Asia-Pacific Semiconductor Market Outlook to 2030

Region:Asia

Author(s):Naman Rohilla

Product Code:KROD3449

November 2024

91

About the Report

Asia-Pacific Semiconductor Market Overview

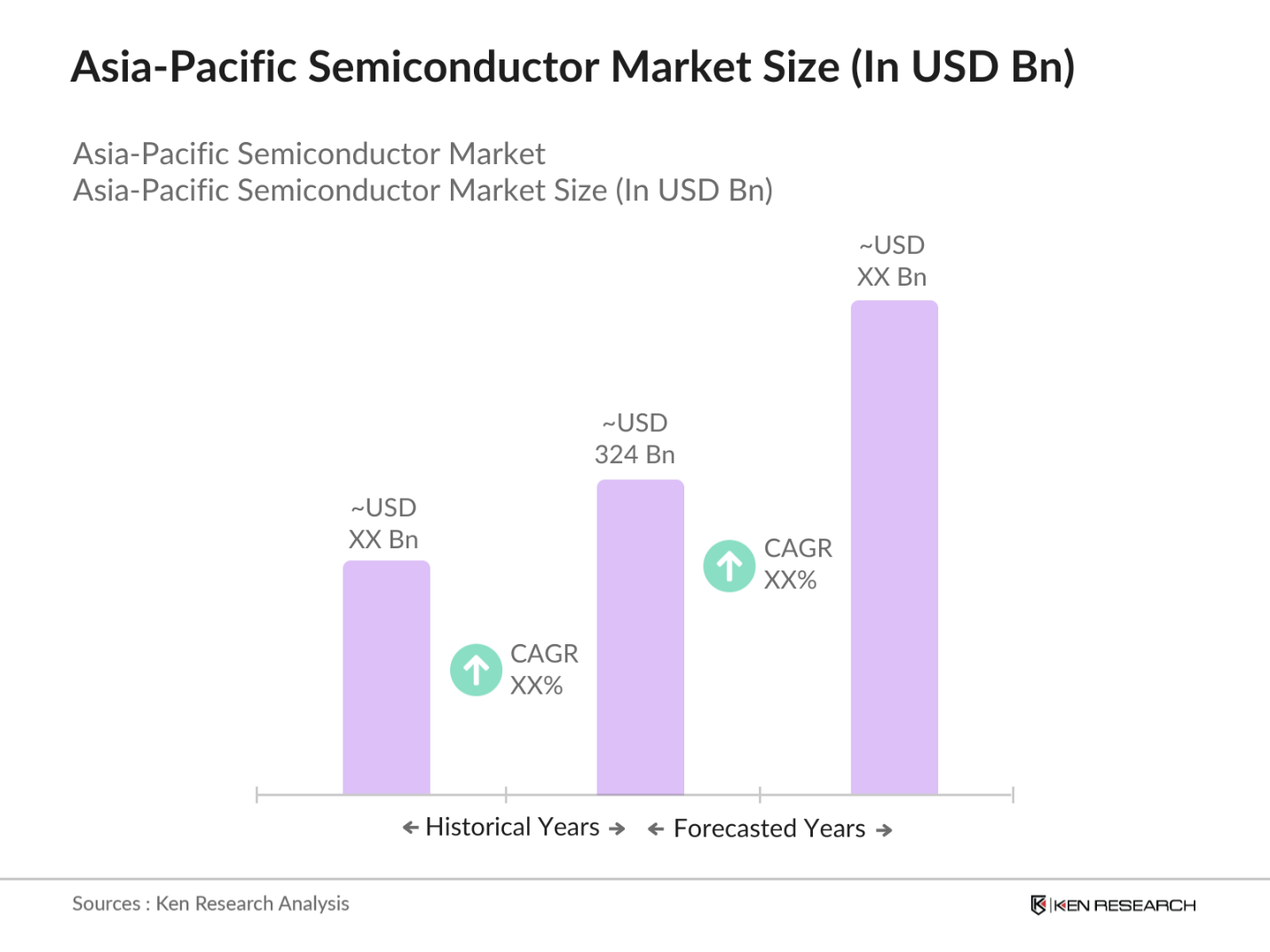

- The Asia-Pacific semiconductor market is a critical driver of the global electronics industry, valued at USD 324 billion. This growth is primarily driven by the rising demand for consumer electronics, including smartphones, tablets, and wearables, as well as the increased adoption of technologies such as 5G, AI, and IoT in various industries. The region's robust manufacturing ecosystem, especially in China, Taiwan, South Korea, and Japan, supports the production of essential semiconductor components that power these innovations.

- Countries like China and Taiwan dominate the semiconductor industry due to their well-established infrastructure and access to raw materials, allowing them to mass-produce semiconductor components at a competitive cost. China leads with its focus on local production, driven by governmental policies supporting the semiconductor industry. Taiwan, home to major companies like TSMC, is renowned for its cutting-edge fabrication capabilities. South Korea follows closely, with Samsung spearheading advanced memory chip production.

- Smart manufacturing and automation are indeed trends in the Asia-Pacific semiconductor market. The region is witnessing substantial growth driven by advancements in technologies such as robotics, cloud computing, and the Industrial Internet of Things (IIoT). Nearly 44% of APAC manufacturers plan to adopt smart manufacturing within the next year, bolstered by government initiatives aimed at digitalizing manufacturing processes. Japan and South Korea remain leaders in this field, with Japan operating over 250 automated production facilities as of 2022.

Asia-Pacific Semiconductor Market Segmentation

The Asia-Pacific Semiconductor Market is segmented by product type, application, technology, end-user, and geographical region.

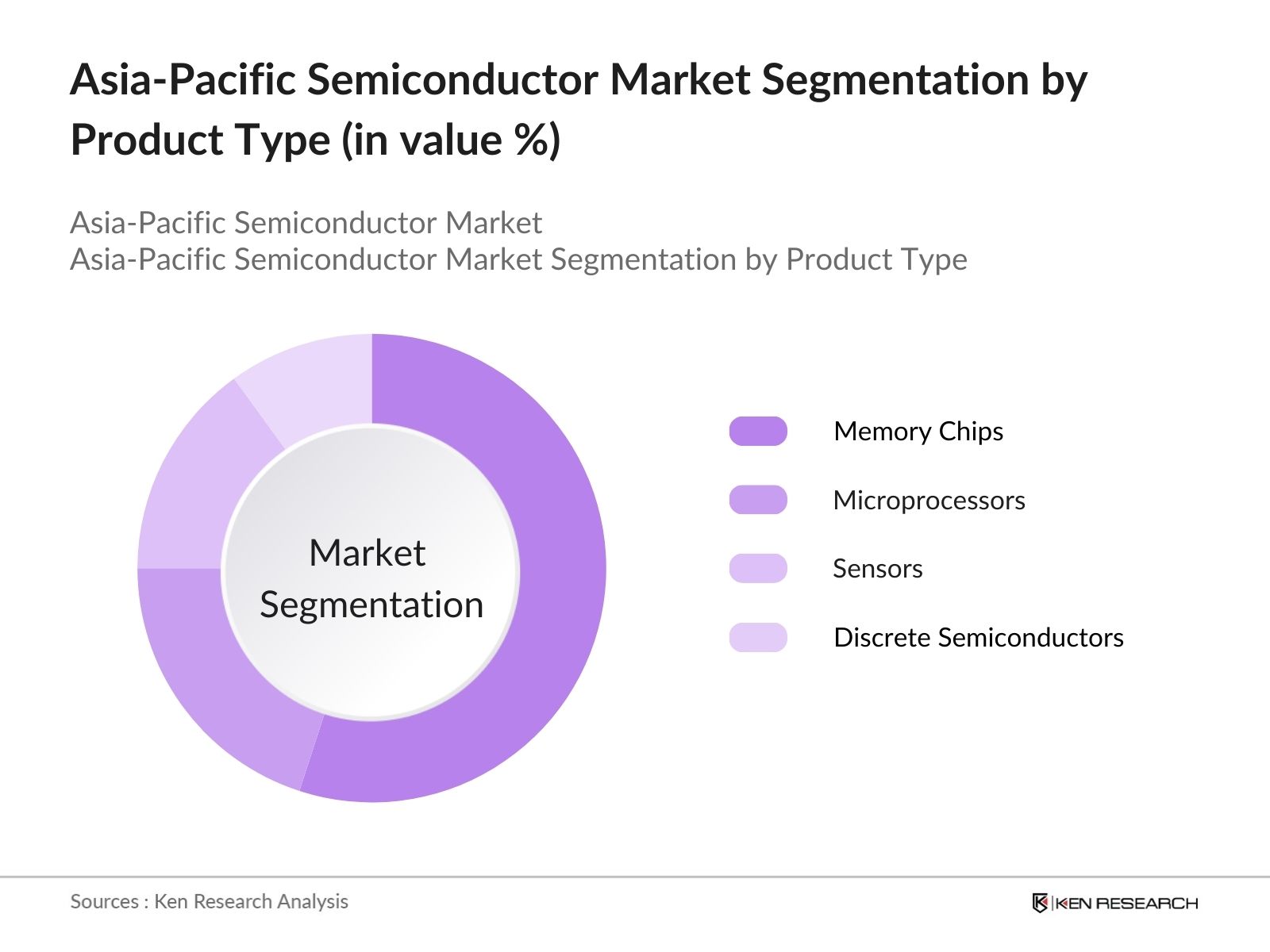

By Product Type: The Asia-Pacific semiconductor market is segmented by product type into memory chips, microprocessors, sensors, and discrete semiconductors. In 2023, memory chips hold a dominant market share, accounting for 55% of the total market. The dominance of memory chips is attributed to their widespread use in consumer electronics, cloud computing, and data storage solutions. Companies like Samsung and SK Hynix lead the memory chip market due to their expertise in high-capacity, high-performance chips, especially in DRAM and NAND technologies.

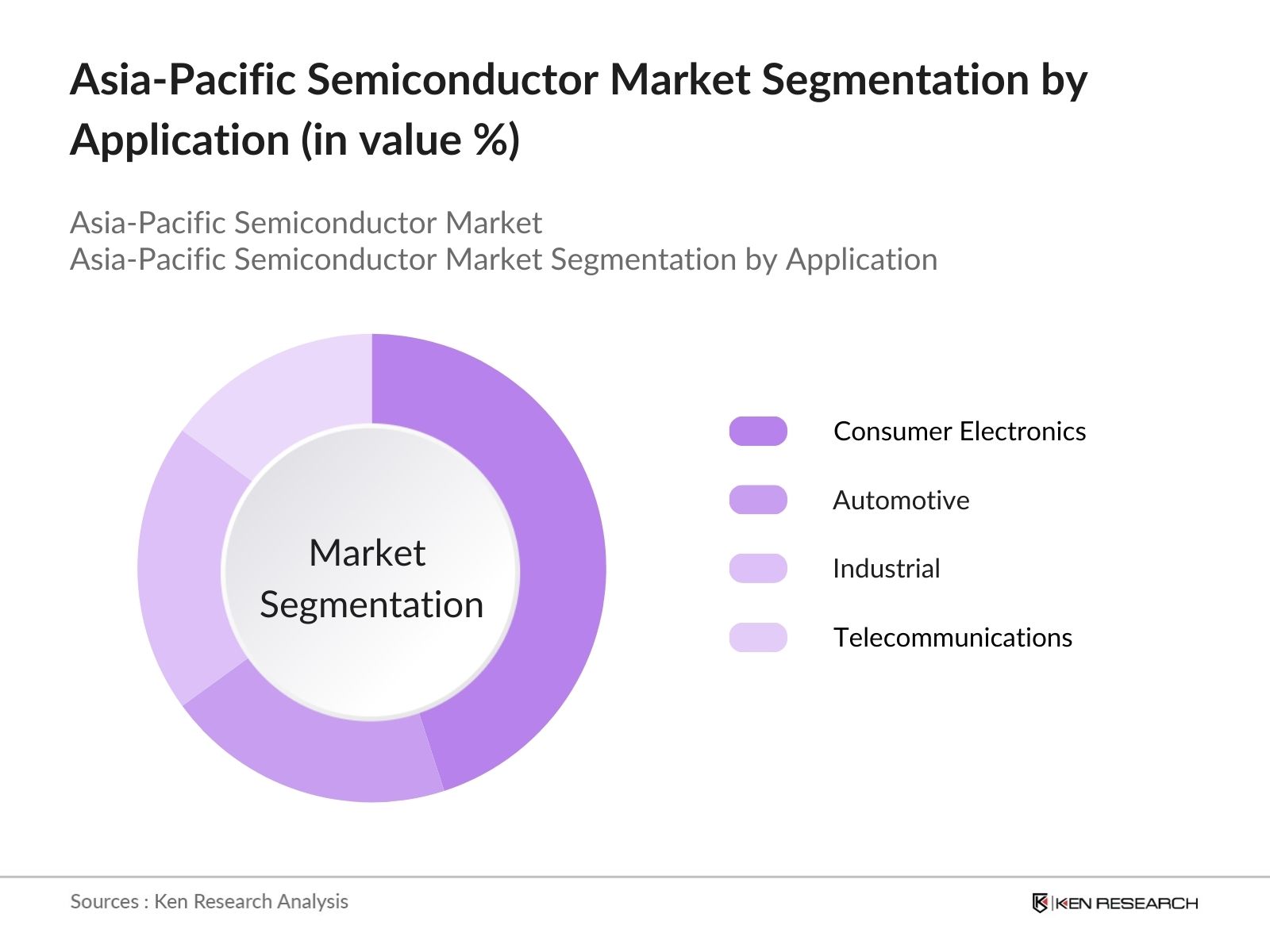

By Application: The market is also segmented by application into consumer electronics, automotive, industrial, and telecommunications. Consumer electronics remains the largest segment, capturing 45% of the market share in 2023. The demand for smartphones, laptops, and smart home devices has driven this segment's growth, with major players such as Apple, Huawei, and Xiaomi relying heavily on semiconductor components for product innovation. The rapid adoption of 5G and AI technologies in electronics has further reinforced the importance of semiconductors in this sector.

Asia-Pacific Semiconductor Market Competitive Landscape

The Asia-Pacific semiconductor market is dominated by a mix of local and global players, with TSMC (Taiwan), Samsung Electronics (South Korea), and Intel (US) at the forefront. These companies' competitive advantage lies in their advanced manufacturing processes, such as EUV lithography and 3D chip stacking, which enable the production of high-performance semiconductors. Furthermore, collaborations and strategic partnerships with global tech giants have solidified their market position.

|

Company |

Establishment Year |

Headquarters |

Market Cap (USD) |

R&D Investment |

Technology Focus |

Number of Fabs |

Global Revenue (2023) |

|

TSMC |

1987 |

Taiwan |

- |

- |

- |

- |

- |

|

Samsung Electronics |

1969 |

South Korea |

- |

- |

- |

- |

- |

|

Intel Corporation |

1968 |

United States |

- |

- |

- |

- |

- |

|

SK Hynix |

1983 |

South Korea |

- |

- |

- |

- |

- |

|

MediaTek |

1997 |

Taiwan |

- |

- |

- |

- |

- |

Asia-Pacific Semiconductor Market Analysis

Asia-Pacific Semiconductor Market Growth Drivers:

- Consumer Electronics Demand: The demand for consumer electronics in the Asia-Pacific region has surged, driven by an increase in disposable income and technological advancements. As of 2023, approximately 1.6 billion smartphones are expected to be sold globally, with a portion from Asia-Pacific, where China alone produced over 310 million smartphones in 2022. The region also accounts for nearly 60% of global television shipments, with Japan and South Korea leading innovations in OLED and QLED technologies. As income levels rise, more consumers are purchasing premium electronic devices like wearables and gaming consoles, further boosting semiconductor demand.

- Industrial Automation (Industry 4.0, IIoT): Industrial automation is becoming a core component of Asia-Pacific's manufacturing sectors, particularly with the integration of Industry 4.0 and IIoT (Industrial Internet of Things). Countries like Japan and South Korea are leading the charge in robot density, with Japan deploying over 374,000 industrial robots by 2022. The region has over 70% of the global industrial robot market. IIoT spending in the region reached nearly $55 billion in 2023, primarily driven by sectors like automotive, electronics, and heavy machinery, thereby increasing semiconductor demand for sensors, processors, and control units.

- Automotive Electronics (ADAS, Electric Vehicles): Automotive electronics, especially ADAS (Advanced Driver Assistance Systems) and Electric Vehicles (EVs), are key growth drivers in the Asia-Pacific semiconductor market. Japan, South Korea, and China are major players, with China selling over 5 million EVs in 2022, a 60% rise from 2021. ADAS technologies have also gained traction, with countries like Japan having 80% of new vehicles equipped with ADAS features. Semiconductors used in vehicle control systems, battery management, and infotainment systems are essential for the continued growth of the automotive sector.

Asia-Pacific Semiconductor Market Challenges:

- Supply Chain Disruptions: Supply chain disruptions remain a critical challenge in the Asia-Pacific semiconductor market. The semiconductor shortage, exacerbated by the COVID-19 pandemic, led to a 20-30% reduction in chip supplies for industries like automotive and consumer electronics in 2022. Countries heavily dependent on semiconductor imports, such as India and Indonesia, faced delays in manufacturing timelines. Even semiconductor manufacturing hubs like Taiwan and South Korea experienced delays due to logistical issues, impacting the supply of essential materials like silicon wafers and photomasks. Source: IMF

- Geopolitical Tensions: Geopolitical tensions, particularly between the United States and China, poseses risks to the Asia-Pacific semiconductor market. Export restrictions on critical technologies, including semiconductors, were imposed in 2022, disrupting trade between the two economic superpowers. China, which accounts for over 25% of global semiconductor demand, has been particularly affected, as restrictions on advanced node chips hamper its technological growth. This situation is further complicated by territorial disputes in the South China Sea, which affects key semiconductor shipping routes.

Asia-Pacific Semiconductor Future Market Outlook

Over the next five years, the Asia-Pacific semiconductor market is poised for major growth, fueled by advancements in AI, 5G technology, and IoT applications. The demand for high-performance chips to support autonomous vehicles, smart cities, and industrial automation is expected to rise, driving the need for cutting-edge semiconductor components. Additionally, government initiatives in countries like India and Vietnam to boost domestic semiconductor manufacturing will further propel market expansion(

Asia-Pacific Semiconductor Market Opportunities:

- Green Technologies: The push for green technologies offers opportunities for semiconductor growth in Asia-Pacific. The region is at the forefront of renewable energy adoption, with China being the largest producer of solar panels, generating over 200 gigawatts of power in 2023. Semiconductors are essential for energy management systems, power inverters, and smart grids. The transition to electric vehicles and the increasing demand for energy-efficient products also contribute to the rising need for semiconductors, with governments in Japan and South Korea offering subsidies for green technology innovations.

- Expansion into Emerging Markets (India, Southeast Asia): Emerging markets in Southeast Asia and India present untapped growth potential for the semiconductor industry. India's electronics industry, valued at over $80 billion in 2023, relies on semiconductor imports to meet its growing demand. Southeast Asia, home to nearly 700 million people, has rapidly increasing digitalization rates, creating demand for semiconductors in sectors like telecommunications, automotive, and consumer electronics. Countries like Vietnam and Indonesia are becoming key players in the global semiconductor supply chain, attracting foreign direct investments.

Scope of the Report

|

By Product Type |

Memory Chips Microprocessors Sensors Discrete Semiconductors |

|

By Application |

Consumer Electronics Automotive Industrial Telecommunications |

|

By Technology |

Advanced Packaging EUV Lithography 3D Chip Design |

|

By End-User |

OEMs Fabless Companies |

|

By Region |

China Taiwan South Korea Japan |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Government and Regulatory Bodies

Banks and Financial Institutes

Investors and Venture Capitalists

Semiconductor Manufacturers

Electronics OEMs

Automotive Manufacturers

Telecommunications Providers

AI and IoT Solution Providers

Industrial Automation Companies

Table of Contents

1. Asia-Pacific Semiconductor Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2. Asia-Pacific Semiconductor Market Size (In USD Bn)

2.1 Historical Market Size

2.2 Year-on-Year Growth Analysis

2.3 Key Market Developments and Milestones

3. Asia-Pacific Semiconductor Market Analysis

3.1 Growth Drivers

3.1.1 Consumer Electronics Demand

3.1.2 Industrial Automation (Industry 4.0, IIoT)

3.1.3 Automotive Electronics (ADAS, Electric Vehicles)

3.1.4 5G and AI Adoption

3.2 Market Challenges

3.2.1 Supply Chain Disruptions

3.2.2 Geopolitical Tensions

3.2.3 Dependency on Exports

3.3 Opportunities

3.3.1 Green Technologies

3.3.2 Government Initiatives in Semiconductor Manufacturing

3.3.3 Expansion into Emerging Markets (India, Southeast Asia)

3.4 Trends

3.4.1 Smart Manufacturing and Automation

3.4.2 Advanced Process Technologies (EUV, FinFET)

3.4.3 AI and Machine Learning Integration

3.5 Government Regulations

3.5.1 Environmental Standards

3.5.2 Trade Policies and Agreements

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem (Manufacturers, Foundries, Design Companies)

3.8 Porters Five Forces

3.9 Competition Ecosystem (Key Semiconductor Hubs: Taiwan, China, South Korea)

4. Asia-Pacific Semiconductor Market Segmentation

4.1 By Product Type (In Value %)

4.1.1 Memory Chips

4.1.2 Microprocessors

4.1.3 Sensors

4.1.4 Discrete Semiconductors

4.2 By Application (In Value %)

4.2.1 Consumer Electronics

4.2.2 Automotive

4.2.3 Industrial

4.2.4 Telecommunications

4.3 By Technology (In Value %)

4.3.1 Advanced Packaging

4.3.2 EUV Lithography

4.3.3 3D Chip Design

4.4 By End-User (In Value %)

4.4.1 OEMs

4.4.2 Fabless Companies

4.5 By Region (In Value %)

4.5.1 China

4.5.2 Taiwan

4.5.3 South Korea

4.5.4 Japan

5. Asia-Pacific Semiconductor Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1 Taiwan Semiconductor Manufacturing Company (TSMC)

5.1.2 Samsung Electronics

5.1.3 Intel Corporation

5.1.4 SK Hynix

5.1.5 Qualcomm

5.1.6 NVIDIA Corporation

5.1.7 Sony Corporation

5.1.8 Toshiba Corporation

5.1.9 Micron Technology

5.1.10 MediaTek

5.1.11 NXP Semiconductors

5.1.12 Fujitsu Semiconductor

5.1.13 Infineon Technologies

5.1.14 Broadcom Inc.

5.1.15 STMicroelectronics

5.2 Cross Comparison Parameters (Revenue, Headquarters, Market Share, Innovation Focus, Manufacturing Capabilities, R&D Investments)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Government Funding and Grants

5.8 Venture Capital Investments

6. Asia-Pacific Semiconductor Market Regulatory Framework

6.1 Environmental and Safety Standards

6.2 Compliance with International Trade Regulations

6.3 Regional Semiconductor Policies (China, Japan, South Korea, Taiwan)

7. Asia-Pacific Semiconductor Future Market Size (In USD Bn)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8. Asia-Pacific Semiconductor Future Market Segmentation

8.1 By Product Type

8.2 By Application

8.3 By Technology

8.4 By End-User

8.5 By Region

9. Asia-Pacific Semiconductor Market Analysts Recommendations

9.1 TAM/SAM/SOM Analysis

9.2 Key Growth Opportunities

9.3 White Space Analysis

Research Methodology

Step 1: Identification of Key Variables

We began by mapping out the entire semiconductor ecosystem, including key players, government bodies, and end-user industries. This phase utilized data from proprietary databases and public records to define the crucial variables influencing market dynamics.

Step 2: Market Analysis and Construction

In this step, we analyzed historical data on semiconductor production and revenue trends, categorizing the market based on product type and application. This analysis involved reviewing company financials, production capacities, and export data.

Step 3: Hypothesis Validation and Expert Consultation

The market hypotheses were validated through interviews with industry experts, including executives from major semiconductor firms and representatives from research institutions. These consultations provided real-time insights into market shifts and future demand trends.

Step 4: Research Synthesis and Final Output

The final phase combined quantitative data from primary and secondary research to produce an accurate and comprehensive analysis of the market. This included detailed forecasts for each market segment and a review of competitive strategies.

Frequently Asked Questions

01. How big is the Asia-Pacific Semiconductor Market?

The Asia-Pacific semiconductor market is valued at USD 324 billion, driven by the rising demand for consumer electronics, automotive electronics, and industrial automation solutions.

02. What are the challenges in the Asia-Pacific Semiconductor Market?

The main challenges include supply chain disruptions, geopolitical tensions, and the dependency on a few key regions like China and Taiwan for semiconductor manufacturing, leading to potential vulnerabilities in global supply.

03. Who are the major players in the Asia-Pacific Semiconductor Market?

Key players include TSMC, Samsung Electronics, Intel Corporation, SK Hynix, and MediaTek, with these companies leading due to their advanced technological capabilities and large-scale production.

04. What are the growth drivers of the Asia-Pacific Semiconductor Market?

The market is propelled by the demand for advanced semiconductor components for 5G, AI, and IoT applications. The automotive sector's shift toward electrification and autonomous driving is also a growth factor.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.