India Road Freight Market Outlook to 2028

Driven by robust supply chain, ignites a working capital market boom

Region:India

Author(s):Tania, Aishwarya and Pranav

Product Code:KR1450

Region:India

Author(s):Tania, Aishwarya and Pranav

Product Code:KR1450

October 2024

56

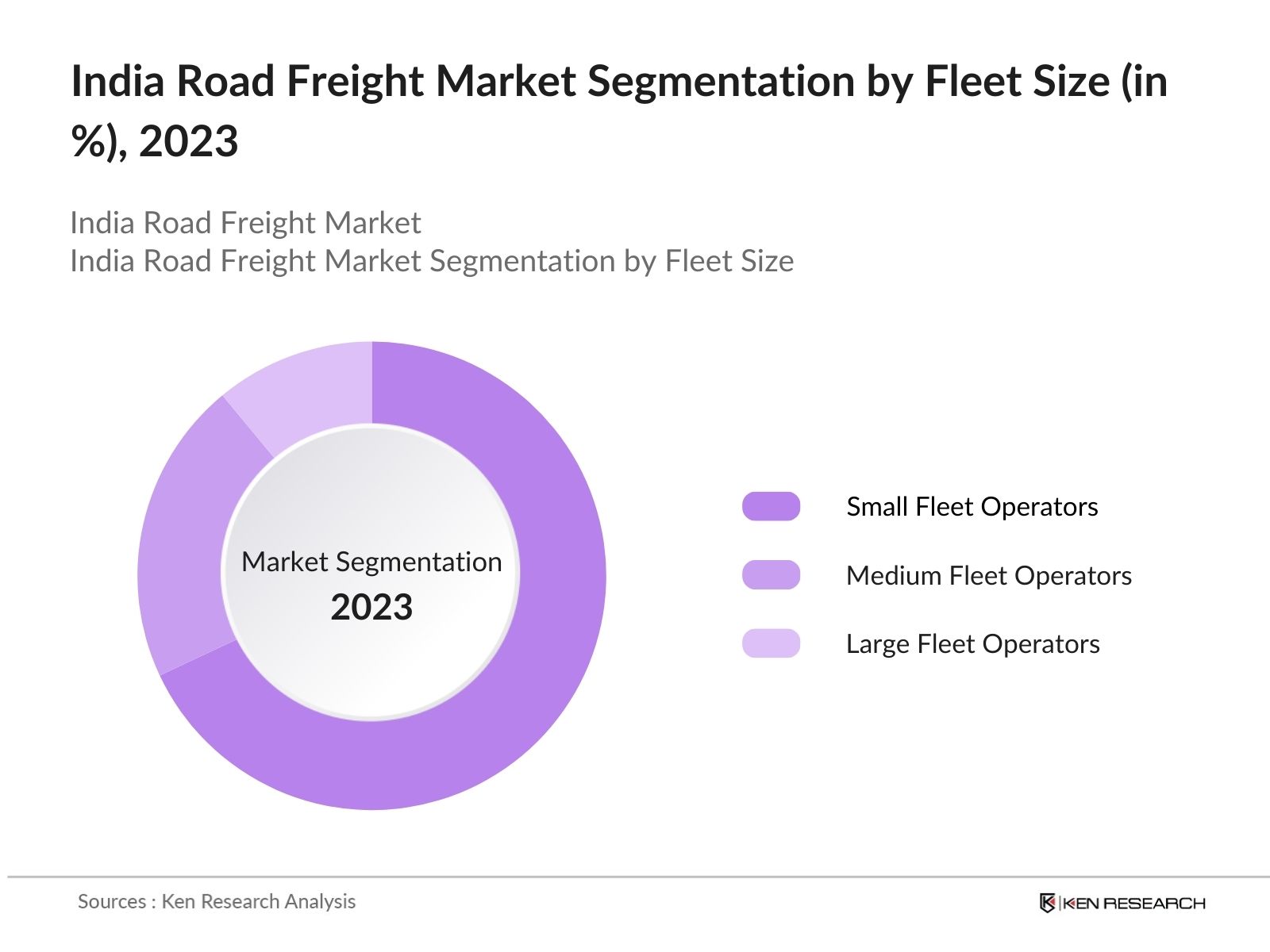

By Fleet Size: India road freight market is segmented by fleet size into small, medium and large fleets. In 2023, small fleet operators dominate the market share, mainly due to their flexibility and ability to operate at lower costs. These operators are vital in serving the spot market and cater to regions where large operators may not find it cost-effective to operate, thereby fulfilling a crucial role in Indias fragmented road freight market.

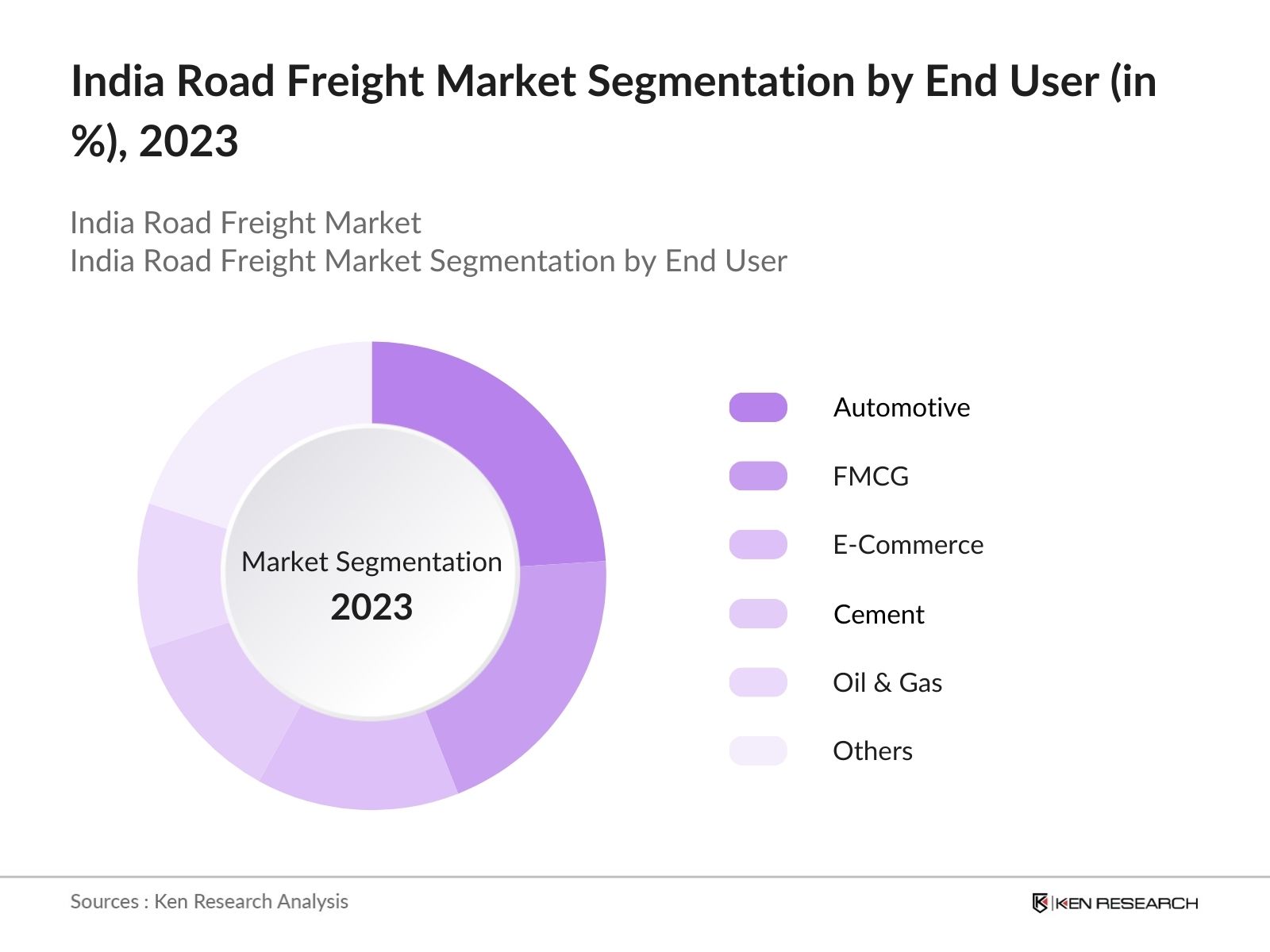

By End User: India road freight market is segmented by end user into automotive, FMCG, e-commerce, cement, oil & gas and others. The automotive sector dominates the end-user segment share. This dominance is due to the high demand for transporting vehicles and automotive parts across Indias manufacturing hubs, coupled with the need for a reliable supply chain to ensure timely production and delivery to various markets.

By Region: The India road freight market is segmented by region into North, South, East, and West. In 2023, the West region dominated the market with share. The dominance of the West region is driven by its strong industrial base, well-developed infrastructure, and proximity to key ports, which facilitate the movement of goods domestically and internationally.

4. Competitive Landscape

|

Company |

Establishment Year |

Headquarters |

|

Tata Motors |

1945 |

Mumbai, Maharashtra |

|

V Trans |

1958 |

Mumbai, Maharashtra |

|

TCI Freight |

1958 |

Gurugram, Haryana |

|

DGFC |

1965 |

Kolkata, West Bengal |

|

Bajaj Finserv |

2007 |

Pune, Maharashtra |

India Road Freight Market Growth Drivers

India Road Freight Market Challenges

Increases in Fuel Prices: Rising fuel prices significantly impact the operational costs for fleet operators in the Indian road freight market. As fuel is a major expense for transportation companies, any increase can lead to higher overall expenses, which erode profitability and reduce competitiveness. This challenge forces operators to either absorb the costs, which affects margins, or pass them on to customers, which can reduce demand.

Limited Access to Capital: Many operators in the Indian road freight market face difficulties in accessing capital, which restricts their ability to expand operations, purchase new vehicles, or maintain service quality. This lack of financial resources hinders growth and prevents companies from meeting the increasing demand for road freight services. Limited access to capital can also affect the ability to invest in technology and training, further constraining operational efficiency.

India Road Freight Market Government Initiative

National Logistics Policy Implementation: In 2024, the Indian government is rolling out the National Logistics Policy, which aims to bring down logistics costs from 14% to 8% of GDP by 2030. The policy focuses on the development of multi-modal logistics parks and the integration of digital technologies. The government is also introducing logistics hubs across key economic zones, enhancing road freight connectivity and efficiency.

Incentives for Electric Vehicles (EVs): The FAME II scheme was launched in April 2019 with an initial budget outlay of INR 10,000 crore, which was later increased to INR 11,500 crore. This funding was intended to support the adoption of electric vehicles (EVs) across various segments, including commercial vehicles. This move is expected to reduce the carbon footprint of the road freight sector and decrease operational costs for fleet operators.

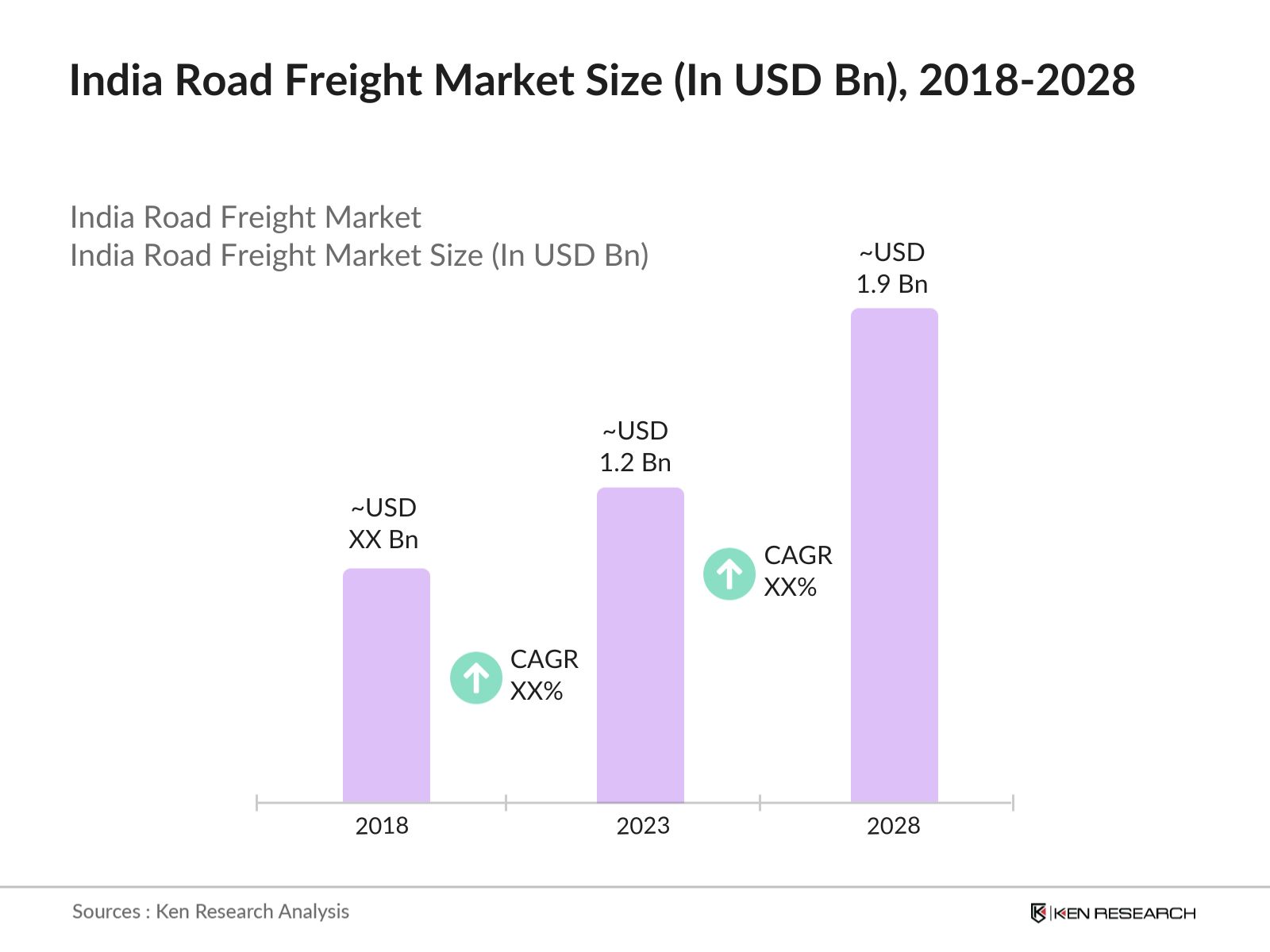

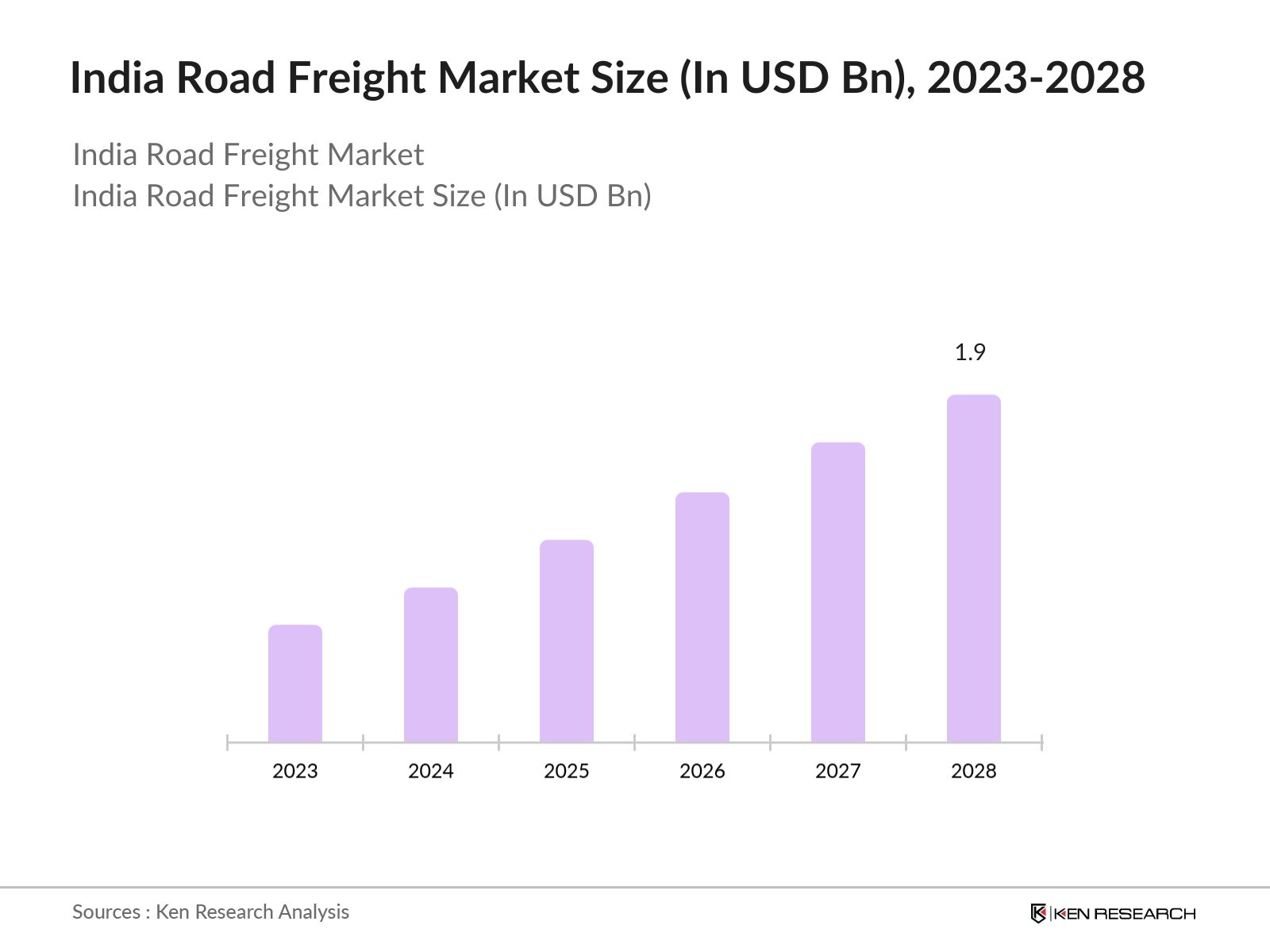

The India Road Freight Market is projected to reach USD 192 Billion by 2028. The market will witness increased adoption of electric vehicles (EVs) and advanced fleet management systems, driven by the need for cost efficiency and sustainability. The automotive, FMCG, and e-commerce sectors are expected to remain dominant, with significant contributions to the overall market revenue.

Future Trends

Expansion of Digitalization in Freight Management: The future of India's road freight market will increasingly rely on digitalization, with the adoption of cloud-based transportation management systems (TMS), electronic logging devices (ELDs), and mobile apps. These technologies will enable real-time tracking, optimize routes, and improve overall efficiency, making digital tools a must-follow trend for companies aiming to stay competitive and reduce operational costs in the evolving logistics landscape.

Growth of Green Logistics Initiatives: As environmental concerns become more prominent, the adoption of green logistics practices is expected to rise. The future will see a greater emphasis on eco-friendly vehicles, fuel-efficient technologies, and carbon-neutral delivery solutions. Companies in the Indian road freight market will invest in sustainable transportation options to align with global environmental standards and reduce their carbon footprint, making green logistics a key long-term target for the industry.

|

By Product Type |

Large Fleet Operators Medium Fleet Operators Small Fleet Operators |

|

By End User |

Automotive FMCG E-Commerce Cement Oil and Gas Steel Construction Material Others |

|

By Region |

North South East West |

1.1 Key Takeaways | India Road Freight Market & Competitive Outlook

2.1 Logistics Industry Overview (Market Size, LPI Index, Modes of Transportation, End User Applicability, Ecosystem)

2.2 India Road Freight Market [Historical / Current & Projected Market Size, Segmentation Split by - Fleet Size (<10, 10-30, 30+); Transporter Turn Over (<10 Cr., 10-25 Cr. 25-100 Cr., >100 Cr.)]

2.3 End User Segment Analysis for Automotive, Cement, FMCG, E-commerce, Steel, Oil & Gas etc. (Market Attractiveness, Margin Analysis, Cluster / Road Freight Corridor Identification across States, Key Challenges & Opportunities)

3.1 Industry Ecosystem (Banks, NBFCs, etc.)

3.2 Process Map for a Working Capital Loan Disbursement (Cash Conversion Cycle, Debt Collection Period, TBD)

3.3 Working Capital Cycle of Medium / Large Fleet Operator

3.4 Working Capital Cycle for the End Users (Automotive, Cement, FMCG, E-commerce, Steel, Oil & Gas etc.)

3.5 Future Growth & Potential of Working Capital Financing - Basis Fleet Size & End User Sectors

4.1 Highlights & Lowlights - Major NBFCs in India

4.2 Benchmarking of Major Players on Attributes - Product Offering, Type of Market Institution, Key Industries Served, Clients Served, Certifications, Book Size, Disbursements, Portfolio Quality

Ecosystem creation for all the major entities and referring to multiple secondary and proprietary databases to perform desk research around market to collate industry level information.

Collating statistics on this industry over the years, penetration of marketplaces and service providers ratio to compute revenue generated for India Road Freight industry. We will also review service quality statistics to understand revenue generated which can ensure accuracy behind the data points shared.

Building market hypothesis and conducting CATIs with industry experts belonging to different road freight companies to validate statistics and seek operational and financial information from company representatives.

Our team will approach multiple construction companies and understand nature of product segments and sales, consumer preference and other parameters, which will support us validate statistics derived through bottom to top approach from such road freight companies.

The India road freight market was valued at USD 1.2 Tn in 2023 and is driven by the expanding e-commerce sector, infrastructure development, and rising demand for efficient logistics solutions across various industries.

Challenges in the India Road Freight market include a severe shortage of skilled truck drivers, overcapacity leading to intense price competition, inadequate road infrastructure in many regions, and fuel price volatility, all of which impact operational efficiency and profitability.

Key players in the India Road Freight market include Tata Motors, V Trans, TCI Freight, DGFC, and Bajaj Finserv. These companies lead the market due to their large fleet sizes, advanced logistics solutions, and extensive geographic reach across India.

The India Road Freight Market is driven by the rapid expansion of e-commerce, significant government investments in infrastructure, rising industrial production, and increasing demand for cold chain logistics to transport perishable goods.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.