight. As residential adoption of electric vehicles increases, the demand for AC chargers continues to grow.

By Application: The Asia Pacific Electric Vehicle Charger market is segmented by application into Residential Charging, Commercial Charging, and Public Charging. Public charging infrastructure is dominating the market due to significant government investments and partnerships with private companies to establish nationwide networks. Public charging stations provide convenience for long-distance travelers and are increasingly integrated into urban centers and along highways, enabling rapid expansion of electric vehicle usage.

Asia Pacific Electric Vehicle Charger Market Competitive Landscape

The market is highly consolidated with key players such as ABB Ltd., Delta Electronics Inc., and Siemens AG leading the charge. These companies dominate the market through partnerships with governments, offering end-to-end solutions for charging infrastructure. Additionally, new entrants in the wireless charging space are challenging traditional players, pushing innovation further. Strategic partnerships between automakers and charger manufacturers have also enhanced market growth.

|

Company Name |

Establishment Year |

Headquarters |

Charger Network Size |

R&D Investment |

Strategic Partnerships |

Market Penetration |

Key Patents |

Global Footprint |

|

ABB Ltd. |

1883 |

Switzerland |

||||||

|

Delta Electronics Inc. |

1971 |

Taiwan |

||||||

|

Siemens AG |

1847 |

Germany |

||||||

|

BYD Company Ltd. |

1995 |

China |

||||||

|

Tesla Inc. |

2003 |

USA |

Asia Pacific Electric Vehicle Charger Industry Analysis

Growth Drivers

- Increased Electric Vehicle Sales: Electric vehicle (EV) sales in the Asia-Pacific region have seen a significant surge due to heightened demand from key markets like China, Japan, and South Korea. The number of new electric vehicle registrations in China reached 8.1 million in 2023, reflecting a 35% increase compared to 2022. This growing adoption of EVs has, in turn, increased the demand for EV chargers to support the expanding fleet of electric cars.

- Government Subsidies and Incentives for EV Infrastructure: Governments across Asia-Pacific have been actively incentivizing EV infrastructure development through subsidies and tax rebates. For instance, In September 2023, the China Electric Vehicle Charging Infrastructure Promotion Alliance (EVCIPA) reported that around 61,000 public charging stations were installed in August 2023. This represents a 39.9% increase compared to the same month in 2022.

- Urbanization and Smart City Initiatives: Rapid urbanization across the Asia-Pacific region has become a significant driver for electric vehicle (EV) adoption, which in turn boosts the demand for EV charging infrastructure. Major cities such as Singapore, Tokyo, and Seoul have been actively implementing smart city initiatives that prioritize the integration of EV charging systems within public spaces, commercial areas, and residential complexes. These urban plans aim to support both personal and public transportation needs by ensuring convenient access to charging stations, thereby enhancing the feasibility of owning and operating electric vehicles in densely populated areas.

Market Challenges

- Installation and Maintenance Costs: The high costs associated with setting up and maintaining EV charging stations remain a significant challenge in the Asia-Pacific region. Establishing fast-charging stations often requires substantial capital investment, which can create financial barriers for businesses, particularly small and medium-sized enterprises (SMEs), looking to enter the EV infrastructure market. Additionally, ongoing maintenance costs further increase the financial burden, making it harder for operators to sustain and expand their charging networks.

- Compatibility Issues Across Different Charger Brands: Compatibility issues across various EV charger brands present another hurdle in the region's EV infrastructure development. Different countries and manufacturers often use distinct charging standards, which complicates the installation and operation of charging stations. The lack of a unified standard across nations makes it challenging for operators to ensure compatibility across various EV models, leading to inefficiencies in deployment and maintenance for charging network providers.

Asia Pacific Electric Vehicle Charger Market Future Outlook

The Asia Pacific Electric Vehicle Charger market is expected to witness robust growth in the coming years. Key factors driving this growth include increasing electric vehicle adoption rates, government initiatives supporting eco-friendly transportation, and advancements in charging technology, particularly in wireless and ultra-fast charging. The continued investment in public charging networks and the integration of renewable energy into the grid are likely to further expand market opportunities.

Market Opportunities

- Growth in Public Charging Infrastructure: The Asia-Pacific region has been experiencing a steady expansion of public EV charging infrastructure, driven by increasing demand for electric vehicles. Governments and private companies have been investing in charging networks, particularly in urban areas and high-density regions. This growth in public charging infrastructure presents a substantial opportunity for further development, as more charging stations are required to support the rising number of electric vehicles on the roads. These developments create a favorable environment for continued investment in EV infrastructure.

- Rising EV Penetration in Emerging Markets: Emerging markets across the Asia-Pacific, such as Indonesia and Thailand, are seeing a growing adoption of electric vehicles. This shift toward electric mobility is creating new opportunities for expanding EV charging networks in these countries. With their current charging infrastructure still in the early stages of development, these markets are poised for significant growth as governments and private entities invest in building a comprehensive charging ecosystem to support the increasing number of electric vehicles.

Scope of the Report

|

Charger Type |

AC Chargers DC Fast Chargers Wireless Chargers |

|

Application |

Residential Charging Commercial Charging Public Charging |

|

Connector Type |

Type 1 (J1772) Type 2 (Mennekes) CHAdeMO CCS |

|

Charging Power |

Up to 11 kW 11 kW to 50 kW Above 50 kW |

|

Region |

China Japan South Korea Australia Southeast Asia |

Products

Key Target Audience

Parking Lot Management Companies

Construction Companies

Electric Utility Companies

Logistics and Delivery Companies

Renewable Energy Companies

Government and Regulatory Bodies (e.g., Ministry of Transport, Energy Regulatory Commission)

Investors and venture capital Firms

Banks and Financial Institutions

Companies

Players Mentioned in the Report

ABB Ltd.

Delta Electronics Inc.

Siemens AG

BYD Company Ltd.

Tesla Inc.

Schneider Electric

Hyundai Motor Group

BP Chargemaster

Enel X

EVgo Services LLC

Table of Contents

1. Asia Pacific Electric Vehicle Charger Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Asia Pacific Electric Vehicle Charger Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Asia Pacific Electric Vehicle Charger Market Analysis

3.1. Growth Drivers (Electric Vehicle Adoption Rate, Government Incentives, Charging Infrastructure)

3.1.1. Increased Electric Vehicle Sales

3.1.2. Government Subsidies and Incentives for EV Infrastructure

3.1.3. Urbanization and Smart City Initiatives

3.1.4. Technological Advancements in Charger Systems

3.2. Market Challenges (High Initial Setup Costs, Limited Range of Charging Stations)

3.2.1. Installation and Maintenance Costs

3.2.2. Compatibility Issues Across Different Charger Brands

3.2.3. Slow Adoption in Rural Areas

3.3. Opportunities (Expansion of Fast-Charging Network, Partnerships with Automakers)

3.3.1. Growth in Public Charging Infrastructure

3.3.2. Rising EV Penetration in Emerging Markets

3.3.3. Integration with Renewable Energy Sources

3.4. Trends (Adoption of Wireless Charging, Increasing Investment in R&D)

3.4.1. Wireless Charging Systems Development

3.4.2. Transition Towards Ultra-Fast Charging Stations

3.4.3. Collaboration Between Charging Network Providers and Automotive Manufacturers

3.5. Government Regulations (EV Policies, Charging Infrastructure Standards)

3.5.1. Regional EV Policies and Mandates

3.5.2. Subsidies for Charging Infrastructure Installation

3.5.3. National Energy Efficiency Plans and Emission Targets

3.6. SWOT Analysis (Strengths, Weaknesses, Opportunities, Threats)

3.7. Stakeholder Ecosystem (Manufacturers, Charging Network Operators, EV Manufacturers)

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

4. Asia Pacific Electric Vehicle Charger Market Segmentation

4.1. By Charger Type (In Value %)

4.1.1. AC Chargers

4.1.2. DC Fast Chargers

4.1.3. Wireless Chargers

4.2. By Application (In Value %)

4.2.1. Residential Charging

4.2.2. Commercial Charging

4.2.3. Public Charging

4.3. By Connector Type (In Value %)

4.3.1. Type 1 (J1772)

4.3.2. Type 2 (Mennekes)

4.3.3. CHAdeMO

4.3.4. CCS

4.4. By Charging Power (In Value %)

4.4.1. Up to 11 kW

4.4.2. 11 kW to 50 kW

4.4.3. Above 50 kW

4.5. By Region (In Value %)

4.5.1. China

4.5.2. Japan

4.5.3. South Korea

4.5.4. Australia

4.5.5. Southeast Asia

5. Asia Pacific Electric Vehicle Charger Market Competitive Analysis

5.1. Detailed Profiles of Major Competitors

5.1.1. ABB Ltd

5.1.2. Delta Electronics Inc.

5.1.3. Siemens AG

5.1.4. Schneider Electric

5.1.5. Tesla Inc.

5.1.6. BYD Company Ltd.

5.1.7. BP Chargemaster

5.1.8. Shell New Energies

5.1.9. ChargePoint Inc.

5.1.10. Enel X

5.1.11. Hyundai Motor Group

5.1.12. EVgo Services LLC

5.1.13. TGOOD Global Ltd.

5.1.14. Eaton Corporation

5.1.15. Blink Charging Co.

5.2. Cross Comparison Parameters (Charger Network Size, Market Share, R&D Investment, EV Partnerships)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers And Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. Asia Pacific Electric Vehicle Charger Market Regulatory Framework

6.1. Government Policies for EV Charger Installations

6.2. Compliance Requirements for Charger Providers

6.3. Certification and Licensing Processes

7. Asia Pacific Electric Vehicle Charger Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Asia Pacific Electric Vehicle Charger Future Market Segmentation

8.1. By Charger Type (In Value %)

8.2. By Application (In Value %)

8.3. By Connector Type (In Value %)

8.4. By Charging Power (In Value %)

8.5. By Region (In Value %)

9. Asia Pacific Electric Vehicle Charger Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The research begins with identifying the key variables influencing the Asia Pacific Electric Vehicle Charger market. This involves extensive secondary research through government publications, automotive reports, and EV infrastructure databases to map stakeholders and define core market dynamics.

Step 2: Market Analysis and Construction

We gather and assess historical data to analyze market penetration and EV adoption across the region. The goal is to construct a comprehensive market model by evaluating key revenue generators, infrastructure development, and the competitive landscape.

Step 3: Hypothesis Validation and Expert Consultation

Expert consultations through computer-assisted interviews with major market players provide insights into operational challenges, sales performance, and future growth projections. This step helps refine the data and validate the market hypotheses.

Step 4: Research Synthesis and Final Output

Final research outputs are produced through the synthesis of secondary research and expert interviews. These outputs include detailed insights on key market segments, growth trends, regulatory impacts, and competitive strategies, ensuring a robust and reliable analysis of the Asia Pacific Electric Vehicle Charger market.

Frequently Asked Questions

01. How big is the Asia Pacific Electric Vehicle Charger Market?

The Asia Pacific Electric Vehicle Charger Market is valued at USD 4.37 billion, supported by government initiatives, increasing electric vehicle adoption, and investments in public and private charging infrastructure.

02. What are the challenges in the Asia Pacific Electric Vehicle Charger Market?

Challenges in Asia Pacific Electric Vehicle Charger Market include high installation costs, slow adoption in rural areas, and compatibility issues across different charger brands, limiting the widespread deployment of charging stations.

03. Who are the major players in the Asia Pacific Electric Vehicle Charger Market?

Key players in the Asia Pacific Electric Vehicle Charger Market include ABB Ltd., Siemens AG, BYD Company Ltd., Tesla Inc., and Delta Electronics Inc., who lead through strategic partnerships, extensive R&D investments, and significant market penetration.

04. What are the growth drivers of the Asia Pacific Electric Vehicle Charger Market?

Growth is driven in Asia Pacific Electric Vehicle Charger Market by government incentives for electric vehicles, urbanization, rising consumer demand for eco-friendly transport, and continuous advancements in charging technologies.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.