Global 3D Automotive Printing Market Outlook 2030

Region:Global

Author(s):Shivani Mehra

Product Code:KROD1669

November 2024

92

About the Report

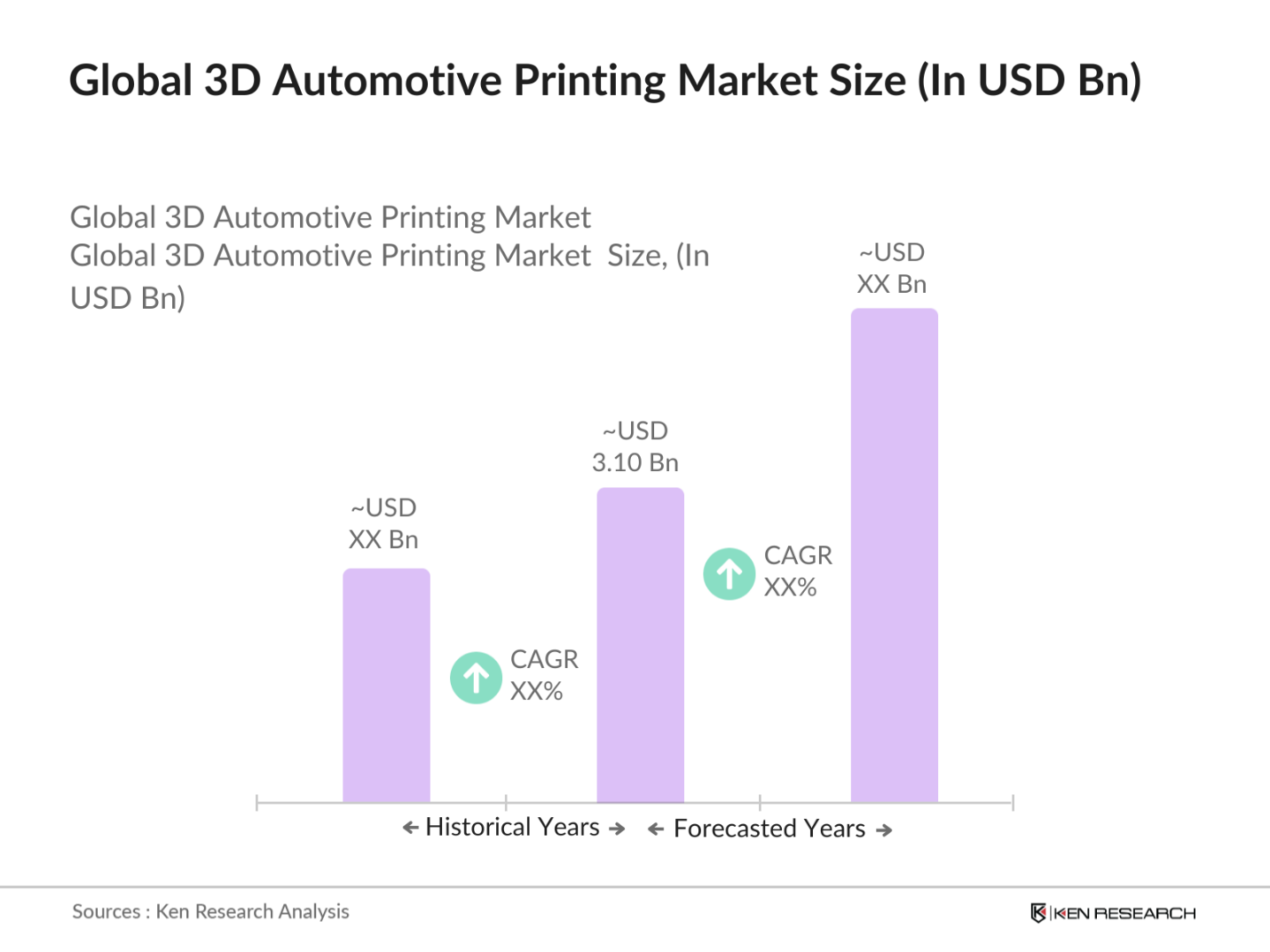

Global 3D Automotive Printing Market Overview

- The Global 3D Automotive Printing market is valued at USD 3.10 billion, based on a detailed analysis of recent market trends. This market is primarily driven by rapid advancements in additive manufacturing technologies, alongside the growing demand for customization in the automotive sector. Manufacturers are increasingly adopting 3D printing to produce more efficient, lightweight components, which helps reduce material waste and lower production costs. This technology is being widely used for end-use parts, prototypes, and manufacturing tools, contributing to its rising importance in the global automotive industry.

- Several cities and countries have emerged as dominant players in the 3D automotive printing market. The United States and Germany lead due to their advanced automotive sectors and technological innovation ecosystems. The U.S. is home to major 3D printing companies and has a high demand for electric vehicles (EVs), while Germanys strong automotive heritage and engineering expertise push the growth of 3D printed components in the production of premium vehicles.

- Governments are offering incentives for the adoption of green technologies in manufacturing, which is directly influencing the growth of 3D printing in the automotive sector. In 2023, the U.S. government launched a $500 million grant program aimed at companies integrating environmentally friendly technologies into their production lines. This includes the use of 3D printing to minimize waste and improve energy efficiency, particularly in automotive manufacturing, where such technologies are crucial for meeting sustainability goals.

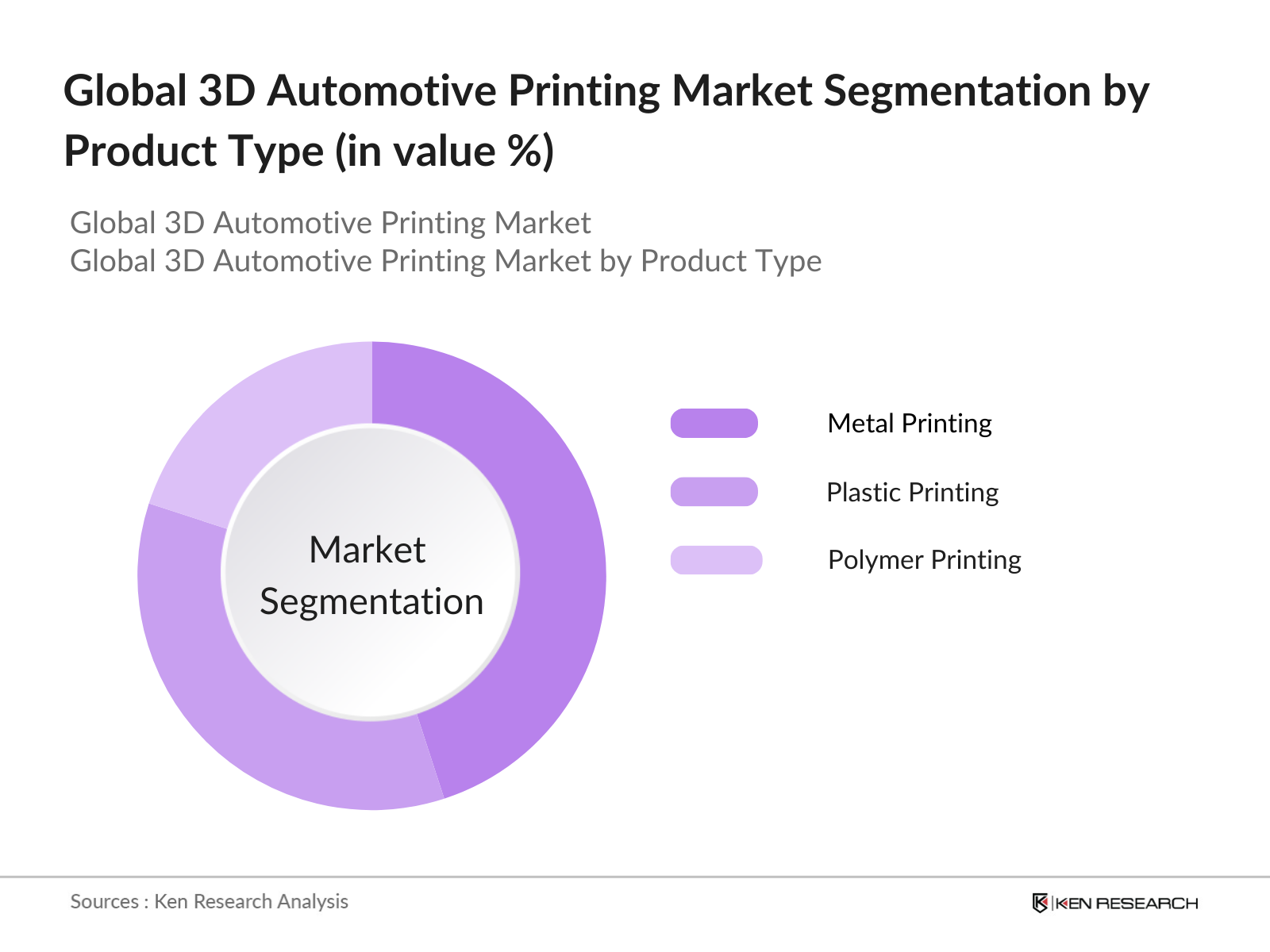

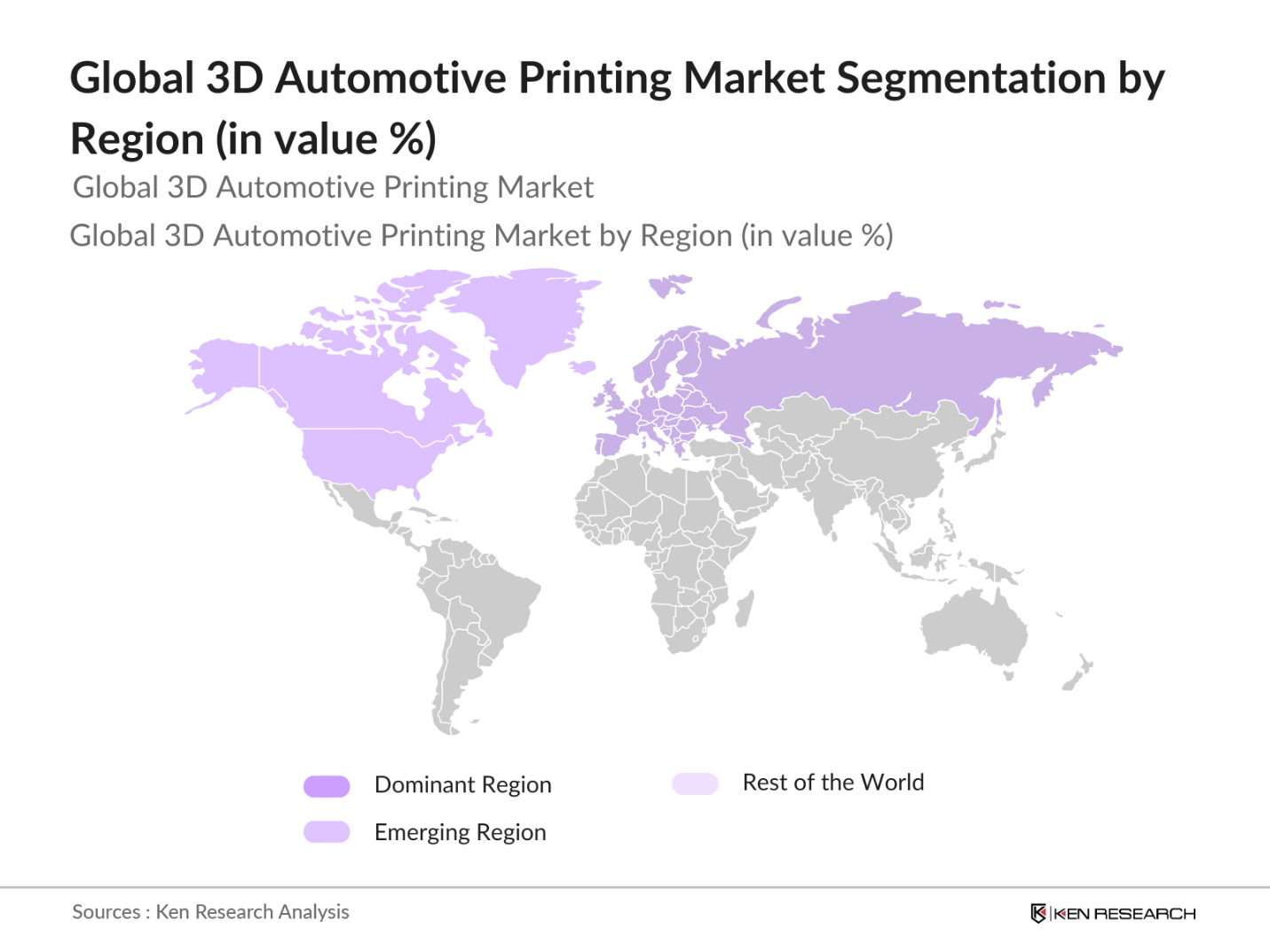

Global 3D Automotive Printing Market Segmentation

By Product Type: The 3D automotive printing market is segmented by product type into metal printing, plastic printing, and polymer printing. Metal printing dominates this segment due to the rising demand for lightweight metal components used in automotive manufacturing. This technology is preferred for producing durable and complex parts, such as engine components and heat exchangers, due to its strength and ability to withstand high temperatures.

By Region: The regional segmentation of the 3D automotive printing market includes North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. Europe dominates the market due to its robust automotive sector, high R&D investments, and government initiatives supporting green technology. The presence of premium car manufacturers like BMW, Audi, and Volkswagen further accelerates the adoption of 3D printing technologies.

Global 3D Automotive Printing Market Competitive Landscape

The 3D automotive printing market is highly competitive, with major players continuously innovating to gain a competitive edge. The market features a mix of established players and new entrants. Key companies are focusing on expanding their product portfolios, enhancing their manufacturing processes, and entering strategic collaborations to strengthen their market positions.

|

Company |

Establishment Year |

Headquarters |

Key Parameters |

|

Stratasys Ltd. |

1989 |

U.S. |

- |

|

3D Systems Corporation |

1986 |

U.S. |

- |

|

EOS GmbH |

1989 |

Germany |

- |

|

Voxeljet AG |

1999 |

Germany |

- |

|

HP Inc. |

1939 |

U.S. |

- |

Global 3D Automotive Printing Market Analysis

Global 3D Automotive Printing Market Growth Drivers

- Increasing Adoption of Lightweight Component: The automotive industry is increasingly shifting toward lightweight components to enhance fuel efficiency and performance. 3D printing technology allows manufacturers to design complex, lightweight parts that reduce vehicle weight significantly. According to the International Energy Agency (IEA), every 10-kilogram reduction in vehicle weight can result in a fuel savings of approximately 1.3 liters per 100 kilometers for light-duty vehicles. The ability to produce such components using 3D printing enables automakers to meet stringent fuel economy regulations and improve overall vehicle efficiency. This shift is particularly relevant as global fuel prices fluctuate, influencing cost-saving measures across industries.

- Customization Demand in Automotive Industry: As consumer preferences for personalized vehicles increase, 3D printing facilitates cost-effective customization. The ability to create tailor-made parts directly from digital models allows automakers to meet specific design and functional requirements without long production times. According to a 2023 report by the European Union, vehicle customization contributes significantly to sales, particularly in high-end markets where buyers are willing to pay more for personalized features. The automotive industry in Europe alone saw a 5% increase in demand for customized vehicle parts, primarily driven by 3D printing technologies.

- Adoption of Electric and Hybrid Vehicles: The growing electric vehicle (EV) market is closely tied to the adoption of 3D printing technology. EVs require complex, lightweight, and efficient components, which can be produced using 3D printing techniques. According to the International Energy Agency (IEA), global EV sales reached 10 million units in 2022, representing a surge in demand for innovative production methods, including 3D printing, to meet the material and design requirements for lightweight batteries and specialized parts. This trend is pushing the boundaries of automotive manufacturing, allowing for more efficient EV production.

Global 3D Automotive Printing Market Challenges

- High Equipment Costs: While 3D printing offers numerous benefits, the initial cost of acquiring advanced 3D printers remains a barrier for many manufacturers. The U.S. Bureau of Economic Analysis highlighted that 3D printers for industrial use can cost upwards of $500,000, limiting accessibility to small and mid-sized companies. This expense adds to the challenge of widespread adoption in the automotive industry, particularly for those focusing on short-term return on investment.

- Limited Material Options: Despite advancements in 3D printing, the range of materials suitable for automotive applications is still restricted. A 2023 study by the European Commission found that available materials in 3D printing are suitable for use in high-performance automotive components, restricting the technology's full potential. This limitation poses a challenge for manufacturers looking to produce parts that require high durability, heat resistance, or specific weight-to-strength ratios.

Global 3D Automotive Printing Market Future Outlook

The global 3D automotive printing market is expected to witness substantial growth, driven by the ongoing advancements in additive manufacturing technologies, a growing emphasis on lightweight components, and the increasing adoption of electric vehicles. The ability to reduce production time, lower costs, and minimize material wastage is also likely to propel the market forward. As more automotive manufacturers integrate 3D printing into their production processes, the market will continue to evolve, offering new opportunities for innovation and customization.

Market Opportunities:

- Use of Metal 3D Printing for End-Use Parts: Metal 3D printing is becoming a critical trend in automotive manufacturing, particularly for end-use parts that require high strength and durability. According to the U.S. Department of Commerce, metal 3D printing in the automotive sector has significantly advanced, enabling the production of components such as engine parts and structural elements, which require precise engineering and material properties. The growing use of metal 3D printing helps manufacturers reduce waste and meet stricter environmental regulations by producing parts that meet stringent durability and sustainability standards.

- Advancements in Additive Manufacturing Technologies: Advancements in additive manufacturing (AM) technologies, including faster printing speeds and higher material quality, are shaping the future of automotive production. The U.S. National Science Foundation (NSF) highlighted in a 2023 report that innovations in AM have significantly reduced printing times for large automotive parts, enabling manufacturers to accelerate production schedules. These advancements are also contributing to enhanced part quality, increasing the potential for 3D printing in mass production for complex and high-performance components.

Scope of the Report

|

By Product Type |

Metal Printing Plastic Printing Polymer Printing |

|

By Vehicle Type |

Passenger Vehicles Commercial Vehicles Electric Vehicles |

|

By Printing Technology |

Stereolithography (SLA) Selective Laser Sintering (SLS) Fused Deposition Modeling (FDM) Digital Light Processing (DLP) |

|

By Material Type |

Metals Polymers Ceramics Composites |

|

By Region |

North-East Midwest West Coast Southern States |

Products

Key Target Audience

Automotive OEMs

Tier-1 Suppliers

Automotive Component Manufacturers

3D Printing Technology Providers

Material Suppliers

Investments and Venture Capitalist Firms

Government and Regulatory Bodies (U.S. Department of Transportation, European Commission)

Electric Vehicle Manufacturers

Companies

Players Mention in the Report

Stratasys Ltd.

3D Systems Corporation

EOS GmbH

Voxeljet AG

HP Inc.

Autodesk Inc.

SLM Solutions Group AG

Materialise NV

ExOne Company

Protolabs, Inc.

GE Additive

Carbon, Inc.

Desktop Metal, Inc.

Renishaw PLC

Ultimaker BV

Table of Contents

01. Global 3D Automotive Printing Market Overview

1.1. Definition and Scope

1.2. Market Valuation and Historical Analysis

1.3. Key Market Developments and Milestones

02. Global 3D Automotive Printing Market Size (In USD Billion)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Major Trends Impacting Market Growth

03. Global 3D Automotive Printing Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Adoption of Lightweight Components

3.1.2. Customization Demand in Automotive Industry

3.1.3. Adoption of Electric and Hybrid Vehicles

3.2. Market Challenges

3.2.1. High Equipment Costs

3.2.2. Limited Material Options

3.3. Market Opportunities

3.3.1. Use of Metal 3D Printing for End-Use Parts

3.3.2. Advancements in Additive Manufacturing Technologies

3.4. Future Trends

3.4.1. Integration with Digital Platforms

3.4.2. Enhanced Production Efficiency

04. Global 3D Automotive Printing Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Metal Printing

4.1.2. Plastic Printing

4.1.3. Polymer Printing

4.2. By Vehicle Type (In Value %)

4.2.1. Passenger Vehicles

4.2.2. Commercial Vehicles

4.2.3. Electric Vehicles

4.3. By Printing Technology (In Value %)

4.3.1. Stereolithography (SLA)

4.3.2. Selective Laser Sintering (SLS)

4.3.3. Fused Deposition Modeling (FDM)

4.3.4. Digital Light Processing (DLP)

4.4. By Material Type (In Value %)

4.4.1. Metals

4.4.2. Polymers

4.4.3. Ceramics

4.4.4. Composites

4.5. By Region (In Value %)

4.5.1. North-East

4.5.2. Midwest

4.5.3. West Coast

4.5.4. Southern States

05. Global 3D Automotive Printing Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Stratasys Ltd.

5.1.2. 3D Systems Corporation

5.1.3. EOS GmbH

5.1.4. Voxeljet AG

5.1.5. HP Inc.

5.1.6. Autodesk Inc.

5.1.7. SLM Solutions Group AG

5.1.8. Materialise NV

5.1.9. ExOne Company

5.1.10. Protolabs, Inc.

5.1.11. GE Additive

5.1.12. Carbon, Inc.

5.1.13. Desktop Metal, Inc.

5.1.14. Renishaw PLC

5.1.15. Ultimaker BV

5.2. Cross Comparison Parameters (Key Parameters, R&D Investment, Market Reach)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

06. Global 3D Automotive Printing Market Regulatory Framework

6.1. Compliance Standards and Environmental Regulations

6.2. Health and Safety Standards

07. Global 3D Automotive Printing Market Future Outlook

7.1. Future Market Size Projections (In USD Billion)

7.2. Key Factors Driving Future Market Growth

08. Global 3D Automotive Printing Market Future Segmentation

8.1. By Product Type (In Value %)

8.2. By Vehicle Type (In Value %)

8.3. By Printing Technology (In Value %)

8.4. By Material Type (In Value %)

8.5. By Region (In Value %)

09. Global 3D Automotive Printing Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Market Entry Strategies

9.3. Key Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The research begins with mapping out the ecosystem of the 3D automotive printing market. This phase focuses on identifying and analyzing the primary stakeholders, including automotive OEMs, 3D printing manufacturers, material suppliers, and regulatory bodies. Secondary research from government databases, industry journals, and proprietary sources is used to assess the market's key influencing factors.

Step 2: Market Analysis and Construction

Historical data and market penetration trends are compiled for the 3D automotive printing market. This step involves analyzing data on the number of installations, production volumes, and revenue generation across regions. A detailed examination of material types, printing technologies, and applications is also conducted to ensure the reliability of revenue projections.

Step 3: Hypothesis Validation and Expert Consultation

Interviews with industry experts from automotive manufacturers and 3D printing technology providers are carried out to validate the market assumptions. These consultations provide insights into operational challenges, emerging trends, and new growth opportunities, ensuring the accuracy of the research.

Step 4: Research Synthesis and Final Output

The final phase includes engaging with key automotive players and industry stakeholders to acquire specific data on product usage, sales, and material consumption. This stage also incorporates feedback from market experts to corroborate the findings and provide a comprehensive analysis of the 3D automotive printing market.

Frequently Asked Questions

01. How big is the Global 3D Automotive Printing Market?

The global 3D automotive printing market was valued at USD 3.10 billion, driven by the demand for customization, lightweight materials, and the rise of electric vehicles.

02. What are the challenges in the 3D Automotive Printing Market?

Challenges include high costs of 3D printing technology, limited material availability, and a lack of standardization across the industry. Additionally, scaling production for mass-market vehicles remains an obstacle.

03. Who are the major players in the Global 3D Automotive Printing Market?

Key players in the market include Stratasys Ltd., 3D Systems Corporation, EOS GmbH, Voxeljet AG, and HP Inc., known for their innovation in printing technologies and materials.

04. What are the growth drivers of the Global 3D Automotive Printing Market?

The market is propelled by advancements in additive manufacturing technologies, growing demand for electric vehicles, and the need for lightweight automotive components to enhance fuel efficiency.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.