KSA Engineering Plastics Market Outlook to 2030

Region:Middle East

Author(s):Shambhavi

Product Code:KROD2800

November 2024

90

About the Report

KSA Engineering Plastics Market Overview

- The KSA Engineering Plastics market, valued at USD 1.3 billion, is driven by its widespread application in key sectors such as automotive, construction, and electronics. As industries within Saudi Arabia seek to enhance operational efficiency and sustainability, the demand for high-performance, lightweight, and durable materials is increasing. Engineering plastics, known for their superior thermal and chemical properties compared to conventional plastics, are becoming a preferred material for manufacturing and industrial applications, which is further supported by the kingdoms growing industrial base.

- Dominant cities within the KSA market include Riyadh, Jeddah, and Dammam, which are home to a significant number of large-scale industrial and manufacturing plants. These cities lead in automotive production, electronics manufacturing, and infrastructural projects, key sectors that utilize engineering plastics extensively. Riyadh's dominance stems from its status as the capital and its proximity to significant construction projects, while Jeddah and Dammam thrive due to their coastal positioning, giving them logistical advantages for import-export activities.

- Saudi Arabias environmental regulations are becoming stricter, with new standards focusing on plastic waste management. The National Environmental Strategy mandates that all companies must recycle a minimum of 30% of their plastic waste by 2024. This shift is compelling industries to adopt more sustainable practices, including the use of recyclable engineering plastics. The Saudi Environmental Agency has also introduced penalties for companies that fail to meet these recycling targets, further driving the market towards eco-friendly products.

KSA Engineering Plastics Market Segmentation

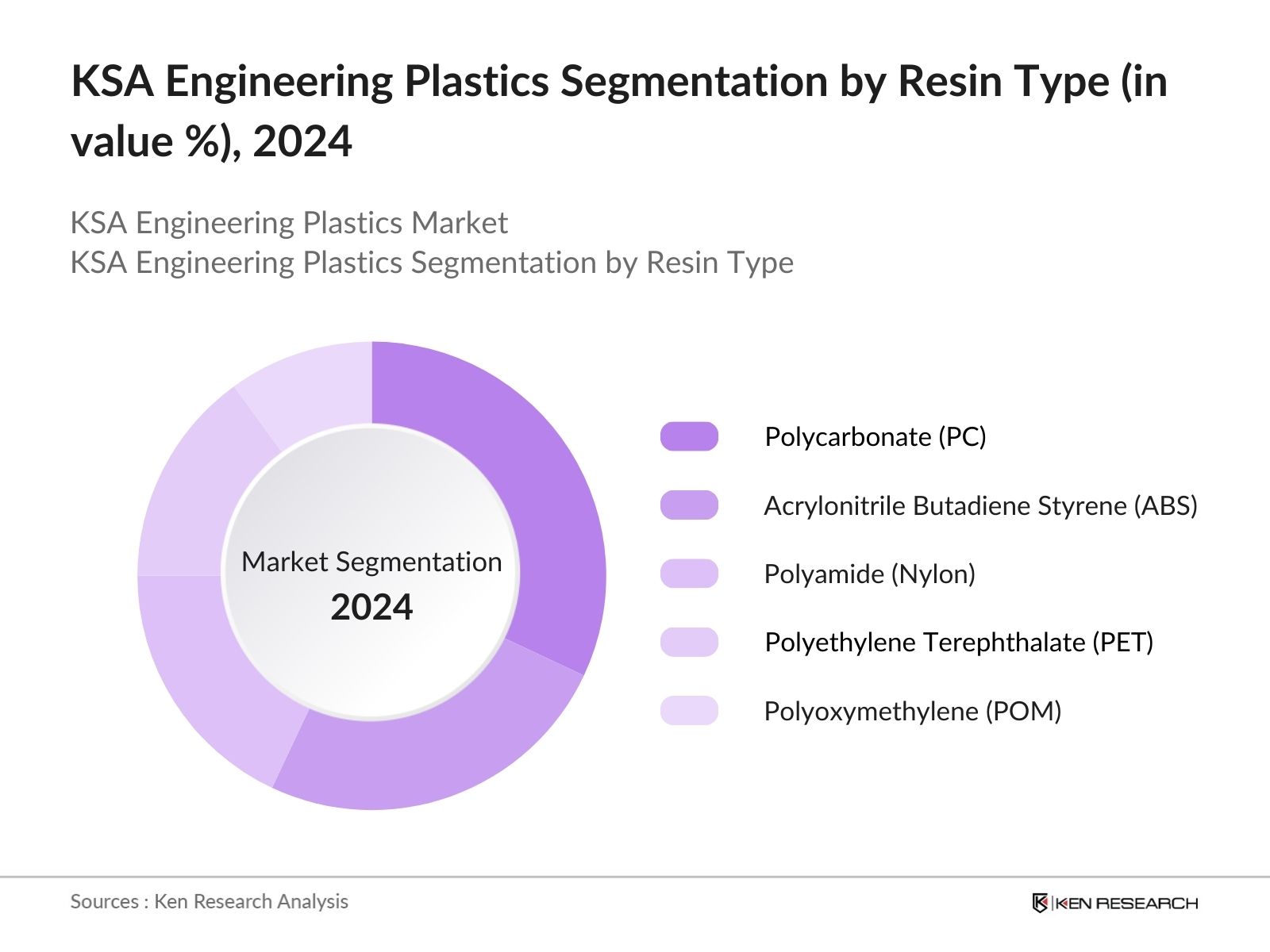

- By Resin Type: The KSA Engineering Plastics market is segmented by resin type into polycarbonate (PC), acrylonitrile butadiene styrene (ABS), polyamide (Nylon), polyethylene terephthalate (PET), and polyoxymethylene (POM). Recently, polycarbonate (PC) has shown dominance in the resin type segmentation, attributed to its usage in automotive and electronics industries where transparency, impact resistance, and heat resistance are essential. Its demand is also heightened by its use in high-strength products like optical discs, eyewear lenses, and bulletproof glass, making it a crucial material in the KSA market.

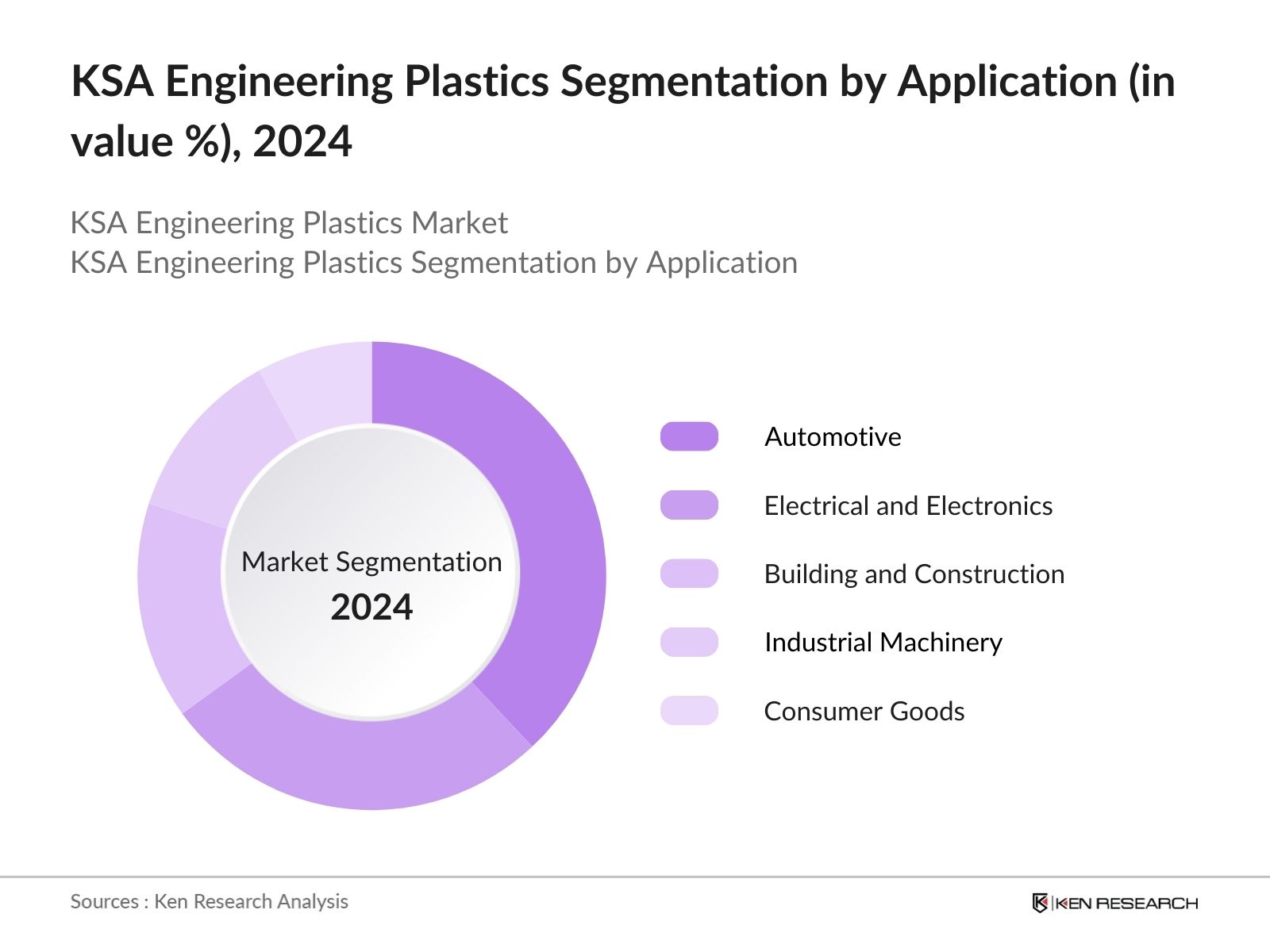

- By Application: The KSA Engineering Plastics market is segmented by application into automotive, electrical and electronics, building and construction, industrial machinery, and consumer goods. Automotive dominates the application segment due to the increasing adoption of lightweight materials for vehicle components. Engineering plastics in the automotive industry enhance fuel efficiency by reducing vehicle weight, and the push for energy-efficient solutions further propels this demand. Additionally, the materials durability and heat resistance make it ideal for under-the-hood applications in cars, leading to its significant market share.

KSA Engineering Plastics Market Competitive Landscape

The KSA Engineering Plastics market is dominated by a few key players with extensive global operations. These companies not only hold significant market shares but also possess strong research and development (R&D) capabilities that contribute to innovation in product development and applications. Key players are heavily investing in expanding their production capacities to meet the growing demand for engineering plastics across different sectors, including automotive, construction, and electronics.

|

Company |

Established Year |

Headquarters |

Global Reach |

R&D Spending |

Innovation Index |

Manufacturing Capabilities |

Environmental Sustainability Initiatives |

Supply Chain Integration |

|

SABIC |

1976 |

Riyadh, Saudi Arabia |

||||||

|

BASF SE |

1865 |

Ludwigshafen, Germany |

||||||

|

Covestro AG |

2015 |

Leverkusen, Germany |

||||||

|

DuPont de Nemours, Inc. |

1802 |

Wilmington, USA |

||||||

|

Mitsubishi Chemical Corp. |

1933 |

Tokyo, Japan |

Growth Drivers

- Industrial Expansion: The rapid industrial expansion in Saudi Arabia, particularly in automotive and construction sectors, is driving the demand for engineering plastics. As of 2024, Saudi Arabia's automotive production has increased to 28,000 vehicles annually, fueled by local initiatives to boost domestic manufacturing. Engineering plastics like polycarbonate and ABS are essential for high-performance, lightweight parts in vehicles and construction materials. According to the World Bank, Saudi Arabia's industrial sector contributed over $200 billion to the economy in 2023, signifying a surge in manufacturing demand that enhances the use of specialized materials like engineering plastics.

- Saudi Vision 2030: Saudi Vision 2030 is fostering industrial diversification by promoting localization in various sectors, including petrochemicals, which are crucial for engineering plastics production. The policy's aim to raise non-oil exports to 50% by 2030 is pushing local industries to produce more specialized plastics. In 2023, the non-oil industrial GDP contribution reached $138 billion, according to the IMF, underscoring the program's success in diversifying the economy and driving demand for high-performance plastics in automotive, aerospace, and electronics sectors.

- Rise in Renewable Energy Projects: The growing number of renewable energy projects in Saudi Arabia is increasing the use of engineering plastics in solar and wind energy equipment. The country aims to generate 27 gigawatts of renewable energy by 2024, with $7 billion allocated to solar projects. Engineering plastics such as polyetheretherketone (PEEK) are extensively used in solar panels and wind turbines due to their durability and heat resistance. As these projects scale, the demand for specialized materials will increase. The Ministry of Energy estimates that renewables will form 30% of the countrys energy mix by 2025.

Market Challenges

- High Production Costs (Raw Material Prices): One of the main challenges in the KSA engineering plastics market is the high cost of raw materials. The global oil price volatility has led to fluctuations in the price of petrochemicals, which are critical inputs for producing engineering plastics. The reliance on imported raw materials also adds to production costs, making local manufacturing less competitive compared to other markets.

- Environmental Regulations (Plastic Waste and Recycling Standards): The Kingdoms new environmental regulations, aimed at reducing plastic waste, present a challenge for the engineering plastics sector. As per Saudi Arabia's 2024 National Environmental Strategy, stringent recycling and waste management policies are in place, requiring industries to adhere to new standards. This adds to operational costs for manufacturers as they must integrate eco-friendly processes into their production lines.

KSA Engineering Plastics Future Market Outlook

Over the next five years, the KSA Engineering Plastics market is poised for considerable growth. This is driven by the government's continued support of local manufacturing, along with the diversification of industries in line with the Vision 2030 strategy. Advancements in technology, such as 3D printing and bioplastics, will further drive demand for engineering plastics in key sectors such as automotive, aerospace, and electronics. Additionally, increasing consumer awareness around sustainability is likely to fuel innovation in recyclable and eco-friendly plastics, leading to further market expansion.

Opportunities

- Government Initiatives (Encouragement of Local Manufacturing): Government initiatives aimed at boosting local manufacturing present significant opportunities for the engineering plastics market. Programs under Saudi Vision 2030, like the National Industrial Development and Logistics Program (NIDLP), focus on enhancing the domestic production of advanced materials, including engineering plastics. This financial backing is expected to increase local production and reduce reliance on imports, creating new growth avenues for the domestic engineering plastics industry.

- Technological Advancements (Development of Bio-based Engineering Plastics): With the global push towards sustainability, there is an opportunity for the development of bio-based engineering plastics in Saudi Arabia. The global market for bio-based plastics reached 2.11 million tons in 2023, and Saudi Arabia is looking to tap into this trend by investing in research and development. In 2023, the Saudi government announced plans to invest $1.5 billion in green technologies, including bio-based plastics, to meet environmental goals under Vision 2030. This shift toward eco-friendly products could provide a competitive edge for local manufacturers.

Scope of the Report

|

Segment |

Sub-Segments |

|

Resin Type |

Polycarbonate (PC) |

|

Acrylonitrile Butadiene Styrene (ABS) |

|

|

Polyamide (Nylon) |

|

|

Polyethylene Terephthalate (PET) |

|

|

Polyoxymethylene (POM) |

|

|

Application |

Automotive |

|

Electrical and Electronics |

|

|

Building and Construction |

|

|

Industrial Machinery |

|

|

Consumer Goods |

Products

Key Target Audience

Automotive Manufacturers

Electronics and Electrical Equipment Producers

Construction Companies

Industrial Machinery Manufacturers

Consumer Goods Manufacturers

Government and Regulatory Bodies (Ministry of Industry and Mineral Resources, Saudi Standards, Metrology and Quality Organization)

Investors and Venture Capitalist Firms

Raw Material Suppliers and Distributors

Companies

Players Mentioned in the report

SABIC

BASF SE

DuPont de Nemours, Inc.

Covestro AG

Mitsubishi Chemical Corporation

Arkema S.A.

Lanxess AG

Celanese Corporation

Solvay S.A.

LG Chem Ltd.

Eastman Chemical Company

RTP Company

Ensinger GmbH

Evonik Industries AG

Asahi Kasei Corporation

Table of Contents

1. KSA Engineering Plastics Market Overview

1.1. Market Size and Growth Drivers

1.2. Dominant Cities and Reasons for Dominance

1.3. Environmental Regulations Impacting the Market

2. KSA Engineering Plastics Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. KSA Engineering Plastics Market Analysis

3.1. Growth Drivers

3.1.1. Industrial Expansion

3.1.2. Saudi Vision 2030 and Economic Diversification

3.1.3. Rise in Renewable Energy Projects

3.2. Market Challenges

3.2.1. High Production Costs (Raw Material Prices)

3.2.2. Environmental Regulations (Plastic Waste and Recycling Standards)

3.3. Opportunities

3.3.1. Government Initiatives (Encouragement of Local Manufacturing)

3.3.2. Technological Advancements (Development of Bio-based Engineering Plastics)

3.4. Trends

3.4.1. Increased Adoption of Recyclable Engineering Plastics

3.4.2. Growing Demand for High-Performance Materials in Automotive and Aerospace

3.4.3. Expansion of Local Manufacturing Facilities

3.5. Government Regulations

3.5.1. Environmental Compliance Standards

3.5.2. Plastic Waste Recycling Mandates

3.5.3. Incentives for Sustainable Material Usage

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porter’s Five Forces Analysis

3.9. Competitive Ecosystem

4. KSA Engineering Plastics Market Segmentation

4.1. By Resin Type (In Value %)

4.1.1. Polycarbonate (PC)

4.1.2. Acrylonitrile Butadiene Styrene (ABS)

4.1.3. Polyamide (Nylon)

4.1.4. Polyethylene Terephthalate (PET)

4.1.5. Polyoxymethylene (POM)

4.2. By Application (In Value %)

4.2.1. Automotive

4.2.2. Electrical and Electronics

4.2.3. Building and Construction

4.2.4. Industrial Machinery

4.2.5. Consumer Goods

5. KSA Engineering Plastics Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. SABIC

5.1.2. BASF SE

5.1.3. Covestro AG

5.1.4. DuPont de Nemours, Inc.

5.1.5. Mitsubishi Chemical Corporation

5.2. Cross Comparison Parameters (Global Reach, R&D Spending, Innovation Index, Manufacturing Capabilities, Environmental Sustainability Initiatives, Supply Chain Integration)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Incentives and Grants

5.9. Private Equity Investments

6. KSA Engineering Plastics Market Regulatory Framework

6.1. Environmental Compliance Standards

6.2. Plastic Waste and Recycling Mandates

6.3. Certification and Accreditation Processes

6.4. Government Incentives for Sustainable Plastics

7. KSA Engineering Plastics Market Future Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Growth

8. KSA Engineering Plastics Future Market Segmentation

8.1. By Resin Type

8.2. By Application

9. KSA Engineering Plastics Market Analysts’ Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Target Audience Profiling

9.3. Competitive Landscape Analysis

9.4. Marketing and Go-To-Market Strategies

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The first step in this research involved mapping out all key stakeholders in the KSA Engineering Plastics market. This was achieved through comprehensive desk research using both secondary and proprietary sources to capture all relevant industry dynamics. The goal was to identify critical factors driving and shaping the market.

Step 2: Market Analysis and Construction

In this phase, historical data related to market performance, major applications, and resin types were gathered and analyzed. This helped identify patterns in consumption and growth drivers, along with emerging opportunities in local manufacturing and export potential.

Step 3: Hypothesis Validation and Expert Consultation

Key industry hypotheses were validated through interviews with professionals from leading companies in the engineering plastics industry. These consultations provided insights into operational challenges, financial forecasts, and the competitive landscape.

Step 4: Research Synthesis and Final Output

In the final stage, the gathered data was synthesized into a comprehensive analysis, incorporating both top-down and bottom-up approaches. The final output was verified through direct engagement with engineering plastics manufacturers, ensuring accuracy and completeness.

Frequently Asked Questions

01. How big is the KSA Engineering Plastics Market?

The KSA Engineering Plastics market is valued at USD 1.3 billion, driven by increasing demand from key sectors like automotive, electronics, and construction.

02. What are the challenges in the KSA Engineering Plastics Market?

Challenges include high production costs due to fluctuating raw material prices and stringent environmental regulations aimed at controlling plastic waste.

03. Who are the major players in the KSA Engineering Plastics Market?

Key players include SABIC, BASF SE, DuPont de Nemours, Covestro AG, and Mitsubishi Chemical Corporation. These companies dominate due to their advanced R&D capabilities and extensive manufacturing presence.

04. What are the growth drivers of the KSA Engineering Plastics Market?

The market is driven by increasing demand from the automotive and construction sectors, the push for lightweight and durable materials, and government initiatives under Saudi Vision 2030.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.