North America Automotive Fasteners Market Outlook to 2030

Region:North America

Author(s):Sanjeev

Product Code:KROD8749

Region:North America

Author(s):Sanjeev

Product Code:KROD8749

November 2024

96

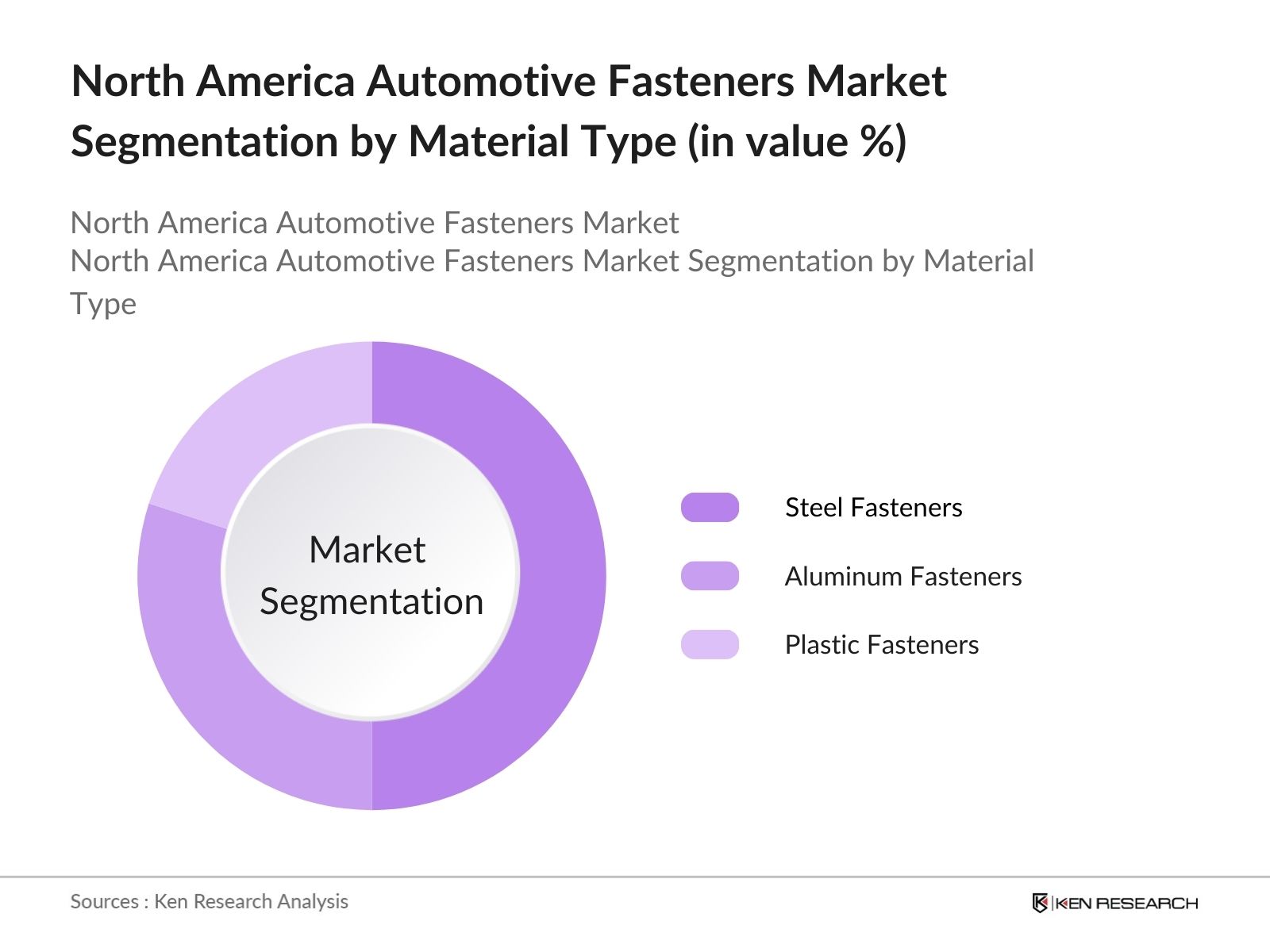

By Material Type: The market is segmented by material type into steel fasteners, aluminum fasteners, and plastic fasteners. Among these, steel fasteners hold the dominant market share due to their durability and wide application across different vehicle components. Despite the rise of lightweight materials, steel remains crucial, especially in heavy-duty automotive applications, which require enhanced strength and reliability. Manufacturers also favor steel fasteners for their cost-effectiveness and long-term performance.

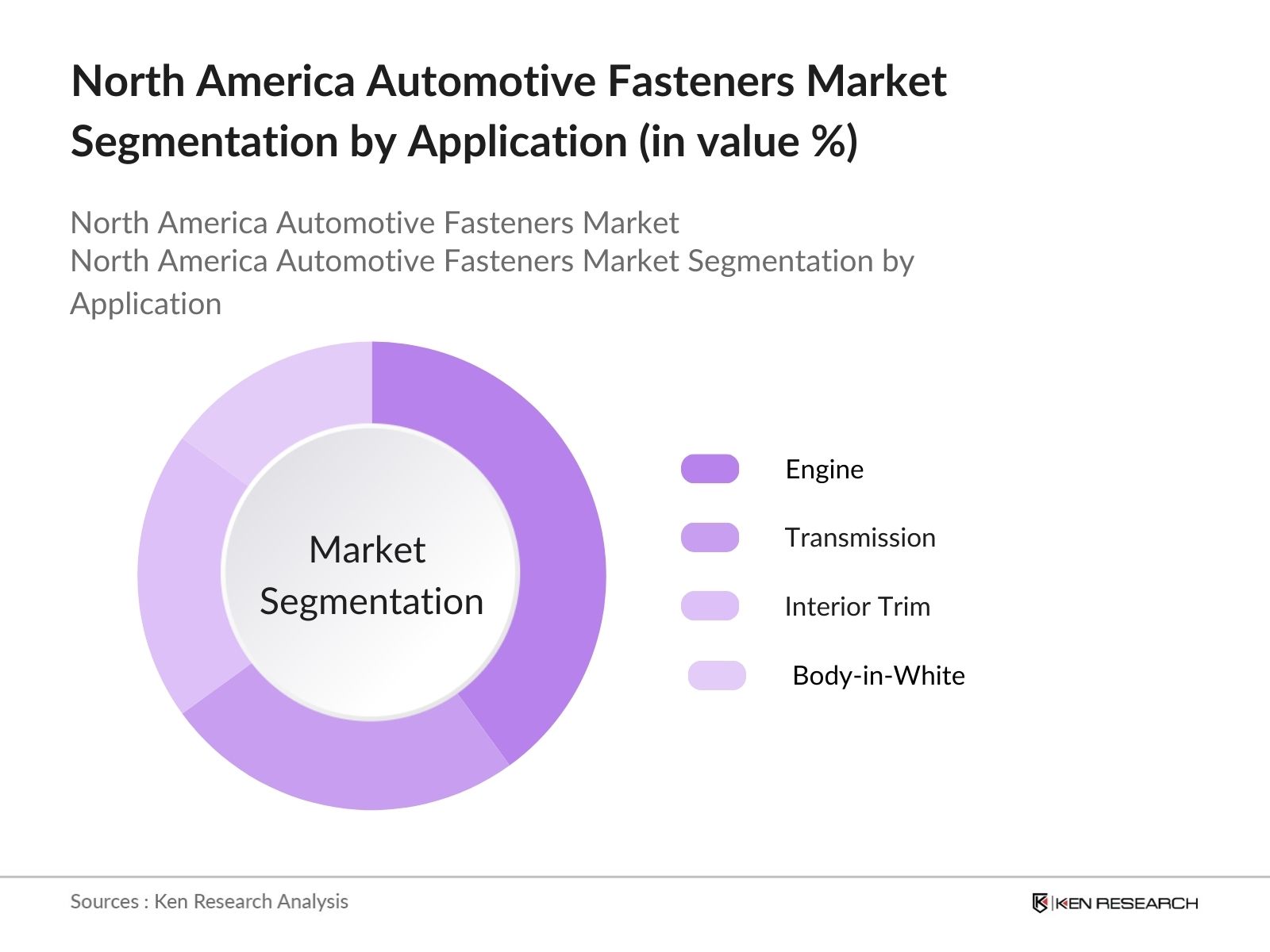

By Application: In terms of application, the market is divided into engine, transmission, interior trim, and body-in-white (BIW). Fasteners for engine applications command the largest share due to the high precision and performance standards required in engine assembly. The need for temperature and corrosion-resistant fasteners makes this segment highly specialized. As vehicle engines become more complex and shift towards hybrid or electric technology, the demand for high-performance fasteners in this segment continues to rise.

The North America Automotive Fasteners market is dominated by key global and regional players who have established a strong foothold due to their innovation, production capabilities, and strategic partnerships with OEMs. This consolidation allows these companies to exert significant influence over market trends and pricing.

|

Company |

Establishment Year |

Headquarters |

Revenue (USD Bn) |

Employees |

No. of Patents |

OEM Partnerships |

Material Expertise |

Sustainability Initiatives |

R&D Investments |

|

Stanley Black & Decker |

1843 |

New Britain, CT, USA |

|||||||

|

Illinois Tool Works |

1912 |

Glenview, IL, USA |

|||||||

|

Lisi Automotive |

1777 |

Grandvillars, France |

|||||||

|

PennEngineering |

1942 |

Danboro, PA, USA |

|||||||

|

Fastenal Company |

1967 |

Winona, MN, USA |

Over the next five years, the North America Automotive Fasteners market is expected to witness steady growth driven by the expansion of electric vehicle (EV) production, technological advancements in fastener materials, and the increasing use of lightweight components in automotive manufacturing. As regulations around emissions tighten, the demand for sustainable and eco-friendly fasteners will rise. Additionally, the aftermarket for automotive repair and customization will continue to contribute to the market's growth trajectory.

|

By Material Type |

Steel Fasteners Aluminum Fasteners Plastic Fasteners |

|

By Application |

Engine Transmission Interior Trim Body-in-White |

|

By End-User |

Passenger Vehicles Light Commercial Vehicles Heavy Commercial Vehicles Electric Vehicles |

|

By Functionality |

Permanent Fasteners Removable Fasteners Semi-permanent Fasteners |

|

By Region |

United States Canada Mexico |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Increasing Automotive Production (Number of vehicles produced)

3.1.2. Shift Towards Lightweight Materials (Usage of aluminum and high-performance plastic fasteners)

3.1.3. Rise in Electric Vehicle Adoption (Fasteners specific to EV architecture)

3.1.4. Stringent Emission Norms (Environmental regulations for vehicle manufacturing)

3.2. Market Challenges

3.2.1. Volatility in Raw Material Prices (Steel, aluminum, plastic costs)

3.2.2. Intense Competition from Local Manufacturers

3.2.3. Complex Supply Chain Management (Lead times and logistic issues)

3.3. Opportunities

3.3.1. Advancements in Fastening Technology (Automated assembly and self-locking fasteners)

3.3.2. Growing Aftermarket Demand for Specialty Fasteners (Performance vehicles and customization)

3.3.3. Expansion into Hybrid and Electric Vehicle Segments

3.4. Trends

3.4.1. Use of Recyclable and Sustainable Fasteners

3.4.2. Development of Smart Fasteners with Sensors

3.4.3. Modular Fastening Systems for Efficient Assembly

3.5. Government Regulations

3.5.1. Automotive Safety Standards (Crashworthiness regulations impacting fastener specifications)

3.5.2. Vehicle Emission Norms

3.5.3. Trade Tariffs and Import/Export Regulations

3.5.4. Standards on Material Composites and Corrosion Resistance

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (Manufacturers, Suppliers, OEMs, Aftermarket)

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

4.1. By Material Type (In Value %) 4.1.1. Steel Fasteners

4.1.2. Aluminum Fasteners

4.1.3. Plastic Fasteners

4.2. By Application (In Value %) 4.2.1. Engine

4.2.2. Transmission

4.2.3. Interior Trim

4.2.4. Body-in-White (BIW)

4.3. By End-User (In Value %) 4.3.1. Passenger Vehicles

4.3.2. Light Commercial Vehicles

4.3.3. Heavy Commercial Vehicles

4.3.4. Electric Vehicles

4.4. By Functionality (In Value %) 4.4.1. Permanent Fasteners

4.4.2. Removable Fasteners

4.4.3. Semi-permanent Fasteners

4.5. By Region (In Value %)

4.5.1. United States

4.5.2. Canada

4.5.3. Mexico

5.1. Detailed Profiles of Major Competitors 5.1.1. Stanley Black & Decker

5.1.2. Illinois Tool Works

5.1.3. Lisi Automotive

5.1.4. Nifco Inc.

5.1.5. Bulten AB

5.1.6. PennEngineering

5.1.7. Bossard Group

5.1.8. Fastenal Company

5.1.9. Wrth Group

5.1.10. KAMAX Group

5.1.11. Acument Global Technologies

5.1.12. Simmonds Marshall Limited

5.1.13. Delo Industrial Adhesives

5.1.14. Boltun Corporation

5.1.15. A Raymond Group

5.2. Cross Comparison Parameters (Market Specific)

Material Innovation

Product Portfolio Diversification

Global Production Footprint

Revenue Share from OEMs vs Aftermarket

Sustainability Initiatives (Eco-friendly materials)

Technology Integration (Smart fasteners)

Manufacturing Capabilities (Automation, robotics integration)

Strategic Partnerships with OEMs

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Automotive Industry Material Standards

6.2. Safety Compliance Regulations

6.3. Environmental Impact Certifications

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Material Type (In Value %)

8.2. By Application (In Value %)

8.3. By End-User (In Value %)

8.4. By Functionality (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsThe initial phase involves constructing an ecosystem map of the North America Automotive Fasteners Market. Extensive desk research and secondary data sources such as industry reports, government databases, and proprietary insights are used to identify critical variables influencing market trends.

Historical data from various industry sources is compiled, focusing on fastener consumption across automotive production and aftermarket sectors. The analysis covers market penetration of different material types and application areas, supported by revenue statistics.

Market hypotheses are tested and validated using expert interviews. These interviews, conducted with key stakeholders from major automotive OEMs and fastener manufacturers, provide real-time insights into market conditions and future trends.

A bottom-up approach is employed to analyze company-specific data and integrate these findings into broader market insights. The final report synthesizes all data points to provide a comprehensive, accurate analysis of the North America Automotive Fasteners Market.

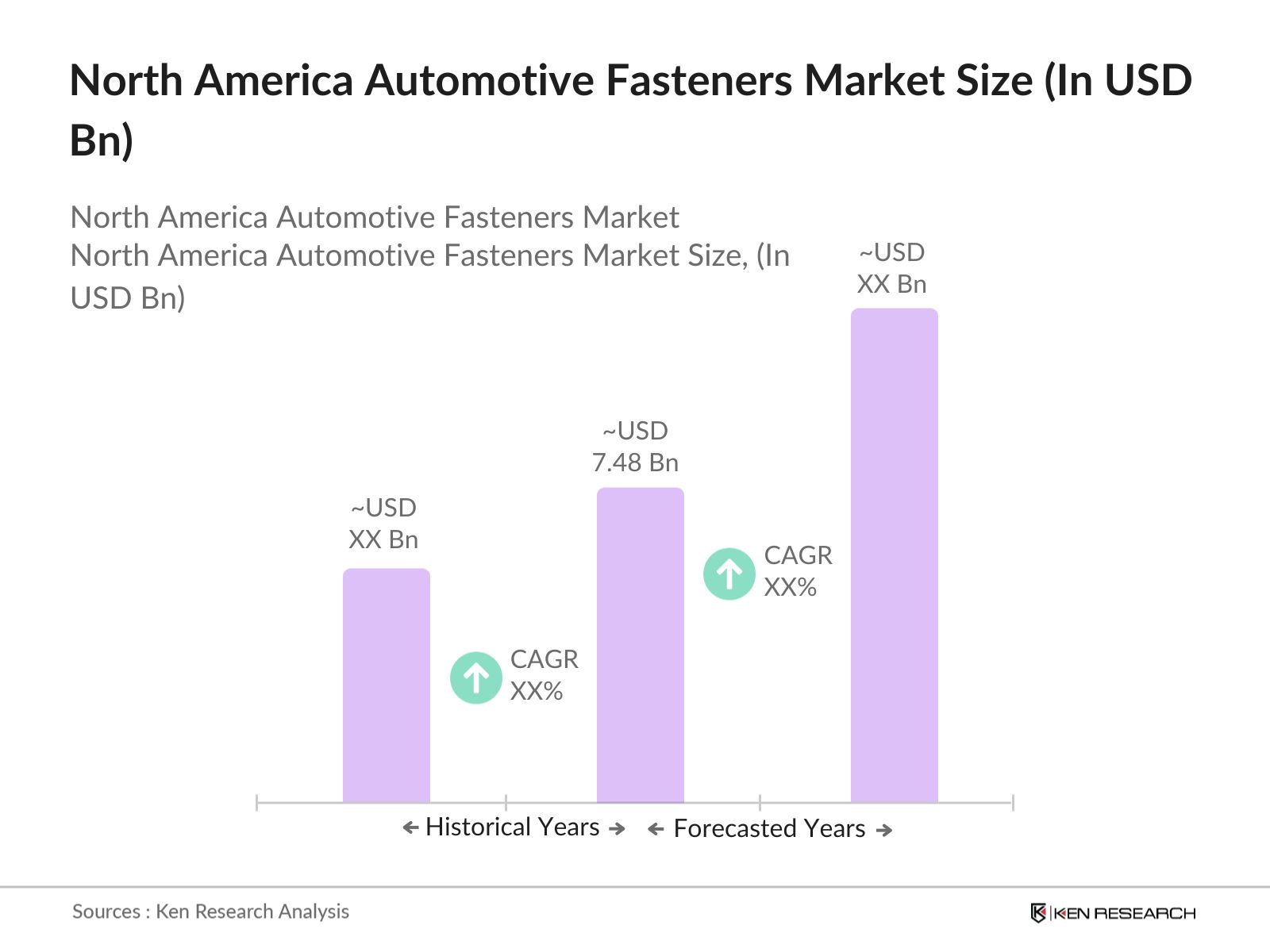

The North America Automotive Fasteners Market was valued at USD 7.48 billion, driven by increasing automotive production and the expansion of electric vehicle manufacturing.

The challenges include fluctuations in raw material prices, intense competition from local manufacturers, and the complexity of supply chain management due to rising demand.

Key players include Stanley Black & Decker, Illinois Tool Works, PennEngineering, Fastenal Company, and Lisi Automotive, who dominate through strong OEM partnerships and innovation.

Key drivers include the rise in electric vehicle adoption, advancements in lightweight materials for fuel efficiency, and the growing demand for durable and high-performance fasteners.

Current trends include the development of smart fasteners with integrated sensors, the use of recyclable materials, and increased automation in fastener manufacturing for efficient vehicle assembly.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.