Europe ADAS Market Outlook to 2030

Region:Europe

Author(s):Meenakshi Bisht

Product Code:KROD7840

November 2024

81

About the Report

Europe ADAS Market Overview

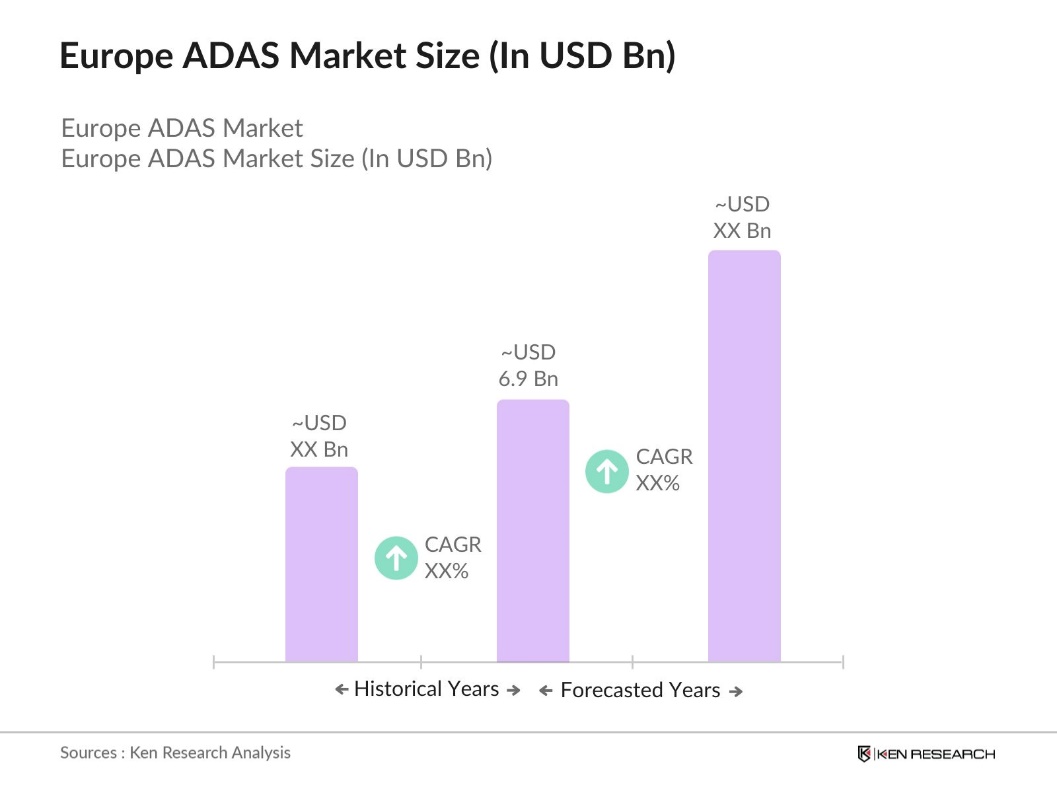

- The Europe ADAS Market is valued at USD 6.9 billion, based on a five-year historical analysis. This substantial market size is driven by stringent safety regulations, increasing consumer demand for vehicle safety features, and rapid advancements in automotive technologies. Additionally, the integration of ADAS with electric and autonomous vehicles further propels market growth, supported by significant investments from both automotive manufacturers and technology providers.

- Key countries dominating the Europe ADAS market include Germany, France, the United Kingdom, Italy, and Spain. Germany leads the market due to its robust automotive industry, home to major car manufacturers like Volkswagen, BMW, and Mercedes-Benz, which prioritize the incorporation of advanced safety systems in their vehicles. France and the UK also exhibit strong market presence driven by high consumer awareness and supportive government policies promoting vehicle safety and innovation.

- The EU General Safety Regulation is a crucial framework shaping the ADAS market. Enforced in 2022, this regulation mandates that all new vehicles in the EU be equipped with essential safety features, including automatic emergency braking, lane departure warning, and advanced driver monitoring systems. The regulation aims to significantly reduce road fatalities and injuries, with the target set for 2030 to achieve a minimum reduction of 50% in fatalities compared to 2020 levels.

Europe ADAS Market Segmentation

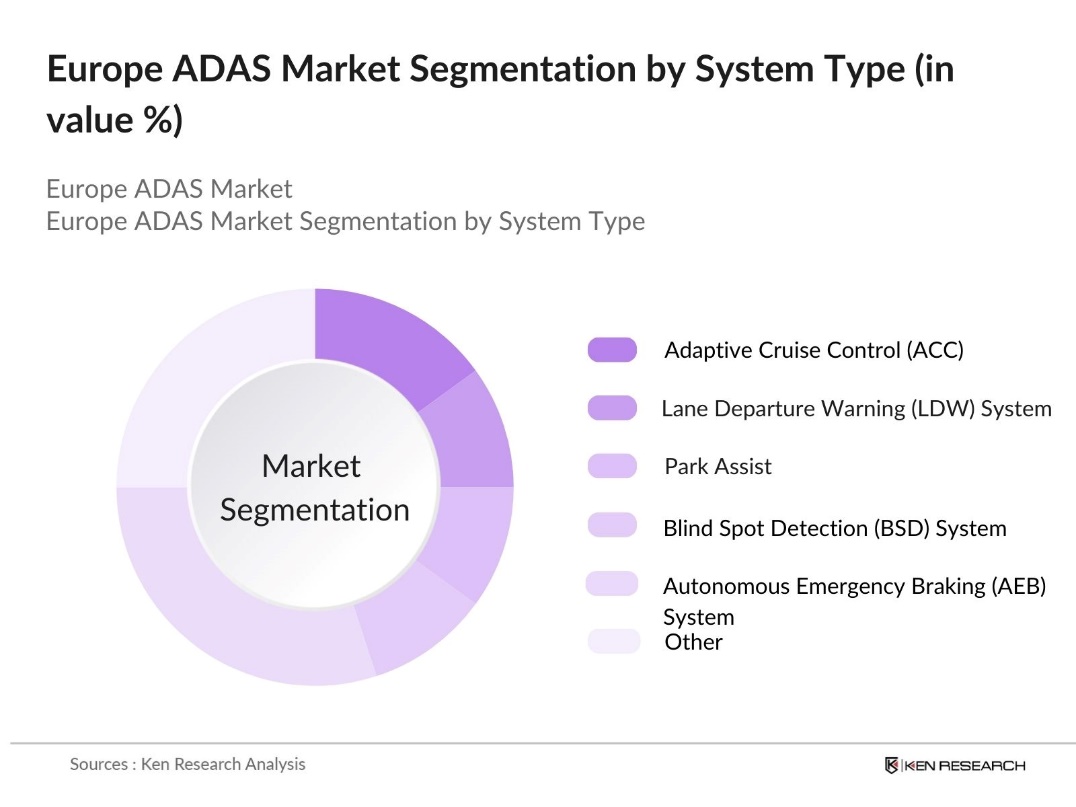

By System Type: The market is segmented by system type into Adaptive Cruise Control (ACC), Lane Departure Warning (LDW) System, Park Assist, Blind Spot Detection (BSD) System, Tire Pressure Monitoring System (TPMS), Autonomous Emergency Braking (AEB) System, and Others. Among these, Autonomous Emergency Braking (AEB) Systems have a dominant market share due to its attributed to their critical role in enhancing vehicle safety by automatically applying brakes to prevent collisions, thereby reducing accidents and saving lives.

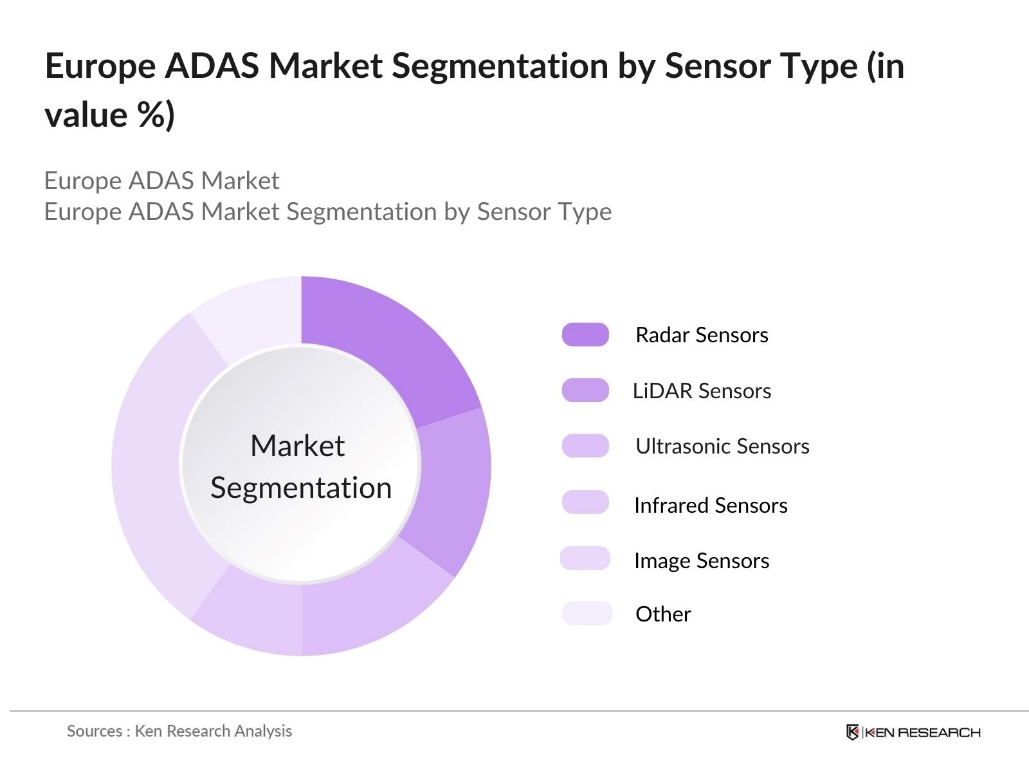

By Sensor Type: The market is segmented by sensor type into Radar Sensors, LiDAR Sensors, Ultrasonic Sensors, Infrared Sensors, and Image Sensors. Image Sensors hold the largest market share of 30% in 2023. The prevalence of image sensors is driven by their ability to provide high-resolution data essential for accurate object detection and classification. Image sensors are integral to systems like AEB, LDW, and BSD, enabling precise monitoring of the vehicle's surroundings.

Europe ADAS Market Competitive Landscape

The Europe ADAS market is dominated by a few major players, including Robert Bosch GmbH, Continental AG, ZF Friedrichshafen AG, Valeo SA, and DENSO Corporation. This consolidation highlights the significant influence of these key companies, which leverage their extensive research and development capabilities, strong brand presence, and strategic partnerships to maintain their market leadership. These companies are at the forefront of technological innovations, continuously enhancing their ADAS offerings to meet the evolving demands of automotive manufacturers and consumers.

Europe ADAS Industry Analysis

Growth Drivers

- Stringent Safety Regulations: The European Union has implemented robust safety regulations for vehicles to enhance road safety. In the number of fatalities from road accidents in the EU was 20,653, which represents a 4% increase from 19,917 fatalities in 2021. Furthermore, the EU aims to reduce road deaths to zero by 2050 as part of its Vision Zero strategy. These regulations are driving the demand for Advanced Driver Assistance Systems (ADAS), leading to increased investments in technology and safety features.

- Increasing Vehicle Electrification: The push for electrification in the automotive sector is creating opportunities for ADAS. In 2023, battery-electric vehicles accounted for approximately 14.6% of new car sales in the European Union. This growth is driven by government incentives, such as grants and subsidies, to promote EV adoption, as well as a growing emphasis on sustainability. The integration of ADAS in electric vehicles enhances safety and efficiency, further appealing to environmentally conscious consumers.

- Rising Consumer Awareness: Consumer awareness of vehicle safety features is increasing, driving demand for Advanced Driver Assistance Systems (ADAS). As consumers prioritize safety in their vehicle purchases, this trend is supported by road safety campaigns and educational initiatives across Europe. Greater awareness of the benefits of ADAS encourages drivers to seek vehicles equipped with these technologies, motivating manufacturers to innovate and enhance their safety offerings in response to consumer preferences.

Market Challenges

- High Implementation Costs: The implementation of Advanced Driver Assistance Systems (ADAS) involves significant costs that can hinder market growth. The initial investment for advanced sensor systems is often substantial, presenting a barrier for many automakers, especially smaller companies. Additionally, compliance with stringent safety regulations necessitates ongoing investments in research and development, further straining budgets. The challenge is exacerbated by supply chain issues, which impact production capabilities and lead to delays in deploying these technologies in vehicles.

- Infrastructure Limitations: Inadequate infrastructure presents a significant challenge to the widespread adoption of ADAS technologies. Many European countries lack the necessary road infrastructure to support advanced vehicle systems, such as vehicle-to-infrastructure communication. This deficiency limits the effectiveness of ADAS features, including real-time traffic updates and smart navigation systems. Moreover, investment in infrastructure development is often slow and inconsistent across regions, complicating the integration and functionality of ADAS in vehicles.

Europe ADAS Market Future Outlook

Over the next five years, the Europe ADAS market is expected to show significant growth driven by continuous advancements in ADAS technologies, increasing adoption of autonomous vehicles, and supportive government regulations aimed at enhancing road safety. The integration of artificial intelligence and machine learning into ADAS will further enhance system capabilities, making vehicles smarter and safer.

Market Opportunities

- Integration with Autonomous Vehicles: The integration of Advanced Driver Assistance Systems (ADAS) with autonomous vehicle technology offers significant growth opportunities in the European market. Numerous pilot projects for autonomous vehicles are currently underway, showcasing the industry's commitment to advancing this technology. These initiatives utilize ADAS features such as adaptive cruise control and automatic lane change, laying the groundwork for fully autonomous driving. Continued advancements in this sector are anticipated to create synergies that will further stimulate the growth of the ADAS market.

- Expansion in Emerging Markets: Emerging markets in Europe, particularly in Eastern Europe, present considerable growth potential for the ADAS market. As vehicle ownership increases in these regions, so does the demand for advanced safety technologies. Governments are adopting stricter safety regulations similar to those in Western Europe, which aims to improve road safety standards. This growing awareness among consumers about the benefits of ADAS is expected to drive adoption, while investments in infrastructure and vehicle technology will further bolster market growth in these emerging markets.

Scope of the Report

|

System Type |

Adaptive Cruise Control (ACC) |

|

Sensor Type |

Radar Sensors |

|

Vehicle Type |

Passenger Cars |

|

Offering |

Hardware |

|

Region |

Germany |

Products

Key Target Audience

Automotive Manufacturers (e.g., Volkswagen Group, BMW Group)

Tier 1 Suppliers (e.g., Bosch, Continental)

Automotive Technology

Fleet Management Companies

Insurance Companies

Investor and Venture Capitalist Firms (e.g., Sequoia Capital, Accel Partners)

Government and Regulatory Bodies (e.g., European Commission, European Automobile Manufacturers Association)

Banks and Financial Institutions

Companies

Players Mentioned in the Report

Robert Bosch GmbH

Continental AG

ZF Friedrichshafen AG

Valeo SA

DENSO Corporation

Aptiv PLC

Magna International Inc.

Autoliv Inc.

Hella GmbH & Co. KGaA

Mobileye N.V.

Table of Contents

1. Europe ADAS Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2. Europe ADAS Market Size (In USD Mn)

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3. Europe ADAS Market Analysis

3.1 Growth Drivers

3.1.1 Stringent Safety Regulations

3.1.2 Technological Advancements

3.1.3 Rising Consumer Awareness

3.1.4 Increasing Vehicle Electrification

3.2 Market Challenges

3.2.1 High Implementation Costs

3.2.2 Infrastructure Limitations

3.2.3 Data Privacy Concerns

3.3 Opportunities

3.3.1 Integration with Autonomous Vehicles

3.3.2 Expansion in Emerging Markets

3.3.3 Development of Multifunctional Sensors

3.4 Trends

3.4.1 Adoption of AI and Machine Learning

3.4.2 Collaboration Between OEMs and Tech Firms

3.4.3 Growth of Over-the-Air (OTA) Updates

3.5 Government Regulations

3.5.1 EU General Safety Regulation

3.5.2 Euro NCAP Assessments

3.5.3 National Road Safety Programs

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem

3.8 Porter's Five Forces Analysis

3.9 Competitive Landscape

4. Europe ADAS Market Segmentation

4.1 By System Type (In Value %)

4.1.1 Adaptive Cruise Control (ACC)

4.1.2 Lane Departure Warning (LDW) System

4.1.3 Park Assist

4.1.4 Blind Spot Detection (BSD) System

4.1.5 Tire Pressure Monitoring System (TPMS)

4.1.6 Autonomous Emergency Braking (AEB) System

4.1.7 Others

4.2 By Sensor Type (In Value %)

4.2.1 Radar Sensors

4.2.2 LiDAR Sensors

4.2.3 Ultrasonic Sensors

4.2.4 Infrared Sensors

4.2.5 Image Sensors

4.3 By Vehicle Type (In Value %)

4.3.1 Passenger Cars

4.3.2 Light Commercial Vehicles (LCVs)

4.3.3 Heavy Commercial Vehicles (HCVs)

4.4 By Offering (In Value %)

4.4.1 Hardware

4.4.2 Software

4.5 By Region (In Value %)

4.5.1 Germany

4.5.2 United Kingdom

4.5.3 France

4.5.4 Italy

4.5.5 Spain

4.5.6 Rest of Europe

5. Europe ADAS Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1 Robert Bosch GmbH

5.1.2 Continental AG

5.1.3 ZF Friedrichshafen AG

5.1.4 Valeo SA

5.1.5 DENSO Corporation

5.1.6 Aptiv PLC

5.1.7 Magna International Inc.

5.1.8 Autoliv Inc.

5.1.9 Hella GmbH & Co. KGaA

5.1.10 Mobileye N.V.

5.1.11 NVIDIA Corporation

5.1.12 Infineon Technologies AG

5.1.13 NXP Semiconductors N.V.

5.1.14 Texas Instruments Incorporated

5.1.15 STMicroelectronics N.V.

5.2 Cross Comparison Parameters (Revenue, Market Share, Product Portfolio, R&D Investment, Regional Presence, Strategic Initiatives, Partnerships, Technological Innovations)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6. Europe ADAS Market Regulatory Framework

6.1 Safety Standards

6.2 Compliance Requirements

6.3 Certification Processes

7. Europe ADAS Future Market Size (In USD Mn)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8. Europe ADAS Future Market Segmentation

8.1 By System Type (In Value %)

8.2 By Sensor Type (In Value %)

8.3 By Vehicle Type (In Value %)

8.4 By Offering (In Value %)

8.5 By Region (In Value %)

9. Europe ADAS Market Analysts Recommendations

9.1 Total Addressable Market (TAM) Analysis

9.2 Serviceable Available Market (SAM) Analysis

9.3 Serviceable Obtainable Market (SOM) Analysis

9.4 Customer Cohort Analysis

9.5 Marketing Initiatives

9.6 White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the Europe ADAS Market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, we compile and analyze historical data pertaining to the Europe ADAS Market. This includes assessing market penetration, the ratio of system types to sensor types, and the resultant revenue generation. Furthermore, an evaluation of service quality statistics will be conducted to ensure the reliability and accuracy of the revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses will be developed and subsequently validated through computer-assisted telephone interviews (CATIs) with industry experts representing a diverse array of companies. These consultations will provide valuable operational and financial insights directly from industry practitioners, which will be instrumental in refining and corroborating the market data.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with multiple ADAS manufacturers to acquire detailed insights into product segments, sales performance, consumer preferences, and other pertinent factors. This interaction will serve to verify and complement the statistics derived from the bottom-up approach, thereby ensuring a comprehensive, accurate, and validated analysis of the Europe ADAS market.

Frequently Asked Questions

01. How big is the Europe ADAS Market?

The Europe ADAS Market was valued at USD 6.9 billion, driven by stringent safety regulations, technological advancements, and increasing consumer demand for enhanced vehicle safety features.

02. What are the challenges in the Europe ADAS Market?

Challenges in Europe ADAS Market include high implementation costs, integration complexities with existing vehicle systems, and data privacy concerns related to the use of advanced sensors and cameras.

03. Who are the major players in the Europe ADAS Market?

Key players in the Europe ADAS Market include Robert Bosch GmbH, Continental AG, ZF Friedrichshafen AG, Valeo SA, and DENSO Corporation. These companies dominate due to their extensive R&D capabilities, strong brand presence, and strategic partnerships.

04. What are the growth drivers of the Europe ADAS Market?

The Europe ADAS Market is propelled by factors such as stringent safety regulations, rapid technological advancements, increasing consumer awareness about vehicle safety, and the growing adoption of electric and autonomous vehicles.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.