Middle East & Africa Architectural Flat Glass Market Outlook to 2030

Region:Middle East

Author(s):Abhinav kumar

Product Code:KROD5159

December 2024

98

About the Report

Middle East & Africa Architectural Flat Glass Market Overview

- The Middle East & Africa Architectural Flat Glass market has been experiencing steady growth, primarily driven by the region's increasing construction activities, both in residential and commercial sectors. , based on a five-year historical analysis. The growth of this market is fueled by rapid urbanization, a surge in infrastructure projects, and rising demand for energy-efficient buildings. These factors, along with government-led initiatives promoting sustainable construction, have significantly bolstered the demand for architectural flat glass across the region.

- The dominance of countries such as the United Arab Emirates, Saudi Arabia, and Egypt is particularly notable due to their ambitious construction projects, including smart cities and luxury real estate developments. The UAE and Saudi Arabia lead the market, driven by large-scale government projects like Neom and Expo 2020, which require advanced glass technologies for energy efficiency and aesthetics. Egypt, meanwhile, is also witnessing significant growth due to infrastructure projects like the New Administrative Capital.

- Smart city initiatives across the Middle East, particularly in countries like the UAE and Saudi Arabia, offer a promising opportunity for the flat glass market. Neom, Saudi Arabia’s $500 billion megacity project, is a prime example, where smart glass technologies are being integrated into building designs to enhance energy efficiency and user comfort. Smart glass, which can adjust its transparency based on environmental conditions, is becoming increasingly popular in smart cities to reduce cooling costs. The UAE alone is investing billions in similar projects, further driving demand for advanced architectural flat glass.

Middle East & Africa Architectural Flat Glass Market Segmentation

By Product Type: The Middle East & Africa Architectural Flat Glass market is segmented by product type into Low-Emissivity (Low-E) Glass, Solar Control Glass, Laminated Glass, Toughened/Safety Glass, and Insulated Glazing Units (IGUs). Low-E glass dominates this segment due to its superior thermal insulation properties, making it ideal for the region's hot climate. The glass is widely used in both residential and commercial buildings to minimize energy consumption by reducing heat transfer. The demand for Low-E glass is further boosted by government regulations encouraging the use of energy-efficient building materials in line with sustainability goals.

By Application: The market is also segmented by application into Residential Buildings, Commercial Buildings, Industrial Facilities, and Infrastructure Projects. Commercial buildings dominate the market in terms of application, accounting for the largest share due to the region's growing commercial real estate sector. Countries like the UAE and Saudi Arabia are home to high-profile skyscrapers and office buildings, where the demand for aesthetic, durable, and energy-efficient glass is paramount. This segment benefits from the rise in large-scale commercial complexes and luxury hotels in urban areas.

Middle East & Africa Architectural Flat Glass Market Competitive Landscape

The Middle East & Africa Architectural Flat Glass market is dominated by both regional and international players, with significant consolidation observed in the market. Leading companies include AGC Inc., Saint-Gobain, and Guardian Industries, among others. These companies have established strong positions through strategic partnerships, continuous product innovations, and a focus on sustainability. The market is characterized by ongoing investments in R&D to develop sustainable glass products. Key players also focus on enhancing production capacity to meet the rising demand from the construction sector. Additionally, mergers and acquisitions are frequent as companies seek to expand their geographical presence and strengthen their product portfolios.

|

Company |

Establishment Year |

Headquarters |

Product Range |

Revenue |

Market Presence |

R&D Investments |

Production Capacity |

Technological Innovations |

|

AGC Inc. |

1907 |

Japan |

_ |

_ |

_ |

_ |

_ |

_ |

|

Saint-Gobain |

1665 |

France |

_ |

_ |

_ |

_ |

_ |

_ |

|

Guardian Industries |

1932 |

USA |

_ |

_ |

_ |

_ |

_ |

_ |

|

Sisecam Group |

1935 |

Turkey |

_ |

_ |

_ |

_ |

_ |

_ |

|

Emirates Glass LLC |

1998 |

UAE |

_ |

_ |

_ |

_ |

_ |

_ |

Middle East & Africa Architectural Flat Glass Industry Analysis

Growth Drivers

- Urbanization: Urbanization continues to accelerate across the Middle East and Africa, with the World Bank estimating that by 2024, over 60% of the population in the Middle East will be living in urban areas. This rapid urban growth is driving the demand for new infrastructure, including residential and commercial buildings, which in turn fuels the need for architectural flat glass. Major cities such as Cairo, Lagos, and Johannesburg are seeing significant urban infrastructure expansion, contributing to increased demand for flat glass for windows, facades, and other applications in modern constructions.

- Industrialization: Industrialization efforts in the region are amplifying the demand for sustainable building materials, including architectural flat glass. The IMF reports that several African and Middle Eastern nations are actively promoting local industries to boost economic growth, with construction being a key sector. Flat glass, used in sustainable building designs, supports the region's green building initiatives, and the rising adoption of energy-efficient glass is crucial for new industrial buildings. The UAE, for example, is rapidly expanding its industrial base, adding over 1,000 new factories since 2020. Source

- Government Regulations: Energy efficiency mandates and green building regulations are critical growth drivers for the flat glass market. Governments in the region are prioritizing energy-efficient buildings, with Saudi Arabia's Vision 2030 and the UAE's Green Building Regulations mandating the use of low-emissivity glass to reduce energy consumption. The International Energy Agency highlights that buildings account for nearly 40% of global energy consumption, prompting regional authorities to enforce stricter standards for construction materials. By 2024, the GCC's energy conservation measures are expected to have influenced most new constructions, boosting demand for energy-efficient architectural glass. Source

Market Challenges

- Fluctuating Raw Material Costs: The volatility of raw material costs poses significant challenges to flat glass manufacturers in the region. Key raw materials like soda ash and silica sand have seen price fluctuations due to supply disruptions and increased transportation costs. The World Bank’s commodity price data shows that from 2022 to 2023, soda ash prices have risen by over 30%, creating pressure on manufacturers' profit margins, especially as price increases cannot always be passed on to customers due to competitive market conditions.

- Energy-Intensive Manufacturing (Cost Implications, Environmental Impact) Manufacturing flat glass is highly energy-intensive, contributing to higher production costs and environmental concerns. The World Bank indicates that energy costs in the Middle East, while relatively low due to oil and gas availability, are still a significant cost factor for glass manufacturers. Moreover, countries like Egypt and South Africa are under increasing pressure to reduce their carbon emissions. The push towards more energy-efficient processes will require substantial investments, impacting profitability for glass producers.

Middle East & Africa Architectural Flat Glass Market Future Outlook

Over the next few years, the Middle East & Africa Architectural Flat Glass market is expected to witness significant growth, driven by continuous advancements in glass technology, government regulations promoting green building standards, and increased investments in infrastructure development. Major growth will be concentrated in the GCC countries, where construction of smart cities and high-rise buildings is rapidly accelerating. The increasing adoption of energy-efficient glass products, such as Low-E and solar control glass, will further contribute to the market’s growth trajectory.

Opportunities

- Growth in Smart Cities Projects: Smart city initiatives across the Middle East, particularly in countries like the UAE and Saudi Arabia, offer a promising opportunity for the flat glass market. Neom, Saudi Arabia’s $500 billion megacity project, is a prime example, where smart glass technologies are being integrated into building designs to enhance energy efficiency and user comfort. Smart glass, which can adjust its transparency based on environmental conditions, is becoming increasingly popular in smart cities to reduce cooling costs. The UAE alone is investing billions in similar projects, further driving demand for advanced architectural flat glass.

- Rising Demand for Energy-Efficient Buildings: As part of global efforts to reduce energy consumption, the demand for energy-efficient buildings is rising, especially in regions with extreme climates like the Middle East and Africa. Low-emissivity (Low-E) glass, which minimizes the amount of infrared and ultraviolet light passing through without compromising visible light, is seeing higher demand. The International Energy Agency reports that solar control glass can reduce cooling costs by 20%, making it an attractive option for both residential and commercial buildings in these hot regions.

Scope of the Report

|

Product Type |

Low-Emissivity (Low-E) Glass Solar Control Glass Laminated Glass Toughened/Safety Glass Insulated Glazing Units (IGUs) |

|

Application |

Residential Buildings Commercial Buildings Industrial Facilities Infrastructure Projects |

|

Technology |

Float Glass Process Rolled Glass Process Coating Technologies Laminating Technologies |

|

Thickness |

Below 6mm 6mm 12mm Above 12mm |

|

Region |

GCC Countries North Africa Sub-Saharan Africa Levant |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Architectural Companies

Construction Companies

Real Estate Development Industries

Investors and Venture Capitalist Firms

Glass Manufacturing Companies

Government and Regulatory Bodies (e.g., Saudi Energy Efficiency Center, UAE Ministry of Climate Change and Environment)

Contractor and Builder Companies

Companies

Players Mentioned in the Report

AGC Inc.

Saint-Gobain S.A.

Guardian Industries

Sisecam Group

Emirates Glass LLC

Qatar Glass Industry

PFG Building Glass

Pilkington (NSG Group)

Zamil Glass Industries

BDL Gulf Glass

Table of Contents

1. Middle East & Africa Architectural Flat Glass Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

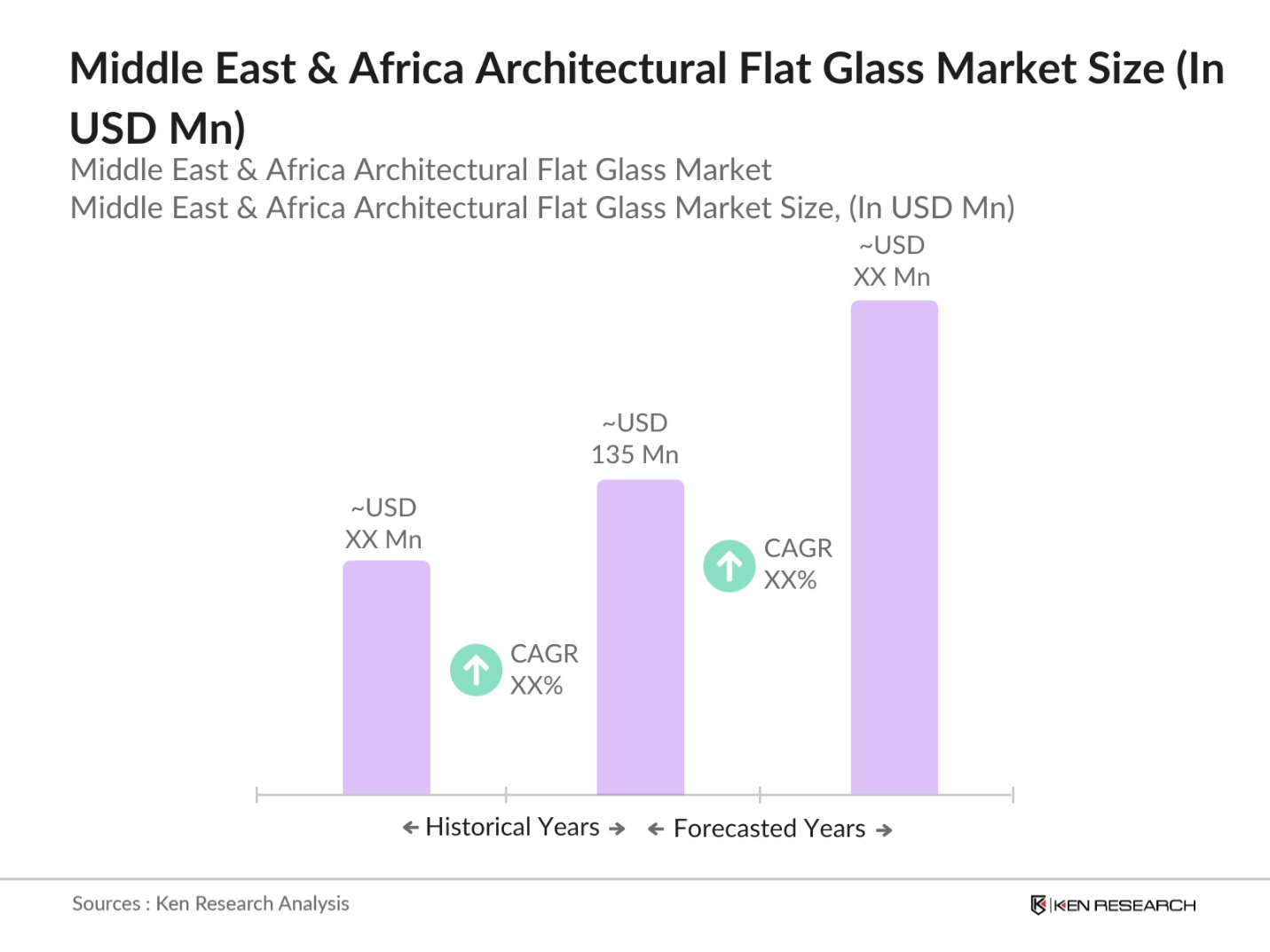

2. Middle East & Africa Architectural Flat Glass Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Middle East & Africa Architectural Flat Glass Market Analysis

3.1. Growth Drivers

3.1.1. Rise in Urbanization

3.1.2. Construction Industry Growth

3.1.3. Government Regulations and Building Codes

3.1.4. Demand for Energy-Efficient Glass Products

3.2. Market Challenges

3.2.1. High Raw Material Costs

3.2.2. Intense Price Competition

3.2.3. Regulatory and Certification Hurdles

3.3. Opportunities

3.3.1. Growth in Eco-friendly and Energy-efficient Glass Solutions

3.3.2. Increasing Demand for Smart Glass

3.3.3. Expansion of Sustainable Construction

3.4. Trends

3.4.1. Shift Towards High-performance Architectural Glass

3.4.2. Growing Popularity of Glass Facades

3.4.3. Integration of Glass with Smart Technology

3.5. Government Regulation

3.5.1. Energy-efficient Building Code Regulations

3.5.2. Environmental Impact of Construction Materials

3.5.3. Regulatory Standards for Safety Glass

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porter’s Five Forces Analysis

3.9. Competition Ecosystem

4. Middle East & Africa Architectural Flat Glass Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Clear Glass

4.1.2. Tinted Glass

4.1.3. Low-E Glass

4.1.4. Laminated Glass

4.1.5. Tempered Glass

4.2. By Application (In Value %)

4.2.1. Residential

4.2.2. Commercial

4.2.3. Industrial

4.2.4. Automotive (Windshields, Side Windows)

4.2.5. Others (e.g., Bulletproof Glass)

4.3. By End-User Industry (In Value %)

4.3.1. Construction

4.3.2. Automotive

4.3.3. Aerospace

4.3.4. Furniture and Interiors

4.3.5. Others (Solar, Electronics)

4.4. By Region (In Value %)

4.4.1. Middle East

4.4.2. North Africa

4.4.3. Sub-Saharan Africa

4.4.4. South Africa

4.5. By Glass Properties (In Value %)

4.5.1. Energy-efficient Glass

4.5.2. Safety Glass (Impact-resistant, Laminated)

4.5.3. Insulated Glass

4.5.4. Solar Control Glass

5. Middle East & Africa Architectural Flat Glass Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Saint-Gobain S.A.

5.1.2. Asahi Glass Co. Ltd.

5.1.3. Guardian Industries

5.1.4. NSG Group

5.1.5. Vitro S.A.B. de C.V.

5.1.6. Schott AG

5.1.7. Mitsubishi Chemical Corporation

5.1.8. PPG Industries, Inc.

5.1.9. China National Glass Industrial Group Corporation

5.1.10. Owens Corning

5.1.11. Xinyi Glass Holdings Limited

5.1.12. Fuyao Glass Industry Group Co., Ltd.

5.1.13. Tamglass

5.1.14. Glassolutions

5.1.15. TSI Inc.

5.2. Cross Comparison Parameters

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Government Grants and Subsidies

5.8. Private Equity Investments

6. Middle East & Africa Architectural Flat Glass Market Regulatory Framework

6.1. Building Code Regulations

6.2. Environmental Compliance Requirements

6.3. Glass Product Certification Processes

7. Middle East & Africa Architectural Flat Glass Market Future Market Size (In USD Mn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Middle East & Africa Architectural Flat Glass Market Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By End-User Industry (In Value %)

8.4. By Region (In Value %)

8.5. By Glass Properties (In Value %)

9. Middle East & Africa Architectural Flat Glass Market Analysts’ Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Strategic Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

In the first step, we mapped out all the relevant stakeholders, including construction companies, architects, glass manufacturers, and government bodies within the Middle East & Africa Architectural Flat Glass Market. Our extensive desk research combined with secondary databases allowed us to gather comprehensive market-level data. This was crucial for identifying the critical variables that drive market dynamics, such as energy efficiency regulations and construction trends.

Step 2: Market Analysis and Construction

We compiled historical data on the market, focusing on key segments like product type and application. Through detailed analysis, we assessed market penetration rates and the supply-demand balance, alongside revenue generation from top architectural flat glass manufacturers. This provided a reliable framework for estimating market sizes.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses were validated through consultations with industry professionals, including glass manufacturers and architects. The feedback from these experts, gathered through interviews, was instrumental in verifying the market data, adding qualitative insights that informed our forecasts.

Step 4: Research Synthesis and Final Output

In the final stage, insights gathered from key market players were synthesized to refine our market forecasts. The interaction with leading glass manufacturers provided crucial details on technological innovations and product segment performance. This ensured a holistic, accurate analysis of the Middle East & Africa Architectural Flat Glass Market.

Frequently Asked Questions

01. How big is the Middle East & Africa Architectural Flat Glass Market?

The Middle East & Africa Architectural Flat Glass Market is valued at USD 135 million, driven by increasing urbanization and a surge in residential and commercial construction activities.

02. What are the challenges in the Middle East & Africa Architectural Flat Glass Market?

Key challenges include fluctuating raw material costs, high energy consumption during manufacturing, and the rising competition from alternative building materials like aluminum and composite panels.

03. Who are the major players in the Middle East & Africa Architectural Flat Glass Market?

Major players include AGC Inc., Saint-Gobain, Guardian Industries, Sisecam Group, and Emirates Glass LLC, each of whom has established a strong market presence through strategic investments and product innovations.

04. What are the growth drivers of the Middle East & Africa Architectural Flat Glass Market?

Growth drivers include the regions focus on sustainable construction, government regulations promoting energy efficiency, and a rising demand for luxury and commercial real estate developments.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.