India Used Two Wheeler Market Outlook to FY 2028

Driven by increased pricing of new Two-Wheelers and increasing working population in the country

Region:India

Author(s):Twinkle & Sunaiyna

Product Code:KR1395

Region:India

Author(s):Twinkle & Sunaiyna

Product Code:KR1395

January 2024

106

Amongst 2 wheelers i.e., scooters & motorcycles, 75% of 2 wheelers sold in FY’23 are motorcycles. Amongst motorcycles, commuting bikes have been the most preferred option. In 2023, there has been increasing focus on product quality & ensuring rigorous certifications & checkpoints to ensure quality of vehicle sold to consumer. BikeDekho, BikeWale, OLX, Quickr are the top players in the online used two-wheelers market. The major challenges in this market are the identification of unauthorized dealers & lack of reasonable financing options.

New 2W Sales in the Indian automotive industry have suffered a major slump in FY’21 and FY’22, with negative growth because of introduction of the BS VI norms, which increased the price of vehicles coupled with COVID pandemic posing lockdown across the country. The growth rate of used Two-Wheelers declined in FY’20, as consumers kept their Two-Wheelers with a view of retaining them for a longer period, since BS VI standards increased the price of new vehicles. Post which the sales increased in FY’22 and FY’23 owing to the rising average household income in India and change in consumer buying behavior.

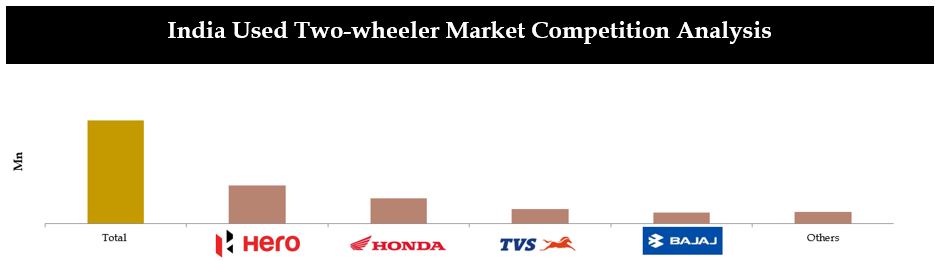

Hero Sure has generated the largest sales volume of 60,000 in FY’23. Their key strategy involved operations via dealerships which targeted Tier 3 & 4 cities along with rural areas. Hero Sure is followed by Honda Best Deal which has a sales volume of 32,000 who have 200+ franchisees in India which work on Exchange & Buy-Sell Model. Most of these players follow a mixed approach of maintaining an offline & online presence and ensure adequate distribution & maintaining relationships post-sales. Ducati offers used bikes with less than 5 years with certified mileage lower than 50,000 km, after passing 35 rigorous tests.

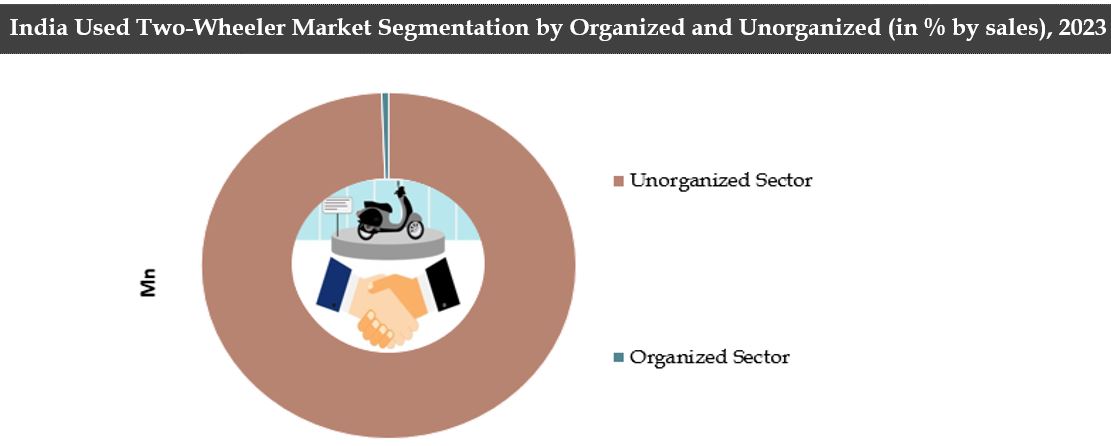

By Organized and unorganized Market: The unorganized sector of the India Used Two-Wheeler market contributes up to ~99% of the overall market whereas the organized sector contributes only ~1% of the revenue. The unorganized sector gains their revenue from commission received from sale of used vehicles and Repair & Maintenance services. The synergy with local unorganized players is expected to escalate the market further.

Organized Sector: Defined as dealers having presence of 2 or more stores in >1 city pan-India and operates on an online marketplace. Majorly OEM’s form the organized market in India.

Unorganized Sector: Defined as dealers having presence of

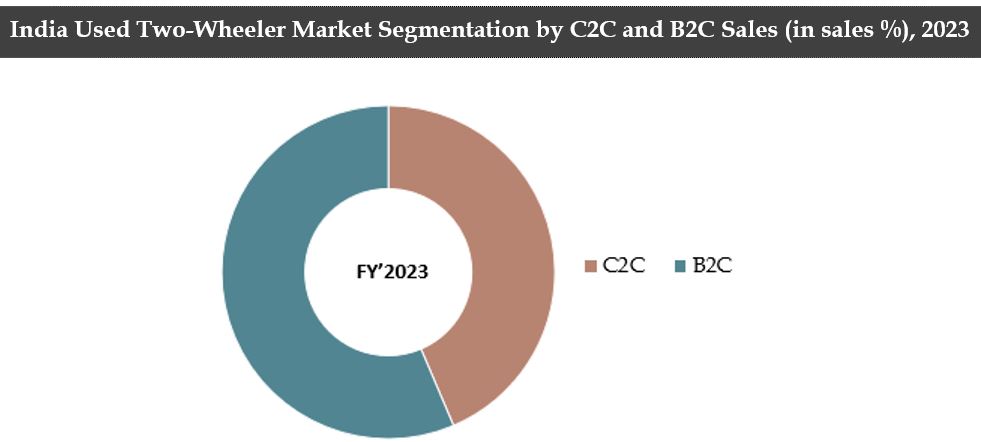

By C2C and B2C Sales: The B2C segment has a dominant share with ~57% of the overall sales whereas C2C segment contributes up to ~44%. The preference of buying from Friends & Family have been driving the C2C market and better value-added services are expected to drive the B2C market due to increasing market organization, the B2C segment is increasing & is expected to continue growing soon.

C2C Model: It includes online and offline sales of used Two-Wheelers between consumers themselves. This may take place among people who know each other such as acquaintances, friends, or relatives.

B2C Model: It includes offline sales of used Two-Wheelers between consumers and businesses, for which the leads are either generated online or directly through Physical Walk-ins. This may take place among people who don’t know each other.

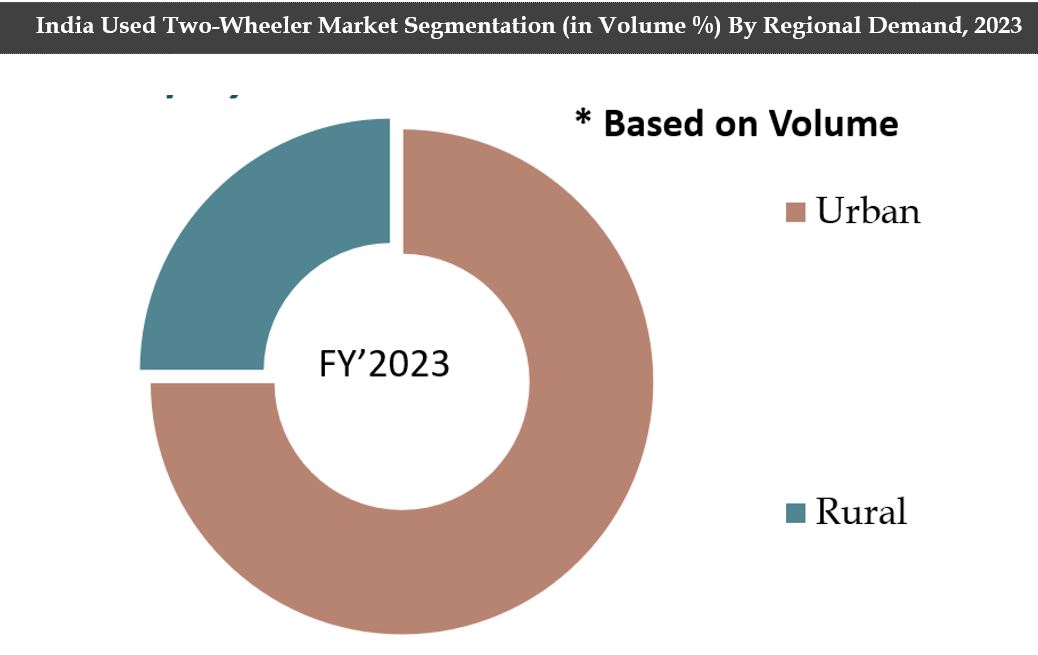

By Regional Demand: Based on volume, the number of used two-wheeler vehicles, 75 per cent of its usage occurred in urban areas and 25 per cent of sales in rural areas. In India, cities like Delhi NCR, Mumbai, Pune & Bangalore have been high potential areas for growth & Pune has displayed medium growth potential. Factors like migrant population, lack of public transport, growing IT hubs with increasing workforce & traffic congestions are few factors which drive the market’s growth.

|

India Used Two-Wheeler Market Segmentation |

|

|

By Organized and Unorganized Market |

· Organized Sector · Unorganized Sector |

|

By C2C & B2C Sales |

· C2C · B2C |

|

By 2W and type of motorcycles |

· Scooters · Motorcycles: Sports, Commuter bikes and others |

|

By Domestic & Import Sales |

· Domestic Production · Imports |

|

By Stock Piece & Customized Sales |

· Stock Piece · Customized |

|

By Engine Capacity |

· 100-110 CC · 125-135 CC · 150-200 CC · Others |

|

By Age of Vehicles |

· 0-2 Years · 2-4 Years · 4-5 Years · 5-6 Years · 6+ Years |

|

India Used two -Wheeler Market By pricing |

|

|

By Engine Capacity |

· 50 cc · 100 cc · 110 cc · 125 cc · 150 cc · 180 cc · 200 cc · 220 cc · 250 cc · 350 cc · 400 cc |

|

By Non-Certified & Certified |

· Non certified · Certified |

|

By Non-Financing & Financing |

· Financing · Non financing |

|

By Regional Demand |

· Rural · Urban |

|

India Used Two-Wheeler Market: By Customer Profile |

|

|

By Gender |

· Male · Female |

|

By Age-Group |

· 0-14 Years · 15-19 Years · 20-24 Years · 25-44 Years · 45-64 Years · 65-79 Years · 80+ Years |

|

By Income Level |

· 2.5 LPA · 5-7 LPA · 7-9 LPA · 9 LPA and Above |

1.1 Executive Summary (Industry Overview, Challenges & Trends)

1.2 Executive Summary – Used Two-Wheeler Financing

2.1 Two-Wheeler Landscape in India

2.2 Overview of Used Two-Wheeler Industry

2.3 Value Chain Analysis of India Used Two-Wheeler Market

2.4 New Two-Wheeler Vehicle Market (FY’2023-FY’2028E)

2.5 Online Market for Used Two-Wheeler

2.6 Mobility Challenges in India

2.7 Business Cycle and Genesis

2.8 Cross Comparison of Used Two-Wheeler Industry with Other Countries

2.9 Comparison Between Unorganized and Organized Dealers on The Basis Of Revenue Streams, Margins, Presence And Target Audience Etc.

2.10 Type of Organized & Unorganized Dealers in the Indian Used Two-Wheeler Market

2.11 Different Type of Stakeholders in the Indian Used Two-Wheeler Market

2.12 Overview of Buying a Used Two-Wheeler

3.1 Used Bike sales: Methodology

3.2 Market Size Scenario on the Basis of GTV, Volume Sales and Average Price

4.1 Market Segmentation on the basis of Organized and Unorganized Market, FY’2023

4.2 Market Segmentation on the basis of C2C & B2C Sales, FY’2023

4.3 Market Segmentation on the basis of Type of 2W and Type of Motorcycles, FY’2023

4.4 Market Segmentation on the basis of Stock Piece & Customized Sales and Domestic Production and Imports, FY’2023

4.5 Market Segmentation on the basis of Engine Capacity (100-110 CC, 125-135 CC, 150-200 CC), FY’2023

4.6 Used Two-Wheeler Pricing (By Engine Capacity & By Best Selling Models: Bikes and Scooters)

4.7 Gender and Brand Wise Scooter Preference

4.8 Market Segmentation on the basis of Non-Certified & Certified and Non-Financing & Financing, FY’2023

4.9 Market Segmentation on the Basis of Major Brands, FY’2023

4.10 Market Segmentation on the Basis of Regional Demand, FY’2023

8.1 Major OEM and Online Platform and Their Finance Partner

8.2 Various Business Models for Sale of Used Two-Wheeler Loans

8.3 Financing Penetration and Trends in The Used Two-Wheeler Financing

8.4 NBFC Portfolio and Role of Technology in Future

8.5 NBFC Players Offering Used Two-Wheeler Financing

8.6 Recent Trends and Role of Technology In The Used Two-Wheeler Financing

8.7 Used Two-Wheeler Financing in India

8.8 Financing Norms

8.9 Risks associated with Two-Wheeler Finance

6.1 Overview of Franchisee Based Business Model

7.1 Sales on the Basis of Volume, FY’2023

7.2 Cross Comparison Between the Major Players in the Used Two-Wheeler Market

7.3 Cross Comparison Between the Major Players in the Used Two-Wheeler Market

7.4 Strengths and Weakness of Organized Players

7.5 Case Study: BikeWale (Car Trade Group)

7.6 Case Study: Honda Best Deal

8.1 Major Pain Points and Solutions

8.2 Online Used Two-Wheeler Market (FY’2023 – FY’2028F)

8.3 Cross Comparison on the Basis of Business Model

8.4 Timeline for a customer process

8.5 Competitive Scenario

8.6 Market Share of The Players in the Online Used Two-Wheeler Market

8.7 Market Share of Online Classifieds, October, 2023

8.8 Cross Comparison of Major Players in the Online Used Two-Wheeler Market

8.9 Strength and Weakness of Major Players in the Online Used Two-Wheeler Market

9.1 Online Vehicle Buying Process

9.1.1 Buying Criteria

9.1.2 Selling Criteria

9.2 Findings on Consumer Analysis

9.3 Online vs Offline Business Stream (on the Basis of Lead Generation)

9.4 Customer Profile Statistics-

9.4.1 By Gender (Male, Female), FY’2023

9.4.2 By Age Group, FY’2023

9.4.3 Income Level, FY’2023

10.1 Government Regulations

10.2 Trends and Development

10.3 Growth Constraints

10.4 SWOT Analysis

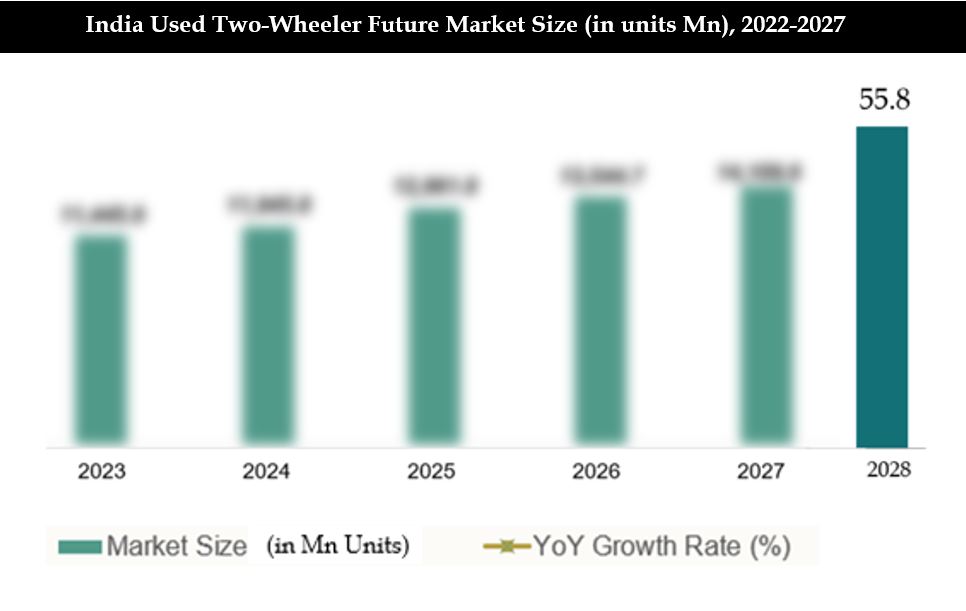

11.1Future Market Size, FY’2023 to FY’2028E (By Sales Volume)

11.2 Opportunity Landscape for Future

11.3 Future Market Segmentation by B2C & C2C by Volume, FY’2028

11.3 Future Market Segmentation by Organized & Unorganized, FY’2028

11.4 Future Growth Drivers for Used Two-Wheelers in India

12.1 Potential Market Opportunity

12.2 Sales Channels

12.3 Profitability Model for Used 2W Dealer

Step: 1 Identifying Key Variables: Ecosystem creation for all the major entities and referring to multiple secondary and proprietary databases to perform desk research around market to collate industry level information.

Step: 2 Market Building: Collating statistics on 2W market over the years, penetration of marketplaces and service providers ratio to compute revenue generated for India Used two-wheeler market. We will also review service quality statistics to understand revenue generated which can ensure accuracy behind the data points shared.

Step: 3 Validating and Finalizing: Building market hypothesis and conducting CATIs with industry exerts belonging to different companies to validate statistics and seek operational and financial information from company representatives.

Step: 4 Research output: Our team will approach multiple used vehicles providing channels and understand nature of product segments and sales, consumer preference and other parameters, which will support us validate statistics derived through bottom to top approach from 2W providers.

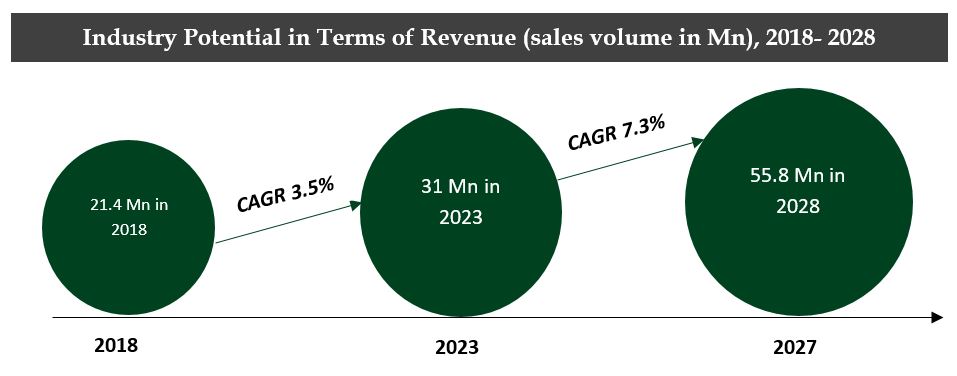

The India Used Two-Wheeler Market was valued at 31.8 Mn Units in 2023.

Higher demand for used vehicles, urbanization and likely to fuel the growth in the India Used Two-Wheeler Market.

BikeWale, OLX, Quikr etc. are some of the key players in the India Used Two-Wheeler Market

The India Used Two-Wheeler Market is expected to reach 55.8 units Mn by 2027.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.