Indonesia Clinical Research Organization Market Outlook to 2030

Region:Indonesia

Author(s):Shreya Garg

Product Code:KROD6093

Region:Indonesia

Author(s):Shreya Garg

Product Code:KROD6093

December 2024

81

Listen to the audio summary

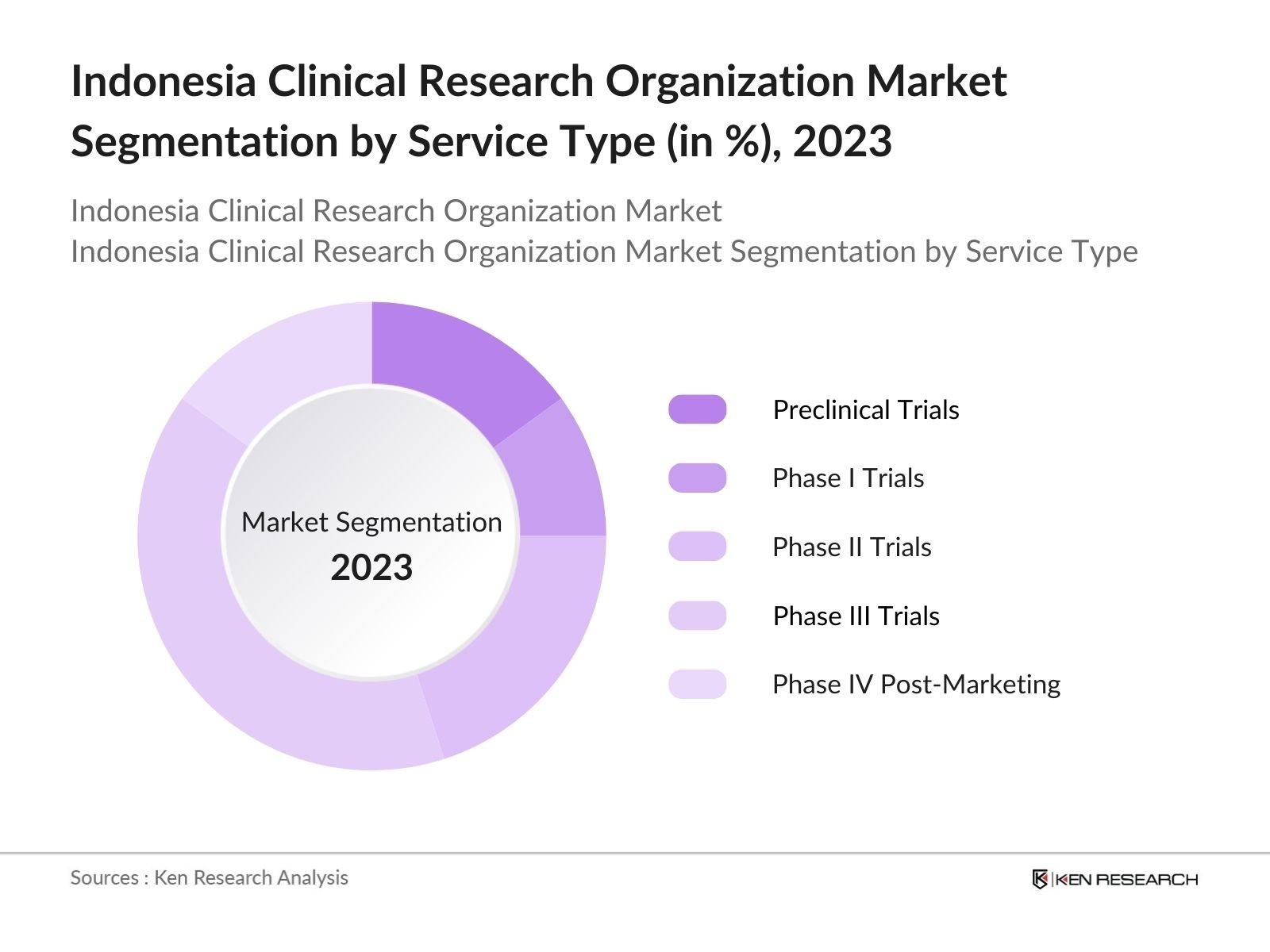

By Service Type: The market is segmented by service type into Preclinical Trials, Phase I Trials, Phase II Trials, Phase III Trials, and Phase IV Post-Marketing Trials. Among these, Phase III Trials hold the largest market share. This segment is dominant because Phase III trials involve a larger patient population and longer study durations, which require more resources and expertise, making it a crucial phase in drug approval. The high cost associated with these trials also increases revenue for CROs in this category, driving its dominance.

By Therapeutic Area: The market in Indonesia is further segmented by therapeutic area into Oncology, Cardiovascular Diseases, Infectious Diseases, Neurology, and Immunology. Oncology dominates this segment due to the high incidence of cancer in Indonesia, which increases the demand for cancer-related clinical trials. Oncology trials are complex, long, and involve a large number of patients, making them highly profitable for CROs. Additionally, the global interest in cancer drug development has made oncology one of the most active therapeutic areas for clinical research.

The Indonesia Clinical Research Organization market is dominated by several key players, including local and global CROs. These companies have a presence due to their long-standing relationships with pharmaceutical companies, operational excellence, and deep regulatory knowledge. The Indonesia CRO market is primarily dominated by global players such as ICON Plc, IQVIA, and Parexel International, alongside prominent local players like Prodia Clinical Laboratory. These companies lead the market through their vast clinical trial networks, comprehensive service offerings, and high expertise in navigating Indonesias regulatory framework.

|

Company Name |

Establishment Year |

Headquarters |

Global Reach |

Therapeutic Specialties |

Number of Trials Conducted |

Local Partnerships |

Regulatory Expertise |

Technology Integration |

Revenue |

|

ICON Plc |

1990 |

Ireland |

|||||||

|

IQVIA |

1982 |

USA |

|||||||

|

Parexel International |

1982 |

USA |

|||||||

|

Prodia Clinical Laboratory |

1973 |

Indonesia |

|||||||

|

Medpace Holdings Inc. |

1992 |

USA |

Over the next five years, the Indonesia Clinical Research Organization market is expected to see substantial growth driven by increasing investments in drug discovery, continuous expansion of healthcare infrastructure, and the availability of a large patient pool for clinical trials. The rise of precision medicine and the integration of advanced clinical trial technologies, such as AI and machine learning, will further enhance the market's capabilities. The governments efforts to streamline regulatory processes and encourage foreign investment in the healthcare sector will attract global pharmaceutical and biotechnology companies to Indonesia.

|

Service Type |

Preclinical Trials Phase I Phase II Phase III Phase IV |

|

Therapeutic Area |

Oncology Cardiovascular Infectious Diseases Neurology Immunology |

|

End User |

Pharma & Biotech Medical Devices Academic Institutions Government Organizations |

|

Clinical Trial Type |

Observational Studies Interventional Studies Expanded Access Trials |

|

Region |

Java Bali Sumatra Sulawesi Kalimantan |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Rising Government Support for Clinical Trials

3.1.2. Expansion of Healthcare Infrastructure

3.1.3. Growing Pharmaceutical R&D Investment

3.1.4. Availability of Skilled Workforce

3.2. Market Challenges

3.2.1. Stringent Regulatory Framework (Regulatory Bottlenecks, Licensing Delays)

3.2.2. Competition with Regional CROs

3.2.3. Limited Patient Recruitment Pools

3.3. Opportunities

3.3.1. Collaboration with Global Pharmaceutical Firms

3.3.2. Increased Demand for Decentralized Trials

3.3.3. Investment in Clinical Trial Technology Solutions

3.4. Trends

3.4.1. Integration of AI in Clinical Trial Processes

3.4.2. Use of Electronic Data Capture (EDC) Systems

3.4.3. Increasing Prevalence of Adaptive Trials

3.5. Government Regulations

3.5.1. Ministry of Health Clinical Trial Guidelines

3.5.2. Bioethics and Data Protection Policies

3.5.3. Approval Process for International CROs

3.6. SWOT Analysis (Strengths, Weaknesses, Opportunities, Threats)

3.7. Stakeholder Ecosystem (CROs, Pharma Companies, Regulatory Agencies, Hospitals)

3.8. Porters Five Forces (Threat of New Entrants, Buyer Power, Supplier Power, etc.)

3.9. Competition Ecosystem

4.1. By Service Type (In Value %)

4.1.1. Preclinical Trials

4.1.2. Phase I Trials

4.1.3. Phase II Trials

4.1.4. Phase III Trials

4.1.5. Phase IV Post-Marketing Trials

4.2. By Therapeutic Area (In Value %)

4.2.1. Oncology

4.2.2. Cardiovascular Diseases

4.2.3. Infectious Diseases

4.2.4. Neurology

4.2.5. Immunology

4.3. By End User (In Value %)

4.3.1. Pharmaceutical & Biotechnology Companies

4.3.2. Medical Device Companies

4.3.3. Academic & Research Institutions

4.3.4. Government Organizations

4.4. By Clinical Trial Type (In Value %)

4.4.1. Observational Studies

4.4.2. Interventional Studies

4.4.3. Expanded Access Trials

4.5. By Region (In Value %)

4.5.1. Java

4.5.2. Bali

4.5.3. Sumatra

4.5.4. Sulawesi

4.5.5. Kalimantan

5.1 Detailed Profiles of Major Companies

5.1.1. Prodia Clinical Laboratory

5.1.2. PPD (Thermo Fisher Scientific)

5.1.3. ICON Plc

5.1.4. Medpace Holdings Inc.

5.1.5. IQVIA

5.1.6. Labcorp Drug Development

5.1.7. PRA Health Sciences

5.1.8. Syneos Health

5.1.9. KCR CRO

5.1.10. Pharm-Olam

5.1.11. Novotech

5.1.12. Parexel International

5.1.13. Covance Inc.

5.1.14. Charles River Laboratories

5.1.15. Worldwide Clinical Trials

5.2 Cross Comparison Parameters (No. of Employees, Headquarters, Global Reach, Revenue, Therapeutic Specialties, Clinical Trial Success Rate, Regulatory Expertise, Operational Efficiency)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Clinical Trial Standards and Guidelines (Ethical Standards, GCP, ICH Guidelines)

6.2. Compliance Requirements (Data Privacy, Patient Consent)

6.3. Certification Processes

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Service Type (In Value %)

8.2. By Therapeutic Area (In Value %)

8.3. By End User (In Value %)

8.4. By Clinical Trial Type (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

In the initial phase, we create an ecosystem map of the major stakeholders in the Indonesia CRO market. This is supported by desk research and proprietary databases that provide in-depth market insights. The goal is to identify the variables influencing the market, such as regulatory policies and clinical trial trends.

Historical market data is collected and analyzed, including CRO penetration rates, services offered, and revenue figures. This analysis helps construct a reliable foundation to estimate the market size and performance.

We validate market hypotheses through interviews with industry experts and stakeholders, providing us with critical financial and operational insights. These consultations are instrumental in refining our data and analysis.

The final phase involves compiling insights from both the top-down and bottom-up approaches to deliver a comprehensive report on the Indonesia CRO market, ensuring accuracy and thoroughness in the data presented.

The Indonesia CRO market is valued at USD 1.2 billion, driven by an expanding pharmaceutical sector and increasing clinical trial activities in the country.

Challenges in the Indonesia CRO market include navigating Indonesias complex regulatory landscape, limited patient recruitment pools, and competition from regional CROs.

Key players in the Indonesia CRO market include ICON Plc, IQVIA, Parexel International, Prodia Clinical Laboratory, and Medpace Holdings Inc.

The Indonesia CRO market is propelled by increasing R&D investments from pharmaceutical companies, government support for clinical trials, and the expansion of Indonesias healthcare infrastructure.

Technological advancements such as AI in clinical trial processes and electronic data capture (EDC) systems are driving efficiency and accuracy, making Indonesia a favorable market for clinical trials in the Indonesia CRO market.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.