Europe Electric Vans Market Outlook to 2030

Region:Global

Author(s):Sanjna

Product Code:KROD4310

November 2024

87

About the Report

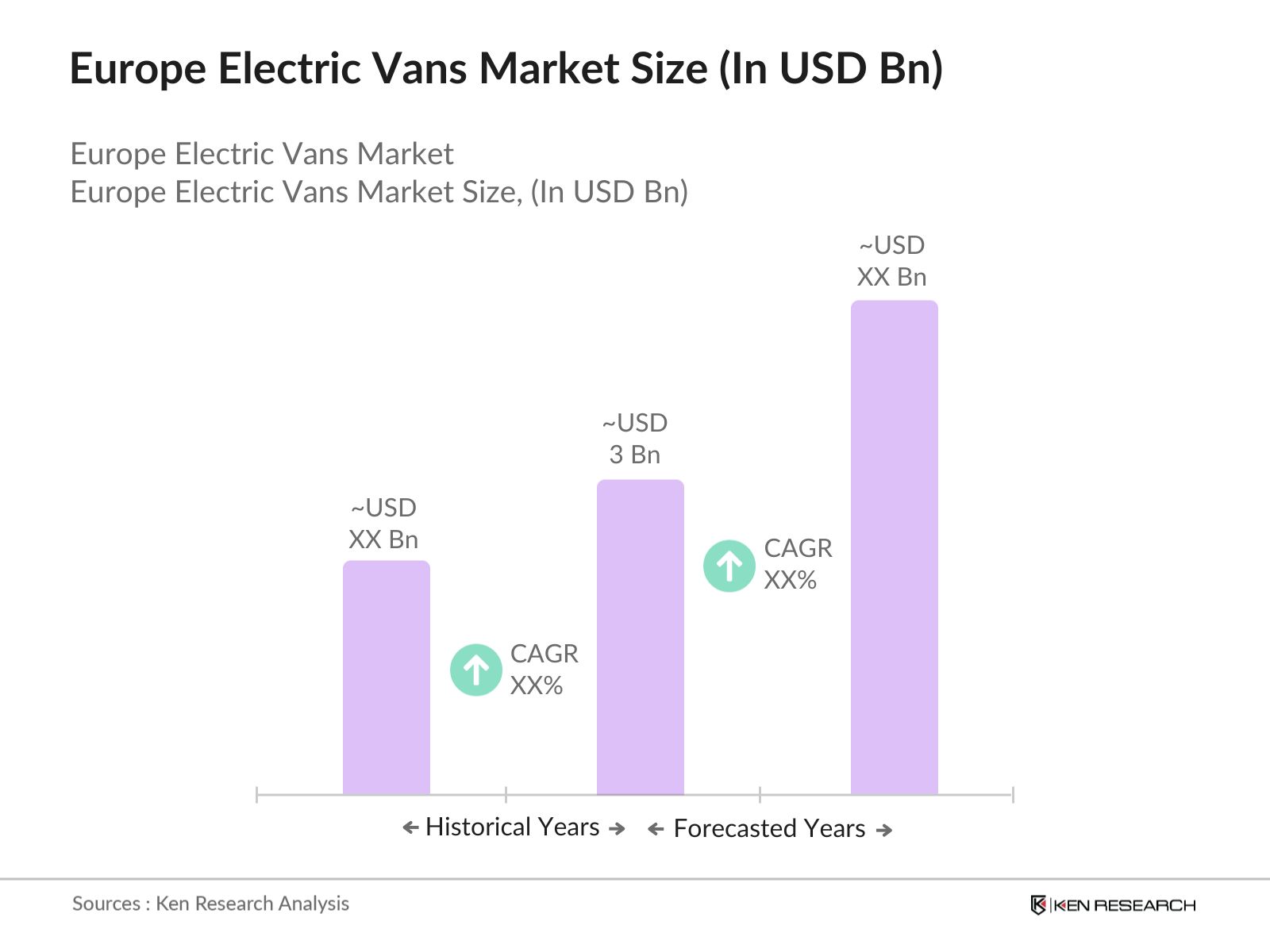

Europe Electric Vans Market Overview

- The Europe Electric Vans market is valued at USD 3 billion, driven by a combination of regulatory measures and a shift towards environmentally friendly transportation. A key driver is the growing adoption of electric vehicles (EVs) by both businesses and governments aiming to meet stricter emission standards. This market is also propelled by the expansion of charging infrastructure and the rising demand for last-mile delivery solutions in urban areas.

- Countries like Germany, France, and the United Kingdom dominate the European Electric Vans market due to their advanced EV infrastructure, strong government support, and aggressive emission reduction targets. Germany, for example, has a well-established automotive industry that is rapidly transitioning to electric vehicles. France offers substantial financial incentives for electric vehicle adoption, while the United Kingdom has set ambitious goals for phasing out internal combustion engine vehicles, fueling the market's growth in these regions.

- Many European cities have introduced zero-emission zones where only electric vehicles, including vans, are allowed to operate. Cities such as London, Amsterdam, and Madrid are leading the way, with over 200 European cities planning to implement such zones by 2025. In 2024, approximately 35% of the population in these cities live within zero-emission zones, which is a major driver for the adoption of electric vans by businesses that operate in these urban areas.

Europe Electric Vans Market Segmentation

By Vehicle Type: The Europe Electric Vans market is segmented by vehicle type into Light Electric Vans, Medium Electric Vans, and Heavy Electric Vans. Light electric vans dominate the market, largely due to their widespread use in urban logistics and last-mile delivery services. Their lower costs, combined with increasing pressure on businesses to adopt eco-friendly transportation, have made light vans the preferred choice for corporate fleets.

By End-User: The market is segmented by end-user into Corporate Fleets, Public Sector Fleets, and Private Consumers. Corporate fleets hold a dominant position in the market, as businesses increasingly shift towards electrifying their fleets to reduce carbon footprints and meet corporate sustainability goals. Major logistics companies and e-commerce giants are leading the adoption of electric vans for last-mile delivery, driven by rising e-commerce demands and government regulations promoting zero-emission zones in major cities.

By End-User: The market is segmented by end-user into Corporate Fleets, Public Sector Fleets, and Private Consumers. Corporate fleets hold a dominant position in the market, as businesses increasingly shift towards electrifying their fleets to reduce carbon footprints and meet corporate sustainability goals. Major logistics companies and e-commerce giants are leading the adoption of electric vans for last-mile delivery, driven by rising e-commerce demands and government regulations promoting zero-emission zones in major cities.

Europe Electric Vans Market Competitive Landscape

The Europe Electric Vans market is characterized by the presence of several established players and new entrants, including both traditional automakers and EV startups. The market is consolidated, with key companies holding significant market power due to their established distribution networks and technological advancements in battery efficiency. The market is dominated by a few major players, including Daimler AG, Renault Group, Nissan Motor Co., Ltd., Volkswagen AG, and Ford Motor Company.

|

Company |

Establishment Year |

Headquarters |

Battery Range |

Charging Time |

Production Volume |

Number of Models |

Key Partnerships |

Sustainability Initiatives |

|

Daimler AG |

1926 |

Stuttgart, Germany |

- |

- |

- |

- |

- |

- |

|

Renault Group |

1899 |

Boulogne-Billancourt, France |

- |

- |

- |

- |

- |

- |

|

Nissan Motor Co., Ltd. |

1933 |

Yokohama, Japan |

- |

- |

- |

- |

- |

- |

|

Volkswagen AG |

1937 |

Wolfsburg, Germany |

- |

- |

- |

- |

- |

- |

|

Ford Motor Company |

1903 |

Dearborn, USA |

- |

- |

- |

- |

- |

- |

Europe Electric Vans Market Analysis

Growth Drivers

- Adoption of Electric Vehicles: By 2024, the European Union (EU) targets a reduction of greenhouse gas emissions by 55% from 1990 levels, pushing industries to adopt electric vehicles to meet these targets. In the electric van sector, countries like Germany, France, and the UK have made considerable investments to support the transition. Over 500,000 electric vans are projected to be in operation by 2025 in Europe, driven by policies that favor zero-emission vehicles.

- Government Regulations on Emissions: The EUs introduction of strict emission regulations like the Euro 7 standards, which mandate significant reductions in nitrogen oxides (NOx) and particulate matter emissions from all vehicles, directly supports the adoption of electric vans. Electric vehicles (including vans) are exempt from these emission limits, making them a highly attractive option for businesses operating in heavily regulated sectors. In 2024, these regulations are expected to cut emissions from vehicles by up to 50%, accelerating the push toward electrification.

- Corporate Fleet Electrification: In response to sustainability goals, numerous corporations are transitioning their fleets to electric vehicles. For example, logistics companies such as DHL and Amazon have committed to deploying electric vans across their European fleets, aiming to achieve zero-emission operations by 2030. In 2024, it is estimated that over 50,000 corporate electric vans will be in operation across major European logistics firms, spurred by carbon taxes and fleet electrification incentives from the European Union.

Challenges

- Limited Charging Infrastructure: Although the adoption of electric vans is growing, the lack of a widespread and reliable charging infrastructure remains a significant challenge. Europe currently has approximately 340,000 charging points as of 2024, but only about 15% are suitable for commercial electric vehicles like vans. This shortage hampers long-distance operations and causes operational delays for logistics firms. To meet future demand, Europe needs to deploy over 1 million charging points by 2025, a goal that remains distant under the current pace of development.

- High Initial Costs Compared to ICE Vans: Electric vans currently have higher upfront costs compared to their internal combustion engine (ICE) counterparts, primarily due to the cost of batteries. As of 2024, the average price of an electric van is $48,856.55, while ICE vans cost approximately $32,571.03. This price gap, although decreasing, still presents a barrier for smaller businesses, despite long-term savings from lower fuel and maintenance costs. The EU is working to reduce this disparity through various subsidy programs, but the cost difference continues to be a hurdle.

Europe Electric Vans Market Future Outlook

Europe Electric Vans market is expected to experience significant growth, driven by increasing regulatory pressure to reduce emissions, advancements in electric van technology, and rising consumer demand for greener transportation solutions. Governments across Europe are providing generous incentives to encourage the adoption of electric vehicles, particularly in urban centers where emission-free zones are becoming more common. Additionally, corporate fleet electrification, particularly in logistics and delivery services, will further fuel market expansion.

Market Opportunities

- Advancements in Battery Technology: Technological advancements in battery storage and efficiency offer promising opportunities for the electric van market. By 2024, the energy density of lithium-ion batteries used in electric vans has improved by over 30%, extending the range and reducing charging time. These advancements lower operational costs and mitigate range anxiety for fleet operators. Additionally, developments in solid-state batteries could further enhance energy storage capacities and safety, which would likely accelerate fleet electrification in Europe.

- Expansion of Charging Networks: Government and private sector investments are expanding the electric charging network across Europe. By the end of 2024, the EU will have allocated USD 1.4 billion to develop high-speed charging stations along key transport corridors under its Connecting Europe Facility program. This initiative aims to install 120,000 new charging points by 2025, ensuring seamless electric van operations for businesses, especially in the logistics sector. This expansion is critical for alleviating concerns about charging infrastructure, particularly for commercial vehicles.

Scope of the Report

|

Segment |

Sub-segments |

|

Vehicle Type |

Light Electric Vans |

|

Medium Electric Vans |

|

|

Heavy Electric Vans |

|

|

End-User |

Corporate Fleets |

|

Public Sector Fleets |

|

|

Private Consumers |

|

|

Charging Type |

Fast Charging |

|

Slow Charging |

|

|

Battery Type |

Lithium-ion Battery |

|

Solid-state Battery |

|

|

Region |

Germany |

|

France |

|

|

United Kingdom |

|

|

Netherlands |

|

|

Spain |

|

|

Italy |

|

|

Norway |

|

|

Sweden |

Products

Key Target Audience

Corporate Fleet Managers

Electric Vehicle Manufacturers

Logistics and Delivery Companies

Charging Infrastructure Providers

Battery Manufacturers and Suppliers

Investors and Venture Capitalist Firms

Government and Regulatory Bodies (European Commission, National Transport Authorities)

Companies

Players Mentioned in the Report

Daimler AG

Renault Group

Nissan Motor Co., Ltd.

Volkswagen AG

Ford Motor Company

Rivian Automotive, Inc.

Arrival Ltd.

Mercedes-Benz Vans

BYD Auto Co., Ltd.

Stellantis N.V.

Table of Contents

1. Europe Electric Vans Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Europe Electric Vans Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Europe Electric Vans Market Analysis

3.1. Growth Drivers (Electric vehicle adoption, Emission regulations, Incentives for green transport)

3.1.1. Adoption of electric vehicles

3.1.2. Government regulations on emissions

3.1.3. Corporate fleet electrification

3.2. Market Challenges (Infrastructure, Cost barriers, Range anxiety)

3.2.1. Limited charging infrastructure

3.2.2. High initial costs compared to ICE vans

3.2.3. Battery limitations and range anxiety

3.3. Opportunities (Technological advancements, Government support, Corporate partnerships)

3.3.1. Advancements in battery technology

3.3.2. Expansion of charging networks

3.3.3. Fleet conversion incentives

3.4. Trends (Connected mobility, Shared transportation, Micro-distribution networks)

3.4.1. Integration of IoT for vehicle performance monitoring

3.4.2. Emergence of shared electric van services

3.4.3. Growth of last-mile delivery using electric vans

3.5. Government Regulation (Emission targets, Subsidies, Incentive programs)

3.5.1. Euro 7 emission standards

3.5.2. Subsidies and tax rebates for electric vans

3.5.3. Zero-emission zone mandates in cities

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competitive Ecosystem

4. Europe Electric Vans Market Segmentation

4.1. By Vehicle Type (In Value %)

4.1.1. Light Electric Vans

4.1.2. Medium Electric Vans

4.1.3. Heavy Electric Vans

4.2. By End-User (In Value %)

4.2.1. Corporate Fleets

4.2.2. Public Sector Fleets

4.2.3. Private Consumers

4.3. By Charging Type (In Value %)

4.3.1. Fast Charging

4.3.2. Slow Charging

4.4. By Battery Type (In Value %)

4.4.1. Lithium-ion Battery

4.4.2. Solid-state Battery

4.5. By Region (In Value %)

4.5.1. Germany

4.5.2. France

4.5.3. United Kingdom

4.5.4. Netherlands

4.5.5. Spain

4.5.6. Italy

4.5.7. Norway

4.5.8. Sweden

5. Europe Electric Vans Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Daimler AG

5.1.2. Renault Group

5.1.3. Nissan Motor Co., Ltd.

5.1.4. Stellantis N.V.

5.1.5. Ford Motor Company

5.1.6. Volkswagen AG

5.1.7. Rivian Automotive, Inc.

5.1.8. Arrival Ltd.

5.1.9. Mercedes-Benz Vans

5.1.10. BYD Auto Co., Ltd.

5.2. Cross Comparison Parameters (Battery range, Charging time, Vehicle weight, Payload capacity, Charging network partnerships, Safety features, Price range, Availability in regional markets)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Government Grants

5.8. Private Equity Investments

6. Europe Electric Vans Market Regulatory Framework

6.1. Emission Regulations

6.2. Certification Requirements

6.3. Government Support Programs

7. Europe Electric Vans Future Market Size (In USD Mn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Europe Electric Vans Future Market Segmentation

8.1. By Vehicle Type (In Value %)

8.2. By End-User (In Value %)

8.3. By Charging Type (In Value %)

8.4. By Battery Type (In Value %)

8.5. By Region (In Value %)

9. Europe Electric Vans Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves mapping the ecosystem of the Europe Electric Vans market, identifying all stakeholders such as manufacturers, government bodies, and service providers. Extensive desk research, including the review of secondary and proprietary databases, was conducted to define key variables that impact the market.

Step 2: Market Analysis and Construction

In this phase, historical data pertaining to electric van sales, charging infrastructure, and adoption rates were compiled. A deep analysis of market penetration and revenue generation, especially in key sectors like logistics, was conducted to understand current market dynamics.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses were developed based on initial data findings and then validated through consultations with industry experts via CATIs (Computer Assisted Telephone Interviews). Insights from key stakeholders were used to confirm market trends and financial performance.

Step 4: Research Synthesis and Final Output

The final stage involved synthesizing research findings and consulting with electric van manufacturers to obtain detailed product segment insights. These interactions helped ensure the accuracy and comprehensiveness of the report, ensuring a validated and actionable analysis of the market.

Frequently Asked Questions

01. How big is the Europe Electric Vans Market?

The Europe Electric Vans market is valued at USD 3 billion, driven by strong regulatory support for emission reduction and increasing demand for eco-friendly transportation solutions.

02. What are the challenges in the Europe Electric Vans Market?

The primary challenges in Europe Electric Vans market include the high initial cost of electric vans, the limited availability of charging infrastructure, and concerns over battery range and vehicle performance in harsh weather conditions.

03. Who are the major players in the Europe Electric Vans Market?

Key players in Europe Electric Vans market include Daimler AG, Renault Group, Nissan Motor Co., Ltd., Volkswagen AG, and Ford Motor Company. These companies dominate due to their strong technological capabilities, established distribution networks, and strategic partnerships.

04. What are the growth drivers of the Europe Electric Vans Market?

Europe Electric Vans market is driven by regulatory initiatives promoting the adoption of zero-emission vehicles, advancements in battery technology, and the growing demand for electric vans in urban logistics and last-mile delivery services.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.