Global Fire Truck Market Outlook 2030

Region:Global

Author(s):Shivani Mehra

Product Code:KROD4080

November 2024

83

About the Report

Global Fire Truck Market Overview

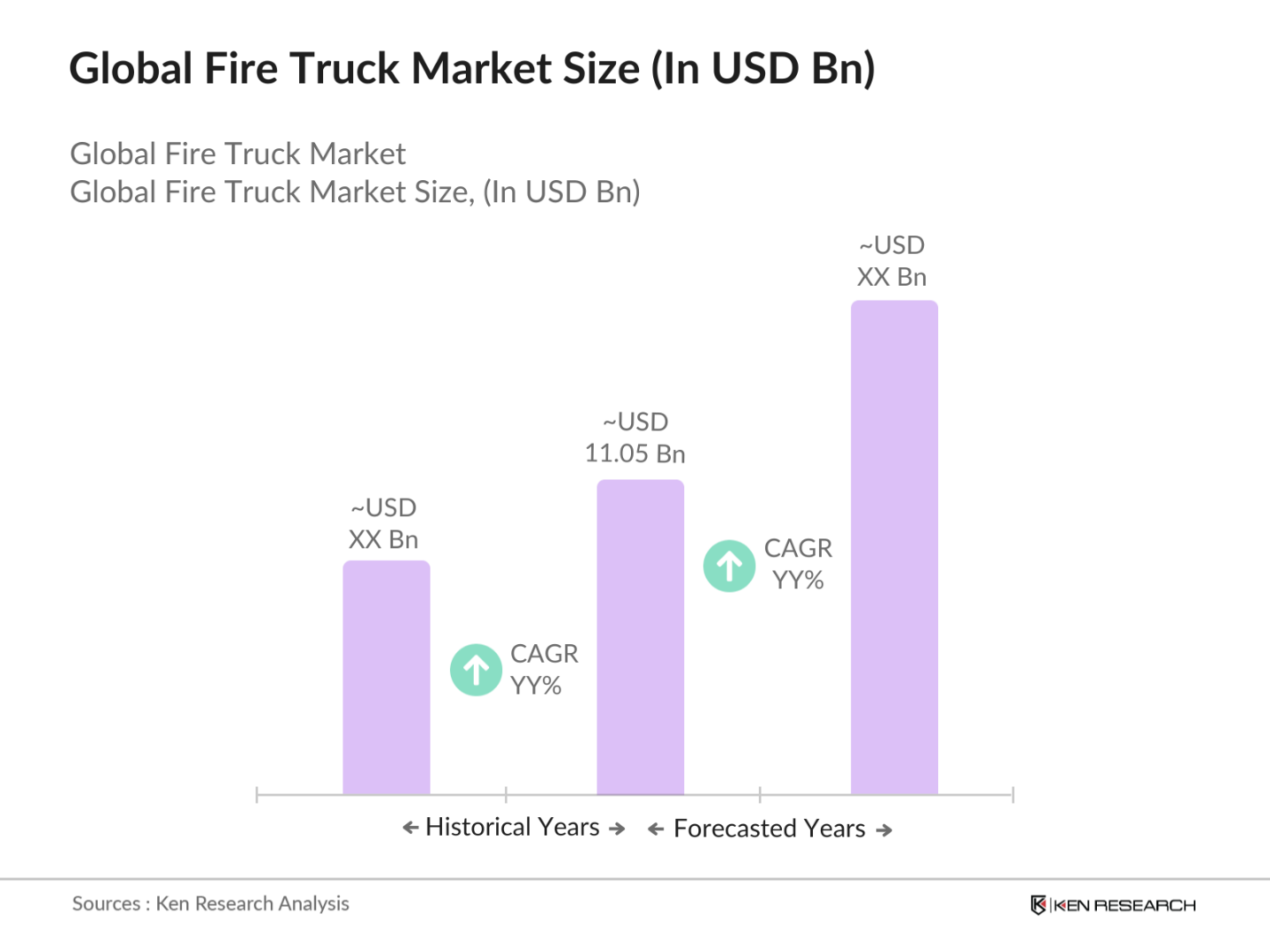

- The Global Fire Truck Market is valued at USD 11.05 billion. The market's growth is driven by the rising frequency of natural disasters, such as wildfires, and the increased focus on infrastructure development, especially in urban areas. Additionally, government funding for emergency services and fire safety equipment has also contributed significantly to the market. The continuous demand for high-performance fire trucks for both municipal and industrial applications fuels market growth.

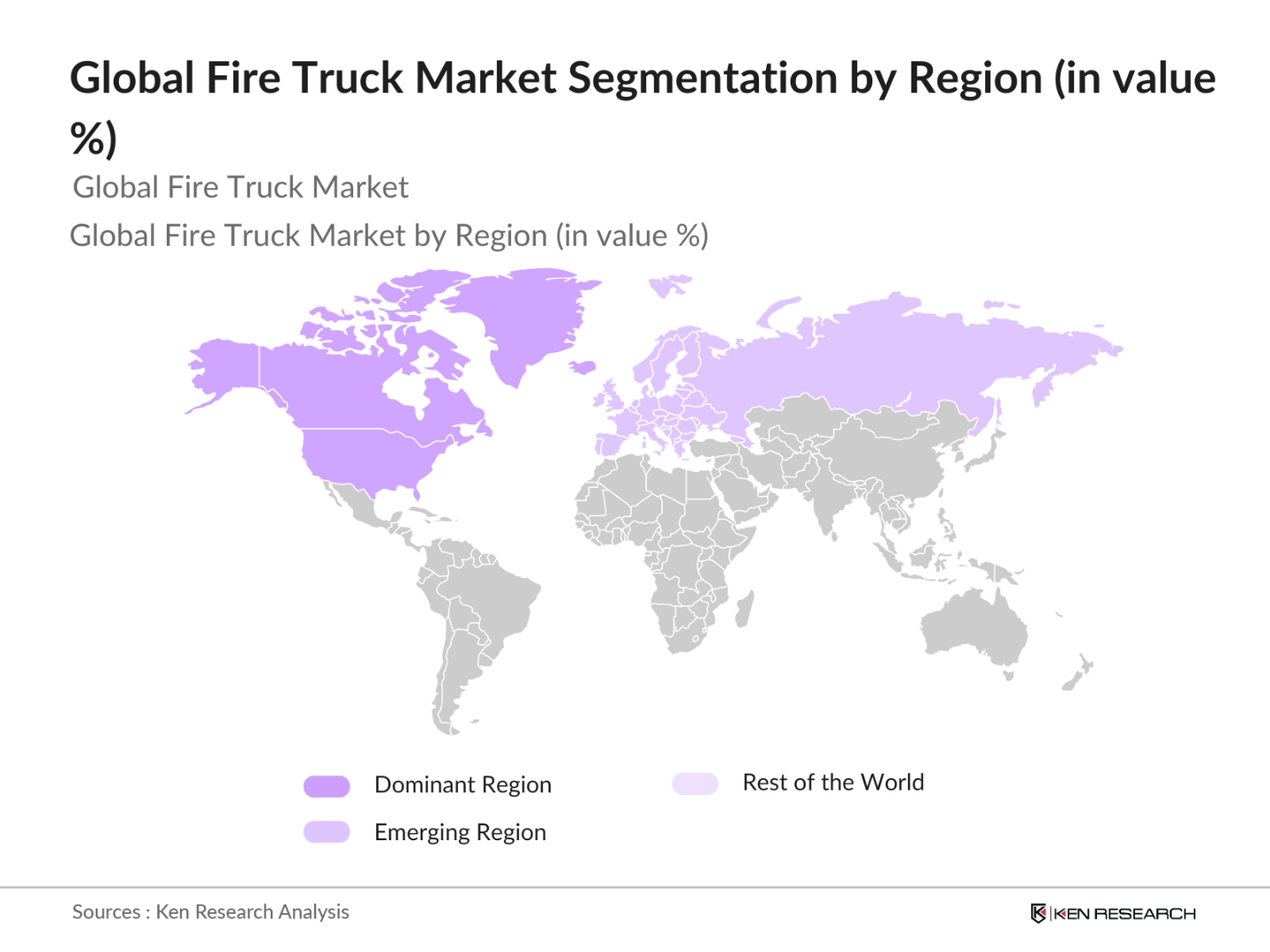

- North America, particularly the United States, and Europe are dominant regions in the fire truck market. In the United States, the need for modern firefighting equipment is driven by high urbanization rates and extensive infrastructure projects. In Europe, countries like Germany and France have well-established fire safety regulations, driving consistent demand for technologically advanced fire trucks. In both regions, strong government regulations concerning fire safety standards have led to a steady demand for state-of-the-art fire trucks.

- Governments are also tightening regulations around fire equipment certification. In 2023, the U.S. introduced the Emergency Response Vehicle Certification Program, mandating that all new fire trucks meet enhanced safety standards. This move has pushed manufacturers to ensure compliance with new safety regulations, ensuring the trucks are outfitted with advanced firefighting equipment and technologies.

Global Fire Truck Market Segmentation

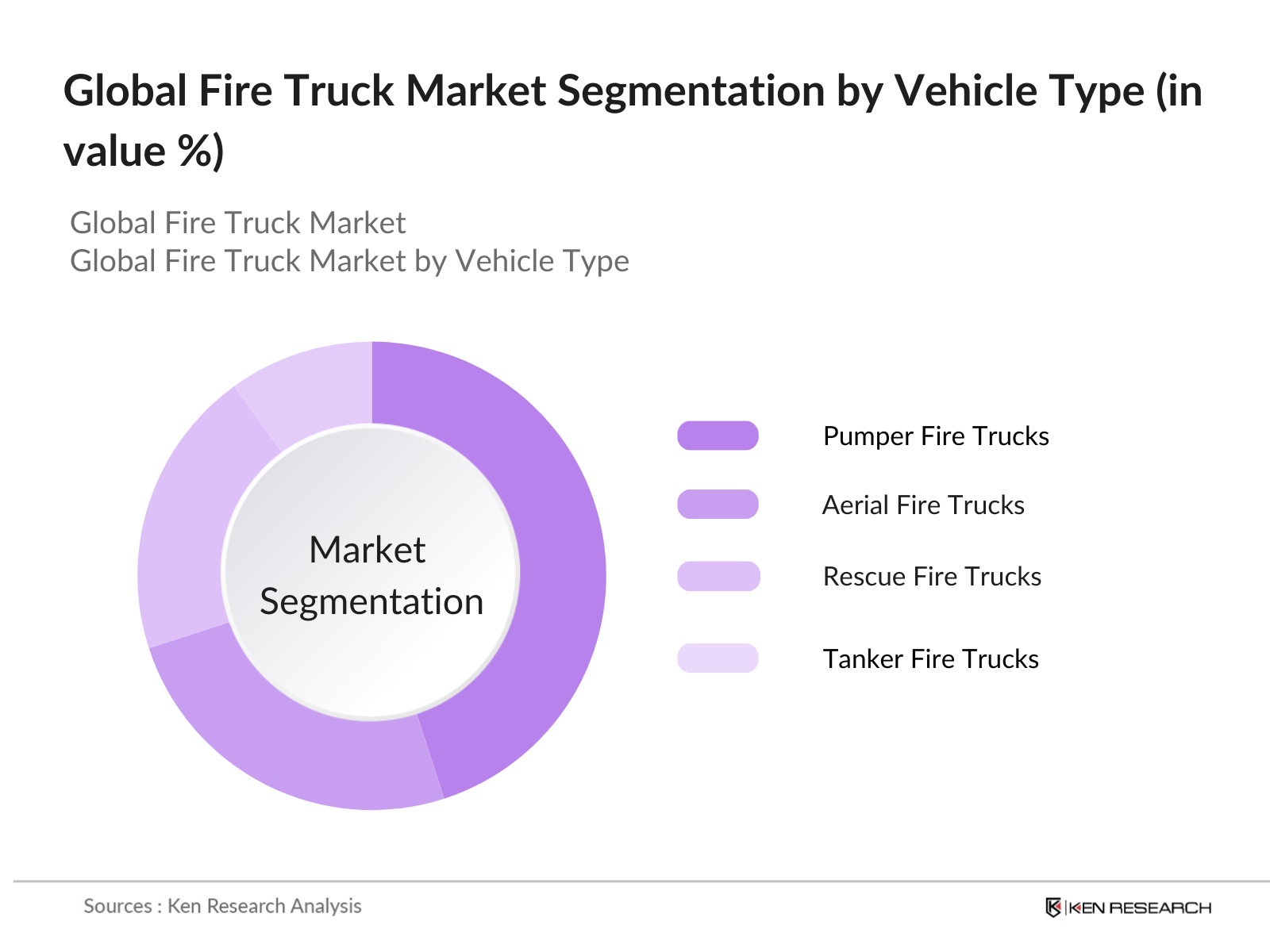

By Vehicle Type: The fire truck market is segmented by vehicle type into Aerial Fire Trucks, Pumper Fire Trucks, Rescue Fire Trucks, and Tanker Fire Trucks. Among these, pumper fire trucks dominate the market due to their multifunctionality in both municipal and industrial firefighting operations. Pumper fire trucks are typically equipped with essential firefighting equipment such as hoses, water tanks, and pumps, making them suitable for a wide range of emergencies. The versatility and reliability of these vehicles are the key factors contributing to their dominance.

By Region: The fire truck market is segmented by region into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa. Among these, North America dominates the market due to its high urbanization rates and advanced fire safety infrastructure. The United States, in particular, plays a crucial role in this dominance, driven by its continuous investments in upgrading emergency services. The adoption of cutting-edge technologies, such as electric fire trucks and AI-powered firefighting systems, has further strengthened North America's leading position in the global fire truck market.

Global Fire Truck Market Competitive Landscape

The market is dominated by key global manufacturers such as Rosenbauer International AG, Oshkosh Corporation, and Magirus GmbH, all of which benefit from their comprehensive product lines and strong distribution networks. These companies have consistently innovated with advancements in fire truck technology, including electric and hybrid models, contributing to their dominant position in the market.

|

Company Name |

Established |

Headquarters |

Global Presence |

Revenue (USD Bn) |

Product Line |

Technological Advancements |

Major Contracts |

|

Rosenbauer International AG |

1866 |

Leonding, Austria |

|||||

|

Oshkosh Corporation |

1917 |

Wisconsin, USA |

|||||

|

Magirus GmbH |

1864 |

Ulm, Germany |

|||||

|

E-ONE Inc. |

1974 |

Florida, USA |

|||||

|

Morita Holdings Corporation |

1907 |

Osaka, Japan |

Global Fire Truck Market Analysis

Market Growth Drivers

- Increasing Urbanization (Impact on Emergency Services): With rapid urbanization, emergency services in major cities are under strain. In 2023, the global urban population reached 4.46 billion, driving demand for enhanced fire safety infrastructure. Countries such as India saw urban population growth by over 20 million people between 2022. This surge increases the need for better-equipped fire services, leading to significant demand for fire trucks, particularly in emerging economies. The rise in urban housing and commercial development results in a more complex fire risk profile, necessitating modernized, high-capacity fire trucks to meet these emerging challenges.

- Expansion in Industrial and Commercial Construction: Industrial and commercial construction is seeing a boom worldwide. Between 2022, global commercial construction output reached $10 trillion, which inherently increases the need for fire safety infrastructure, including fire trucks. In countries like China, the government has prioritized commercial development, spurring demand for specialized fire trucks designed for industrial environments. As commercial zones expand, fire trucks capable of navigating larger areas and carrying more equipment are becoming essential for fire departments.

- Rising Frequency of Wildfires: In 2023, wildfires burned over 9.2 million acres in the United States alone, while Australia faced severe wildfires, destroying over 12 million acres of land in 2022. These increasingly frequent and destructive fires have highlighted the need for robust firetruck fleets specifically designed for wildfire control. Governments are increasing investments in off-road, all-terrain fire trucks with higher water capacity and advanced firefighting capabilities to address this rising threat.

Market Challenges

- High Initial Purchase Costs (Fire Truck Market): Fire trucks are among the most expensive emergency vehicles, with an average cost of $500,000 to $1 million for standard models and specialized units exceeding $1.5 million. These high upfront costs often burden municipal budgets, particularly in developing countries where fire departments operate on limited financial resources. Many local governments face challenges in securing funds for fleet upgrades, resulting in an aging fleet that struggles to meet modern firefighting demands.

- Maintenance and Operation Costs: The operational costs of maintaining fire trucks can be as high as $15,000 annually per vehicle. Expenses include fuel, regular maintenance, and repair costs, which are exacerbated by the specialized nature of fire trucks. In many regions, government budgets are insufficient to cover these rising operational costs, leading to an overburdened and under-maintained fleet. This is particularly an issue in rural areas where funding for emergency services is even more constrained.

Global Fire Truck Market Future Outlook

Over the next few years, the Global Fire Truck Market is expected to see consistent growth driven by rising awareness of fire safety, advancements in firefighting technologies, and increasing investments by governments worldwide in emergency response infrastructure. The integration of electric and hybrid fire trucks and the use of AI for automated firefighting operations are set to shape the future of the industry. Additionally, the growing demand for high-performance and environmentally friendly vehicles is likely to create new opportunities for market expansion.

Market Opportunities

- Shift Towards Green and Sustainable Vehicles: Governments worldwide are pushing for the use of green and sustainable fire trucks as part of their broader climate goals. Norway, for example, mandated that all new fire trucks purchased after 2025 must be zero-emission vehicles. This trend towards sustainability is pushing manufacturers to innovate in terms of energy-efficient vehicles, primarily through the development of electric and hybrid models. These vehicles are not only environmentally friendly but also offer lower operational costs.

- Focus on High-Capacity, Multi-Utility Trucks: There is an increasing focus on the development of high-capacity, multi-utility fire trucks that can serve various purposes, such as rescue operations, high-rise firefighting, and industrial fire incidents. Fire trucks with larger water tanks and higher pressure pumps are being deployed in commercial zones and industrial hubs. In 2023, the U.K. government funded a 250 million initiative to upgrade its fleet to multi-purpose trucks, emphasizing utility and adaptability for different emergency scenarios.

Scope of the Report

|

By Vehicle Type |

Aerial Fire Trucks Pumper Fire Trucks Rescue Fire Trucks Tanker Fire Trucks |

|

By Application |

Municipal Firefighting Industrial Firefighting Airport Rescue Wildland Firefighting |

|

By Drive Configuration |

4X2 Drive 4X4 Drive 6X4 Drive |

|

By Water Tank Capacity |

Below 1000 Litres 1000-4000 Litres Above 4000 Litres |

|

By Region |

North America Europe Asia Pacific Latin America Middle East & Africa |

Products

Key Target Audience

Government and Regulatory Bodies (e.g., National Fire Protection Association, European Committee for Standardization)

Fire Truck Manufacturers

Fire Safety Equipment Suppliers

Industrial Fire Safety Teams

Municipal Fire Departments

Airports and Aviation Authorities

Investment and Venture Capitalist Firms

Emergency Response Organizations

Companies

Major Players in the Global Fire Truck Market

Rosenbauer International AG

Oshkosh Corporation

E-ONE Inc.

Magirus GmbH

Morita Holdings Corporation

Spartan Motors Inc.

Ziegler Group

Gimaex

Pierce Manufacturing Inc.

HME Ahrens-Fox

Sutphen Corporation

W.S. Darley & Co.

KME Fire Apparatus

Scania AB

Volvo Trucks

Table of Contents

01. Global Fire Truck Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (Global Fire Truck Market)

1.4. Market Segmentation Overview (Vehicle Type, Application, Drive Configuration, Water Tank Capacity, Region)

02. Global Fire Truck Market Size (In USD Bn)

2.1. Historical Market Size (USD Billion)

2.2. Year-On-Year Growth Analysis (Global Fire Truck Market)

2.3. Key Market Developments and Milestones (Fire Truck Market Innovations, New Technologies)

03. Global Fire Truck Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Urbanization (Impact on Emergency Services)

3.1.2. Government Infrastructure Investments (Fire Safety Equipment)

3.1.3. Expansion in Industrial and Commercial Construction

3.1.4. Rising Frequency of Wildfires

3.2. Market Challenges

3.2.1. High Initial Purchase Costs (Fire Truck Market)

3.2.2. Maintenance and Operation Costs

3.2.3. Availability of Skilled Personnel

3.3. Opportunities

3.3.1. Advancements in Electric Fire Trucks

3.3.2. Adoption of Smart Firefighting Systems

3.3.3. Integration of AI and IoT Technologies

3.4. Trends

3.4.1. Shift Towards Green and Sustainable Vehicles

3.4.2. Focus on High-Capacity, Multi-Utility Trucks

3.4.3. Adoption of Autonomous Fire Trucks

3.5. Government Regulation

3.5.1. Fire Safety Codes and Standards (NFPA, Local Regulations)

3.5.2. Emission Control Standards for Fire Trucks

3.5.3. Fire Equipment Certification and Compliance

3.5.4. Public-Private Partnerships in Emergency Response Systems

3.6. SWOT Analysis (Global Fire Truck Market)

3.7. Stake Ecosystem

3.8. Porters Five Forces (Global Fire Truck Market)

3.9. Competition Ecosystem (Fire Truck Market)

04. Global Fire Truck Market Segmentation

4.1. By Vehicle Type (In Value %)

4.1.1. Aerial Fire Trucks

4.1.2. Pumper Fire Trucks

4.1.3. Rescue Fire Trucks

4.1.4. Tanker Fire Trucks

4.2. By Application (In Value %)

4.2.1. Municipal Firefighting

4.2.2. Industrial Firefighting

4.2.3. Airport Rescue

4.2.4. Wildland Firefighting

4.3. By Drive Configuration (In Value %)

4.3.1. 4X2 Drive

4.3.2. 4X4 Drive

4.3.3. 6X4 Drive

4.4. By Water Tank Capacity (In Value %)

4.4.1. Below 1000 Litres

4.4.2. 1000-4000 Litres

4.4.3. Above 4000 Litres

4.5. By Region (In Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia Pacific

4.5.4. Latin America

4.5.5. Middle East & Africa

05. Global Fire Truck Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1. Rosenbauer International AG

5.1.2. Oshkosh Corporation

5.1.3. E-ONE Inc.

5.1.4. Magirus GmbH

5.1.5. Morita Holdings Corporation

5.1.6. Spartan Motors Inc.

5.1.7. Ziegler Group

5.1.8. Gimaex

5.1.9. Pierce Manufacturing Inc.

5.1.10. HME Ahrens-Fox

5.1.11. Sutphen Corporation

5.1.12. W.S. Darley & Co.

5.1.13. KME Fire Apparatus

5.1.14. Scania AB

5.1.15. Volvo Trucks

5.2 Cross Comparison Parameters (Vehicle Production Capacity, Headquarters, Inception Year, Global Presence, Revenue, Workforce Size, Product Portfolio, Key Partnerships)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7 Venture Capital Funding

5.8. Government Grants and Subsidies

5.9. Private Equity Investments

06. Global Fire Truck Market Regulatory Framework

6.1. Fire Equipment Certification Standards (NFPA, EN Standards)

6.2. Safety and Emission Regulations

6.3. Compliance Requirements

6.4. National and Local Fire Safety Regulations

07. Global Fire Truck Future Market Size (In USD Bn)

7.1. Future Market Size Projections (Fire Truck Market)

7.2. Key Factors Driving Future Market Growth

08. Global Fire Truck Market Future Segmentation

8.1. By Vehicle Type (In Value %)

8.2. By Application (In Value %)

8.3. By Drive Configuration (In Value %)

8.4. By Water Tank Capacity (In Value %)

8.5. By Region (In Value %)

09. Global Fire Truck Market Analyst Recommendations

9.1. TAM/SAM/SOM Analysis (Total Addressable Market, Serviceable Available Market, Serviceable Obtainable Market)

9.2. Customer Segmentation Analysis (Fire Truck Market)

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The research process begins with identifying critical stakeholders in the fire truck market, including manufacturers, fire departments, and regulatory bodies. Extensive desk research is conducted, utilizing secondary databases to define market variables such as production capacities, sales figures, and technological advancements.

Step 2: Market Analysis and Construction

During this phase, historical data related to the fire truck market is compiled, with a focus on regional market penetration and key operational metrics. This step also includes an analysis of the technological trends driving growth in the market.

Step 3: Hypothesis Validation and Expert Consultation

The research hypotheses are validated through consultations with industry experts via interviews. These consultations provide insights into operational challenges, financial performance, and emerging opportunities in the market, ensuring data accuracy.

Step 4: Research Synthesis and Final Output

The final phase involves integrating data collected from fire truck manufacturers and distributors to validate revenue forecasts and analyze key growth drivers. The result is a comprehensive report that provides actionable insights into the market dynamics.

Frequently Asked Questions

01. How big is the Global Fire Truck Market?

The Global Fire Truck Market is valued at USD 11.05 billion, driven by growing urbanization and increasing government investment in emergency services.

02. What are the key challenges in the Global Fire Truck Market?

Key challenges include the high initial cost of fire trucks, maintenance and operational costs, and a shortage of skilled personnel to operate advanced vehicles.

03. Who are the major players in the Global Fire Truck Market?

Major players in the market include Rosenbauer International AG, Oshkosh Corporation, Magirus GmbH, E-ONE Inc., and Morita Holdings Corporation.

04. What are the growth drivers in the Global Fire Truck Market?

The market is primarily driven by advancements in fire truck technology, rising demand for emergency services, and government investments in public safety infrastructure.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.