Global Hyperconverged Infrastructure Market Outlook to 2030

Region:Global

Author(s):Mukul

Product Code:KROD8180

Region:Global

Author(s):Mukul

Product Code:KROD8180

October 2024

83

The Global Hyperconverged Infrastructure market is characterized by a consolidation of major players who offer innovative solutions and compete on the basis of technological advancements and strategic partnerships. Large vendors like Nutanix, Dell Technologies, and VMware dominate the market due to their expansive product portfolios, strong customer bases, and investments in research and development.

|

Company |

Establishment Year |

Headquarters |

No. of Employees |

Revenue (USD Bn) |

Product Portfolio |

Recent Acquisition |

Regional Presence |

Key Partnerships |

R&D Investments |

|

Nutanix Inc. |

2009 |

San Jose, California |

|||||||

|

Dell Technologies Inc. |

1984 |

Round Rock, Texas |

|||||||

|

VMware Inc. |

1998 |

Palo Alto, California |

|||||||

|

Cisco Systems Inc. |

1984 |

San Jose, California |

|||||||

|

Hewlett Packard Enterprise (HPE) |

2015 |

Houston, Texas |

The Hyperconverged Infrastructure market is expected to witness significant growth in the coming years, driven by the increasing demand for cloud-based services, edge computing solutions, and the rapid expansion of digital infrastructure across emerging markets. Businesses are shifting toward hybrid cloud environments, and HCI systems are expected to play a pivotal role in enabling seamless management and scalability of IT operations. Moreover, the adoption of AI and machine learning technologies in HCI systems is set to enhance the automation of IT tasks, leading to higher efficiency and cost savings for enterprises.

|

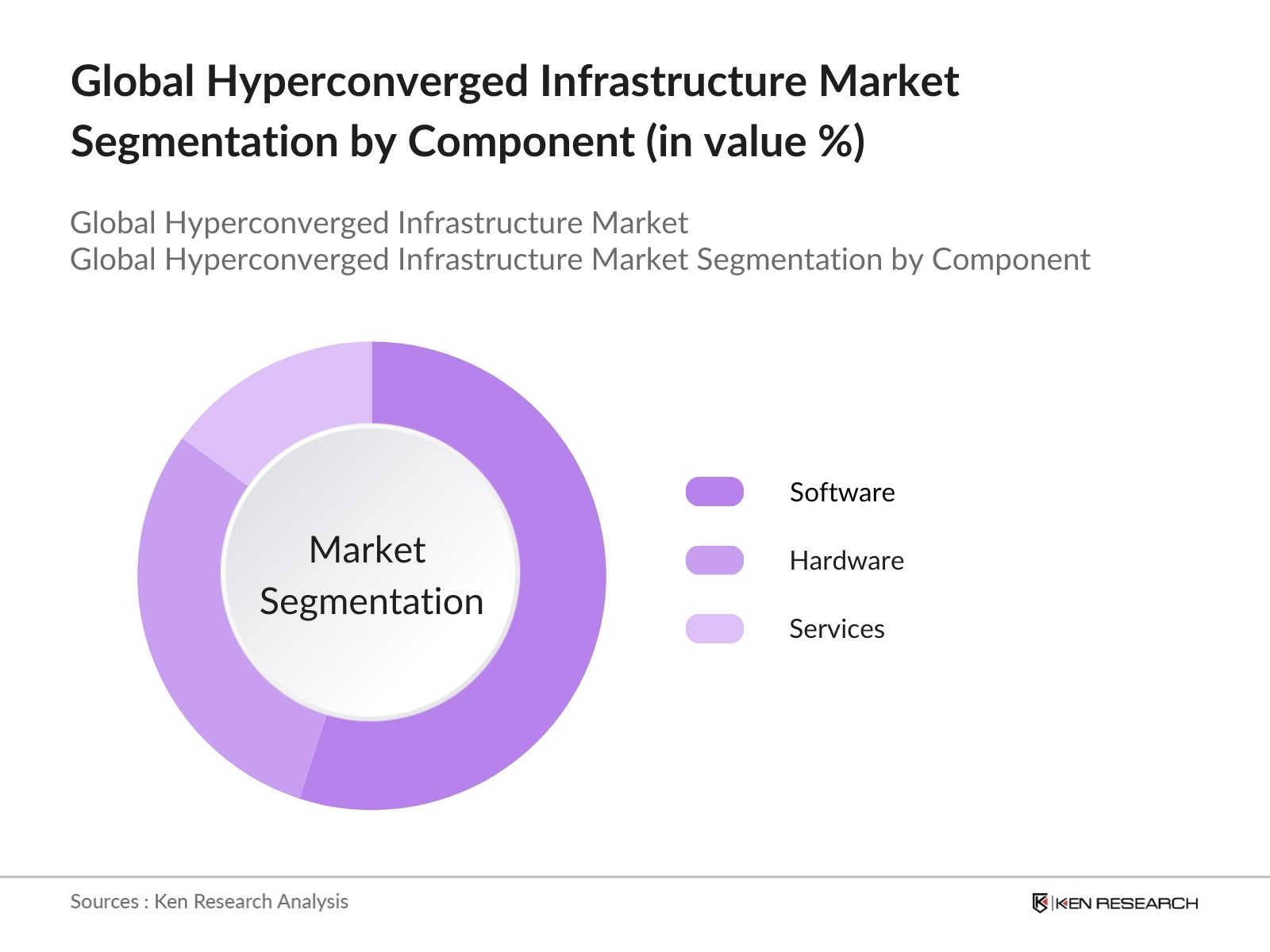

Component |

Software, Hardware, Services (Consulting, Support, Implementation) |

|

Organization Size |

Small and Medium Enterprises (SMEs), Large Enterprises |

|

Deployment Mode |

On-Premises, Cloud-Based, Hybrid |

|

End-User Industry |

IT & Telecom, BFSI, Healthcare, Government, Education |

|

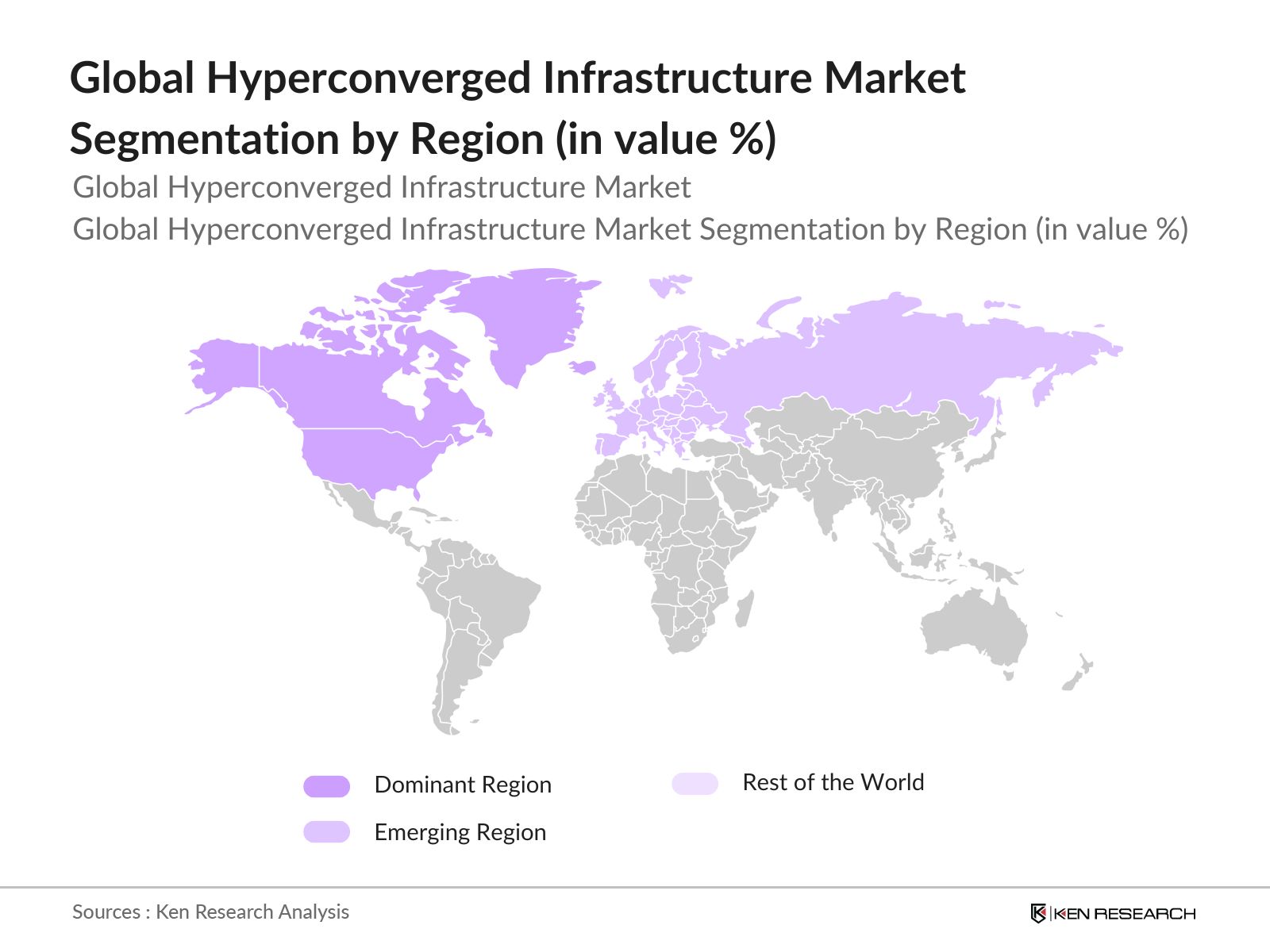

Region |

North America, Europe, Asia Pacific, Latin |

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Key Market Developments and Milestones

1.4 Market Segmentation Overview

2.1 Historical Market Size

2.2 Year-on-Year Growth Analysis

2.3 Key Market Drivers (Scalability, Cost Efficiency, Infrastructure Simplification)

2.4 Technological Advancements Impacting Market Size

3.1 Growth Drivers

3.1.1. Cloud Adoption

3.1.2. Data Center Modernization

3.1.3. Rising Demand for Virtualization

3.1.4. Enhanced Business Agility

3.2 Market Challenges

3.2.1. High Initial Investment Costs

3.2.2. Data Security Concerns

3.2.3. Integration with Legacy Systems

3.3 Opportunities

3.3.1. Expansion of Edge Computing

3.3.2. Growing Adoption of AI and ML in HCI Solutions

3.3.3. SMB Market Penetration

3.4 Trends

3.4.1. Software-Defined Data Centers (SDDC) Adoption

3.4.2. Automation and Orchestration

3.4.3. Integration of Multi-Cloud and Hybrid Cloud Solutions

3.5 Government Regulations

3.5.1. Data Protection and Privacy Laws

3.5.2. Compliance with Global Standards for IT Infrastructure

3.5.3. Cybersecurity Regulations for Critical Infrastructure

3.6 SWOT Analysis

3.7 Porters Five Forces Analysis (Threat of New Entrants, Supplier Power, Buyer Power, Competitive Rivalry, Threat of Substitutes)

3.8 Competitive Landscape Ecosystem (OEMs, System Integrators, Managed Service Providers)

4.1 By Component (In Value %)

4.1.1. Software

4.1.2. Hardware

4.1.3. Services (Consulting, Support, Implementation)

4.2 By Organization Size (In Value %)

4.2.1. Small and Medium Enterprises (SMEs)

4.2.2. Large Enterprises

4.3 By Deployment Mode (In Value %)

4.3.1. On-Premises

4.3.2. Cloud-Based

4.3.3. Hybrid

4.4 By End-User Industry (In Value %)

4.4.1. IT & Telecom

4.4.2. BFSI

4.4.3. Healthcare

4.4.4. Government

4.4.5. Education

4.5 By Region (In Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia Pacific

4.5.4. Latin America

4.5.5. Middle East & Africa

5.1 Detailed Profiles of Major Competitors

5.1.1. Nutanix Inc.

5.1.2. Dell Technologies Inc.

5.1.3. Hewlett Packard Enterprise (HPE)

5.1.4. Cisco Systems Inc.

5.1.5. VMware Inc.

5.1.6. Microsoft Corporation

5.1.7. Scale Computing

5.1.8. Pivot3 Inc.

5.1.9. Huawei Technologies Co., Ltd.

5.1.10. IBM Corporation

5.1.11. NetApp Inc.

5.1.12. DataCore Software

5.1.13. Fujitsu Limited

5.1.14. StarWind Software Inc.

5.1.15. Hitachi Vantara Corporation

5.2 Cross Comparison Parameters (Number of Employees, Revenue, Headquarters, Regional Presence, Product Portfolio, R&D Investments, Recent Mergers & Acquisitions, Key Partnerships)

5.3 Market Share Analysis

5.4 Strategic Initiatives (Joint Ventures, Strategic Alliances, New Product Launches, Geographic Expansion)

5.5 Mergers & Acquisitions Activity

5.6 Investment Analysis (Private Equity, Venture Capital, Corporate Funding)

5.7 Government Grants and Funding Programs

6.1 Global IT Infrastructure Standards and Certifications

6.2 Data Sovereignty and Localization Laws

6.3 Cybersecurity Regulations for HCI Systems

6.4 Environmental and Energy Efficiency Regulations

7.1 Future Market Growth Forecast

7.2 Key Factors Driving Future Market Growth

8.1 By Component (In Value %)

8.2 By Organization Size (In Value %)

8.3 By Deployment Mode (In Value %)

8.4 By End-User Industry (In Value %)

8.5 By Region (In Value %)

9.1 TAM/SAM/SOM Analysis

9.2 Competitive Positioning Matrix

9.3 Strategic Marketing Initiatives for Market Penetration

9.4 White Space Opportunity Analysis

The research begins with mapping out the HCI market landscape, identifying all relevant stakeholders such as vendors, end-users, and service providers. Key variables that influence market dynamics, including cloud adoption rates, enterprise IT budgets, and regulatory frameworks, are identified through in-depth secondary research.

This phase involves analyzing historical data and trends within the HCI market, assessing revenue growth, market penetration, and the deployment of IT infrastructure. By compiling data from both primary and secondary sources, we can estimate the markets current size and future potential.

To validate initial findings, expert consultations are conducted with key stakeholders from the HCI ecosystem, including IT managers and service providers. These insights are crucial for refining the market data and understanding practical implications.

In this final step, the validated data is synthesized into a comprehensive report, highlighting critical insights into the HCI market. This includes data on key product segments, competitive strategies, and future market trends, ensuring a well-rounded analysis.

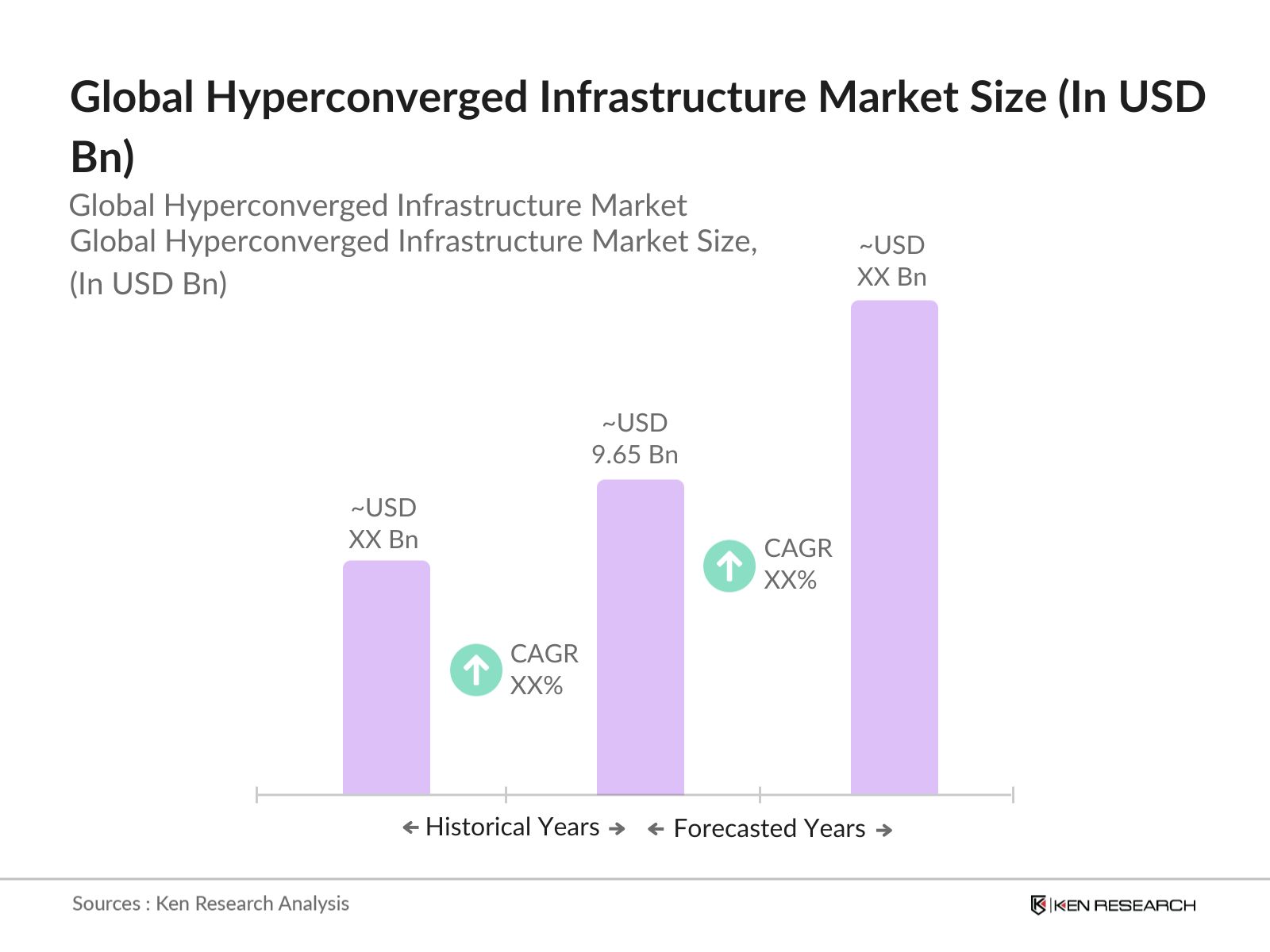

The global hyperconverged infrastructure market is valued at USD 9.65 billion based on a five-year historical analysis, driven by the growing demand for simplified IT operations and cloud-based solutions across various sectors.

Challenges include high initial investment costs, difficulties in integrating with legacy IT systems, and concerns surrounding data security, particularly for large-scale deployments.

Key players in the market include Nutanix Inc., Dell Technologies Inc., VMware Inc., Cisco Systems Inc., and Hewlett Packard Enterprise (HPE). These companies dominate the market due to their innovative product portfolios and strong global presence.

The market is primarily driven by increased cloud adoption, the need for IT infrastructure modernization, and rising demand for scalable and cost-efficient solutions in sectors like IT, telecom, and BFSI.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.