Global Urban Air Mobility Infrastructure Market Outlook to 2030

Region:Global

Author(s):Shubham Kashyap

Product Code:KROD4425

Region:Global

Author(s):Shubham Kashyap

Product Code:KROD4425

December 2024

82

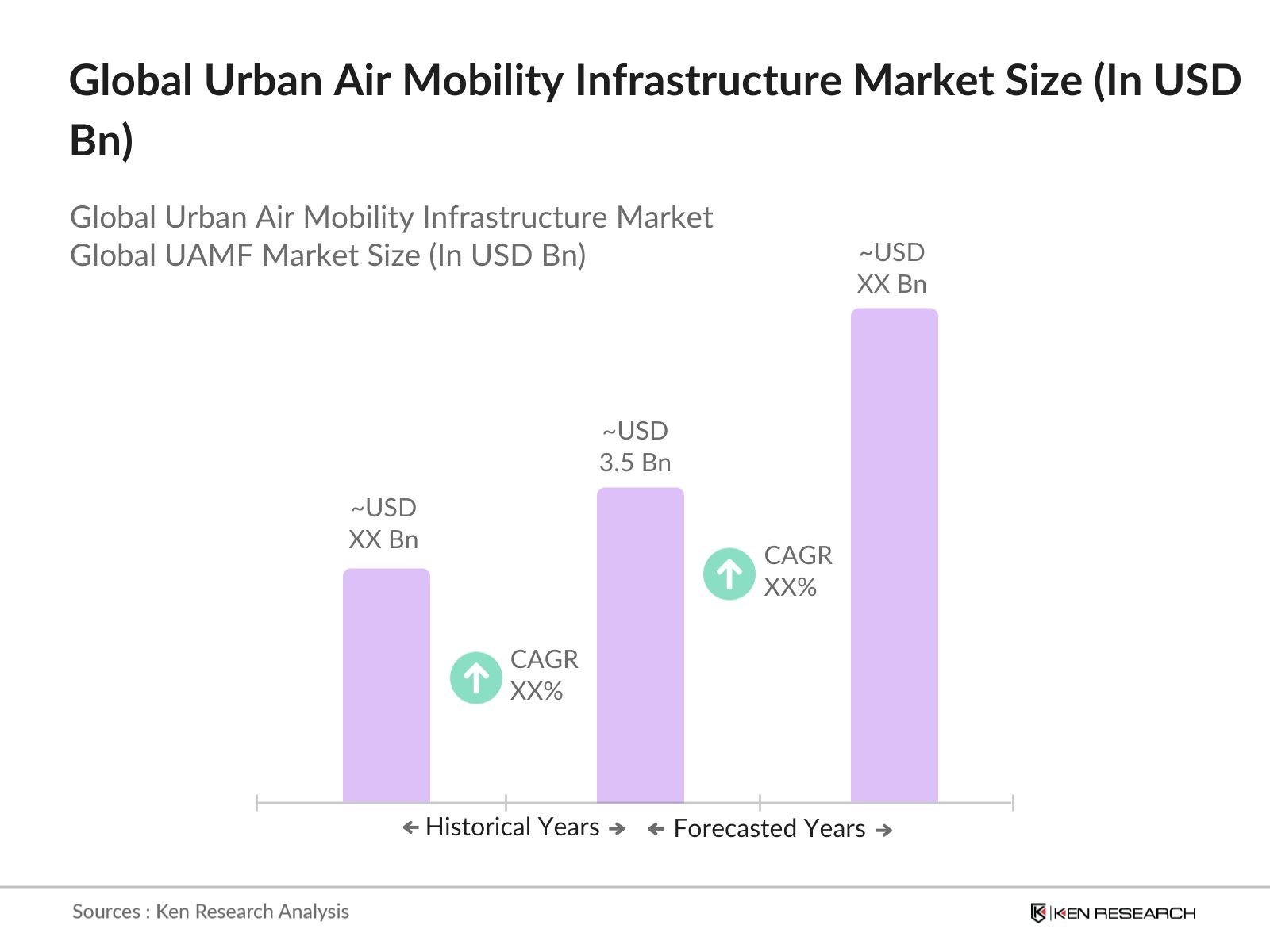

The global urban air mobility (UAM) infrastructure market is valued at USD 3.50 billion, driven by growing investments in electric vertical take-off and landing (eVTOL) aircraft infrastructure and increasing urbanization. UAM infrastructure includes vertiports, air traffic management systems, and charging stations necessary for the operation of eVTOLs in urban settings. The need to reduce congestion in major metropolitan areas is pushing governments and private companies to collaborate on building infrastructure that enables the safe operation of air taxis, cargo drones, and emergency response services.

The global urban air mobility infrastructure market is highly competitive, with key players focusing on expanding their capabilities and partnerships to deliver integrated infrastructure solutions. Companies are investing in research and development to enhance vertiport design, optimize air traffic management systems, and improve battery charging technologies for electric aircraft. Several companies are also forming strategic partnerships with city governments and aviation authorities to secure prime locations for vertiport construction and gain early market entry.

|

Company Name |

Establishment Year |

Headquarters |

Market Presence |

R&D Investment |

Global Reach |

Product Portfolio |

Certifications |

|

Joby Aviation |

2009 |

California, USA |

|||||

|

Lilium |

2015 |

Munich, Germany |

|||||

|

Archer Aviation |

2018 |

California, USA |

|||||

|

Volocopter |

2011 |

Bruchsal, Germany |

|||||

|

Urban Aeronautics |

2001 |

Israel |

Growth Drivers

Market Challenges

The global urban air mobility infrastructure market is poised for rapid expansion, driven by technological advancements, urbanization, and growing demand for sustainable transportation solutions. By 2028, major cities are expected to have established UAM networks, supported by a robust infrastructure of vertiports, air traffic management systems, and charging stations. Governments and private developers will continue to collaborate on creating the regulatory frameworks and physical infrastructure needed to support UAM services.

Future Market Opportunities

|

Infrastructure Type |

Vertiports Air Traffic Management Systems Charging Stations |

|

Vehicle Type |

Passenger eVTOL Cargo eVTOL Autonomous Drones |

|

End-User |

Government Agencies Private Developers Urban Planners |

|

Application |

Passenger Transportation Goods and Cargo Transportation Emergency Services Air Taxi Services |

|

Region |

North America Europe Asia-Pacific Middle East & Africa Latin America |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (Regulatory Approvals, Infrastructure Development, Technology Adoption)

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis (Investment in Vertiports, Adoption of Air Traffic Management Systems, UAM Pilot Programs)

2.3. Key Market Developments and Milestones (Government Collaborations, Public-Private Partnerships, Technological Advancements)

3.1. Growth Drivers

3.1.1. Urbanization and Increasing Traffic Congestion (Demand for Efficient Transportation)

3.1.2. Government Regulations Supporting UAM (Funding for Infrastructure, Airspace Management)

3.1.3. Technological Advancements in eVTOL and Battery Efficiency

3.1.4. Expansion of Smart City Initiatives (Integration of UAM into Existing Transportation Networks)

3.2. Market Challenges

3.2.1. Regulatory and Safety Concerns (Certification Processes, Noise Pollution)

3.2.2. High Infrastructure Development Costs (Vertiport Construction, Air Traffic Management Systems)

3.2.3. Air Traffic Management in Urban Areas (Coordination of Low-Altitude Airspace)

3.2.4. Public Perception and Acceptance of UAM (Safety Concerns, Trust in Autonomous Systems)

3.3. Opportunities

3.3.1. Integration of UAM with Existing Public Transportation Networks

3.3.2. Development of Green and Sustainable UAM Infrastructure

3.3.3. International Collaborations on Regulatory Frameworks and Standards

3.3.4. Increased Investment in Advanced Air Traffic Management Systems

3.4. Trends

3.4.1. Rise of Autonomous Air Traffic Management Solutions (AI and Machine Learning Integration)

3.4.2. Development of Multi-Modal Mobility Hubs (Vertiport Integration with Rail and Road Systems)

3.4.3. Increased Focus on Renewable Energy-Powered Vertiports and Charging Stations

3.4.4. Expansion of Urban Air Mobility Testbed Projects (Pilot Programs in Major Cities)

3.5. Government Regulation

3.5.1. FAAs UAM Pilot Program

3.5.2. EASAs Regulatory Framework for Urban Air Mobility

3.5.3. Funding for Urban Air Mobility Infrastructure Projects (Public Grants, Government-Backed Initiatives)

3.5.4. Airspace Integration Standards (Low-Altitude Flight Regulations)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competitive Landscape

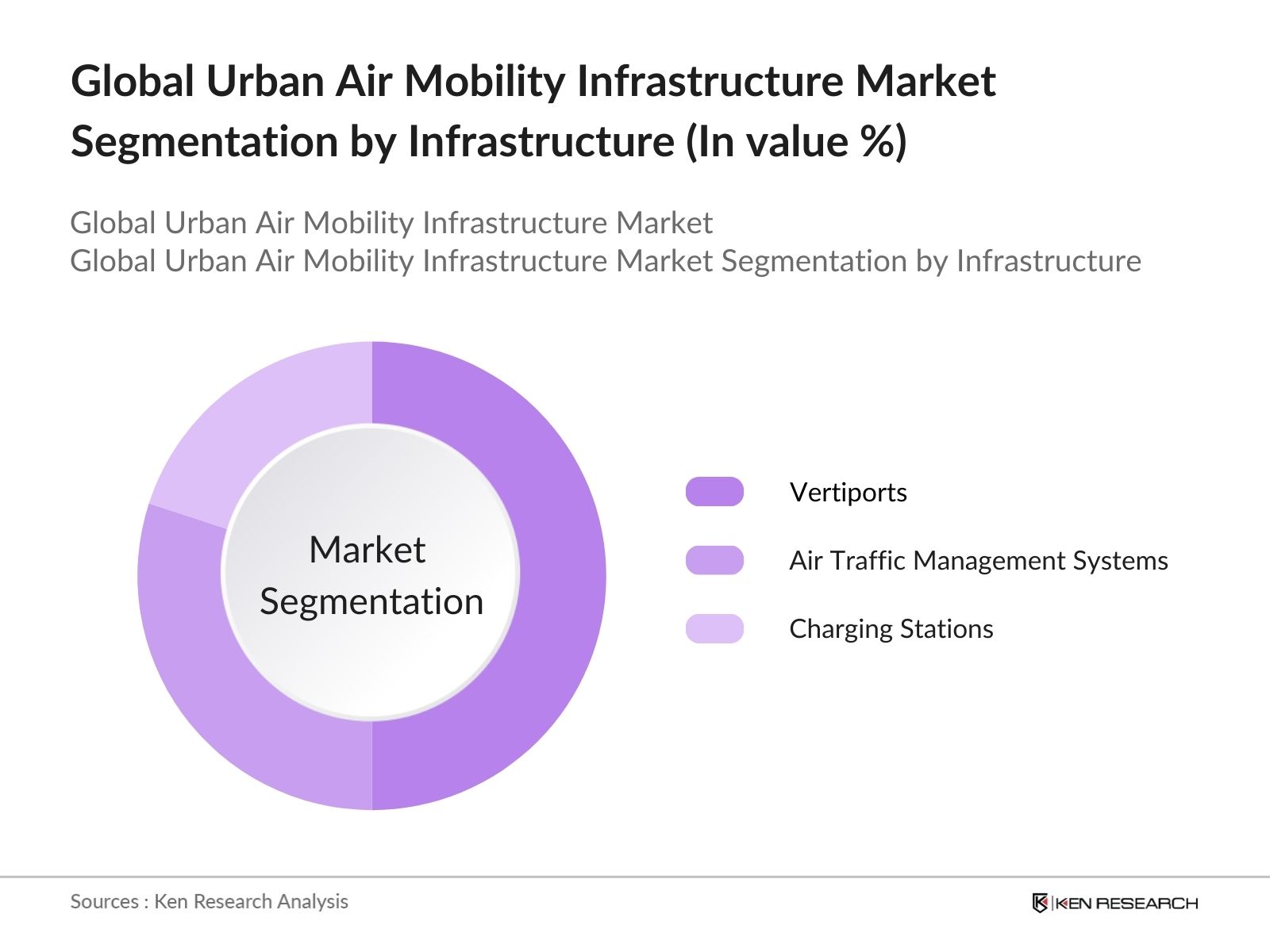

4.1. By Infrastructure Type (In Value %)

4.1.1. Vertiports

4.1.2. Air Traffic Management Systems

4.1.3. Charging Stations

4.2. By Vehicle Type (In Value %)

4.2.1. Passenger eVTOL

4.2.2. Cargo eVTOL

4.2.3. Autonomous Drones

4.3. By End-User (In Value %)

4.3.1. Government Agencies

4.3.2. Private Developers

4.3.3. Urban Planners

4.4. By Application (In Value %)

4.4.1. Passenger Transportation

4.4.2. Goods and Cargo Transportation

4.4.3. Emergency Services

4.4.4. Air Taxi Services

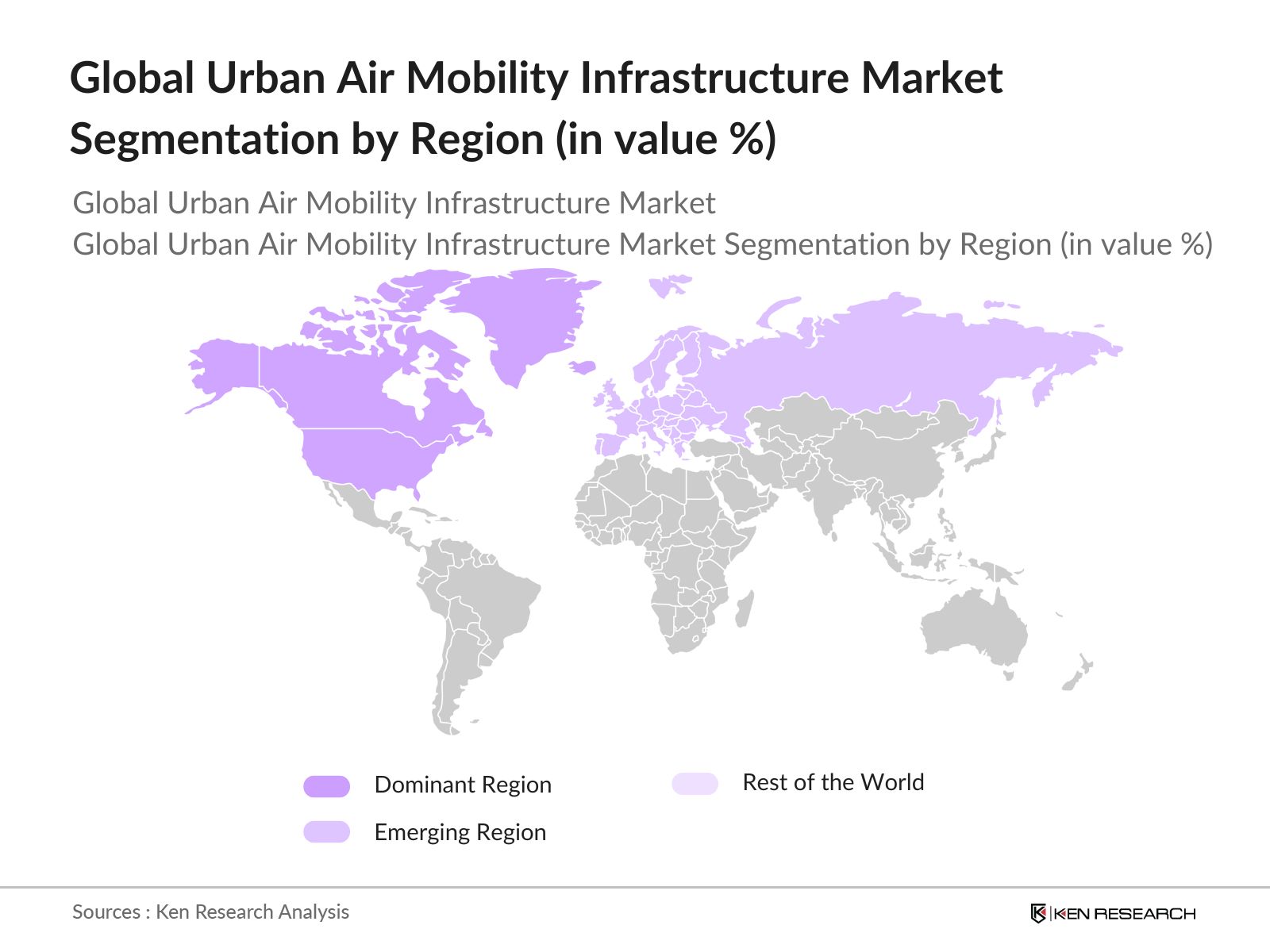

4.5. By Region (In Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia-Pacific

4.5.4. Middle East & Africa

4.5.5. Latin America

5.1. Detailed Profiles of Major Companies

5.1.1. Joby Aviation

5.1.2. Lilium

5.1.3. Archer Aviation

5.1.4. Volocopter

5.1.5. Vertical Aerospace

5.1.6. Urban Aeronautics

5.1.7. EHang Holdings

5.1.8. Airbus SE

5.1.9. Bell Textron

5.1.10. Boeing

5.1.11. Hyundai Motor Group (Supernal)

5.1.12. Embraer (Eve)

5.1.13. Pipistrel Aircraft

5.1.14. Honeywell Aerospace

5.1.15. Safran

5.2. Cross Comparison Parameters (Fleet Size, Infrastructure Investments, Vertiport Partnerships, R&D Expenditure, Market Presence, Government Contracts, Technology Readiness Level, Certification)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. UAM Environmental Standards (Noise Pollution Regulations, Carbon Emission Limits)

6.2. Compliance Requirements (Air Traffic Management Certification, Pilot Licensing)

6.3. Certification Processes (eVTOL Aircraft Certification, Vertiport Construction Standards)

7.1. Future Market Size Projections (Driven by Fleet Expansion, Vertiport Development)

7.2. Key Factors Driving Future Market Growth (Government Funding, Technological Advancements, Urban Mobility Demand)

8.1. By Infrastructure Type (In Value %)

8.2. By Vehicle Type (In Value %)

8.3. By End-User (In Value %)

8.4. By Application (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis (Government Entities, Private Infrastructure Developers, Urban Planners)

9.3. Marketing Initiatives (Focused on Urban Planners and Municipal Governments)

9.4. White Space Opportunity Analysis (Unserved Markets, Gaps in Vertiport Locations)

The initial step involved identifying key stakeholders within the urban air mobility market, such as eVTOL manufacturers, vertiport operators, and government regulators. This process was informed by extensive secondary research and proprietary databases, aiming to define the critical variables shaping market dynamics.

Historical data on UAM infrastructure projects and eVTOL developments were compiled and analyzed. Market penetration rates were assessed, focusing on the ratio of eVTOL testing locations to planned infrastructure developments. This was supplemented by a review of urban transportation initiatives.

Hypotheses were developed and validated through interviews with industry experts, including representatives from UAM infrastructure developers and government regulators. These consultations provided detailed insights into the technical challenges and operational hurdles in the sector.

In the final step, data from eVTOL manufacturers and infrastructure developers were synthesized to produce a comprehensive report. These insights were corroborated with data from industry databases and proprietary research tools, ensuring an accurate market assessment.

The global urban air mobility infrastructure market is valued at USD 3.50 billion, driven by increasing investments in eVTOL infrastructure and urban transportation alternatives.

Challenges in the global urban air mobility infrastructure market include the high cost of infrastructure development, regulatory hurdles in air traffic management, and public concerns regarding the safety and noise levels of eVTOL operations.

Key players in the global urban air mobility infrastructure market include Joby Aviation, Lilium, Archer Aviation, Volocopter, and Vertical Aerospace, who dominate the market due to their early investment in eVTOL technology and strong government partnerships.

Growth drivers in the global urban air mobility infrastructure market include increasing urbanization, advancements in eVTOL technology, and government support for sustainable and efficient urban transportation systems.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.