Global Zero Trust Security Market Outlook to 2030

Region:Global

Author(s):Naman Rohilla

Product Code:KROD5500

Region:Global

Author(s):Naman Rohilla

Product Code:KROD5500

December 2024

94

The global Zero Trust Security market is dominated by several key players, each contributing to market growth through technological advancements and strategic partnerships. The Zero Trust Security market is concentrated, with leading companies leveraging their vast distribution networks and R&D capabilities to innovate and expand globally. These players are strategically positioned to capture market share, especially with the rising demand for cloud-based Zero Trust architectures.

|

Company |

Establishment Year |

Headquarters |

Market Share |

Key Solutions |

R&D Spending |

Cloud Offerings |

Key Partnerships |

Global Presence |

Revenue (2023) |

|

Palo Alto Networks |

2005 |

Santa Clara, USA |

- |

- |

- |

- |

- |

- |

- |

|

Cisco Systems |

1984 |

San Jose, USA |

- |

- |

- |

- |

- |

- |

- |

|

IBM Corporation |

1911 |

Armonk, USA |

- |

- |

- |

- |

- |

- |

- |

|

Microsoft Corporation |

1975 |

Redmond, USA |

- |

- |

- |

- |

- |

- |

- |

|

Zscaler, Inc. |

2007 |

San Jose, USA |

- |

- |

- |

- |

- |

- |

- |

Over the next five years, the Zero Trust Security market is expected to exhibit robust growth driven by factors such as increasing cyberattacks targeting cloud infrastructure, the growing use of IoT devices, and an evolving regulatory landscape. Government agencies and enterprises across all regions are expected to adopt Zero Trust strategies to enhance their cybersecurity infrastructure. Moreover, advancements in artificial intelligence and machine learning are anticipated to further bolster the capabilities of Zero Trust solutions, making them more efficient and adaptive to evolving cyber threats.

Global Zero Trust Security Market Opportunities

|

By Solution Type |

Network Security IAM Data Security Security Analytics Endpoint Security |

|

By Deployment Mode |

On-Premises Cloud |

|

By Authentication Method |

MFA SSO Biometric Authentication |

|

By Vertical |

BFSI IT & Telecommunications Healthcare Government Retail & eCommerce |

|

By Region |

North America Europe Asia-Pacific Latin America Middle East & Africa |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Increasing Cybersecurity Threats

3.1.2. Cloud and IoT Adoption

3.1.3. Regulatory Compliance Mandates

3.1.4. Growing Demand for Remote Work Security Solutions

3.2. Market Challenges

3.2.1. High Implementation Costs

3.2.2. Complex Integration with Legacy Systems

3.2.3. Lack of Skilled Cybersecurity Professionals

3.3. Opportunities

3.3.1. Expansion in Emerging Markets

3.3.2. Adoption of AI-Driven Security

3.3.3. Rise in Hybrid Workforces

3.4. Trends

3.4.1. Identity-Based Segmentation

3.4.2. Integration with DevSecOps

3.4.3. Micro-Segmentation Adoption

3.5. Government Regulations

3.5.1. Data Protection Laws (GDPR, CCPA)

3.5.2. Cybersecurity Maturity Model Certification (CMMC)

3.5.3. National Security Directives

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competitive Landscape Overview

4.1. By Solution Type (In Value %)

4.1.1. Network Security

4.1.2. Identity & Access Management (IAM)

4.1.3. Data Security

4.1.4. Security Analytics

4.1.5. Endpoint Security

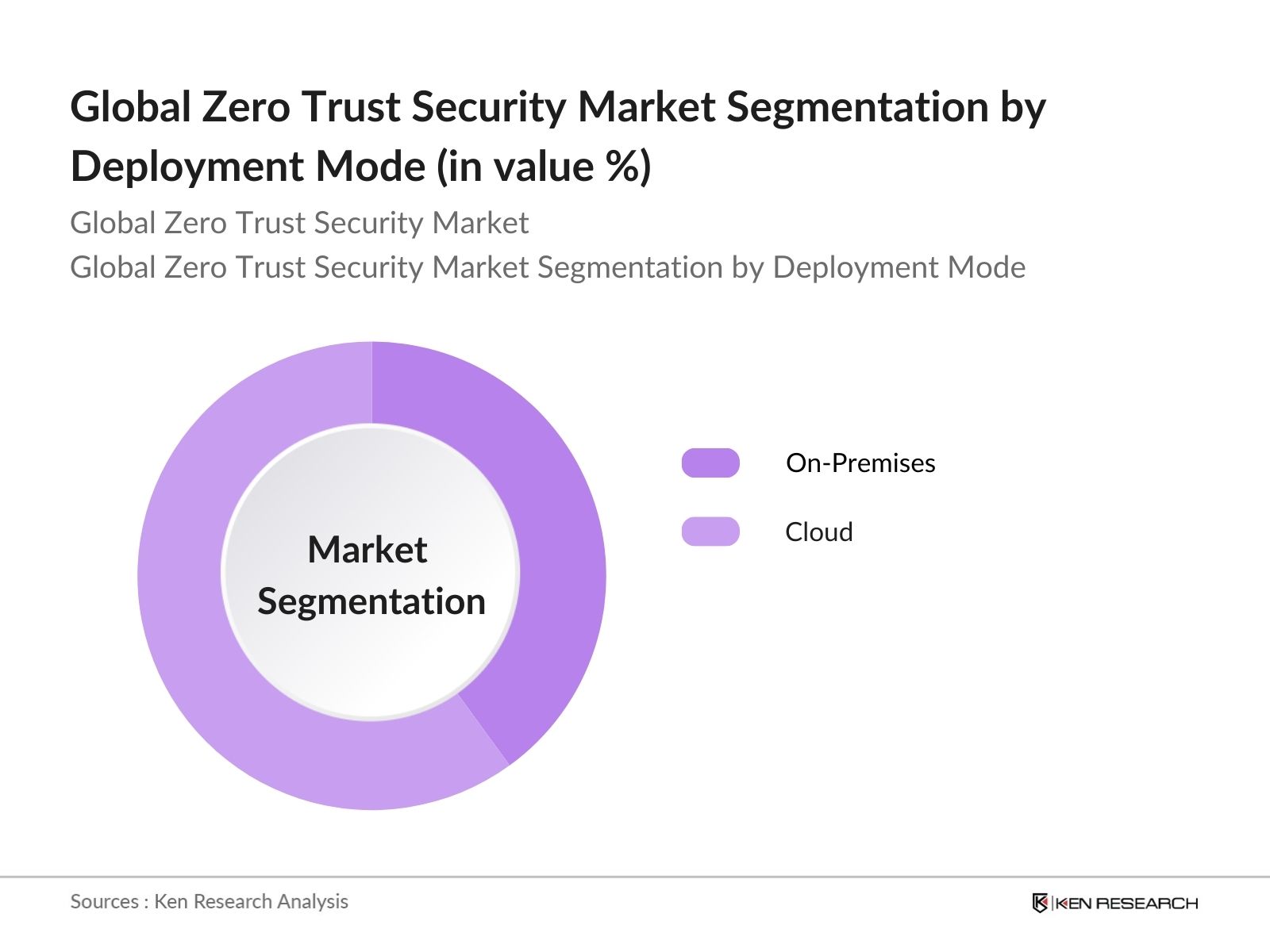

4.2. By Deployment Mode (In Value %)

4.2.1. On-Premises

4.2.2. Cloud

4.3. By Authentication Method (In Value %)

4.3.1. Multi-Factor Authentication (MFA)

4.3.2. Single Sign-On (SSO)

4.3.3. Biometric Authentication

4.4. By Vertical (In Value %)

4.4.1. BFSI

4.4.2. IT & Telecommunications

4.4.3. Healthcare

4.4.4. Government

4.4.5. Retail & eCommerce

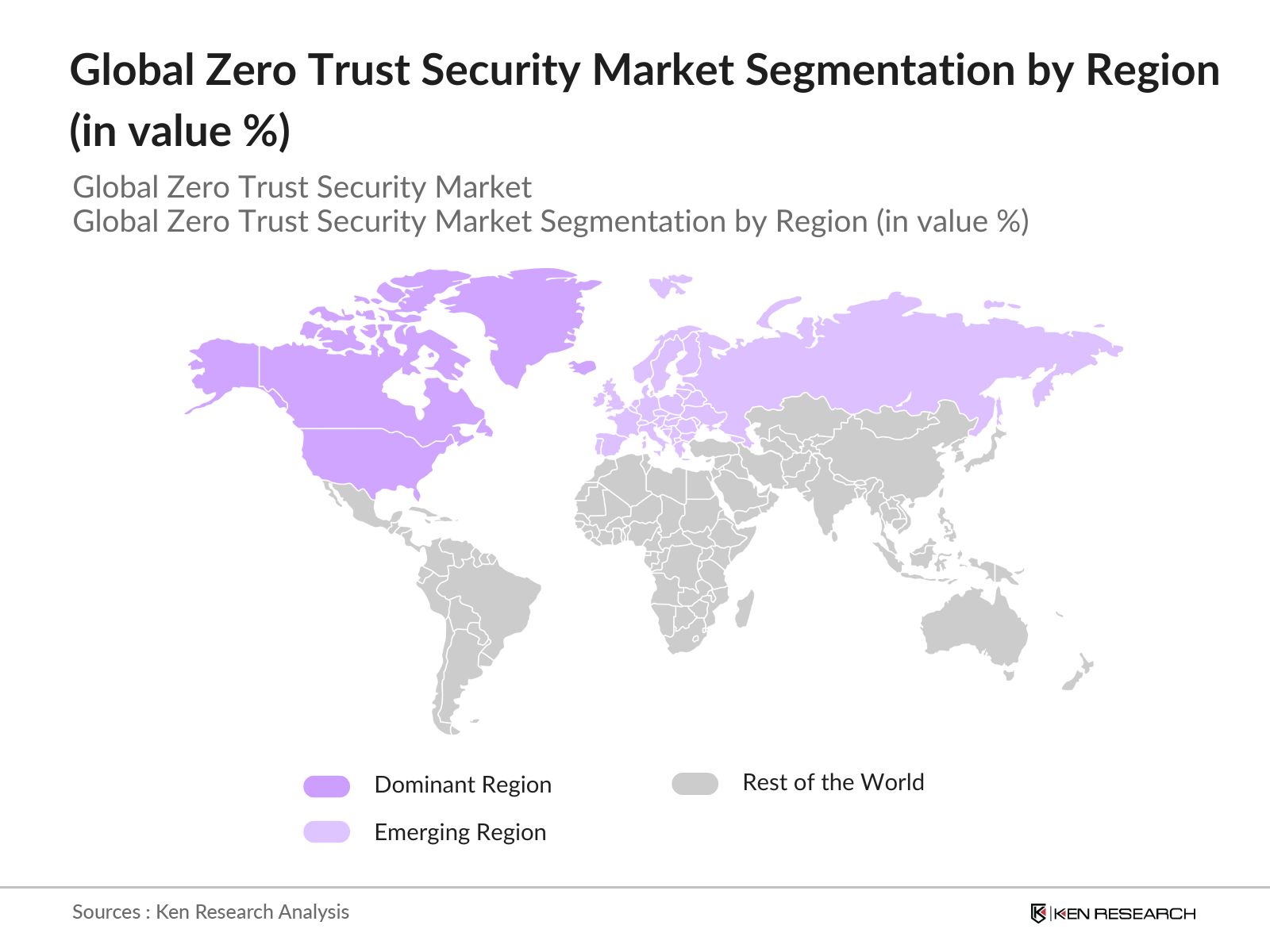

4.5. By Region (In Value %)

4.5.1. North America

4.5.2. Europe

4.5.3. Asia-Pacific

4.5.4. Latin America

4.5.5. Middle East & Africa

5.1. Detailed Profiles of Major Competitors

5.1.1. Palo Alto Networks

5.1.2. Cisco Systems, Inc.

5.1.3. IBM Corporation

5.1.4. Microsoft Corporation

5.1.5. Okta, Inc.

5.1.6. Zscaler, Inc.

5.1.7. Akamai Technologies

5.1.8. Fortinet, Inc.

5.1.9. Cloudflare, Inc.

5.1.10. CrowdStrike Holdings, Inc.

5.1.11. Check Point Software Technologies Ltd.

5.1.12. Broadcom Inc. (Symantec)

5.1.13. VMware, Inc.

5.1.14. Trend Micro Incorporated

5.1.15. Proofpoint, Inc.

5.2. Cross Comparison Parameters (Revenue, Product Offerings, Deployment Capabilities, Target Customer Base, Geographic Presence, Innovation Focus, Partnerships, Market Share)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Compliance Standards

6.2. Industry Certifications

6.3. Data Privacy & Security Laws

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Solution Type (In Value %)

8.2. By Deployment Mode (In Value %)

8.3. By Authentication Method (In Value %)

8.4. By Vertical (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Target Market Prioritization

9.3. Marketing Initiatives

9.4. Strategic Opportunity Identification

Disclaimer Contact UsThe first step involved identifying the key stakeholders and market influencers in the Zero Trust Security ecosystem. We conducted a detailed desk analysis using secondary sources such as industry reports, cybersecurity journals, and regulatory publications.

We analyzed historical data to build market models, focusing on the adoption of Zero Trust Security solutions across industries and regions. Market penetration rates were calculated based on deployment modes (cloud vs. on-premises).

We validated market assumptions through direct interviews with industry leaders and cybersecurity experts. This step ensured that our data accurately reflected current market conditions and growth projections.

The final step involved synthesizing the collected data and expert insights to deliver a comprehensive market report. The data was further validated through cross-verification with multiple industry stakeholders.

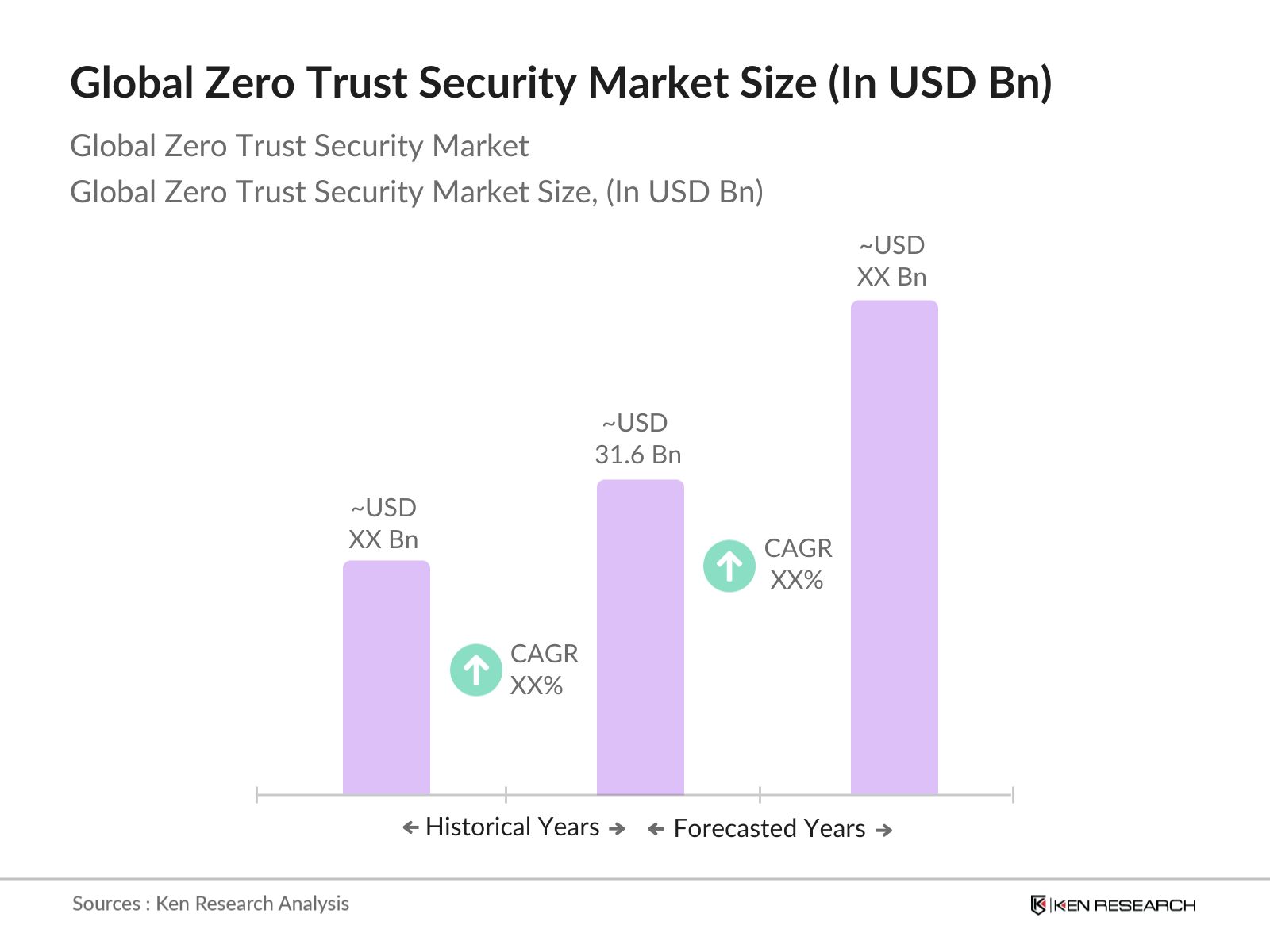

The global Zero Trust Security market is valued at USD 31.6 billion, driven by the increasing need for secure network architectures amid rising cyber threats.

Challenges in the global Zero Trust Security market include high implementation costs, integration difficulties with legacy systems, and a lack of skilled cybersecurity professionals in some regions.

Key players in the global Zero Trust Security market include Palo Alto Networks, Cisco Systems, IBM Corporation, Microsoft Corporation, and Zscaler, Inc., all leading the market due to their innovative product offerings and large global presence.

The global Zero Trust Security market is driven by the growing threat of cyberattacks, cloud and IoT adoption, regulatory compliance requirements, and increasing demand for secure remote access.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.