Global Aircraft Hangar Market Outlook 2030

Region:Global

Author(s):Shivani Mehra

Product Code:KROD2984

Region:Global

Author(s):Shivani Mehra

Product Code:KROD2984

November 2024

94

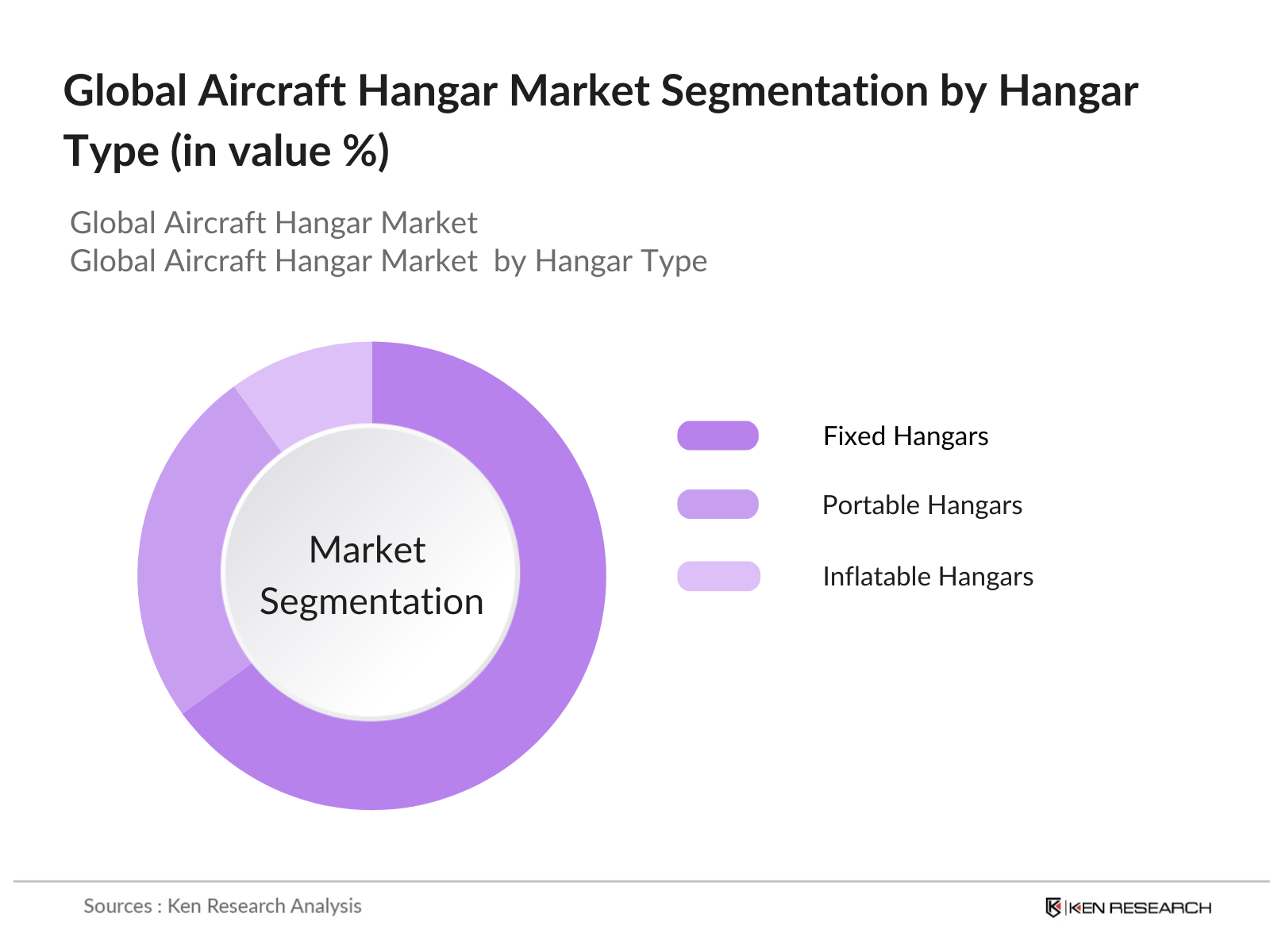

By Hangar Type: The global aircraft hangar market is segmented by hangar type into fixed hangars, portable hangars, and inflatable hangars. Fixed hangars hold the dominant market share due to their long-standing presence in large airports and military bases. Their durability, security features, and ability to accommodate a wide range of aircraft sizes contribute to their widespread use, particularly in developed markets such as North America and Europe.

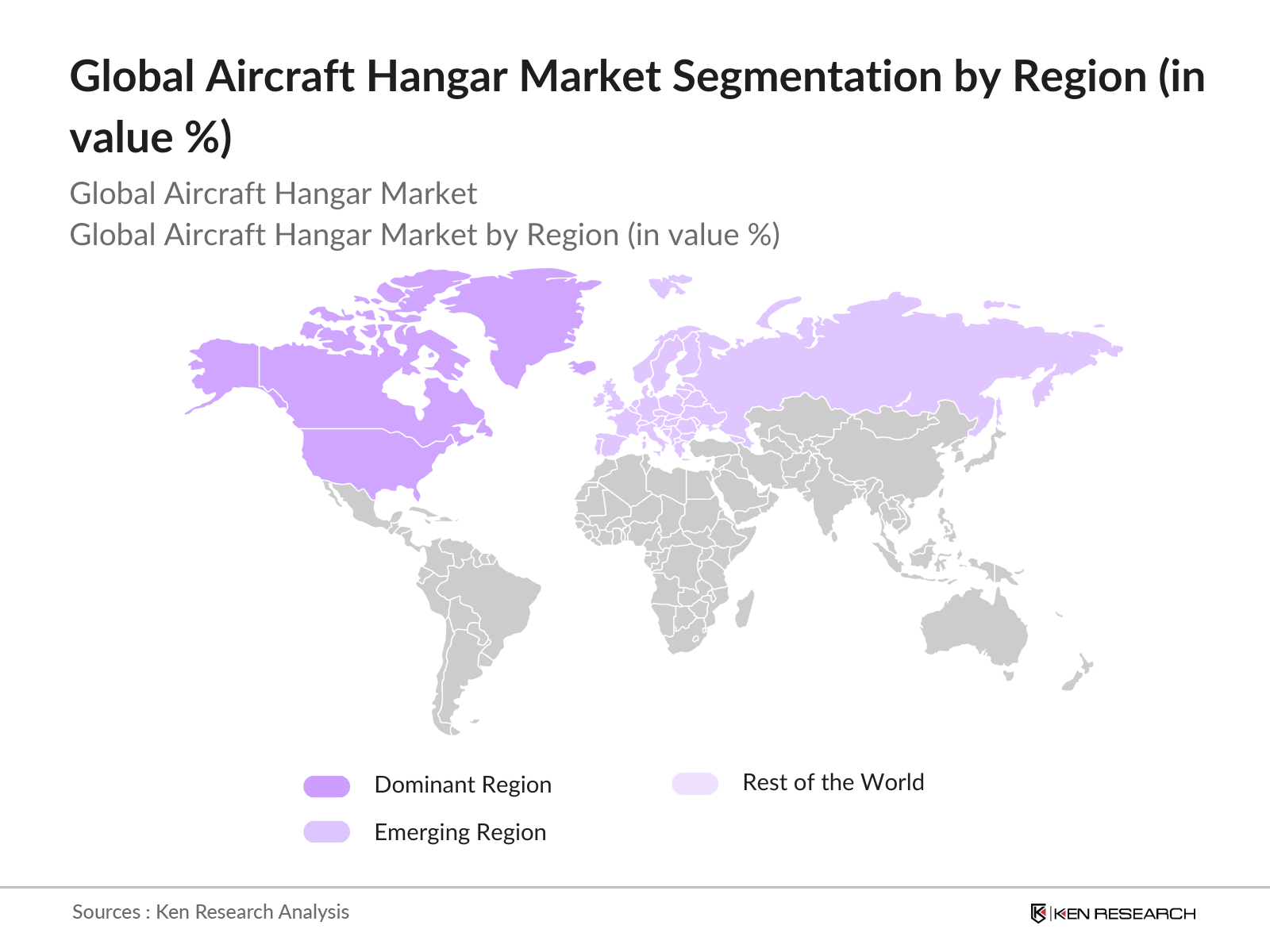

By Region: The global aircraft hangar market is segmented by region into North America, Europe, Asia-Pacific, the Middle East, and Latin America. North America dominates the market due to its advanced aviation industry, presence of major aircraft manufacturers, and the regions extensive network of commercial and military airports. The United States plays a critical role in driving growth within this region, supported by government investments and military spending.

The global aircraft hangar market is highly consolidated, with a few key players dominating the market. Major players include construction giants and aviation infrastructure companies that have extensive experience in building and maintaining hangar facilities. These companies are heavily involved in both the commercial and defense aviation sectors, ensuring a steady flow of projects globally.

|

Company Name |

Year of Establishment |

Headquarters |

Hangar Types Offered |

Annual Revenue |

Global Presence |

Specialization |

Number of Employees |

Key Projects |

|

AECOM |

1990 |

Los Angeles, USA |

- |

- |

- |

- |

- |

- |

|

Butler Manufacturing |

1901 |

Kansas City, USA |

- |

- |

- |

- |

- |

- |

|

Rubb Buildings Ltd |

1977 |

Gateshead, UK |

- |

- |

- |

- |

- |

- |

|

Erect-A-Tube Inc. |

1964 |

Harvard, USA |

- |

- |

- |

- |

- |

- |

|

Megadoor (ASSA ABLOY Group) |

1998 |

Landskrona, Sweden |

- |

- |

- |

- |

- |

- |

Market Challenges

Over the next five years, the global aircraft hangar market is expected to witness significant growth driven by the expansion of airport infrastructure, increasing demand for MRO services, and rising investments in green building technologies. The implementation of smart hangars, featuring automation and IoT integration, is anticipated to streamline operations and enhance safety. Furthermore, emerging markets in the Middle East and Asia-Pacific are projected to offer lucrative opportunities for growth due to the rapid expansion of their aviation sectors and rising air traffic.

Market Opportunities:

|

By Hangar Type |

Fixed Hangars, Portable Hangars Inflatable Hangars |

|

By Aircraft Type |

Commercial Aircraft Military Aircraft Private Jets Helicopters |

|

By Material Type |

Steel Aluminum Composite Materials |

|

By Construction Type |

New Construction Renovation |

|

By Region |

North America Europe Asia-Pacific Middle East Latin America |

Players Mention in the Report

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Increase in Air Traffic (Commercial, Defense, Private)

3.1.2. Expansion of Airport Infrastructure (New Airport Projects, Airport Modernization)

3.1.3. Growth in MRO (Maintenance, Repair, and Overhaul) Activities

3.1.4. Government Initiatives (Infrastructure Funding, Public-Private Partnerships)

3.2. Market Challenges

3.2.1. High Initial Capital Investment (Land Acquisition, Construction Costs)

3.2.2. Stringent Regulatory Requirements (FAA, EASA, ICAO Standards)

3.2.3. Fluctuations in Raw Material Prices (Steel, Aluminum)

3.3. Opportunities

3.3.1. Increasing Demand for Smart Hangars (Automation, IoT Integration)

3.3.2. Growth in Emerging Markets (Middle East, Asia-Pacific)

3.3.3. Rising Demand for Green Hangars (Energy Efficiency, Sustainable Building Materials)

3.4. Trends

3.4.1. Integration of AI & IoT for Predictive Maintenance (Smart Hangar Systems)

3.4.2. Modular Hangar Solutions (Scalable Designs, Rapid Construction)

3.4.3. Use of Renewable Energy (Solar Panels, Wind Power)

3.5. Government Regulations

3.5.1. ICAO Compliance (Safety and Environmental Standards)

3.5.2. Airport Infrastructure Development Policies (Funding, Approvals)

3.5.3. Zoning and Environmental Impact Laws

3.5.4. Fire Safety Standards and Certification (NFPA 409)

3.6. SWOT Analysis

3.7. Stake Ecosystem

3.7.1. Hangar Construction Companies

3.7.2. Material Suppliers (Steel, Concrete, Insulation)

3.7.3. MRO Service Providers

3.8. Porters Five Forces

3.9. Competition Ecosystem

4.1. By Hangar Type (In Value %)

4.1.1. Fixed Hangars

4.1.2. Portable Hangars

4.1.3. Inflatable Hangars

4.2. By Aircraft Type (In Value %)

4.2.1. Commercial Aircraft

4.2.2. Military Aircraft

4.2.3. Private Jets

4.2.4. Helicopters

4.3. By Material Type (In Value %)

4.3.1. Steel

4.3.2. Aluminum

4.3.3. Composite Materials

4.4. By Construction Type (In Value %)

4.4.1. New Construction

4.4.2. Renovation

4.5. By Region (In Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia-Pacific

4.5.4. Middle East

4.5.5. Latin America

5.1. Detailed Profiles of Major Companies

5.1.1. AECOM

5.1.2. Butler Manufacturing

5.1.3. Rubb Buildings Ltd

5.1.4. Erect-A-Tube Inc.

5.1.5. AAR Corp.

5.1.6. Alvan Blanch Development Company

5.1.7. Reid Steel

5.1.8. Fabritecture

5.1.9. Megadoor (ASSA ABLOY Group)

5.1.10. Alaska Structures

5.1.11. Fulfab Inc.

5.1.12. John Reid & Sons Ltd

5.1.13. Sprung Structures

5.1.14. Norco Manufacturing

5.1.15. Big Top Manufacturing Inc.

5.2. Cross Comparison Parameters (Hangar Size, Aircraft Type, Revenue, No. of Hangars Constructed, Headquarters, No. of Employees, Material Expertise, Geographic Presence)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Safety and Security Standards

6.2. Zoning and Building Codes

6.3. Environmental Impact Regulations

6.4. Fire Safety and Hazard Controls

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Hangar Type (In Value %)

8.2. By Aircraft Type (In Value %)

8.3. By Material Type (In Value %)

8.4. By Construction Type (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsThe initial step involves mapping the entire ecosystem of stakeholders within the global aircraft hangar market. Extensive desk research, supplemented by secondary and proprietary databases, is conducted to gather comprehensive industry information. This step helps to identify the critical variables influencing the market, such as technological advancements, raw material pricing, and regulatory requirements.

In this phase, historical data for the global aircraft hangar market is compiled and analyzed. Key factors such as market penetration rates, airport infrastructure projects, and revenue generated by hangar manufacturers are evaluated to estimate current market performance. Furthermore, service quality statistics are considered to ensure the reliability and accuracy of revenue projections.

Market hypotheses are developed and validated through consultations with industry experts, including executives from hangar construction companies, MRO service providers, and aviation authorities. These consultations are conducted via computer-assisted telephone interviews (CATIs) and provide valuable operational and financial insights that refine the data.

The final phase involves engaging with multiple aircraft manufacturers and airport authorities to acquire detailed insights into product segments, sales performance, and future trends. This interaction serves to verify the data derived from the bottom-up analysis and ensure a comprehensive understanding of the global aircraft hangar market.

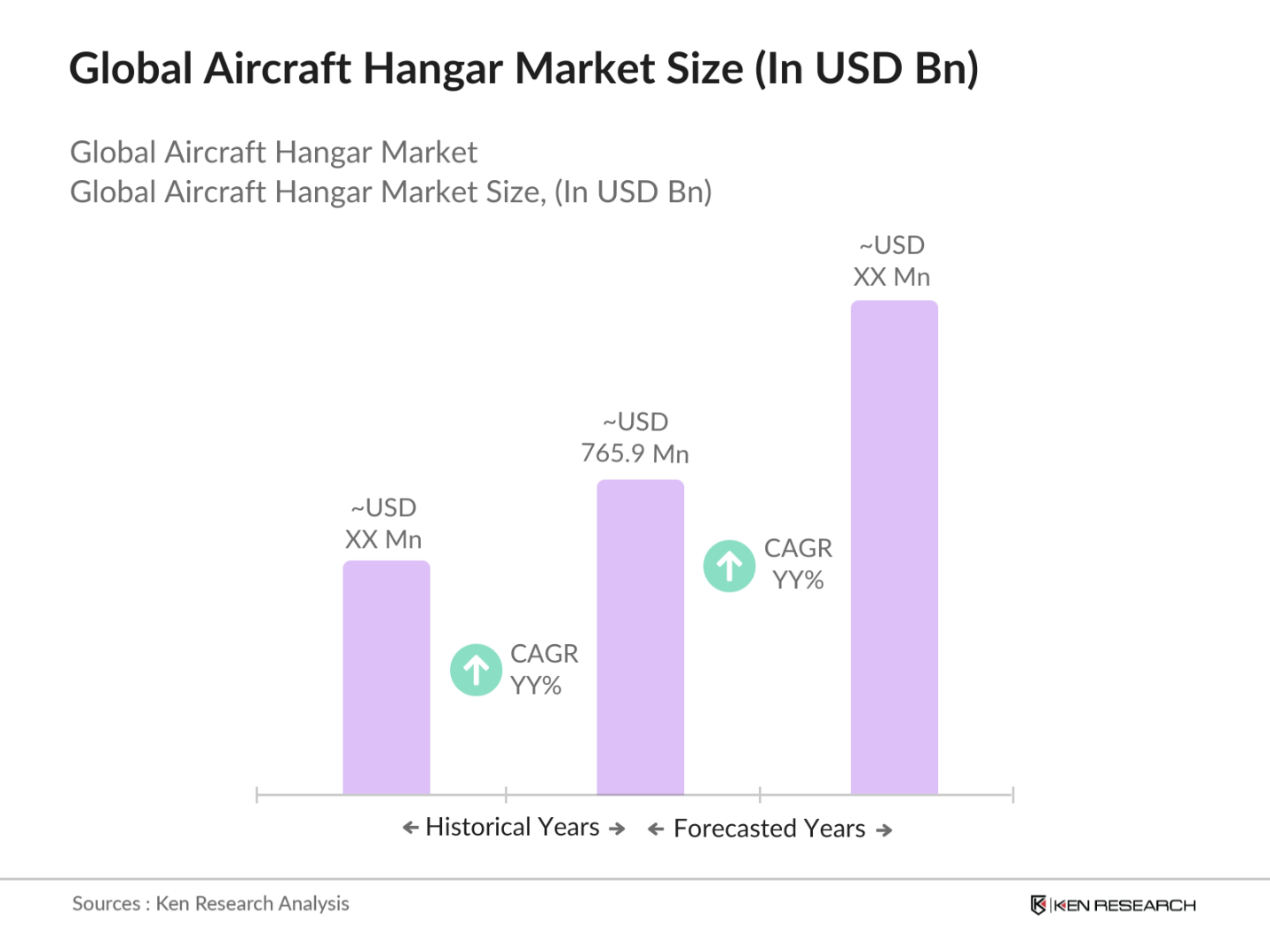

The global aircraft hangar market is valued at USD 765.9 million, driven by the expansion of airport infrastructure, rising air traffic, and increasing demand for MRO services.

The key growth drivers include increasing air traffic, rising demand for MRO services, expansion of airport infrastructure, and technological advancements in hangar automation and energy efficiency.

Key players include AECOM, Butler Manufacturing, Rubb Buildings Ltd, Erect-A-Tube Inc., and Megadoor (ASSA ABLOY Group), which dominate due to their extensive experience in hangar construction and infrastructure projects.

The market faces challenges such as high initial capital investment, fluctuating raw material prices, and stringent regulatory requirements for construction and safety standards.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.