Global Advanced Driver Assistance Systems (ADAS) Market Outlook to 2030

Region:Global

Author(s):Sanjna

Product Code:KROD4142

November 2024

94

About the Report

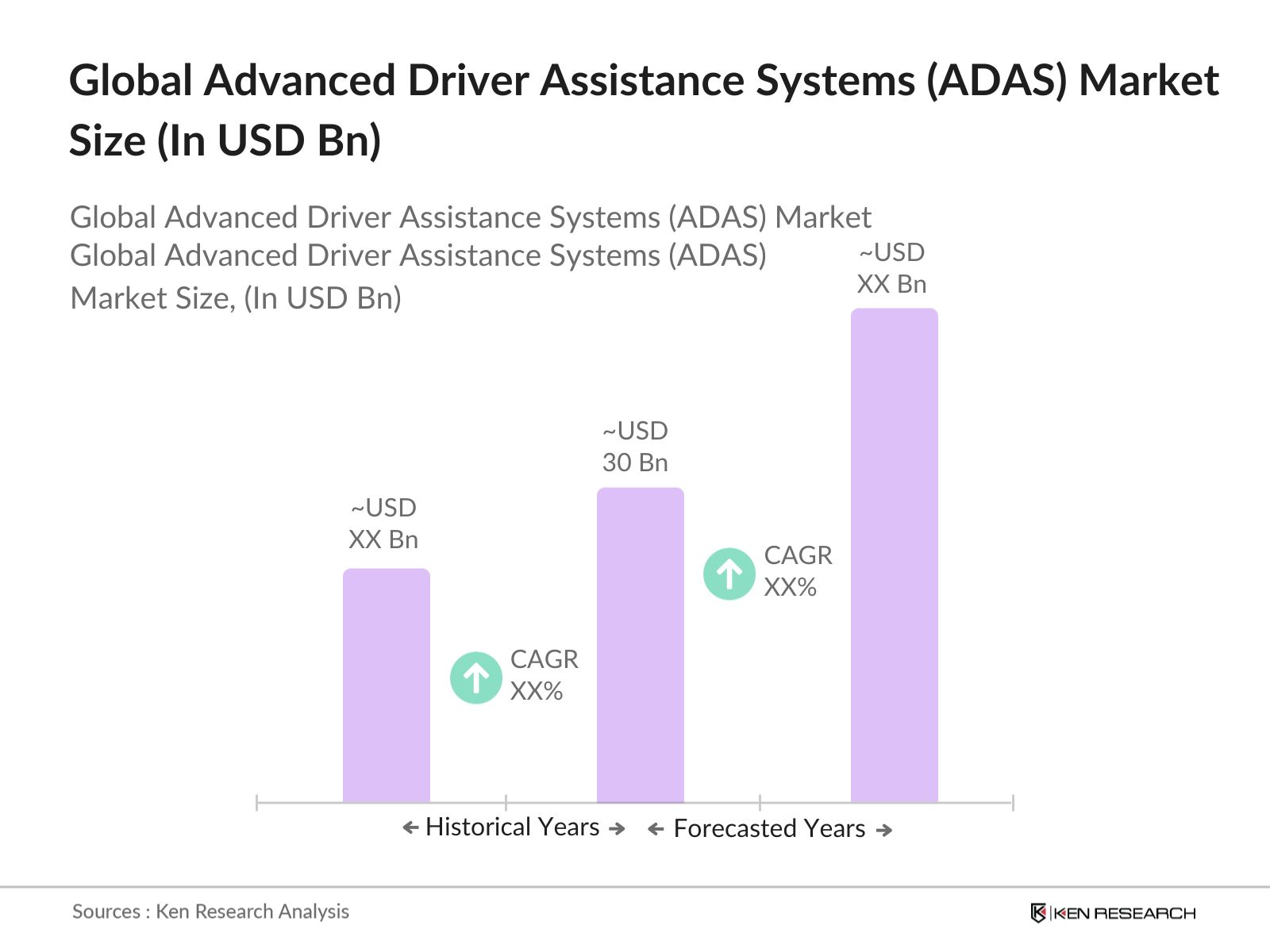

Global Advanced Driver Assistance Systems (ADAS) Market Overview

- The global ADAS market is valued at USD 30 billion, supported by strong growth in sensor technologies, artificial intelligence, and autonomous driving features. This market has seen rapid expansion due to the growing consumer demand for safety features in vehicles, particularly in premium and mid-range passenger cars. The inclusion of technologies like radar, LiDAR, and cameras is propelling the market, driven by a shift toward semi-autonomous and fully autonomous driving systems.

- Key regions such as North America, Europe, and Asia-Pacific dominate the ADAS market due to their high adoption rates of advanced automotive technologies and a robust automotive manufacturing infrastructure. In particular, countries like the United States, Germany, and Japan lead in the ADAS market due to the strong presence of original equipment manufacturers (OEMs) and Tier 1 suppliers. Additionally, stringent vehicle safety regulations and increasing R&D investments in autonomous driving technologies contribute to their dominance.

- Governments and regulatory bodies have established rigorous safety standards to promote ADAS adoption. The European Union, under its General Safety Regulation (GSR), mandates that all new vehicles must include certain ADAS features like automatic emergency braking (AEB) and lane-keeping assistance by 2024. In the U.S., the National Highway Traffic Safety Administration (NHTSA) also requires ADAS features in vehicles to meet federal safety standards. The EU has set a target to reduce road deaths by 50% by 2030, heavily relying on ADAS technologies to achieve this. Compliance with these regulations will drive significant market demand in both regions.

Global Advanced Driver Assistance Systems (ADAS) Market Segmentation

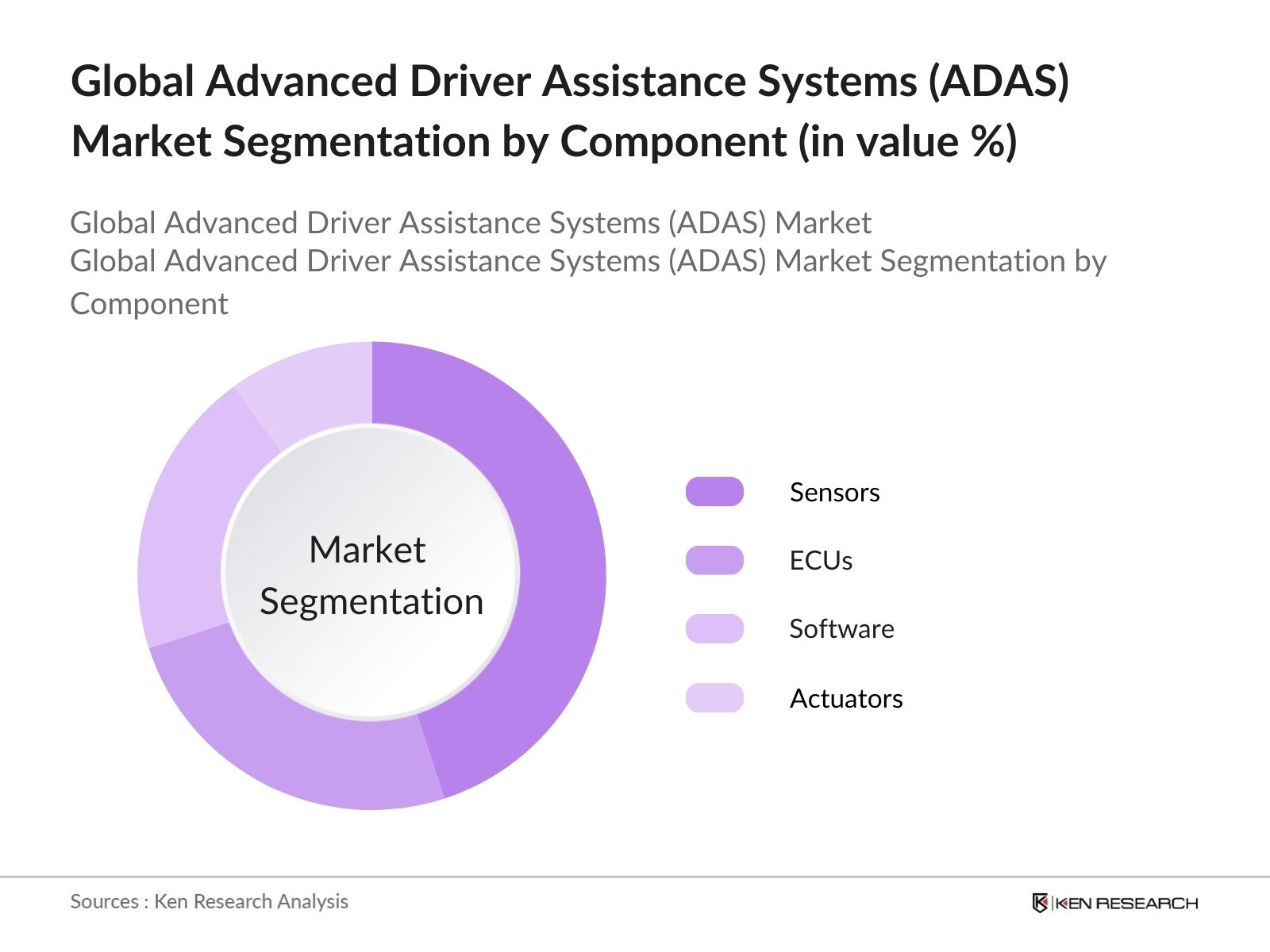

By Component: The global ADAS market is segmented by component into sensors, ECUs (Electronic Control Units), software, and actuators. Sensors, including radar, LiDAR, and cameras, are leading the market due to their critical role in enabling advanced safety functions such as automatic emergency braking, adaptive cruise control, and lane-keeping assistance. The rising demand for accurate, high-speed data processing in autonomous vehicles further strengthens the need for sophisticated sensors.

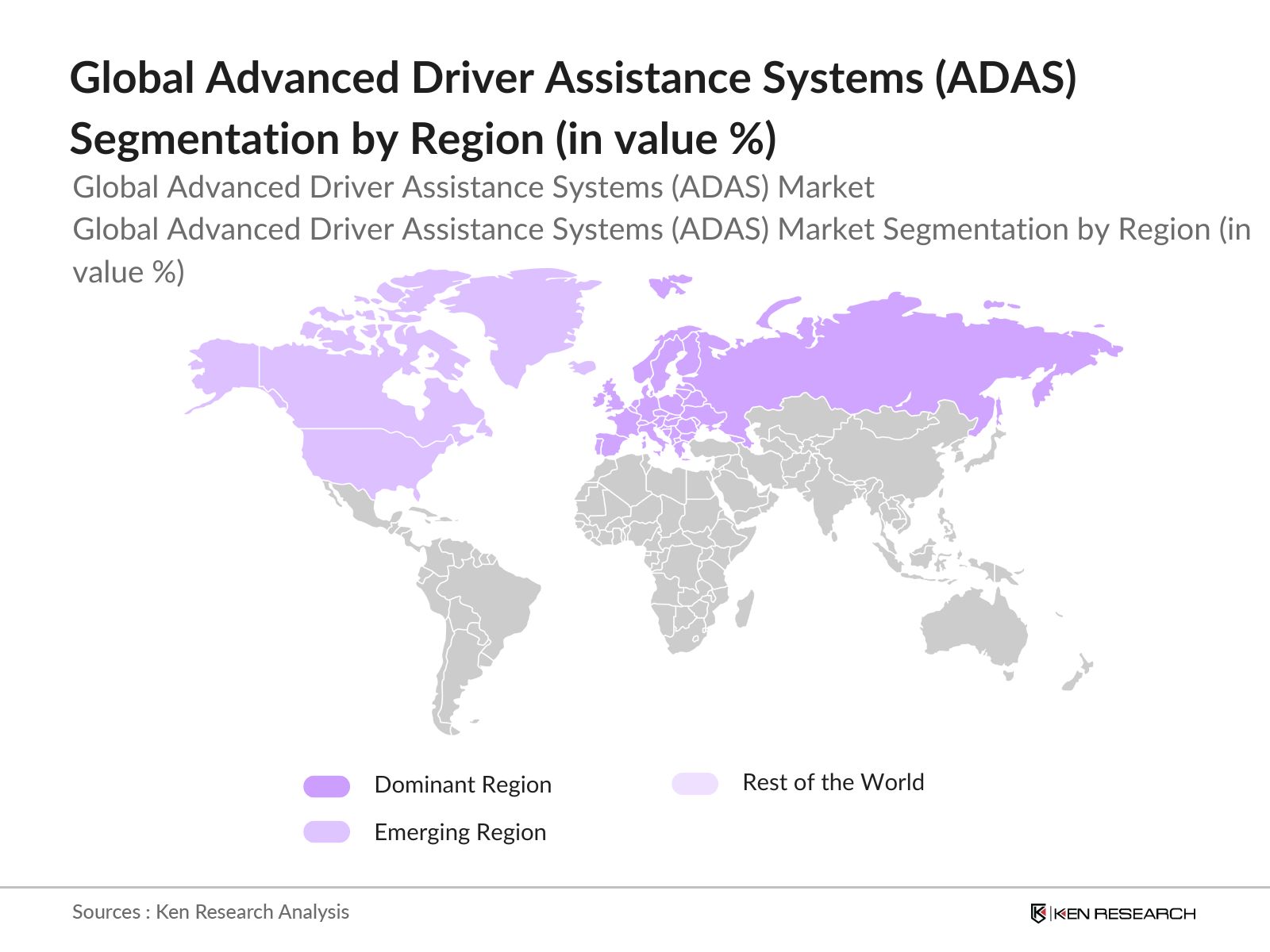

By Region: The ADAS market is regionally segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Europe leads the ADAS market due to stringent regulatory mandates that require the inclusion of various safety features in new vehicles. This is followed closely by North America, where consumer demand for safety features and advanced driver assistance technologies is surging. Asia-Pacific, led by China and Japan, is growing rapidly, driven by the increasing production and sales of automobiles in the region, coupled with governmental support for vehicle safety innovations.

By Region: The ADAS market is regionally segmented into North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Europe leads the ADAS market due to stringent regulatory mandates that require the inclusion of various safety features in new vehicles. This is followed closely by North America, where consumer demand for safety features and advanced driver assistance technologies is surging. Asia-Pacific, led by China and Japan, is growing rapidly, driven by the increasing production and sales of automobiles in the region, coupled with governmental support for vehicle safety innovations.

By System Type: The global ADAS market is segmented by system type into adaptive cruise control (ACC), lane departure warning (LDW), autonomous emergency braking (AEB), parking assistance, and blind-spot detection (BSD). Autonomous emergency braking holds the highest market share due to growing regulations mandating its installation in both passenger and commercial vehicles. With safety being a priority, AEB systems are now integrated as standard in most modern cars, significantly reducing rear-end collisions. This trend, driven by regulatory requirements, especially in Europe and North America, reinforces the demand for AEB systems, giving them a competitive edge in the market.

Global Advanced Driver Assistance Systems (ADAS) Market Competitive Landscape

The ADAS market is characterized by intense competition among global automotive OEMs and suppliers. The market is dominated by key players such as Bosch, Continental, and ZF Friedrichshafen, which hold significant market shares due to their technological innovations and strong partnerships with automotive manufacturers. Additionally, semiconductor companies like Nvidia and Intel Mobileye are emerging as critical players by providing the computing power and AI technologies required for advanced ADAS solutions.

|

Company |

Establishment Year |

Headquarters |

Market Penetration |

Partnerships |

R&D Spending |

ADAS Portfolio |

Geographical Presence |

Patents Filed |

|

Bosch |

1886 |

Germany |

- |

- |

- |

- |

- |

- |

|

Continental AG |

1871 |

Germany |

- |

- |

- |

- |

- |

- |

|

ZF Friedrichshafen AG |

1915 |

Germany |

- |

- |

- |

- |

- |

- |

|

Nvidia Corporation |

1993 |

USA |

- |

- |

- |

- |

- |

- |

|

Intel Mobileye |

1999 |

Israel |

- |

- |

- |

- |

- |

- |

Global Advanced Driver Assistance Systems (ADAS) Market Analysis

Growth Drivers

- Technological Advancements: According to the U.S. Department of Transportation, the integration of sensors and control systems has improved vehicle response times and accuracy in detecting obstacles by over 35% since 2020. The average response time for an ADAS-enabled vehicle is now approximately 100 milliseconds, significantly reducing the chances of accidents. This technological progress is critical, as it reduces road traffic injuries, which accounted for 1.35 million deaths globally in 2023.

- Consumer Safety Demand: Consumer demand for safety features has surged, with 75% of drivers in the U.S. citing safety as the primary reason for choosing ADAS-enabled vehicles. The National Highway Traffic Safety Administration (NHTSA) reported that in 2023, vehicles equipped with ADAS systems showed a 15% reduction in fatal crashes compared to non-equipped vehicles. These systems have been especially effective in reducing collisions related to lane departures and automatic braking scenarios, contributing to a marked decrease in road fatalities in developed markets like the EU and the U.S.

- Regulatory Standards: Government mandates have played a crucial role in accelerating ADAS deployment. The European Union made ADAS mandatory for all new vehicles starting in 2022, covering features like lane-keeping assist and emergency braking systems. By 2024, compliance rates are expected to reach nearly 90% in the region, significantly boosting safety. Similarly, the U.S. NHTSA estimates that approximately 96% of passenger vehicles in 2024 will feature at least one ADAS component, helping meet national road safety objectives.

Challenges

- High Development and Installation Costs: The high cost of developing and installing ADAS systems remains a major barrier, especially in emerging markets. A 2023 report by the World Bank indicates that the average cost of a full ADAS suite is around $3,000 per vehicle, which limits its adoption in lower-income regions. This is especially problematic for markets in Southeast Asia and Africa, where affordability is a key concern. As a result, the penetration of ADAS in these markets remains below 5%.

- Lack of Standardization Across Manufacturers: The lack of standardization across different manufacturers ADAS systems creates compatibility issues. In 2023, the International Organization for Standardization (ISO) reported that only 30% of global automotive manufacturers adhere to common standards for ADAS technologies, leading to fragmented system performance. This disparity hinders the seamless integration of ADAS features across vehicle platforms and increases development costs for cross-compatible systems.

Global Advanced Driver Assistance Systems (ADAS) Market Future Outlook

Global ADAS market is projected to experience robust growth driven by advancements in sensor technologies, increased vehicle automation, and strong government regulations promoting vehicle safety. The integration of artificial intelligence (AI) and machine learning (ML) to enhance real-time object detection and decision-making capabilities in ADAS systems is expected to create significant market opportunities. Furthermore, as automotive manufacturers continue to incorporate higher levels of automation, the demand for more sophisticated ADAS features will surge, particularly in the commercial vehicle segment.

Market Opportunities

- Emerging Markets: Emerging markets present significant growth opportunities for ADAS adoption. The World Bank highlighted that vehicle ownership in regions like Southeast Asia and Latin America increased by 10 million units in 2023, driven by rising incomes and urbanization. Governments in these regions are also initiating road safety programs that mandate ADAS for new vehicle registrations, creating a favorable environment for market expansion. This is especially relevant in countries like Brazil and India, where ADAS adoption is expected to grow significantly due to new regulatory frameworks.

- Next-Gen ADAS Systems: The development of next-gen ADAS systems, which include enhanced AI capabilities and 5G integration, offers substantial growth potential. As of 2024, countries like South Korea and Japan have deployed over 50,000 5G-enabled vehicles, supporting real-time communication for ADAS systems. This technological shift allows for faster data processing and enhanced vehicle-to-vehicle (V2V) communication, further improving the performance of ADAS in high-speed environments.

Scope of the Report

|

Segment |

Sub-Segments |

|

By Component |

Sensors ECUs Software Actuators |

|

By System Type |

Adaptive Cruise Control Lane Departure Warning Autonomous Emergency Braking Parking Assistance Blind Spot Detection |

|

By Vehicle Type |

Passenger Vehicles Commercial Vehicles Electric Vehicles |

|

By Level of Automation |

Level 0 No Automation Level 1 Driver Assistance Level 2 Partial Automation Level 3 Conditional Automation Level 4/5 High/Full Automation |

|

By Region |

North America Europe Asia-Pacific Latin America Middle East & Africa |

Products

Key Target Audience

Automotive OEMs

Tier 1 and Tier 2 Suppliers

ADAS Technology Providers

Semiconductor Manufacturers

Artificial Intelligence and Machine Learning Companies

Autonomous Vehicle Developers

Investors and Venture Capitalist Firms

Government and Regulatory Bodies (e.g., National Highway Traffic Safety Administration, European Commission)

Companies

Players Mentioned in the Report

Bosch

Continental AG

ZF Friedrichshafen AG

Magna International

Aptiv PLC

Veoneer Inc.

Valeo

Denso Corporation

Nvidia Corporation

Intel Mobileye

Table of Contents

1. Global Advanced Driver Assistance Systems (ADAS) Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Global ADAS Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Global ADAS Market Analysis

3.1. Growth Drivers

3.1.1. Technological Advancements

3.1.2. Consumer Safety Demand

3.1.3. Regulatory Standards

3.1.4. Integration of AI and Machine Learning

3.1.5. Increasing Demand for Autonomous Vehicles

3.1.6. Government Regulations on Vehicle Safety

3.1.7. Rising Consumer Awareness and Preference for Safety Features

3.2. Market Challenges

3.2.1. High Development and Installation Costs

3.2.2. Lack of Standardization Across Manufacturers

3.2.3. Data Privacy and Security Concerns

3.3. Opportunities

3.3.1. Emerging Markets

3.3.2. Next-Gen ADAS Systems

3.3.3. Sensor Fusion Technology

3.3.4. Expansion of V2X Communication

3.4. Trends

3.4.1. ADAS Penetration in Mid-range Vehicles

3.4.2. Integration with EV Platforms

3.4.3. Sensor Technology Advancements (Radar, LiDAR, Cameras)

3.5. Regulatory Landscape

3.5.1. National and Regional Safety Standards (NCAP, NHTSA, EU Regulations)

3.5.2. Emission Norms and Autonomous Vehicle Testing Regulations

3.5.3. Industry Collaborations with Government and Testing Bodies

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (OEMs, Tier 1 Suppliers, Technology Providers, Regulators)

3.8. Porters Five Forces Analysis

3.9. Competitive Ecosystem

4. Global ADAS Market Segmentation

4.1. By Component (In Value %)

4.1.1. Sensors (Radar, LiDAR, Camera, Ultrasonic)

4.1.2. ECUs (Electronic Control Units)

4.1.3. Software (Perception Algorithms, Machine Learning, Data Analytics)

4.1.4. Actuators

4.2. By System Type (In Value %)

4.2.1. Adaptive Cruise Control (ACC)

4.2.2. Lane Departure Warning (LDW)

4.2.3. Autonomous Emergency Braking (AEB)

4.2.4. Parking Assistance

4.2.5. Blind Spot Detection (BSD)

4.3. By Vehicle Type (In Value %)

4.3.1. Passenger Vehicles

4.3.2. Commercial Vehicles

4.3.3. Electric Vehicles (EVs)

4.4. By Level of Automation (In Value %)

4.4.1. Level 0 No Automation

4.4.2. Level 1 Driver Assistance

4.4.3. Level 2 Partial Automation

4.4.4. Level 3 Conditional Automation

4.4.5. Level 4/5 High/Full Automation

4.5. By Region (In Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia-Pacific

4.5.4. Latin America

4.5.5. Middle East & Africa

5. Global ADAS Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Bosch

5.1.2. Continental AG

5.1.3. ZF Friedrichshafen AG

5.1.4. Magna International

5.1.5. Aptiv PLC

5.1.6. Veoneer Inc.

5.1.7. Valeo

5.1.8. Denso Corporation

5.1.9. Nvidia Corporation

5.1.10. Intel Mobileye

5.2. Cross Comparison Parameters (Revenue, Market Share, R&D Spending, Partnerships/Collaborations, Technological Innovations, Patent Portfolio, Regional Footprint, Product Portfolio)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. Global ADAS Market Regulatory Framework

6.1. Vehicle Safety Standards

6.2. ADAS Compliance and Certification Requirements

6.3. Testing Procedures for Autonomous Driving Features

7. Global ADAS Future Market Size (In USD Mn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Global ADAS Future Market Segmentation

8.1. By Component (In Value %)

8.2. By System Type (In Value %)

8.3. By Vehicle Type (In Value %)

8.4. By Level of Automation (In Value %)

8.5. By Region (In Value %)

9. Global ADAS Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The first phase involves mapping the entire ADAS market ecosystem, identifying major stakeholders, including automotive manufacturers, suppliers, technology providers, and regulators. Extensive desk research is conducted using secondary and proprietary databases to identify key market variables such as technological advancements, regulatory requirements, and consumer demand.

Step 2: Market Analysis and Construction

Historical market data is analyzed to assess market penetration, vehicle sales, and ADAS feature integration in different regions. Data on vehicle safety regulations and compliance requirements are gathered to estimate revenue and market growth. Further analysis is conducted to evaluate the ratio of ADAS adoption across passenger and commercial vehicles.

Step 3: Hypothesis Validation and Expert Consultation

Interviews are conducted with industry experts, including senior executives from automotive OEMs, ADAS suppliers, and regulatory bodies. These consultations provide operational and financial insights to validate the market hypotheses and further refine the revenue estimates.

Step 4: Research Synthesis and Final Output

The final phase involves synthesizing data collected from secondary research and expert interviews. The findings are verified through bottom-up and top-down approaches to ensure the accuracy and comprehensiveness of the market data. The validated report includes detailed market segmentation, competitive analysis, and future market outlook.

Frequently Asked Questions

01. How big is the Global ADAS market?

Global ADAS market is valued at USD 30 billion, driven by increasing vehicle safety regulations and technological advancements in autonomous driving.

02. What are the challenges in the ADAS market?

Key challenges in Global ADAS market include the high cost of ADAS systems, lack of standardization, and data privacy concerns associated with real-time data processing in autonomous vehicles.

03. Who are the major players in the ADAS market?

Major players in Global ADAS market include Bosch, Continental AG, ZF Friedrichshafen, Nvidia, and Intel Mobileye, which dominate due to their innovation in sensor technology and strong partnerships with automotive manufacturers.

04. What are the growth drivers of the ADAS market?

Global ADAS market is propelled by stringent vehicle safety regulations, consumer demand for safety features, and advancements in AI and sensor technologies that enhance the capabilities of ADAS systems.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.