Global Orthopedic Devices Market Outlook to 2030

Region:Global

Author(s):Shivani Mehra

Product Code:KROD1954

Region:Global

Author(s):Shivani Mehra

Product Code:KROD1954

December 2024

98

Listen to the audio summary

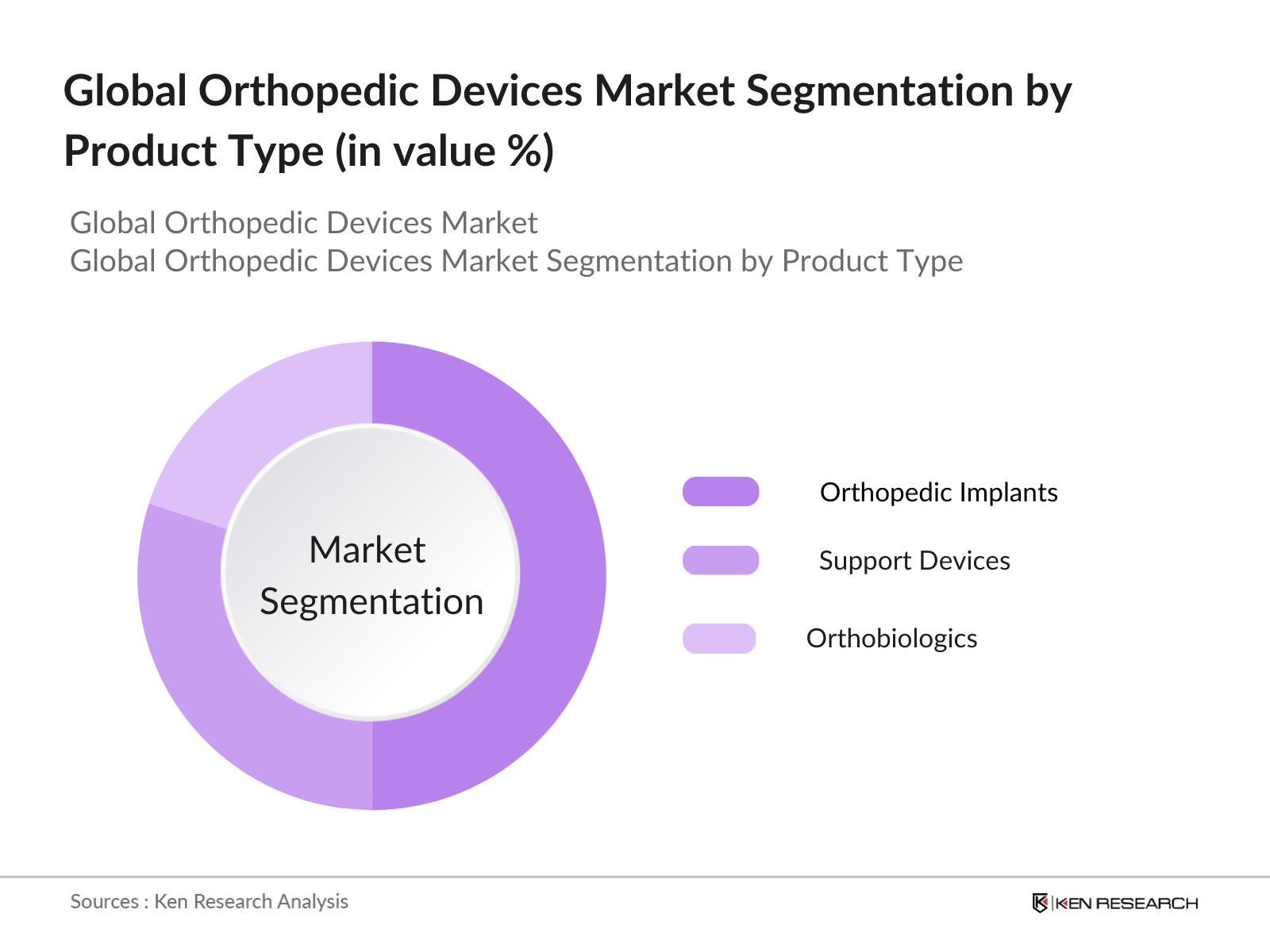

By Product Type: The orthopedic devices market is segmented into orthopedic implants, support devices, and orthobiologics. Orthopedic implants dominate this category due to their widespread application in joint replacements, fracture repairs, and other reconstructive surgeries. The dominance of orthopedic implants is attributed to their integral role in improving patient mobility and recovery times. Additionally, the rising number of joint replacement procedures and trauma-related surgeries across developed and emerging markets ensures this segment remains at the forefront

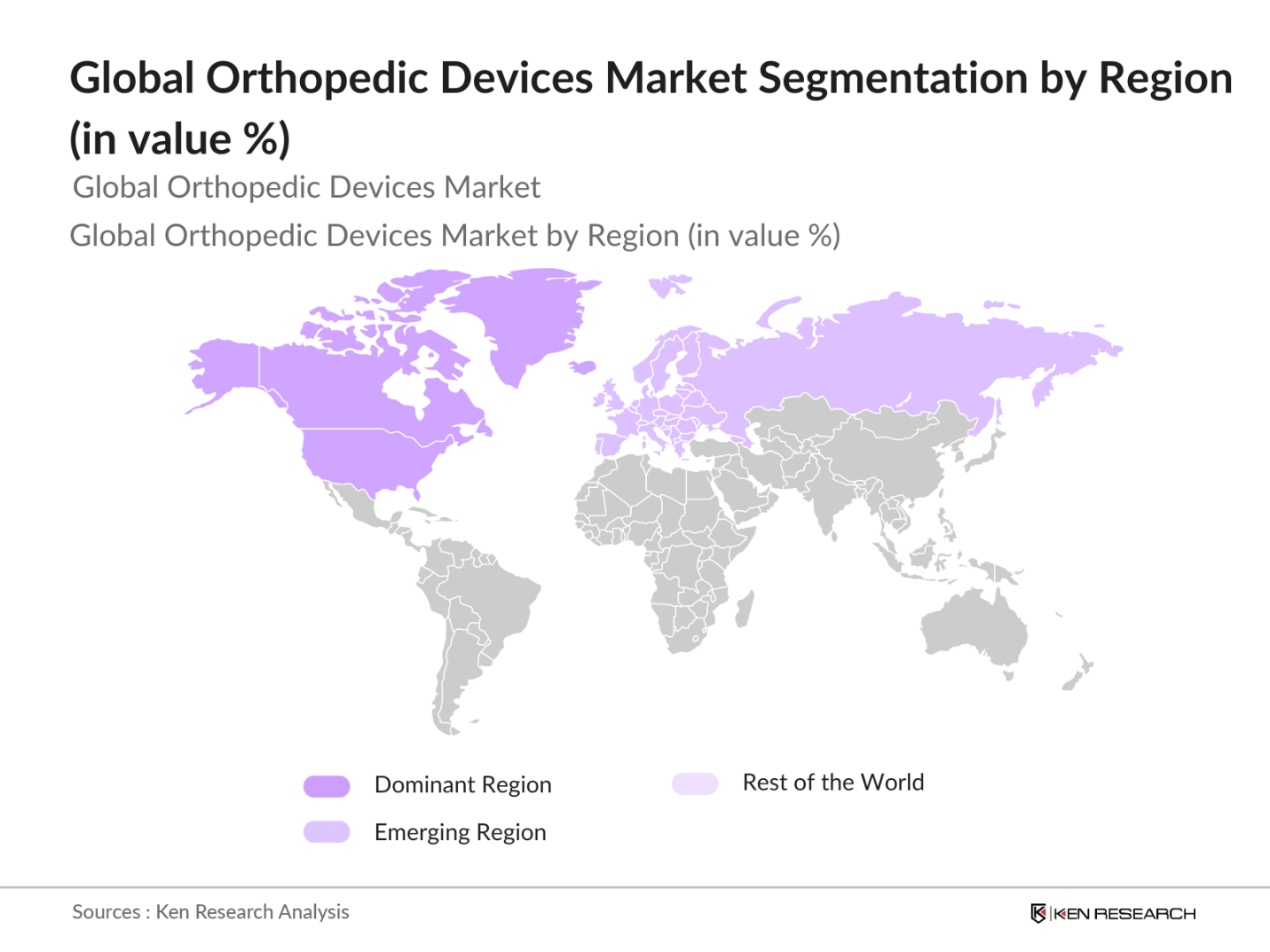

By Region: The regional segmentation of the orthopedic devices market covers North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. North America leads the market, with the U.S. being the largest contributor due to its advanced healthcare system, significant healthcare spending, and the prevalence of orthopedic surgeries. Europe follows closely behind, driven by the high rate of osteoarthritis and joint replacement procedures. The Asia-Pacific region is projected to grow rapidly owing to the increasing healthcare infrastructure and medical tourism in countries like India and China

The global orthopedic devices market is dominated by several key players, including Zimmer Biomet, Stryker Corporation, and Johnson & Johnson, who have established a strong foothold through continuous innovation, acquisitions, and expansion of their product portfolios. These companies hold a competitive advantage due to their focus on research and development, global distribution networks, and strategic collaborations. Emerging players in the Asia-Pacific region, such as MicroPort Scientific Corporation, are also gaining prominence due to their cost-effective solutions and expanding footprint

|

Company |

Year Established |

Headquarters |

Market Presence |

R&D Investments |

Product Innovations |

Global Reach |

Revenue (2023) |

Key Strategic Initiatives |

|

Zimmer Biomet Holdings |

1927 |

USA |

- |

- |

- |

- |

- |

- |

|

Stryker Corporation |

1941 |

USA |

- |

- |

- |

- |

- |

- |

|

Johnson & Johnson |

1886 |

USA |

- |

- |

- |

- |

- |

- |

|

Medtronic PLC |

1949 |

Ireland |

- |

- |

- |

- |

- |

- |

|

MicroPort Scientific |

1998 |

China |

- |

- |

- |

- |

- |

- |

Global Orthopedic Devices Market Growth Drivers

Global Orthopedic Devices Market Challenges

The orthopedic devices market is expected to experience robust growth over the next five years. Factors such as increasing geriatric populations, the rising number of sports injuries, and the growing prevalence of musculoskeletal disorders will drive the demand for orthopedic implants and devices. Technological advancements, including the adoption of 3D printing and robotic-assisted surgeries, are set to play a pivotal role in shaping the future of this market. As the healthcare infrastructure in emerging markets continues to develop, the global orthopedic devices market will witness increased penetration and expanded product offerings

Market Opportunities:

|

By Product Type |

Static Volumetric Displays Swept-Volume Displays Multi-Planar Volumetric Displays |

|

By Display Technology |

Digital Light Processing (DLP) Liquid Crystal Display (LCD) Light Emitting Diode (LED) |

|

By Application |

Medical Imaging AR/VR Advertising and Marketing Engineering and Design |

|

By End-User |

Healthcare, Automotive, Aerospace & Defense Entertainment and Media Education |

|

By Region |

North-East Midwest West Coast Southern States |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers (Increasing demand for joint replacements, trauma care, and sports injuries)

3.1.1. Technological Advancements in Minimally Invasive Surgery

3.1.2. Rising Prevalence of Musculoskeletal Disorders

3.1.3. Growing Aging Population and Osteoarthritis Cases

3.2. Market Challenges (High device costs and regulatory hurdles)

3.2.1. High Costs of Orthopedic Surgeries

3.2.2. Stringent Regulatory Frameworks

3.2.3. Lack of Reimbursement in Emerging Markets

3.3. Opportunities (Development of patient-specific implants and AI-driven solutions)

3.3.1. Patient-Specific Customized Implants

3.3.2. Robotic-Assisted Surgeries

3.3.3. Growth in Emerging Markets

3.4. Trends (Adoption of 3D Printing, Orthobiologics, and IoT-enabled devices)

3.4.1. 3D Printing for Prosthetics and Implants

3.4.2. Increased Usage of Orthobiologics in Bone Healing

3.4.3. Integration of AI and IoT in Orthopedic Devices

3.5. Government Initiatives (Healthcare policies supporting orthopedic care)

3.5.1. Regulatory Approvals in Key Markets (FDA, CE, and Other Regulatory Bodies)

3.5.2. Favorable Reimbursement Policies in Developed Markets

3.5.3. Government Funding for Medical Device Innovation

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competitive Landscape Overview

4.1. By Product Type (In Value %)

4.1.1. Orthopedic Implants

4.1.2. Support Devices

4.1.3. Orthobiologics

4.2. By Application (In Value %)

4.2.1. Hip and Pelvis Devices

4.2.2. Knee and Thigh Devices

4.2.3. Spine Devices

4.2.4. Trauma Fixation Devices

4.3. By End-User (In Value %)

4.3.1. Hospitals and Surgical Centers

4.3.2. Orthopedic Clinics

4.3.3. Ambulatory and Trauma Care Centers

4.4. By Region (In Value %)

4.4.1. North America

4.4.2. Europe

4.4.3. Asia-Pacific

4.4.4. Latin America

4.4.5. Middle East and Africa

5.1. Detailed Profiles of Major Companies (By Revenue, Market Share, R&D Investments)

5.1.1. Zimmer Biomet Holdings Inc.

5.1.2. Stryker Corporation

5.1.3. Smith & Nephew PLC

5.1.4. Johnson & Johnson Services Inc.

5.1.5. Medtronic PLC

5.1.6. Arthrex Inc.

5.1.7. Globus Medical Inc.

5.1.8. NuVasive Inc.

5.1.9. Boston Scientific Corporation

5.1.10. B. Braun SE

5.1.11. Conformis Inc.

5.1.12. Enovis Corp.

5.1.13. MicroPort Scientific Corporation

5.1.14. OrthAlign Corp.

5.1.15. Alphatec Holdings Inc.

5.2. Cross-Comparison Parameters (R&D spending, Product Portfolio, Global Reach, Innovation Focus)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Product Launches, Mergers, and Acquisitions)

5.5. Investment Analysis

5.6. Venture Capital Funding

5.7. Government Grants

5.8. Private Equity Investments

6.1. Compliance with International Standards

6.2. Certification Processes for Medical Devices

6.3. Quality Assurance in Manufacturing

7.1. Market Projections

7.2. Factors Driving Future Market Growth

8.1. By Product Type

8.2. By Application

8.3. By End-User

8.4. By Region

9.1. TAM/SAM/SOM Analysis

9.2. Customer Segment Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

The research begins with a thorough ecosystem mapping of the orthopedic devices market, identifying key stakeholders, including manufacturers, healthcare providers, and regulatory bodies. Desk research using secondary databases provides a foundational understanding of industry-level dynamics.

Next, historical data on orthopedic device sales, surgical volumes, and market penetration is compiled and analyzed. This helps construct accurate market size estimations and revenue generation insights for the forecast period.

Market hypotheses are validated through interviews with industry professionals, including orthopedic surgeons and medical device distributors. These interviews provide qualitative insights that refine market estimates and projections.

Finally, the data is synthesized into actionable insights, corroborated by the bottom-up approach. This includes detailed analysis on product performance, market trends, and future growth projections in the orthopedic devices industry.

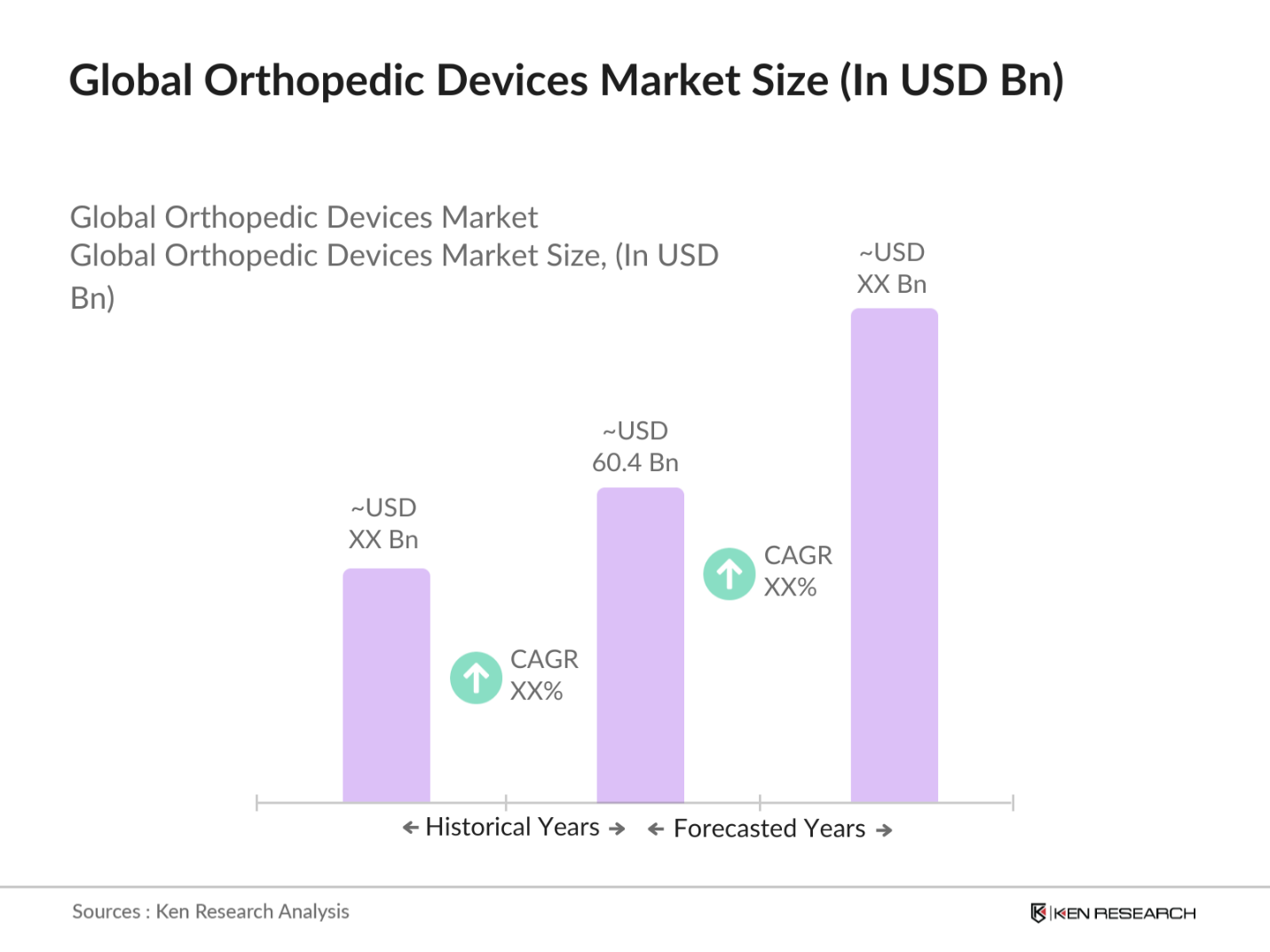

The global orthopedic devices market was valued at USD 60.4billion, driven by the increasing prevalence of musculoskeletal disorders and the adoption of advanced surgical technologies.

Key growth drivers include the growing aging population, rising cases of osteoarthritis, and the increased demand for minimally invasive orthopedic surgeries.

Major players include Zimmer Biomet Holdings Inc., Stryker Corporation, Johnson & Johnson, Medtronic PLC, and MicroPort Scientific Corporation, who dominate the market due to extensive product portfolios and strategic acquisitions.

Challenges include high costs of surgeries, stringent regulatory approvals, and the lack of adequate reimbursement in emerging markets.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.