Global Flow Cytometry Market Outlook to 2030

Region:Global

Author(s):Vijay Kumar

Product Code:KROD2807

Region:Global

Author(s):Vijay Kumar

Product Code:KROD2807

December 2024

89

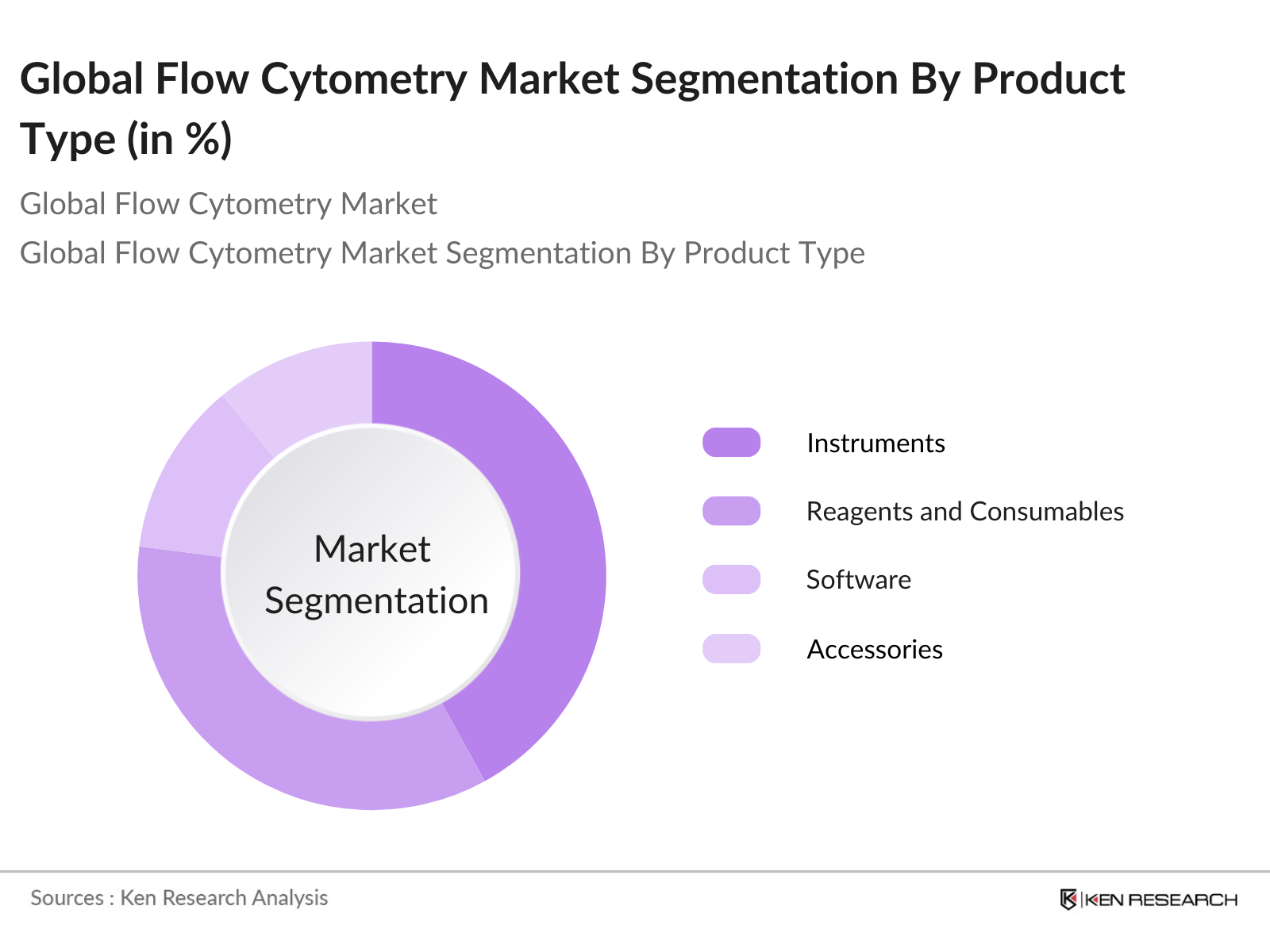

By Product Type: The market is segmented by product type into Instruments, Reagents and Consumables, Software, and Accessories. Recently, instruments have held a dominant market share due to the increasing adoption of advanced flow cytometers in research and clinical settings. Instruments have seen innovations such as multi-parameter analysis, enhancing their capabilities in cell sorting and diagnostics.

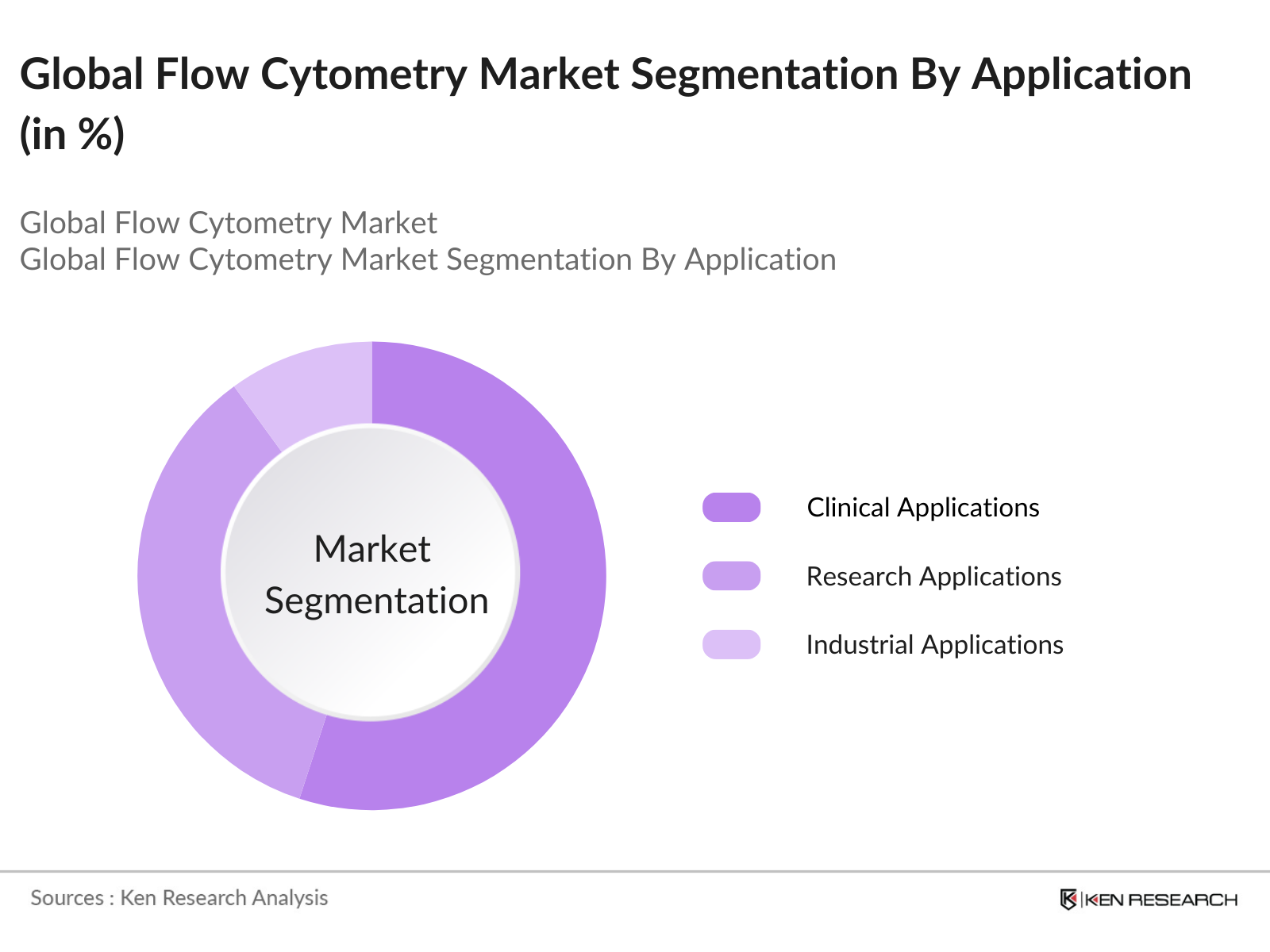

By Application: Flow cytometry is also segmented by applications, including Research Applications, Clinical Applications, and Industrial Applications. Clinical applications have a leading market share due to their essential role in diagnostics, especially for cancer and HIV monitoring. The rapid rise in cancer cases globally has led to an increased reliance on flow cytometry for accurate and early diagnosis.

The global flow cytometry market is characterized by intense competition, with both established global players and emerging companies focusing on innovation and expanding their product portfolios. The major players are leveraging strategic collaborations, product launches, and mergers to solidify their market positions. The market is dominated by companies like Becton, Dickinson and Company and Thermo Fisher Scientific, which offer a broad range of flow cytometry products, including instruments, reagents, and software solutions.

Over the next five years, the global flow cytometry market is expected to experience significant growth driven by continuous technological advancements, increased application in personalized medicine, and growing demand for faster, more accurate diagnostic tools. Flow cytometrys role in advancing precision medicine, especially in oncology, immunology, and drug development, will be pivotal in shaping the future of the market.

|

By Product Type |

Instruments Reagents and Consumables Software Accessories |

|

By Technology |

Cell-Based Flow Cytometry Bead-Based Flow Cytometry |

|

By Application |

Research Applications (Immunology, Molecular Biology, Genomics) Clinical Applications (Cancer Diagnostics, HIV Monitoring) Industrial Applications (Bioprocessing, Quality Control) |

|

By End-User |

Academic and Research Institutes Hospitals and Clinics Pharmaceutical and Biotechnology Companies Clinical Testing Labs |

|

By Region |

North America Europe Asia-Pacific Latin America Middle East & Africa |

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3.1 Growth Drivers

3.1.1 Increasing Demand for Clinical Diagnostics

3.1.2 Rising Adoption in Research Laboratories

3.1.3 Growing Incidence of Cancer and Infectious Diseases

3.1.4 Expansion of Precision Medicine

3.2 Market Challenges

3.2.1 High Equipment and Reagent Costs

3.2.2 Complex Instrumentation and Skilled Workforce Requirement

3.2.3 Stringent Regulatory Approvals (Compliance Challenges)

3.3 Opportunities

3.3.1 Technological Advancements (Multiparameter Analysis, AI Integration)

3.3.2 Growing Applications in Immunology, Hematology, and Oncology

3.3.3 Expansion into Emerging Markets

3.4 Trends

3.4.1 Increasing Use of High-Throughput Flow Cytometers

3.4.2 Integration with Big Data and Cloud-Based Analysis Platforms

3.4.3 Single-Cell Analysis Demand Surge

3.5 Government Regulations and Funding

3.5.1 FDA and EU Directives (Regulatory Environment)

3.5.2 Government Research Funding (NIH, Horizon Europe)

3.5.3 Public-Private Partnerships

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem (Research Institutes, Hospitals, Diagnostic Labs, Pharmaceutical Companies)

3.8 Porters Five Forces

3.9 Competition Ecosystem

4.1 By Product Type (In Value %)

4.1.1 Instruments

4.1.2 Reagents and Consumables

4.1.3 Software

4.1.4 Accessories

4.2 By Technology (In Value %)

4.2.1 Cell-Based Flow Cytometry

4.2.2 Bead-Based Flow Cytometry

4.3 By Application (In Value %)

4.3.1 Research Applications (Immunology, Molecular Biology, Genomics)

4.3.2 Clinical Applications (Cancer Diagnostics, HIV Monitoring)

4.3.3 Industrial Applications (Bioprocessing, Quality Control)

4.4 By End-User (In Value %)

4.4.1 Academic and Research Institutes

4.4.2 Hospitals and Clinics

4.4.3 Pharmaceutical and Biotechnology Companies

4.4.4 Clinical Testing Labs

4.5 By Region (In Value %)

4.5.1 North America

4.5.2 Europe

4.5.3 Asia-Pacific

4.5.4 Latin America

4.5.5 Middle East & Africa

5.1 Detailed Profiles of Major Competitors

5.1.1 Becton, Dickinson and Company

5.1.2 Thermo Fisher Scientific

5.1.3 Beckman Coulter

5.1.4 Merck KGaA

5.1.5 Agilent Technologies

5.1.6 Luminex Corporation

5.1.7 Sysmex Corporation

5.1.8 Miltenyi Biotec

5.1.9 Bio-Rad Laboratories

5.1.10 Sony Biotechnology

5.1.11 Stratedigm

5.1.12 Union Biometrica

5.1.13 Cytek Biosciences

5.1.14 Apogee Flow Systems

5.1.15 Nexcelom Bioscience

5.2 Cross Comparison Parameters (Product Portfolio, Market Presence, Technological Expertise, Revenue, R&D Expenditure, Market Share, Patents Filed, Manufacturing Capacity)

5.3 Market Share Analysis

5.4 Strategic Initiatives (Partnerships, Collaborations, Expansion Strategies)

5.5 Mergers and Acquisitions

5.6 Investment Analysis (Venture Capital Funding, Private Equity)

5.7 Government Grants and Incentives

6.1 Regulatory Guidelines (FDA, EMA, ISO Certifications)

6.2 Compliance Requirements (Good Manufacturing Practice, Good Laboratory Practice)

6.3 Certification and Approval Processes

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Growth

8.1 By Product Type (In Value %)

8.2 By Technology (In Value %)

8.3 By Application (In Value %)

8.4 By End-User (In Value %)

8.5 By Region (In Value %)

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 White Space Opportunity Analysis

9.4 Marketing and Business Strategies

Disclaimer Contact UsThe initial phase involves mapping the ecosystem of the global flow cytometry market by identifying major stakeholders, including manufacturers, researchers, and healthcare institutions. This step relies on extensive secondary research to gather insights into the key variables affecting market growth, such as technological advancements and regulatory frameworks.

Historical data is compiled to analyze market trends and developments, focusing on revenue generation, product penetration, and regional variations. This includes evaluating market entry strategies and competitive positioning within various sub-segments of the flow cytometry market.

Market hypotheses are tested through expert consultations and interviews with key industry participants. These interviews provide detailed insights into industry trends, challenges, and emerging opportunities, enabling the refinement of market estimates and projections.

The final step involves synthesizing the research findings to produce an in-depth analysis of the market, validating the bottom-up approach with primary data from industry participants. This ensures a comprehensive and accurate representation of the global flow cytometry market.

The global flow cytometry market is valued at USD 5 billion, driven by rising demand for clinical diagnostics, particularly in immunology, oncology, and hematology.

Challenges in the global flow cytometry market include high equipment costs, regulatory hurdles, and a lack of skilled professionals to operate complex flow cytometry systems.

Key players in the global flow cytometry market include Becton, Dickinson and Company, Thermo Fisher Scientific, Beckman Coulter, and Merck KGaA, among others.

Growth is driven the global flow cytometry market by advancements in flow cytometry technology, rising applications in clinical diagnostics and research, and increased demand for personalized medicine.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.