USA Fuel Cell Vehicle Market Outlook to 2030

Region:North America

Author(s):Hritika sahu

Product Code:KROD4833

December 2024

88

About the Report

USA Fuel Cell Vehicle Market Overview

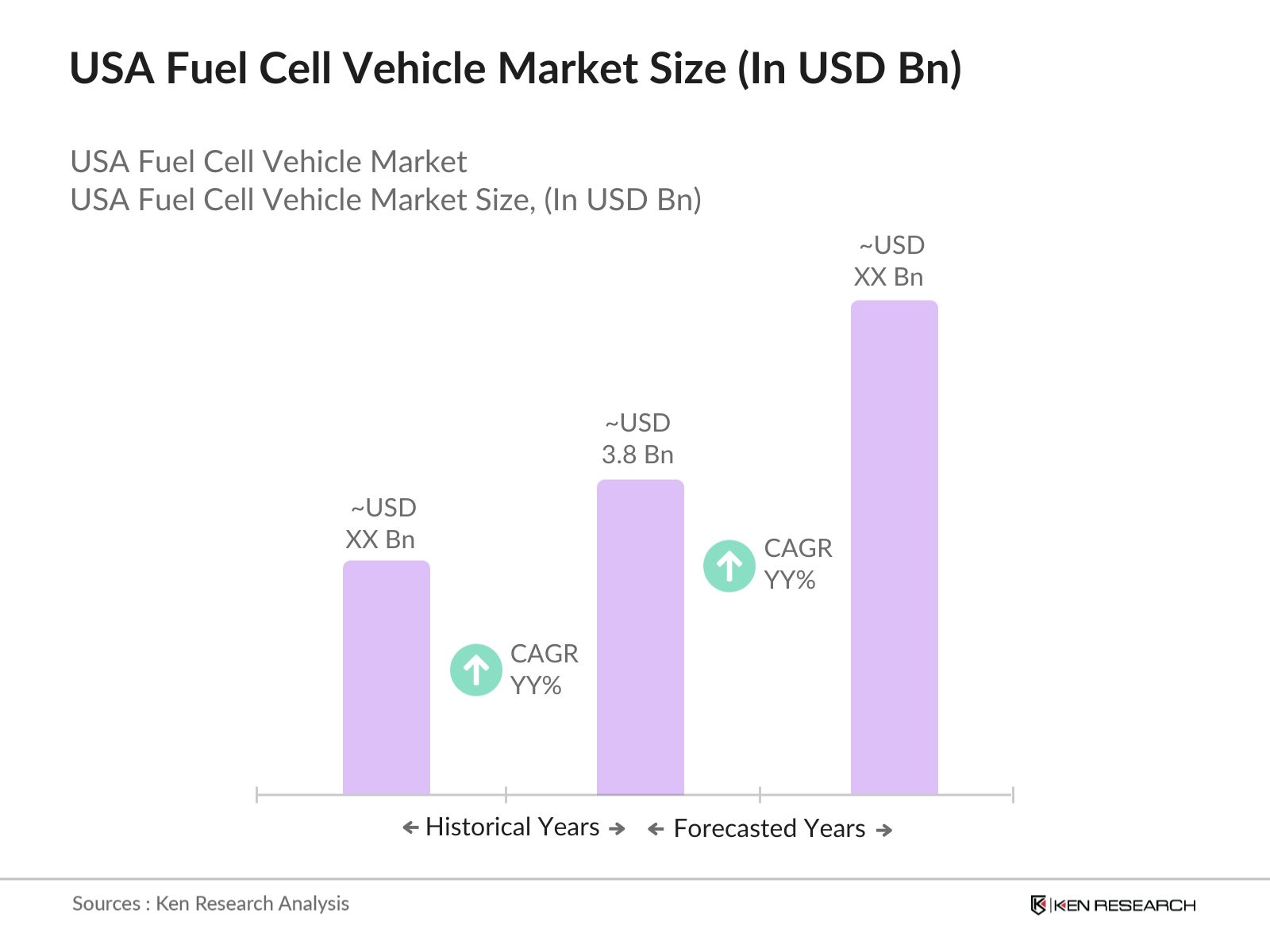

- The USA fuel cell vehicle market is valued at USD 3.8 billion, driven primarily by advancements in fuel cell technology, governmental incentives, and rising consumer demand for zero-emission vehicles. The expansion of hydrogen refueling infrastructure, supported by federal funding, is further enabling the growth of this sector. Innovations by manufacturers to increase vehicle range and efficiency contribute to the markets progression, reflecting the broader automotive industrys shift towards sustainable energy solutions.

- California, Texas, and New York are leading regions in the market due to proactive government policies, established hydrogen infrastructure, and consumer readiness to adopt green technologies. California, in particular, holds a dominant position, benefiting from incentives and a robust network of hydrogen refueling stations, which make it more feasible for consumers to own and operate fuel cell vehicles in the region.

- The Department of Energy's "Hydrogen Shot" initiative, introduced in 2024, aims to reduce hydrogen production costs by 80% to around $1 per kilogram by 2030. This initiative has already received $400 million in federal funding, which is expected to lower the operational costs of fuel cell vehicles in the coming years.

USA Fuel Cell Vehicle Market Segmentation

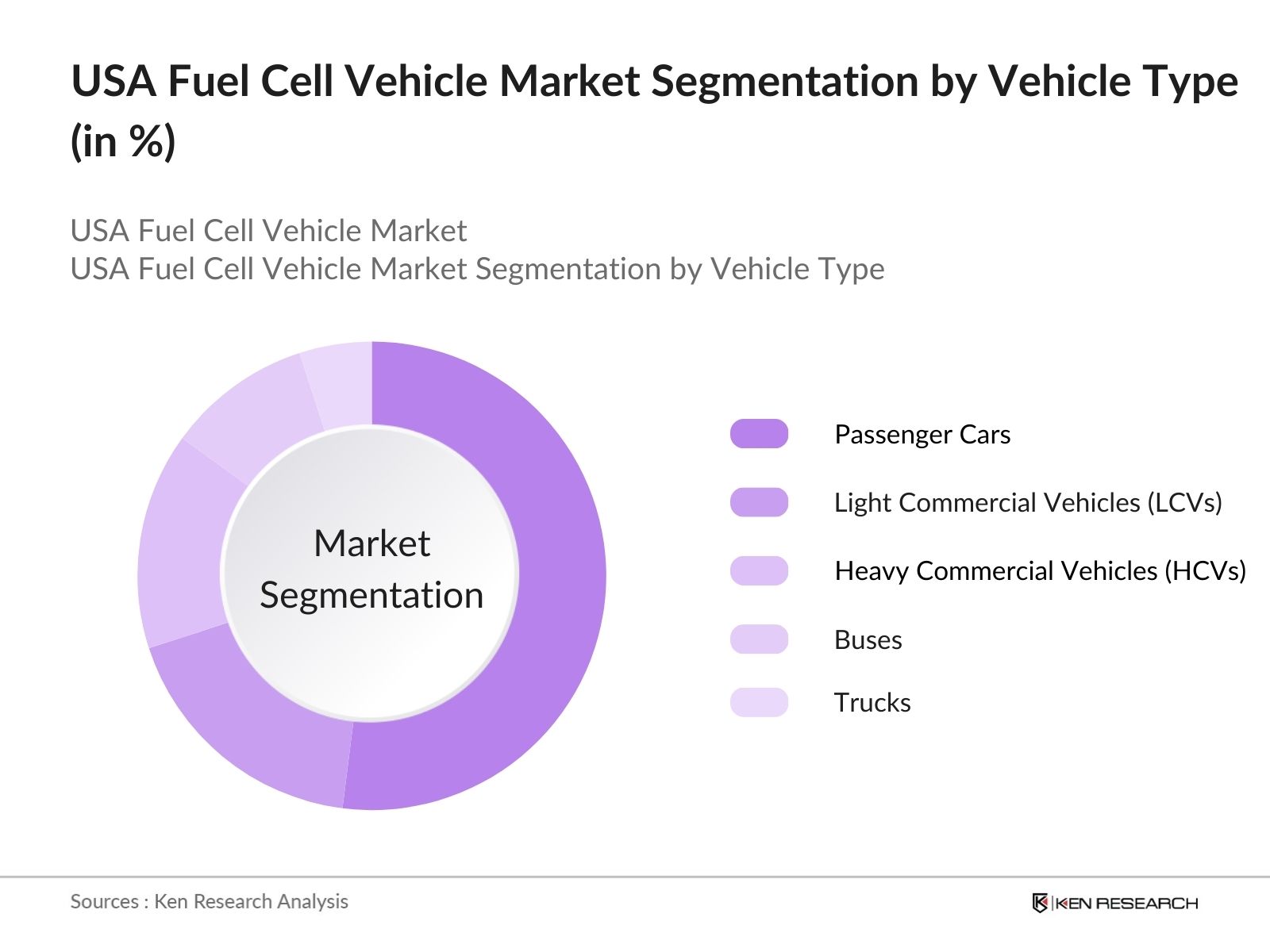

By Vehicle Type: The market is segmented by vehicle type into passenger cars, light commercial vehicles (LCVs), heavy commercial vehicles (HCVs), and buses. Passenger cars currently dominate the vehicle type segment due to high demand among environmentally conscious consumers in urban areas and substantial investments by manufacturers like Toyota and Hyundai. The increasing focus on reducing greenhouse gas emissions in densely populated areas makes passenger cars a prominent choice within this segment.

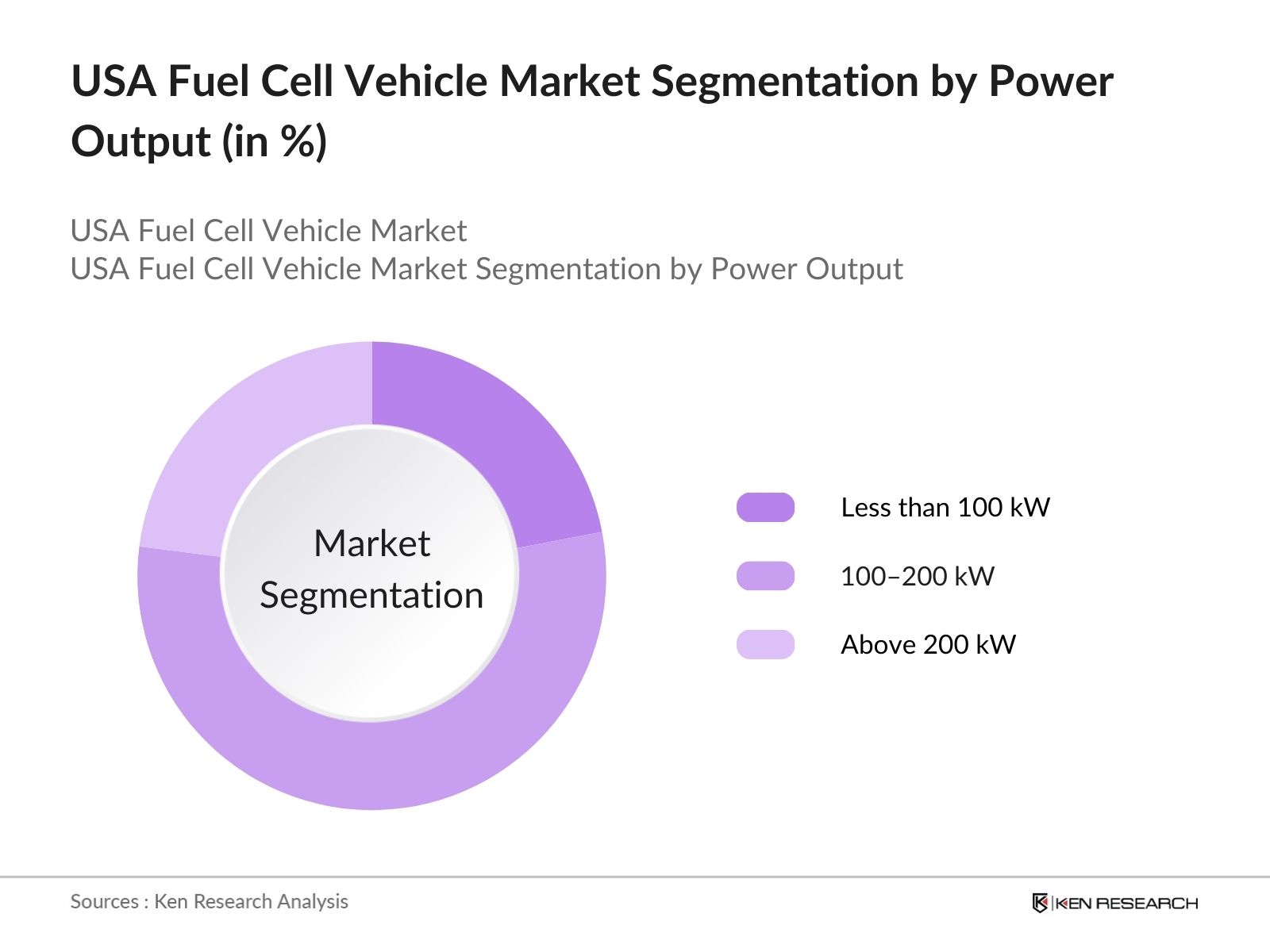

By Power Output: The market is further segmented by power output into less than 100 kW, 100200 kW, and above 200 kW. The 100200 kW segment is leading due to its suitability for mid-range passenger vehicles and light commercial vehicles, meeting consumer demands for vehicles with optimal range and efficiency. This power output range allows manufacturers to balance performance and fuel economy, making it the preferred option among manufacturers and consumers alike.

USA Fuel Cell Vehicle Market Competitive Landscape

The market is dominated by major players who actively contribute to research, innovation, and infrastructure development. Companies like Toyota, Hyundai, and General Motors hold a influence in the market, driven by their substantial investments in fuel cell technology and network expansion.

USA Fuel Cell Vehicle Market Analysis

Market Growth Drivers

- Government Funding for Hydrogen Infrastructure: In 2024, the U.S. Department of Energy allocated $1 billion towards expanding hydrogen refueling infrastructure across major metropolitan areas, aiming to facilitate the adoption of fuel cell vehicles. This funding aligns with the Biden administration's goal of creating a robust hydrogen ecosystem by 2030, directly benefiting fuel cell vehicle accessibility and adoption by establishing 200 new stations nationwide.

- Corporate Fleet Electrification Initiatives: Major companies like Amazon and Walmart have invested in hydrogen fuel cell-powered trucks to meet carbon neutrality goals. In 2024, Amazon committed $500 million towards purchasing over 1,000 fuel cell trucks for its U.S. delivery fleet, expecting to reduce fuel emissions significantly and drive demand for fuel cell vehicle infrastructure and related technology.

- State-Level Incentives Boosting Adoption: California, known for its leadership in clean energy, increased its subsidy budget for zero-emission vehicles by $150 million in 2024, specifically targeting hydrogen fuel cell vehicles. Such incentives are expected to influence other states, making fuel cell vehicles more accessible across the U.S. market.

Market Challenges

- Limited Refueling Infrastructure Nationwide: Despite investments, there are currently only around 100 hydrogen refueling stations in the U.S., with the majority concentrated in California. This limited infrastructure makes cross-country travel and widespread adoption challenging, highlighting the need for substantial infrastructural investment before fuel cell vehicles can become a viable option nationwide.

- Competition from Battery Electric Vehicles (BEVs): As of 2024, the U.S. boasts over 250,000 public EV charging stations, providing BEVs a infrastructural advantage over hydrogen-powered vehicles. With BEV technology becoming more affordable, the market faces stiff competition from this well-established segment, posing a challenge for the fuel cell vehicle sector to differentiate itself.

USA Fuel Cell Vehicle Market Future Outlook

The market is anticipated to witness growth over the next five years. Factors such as continuous government support, the expansion of hydrogen infrastructure, and ongoing technological advancements in fuel cell efficiency are expected to drive market growth.

Future Market Opportunities

- Expansion of Hydrogen Refueling Infrastructure: Over the next five years, the U.S. government is expected to increase hydrogen refueling stations to 500 nationwide, driven by investments under the Infrastructure Investment and Jobs Act. This infrastructure expansion will play a critical role in enabling fuel cell vehicles to become viable alternatives to gasoline and electric options by 2029.

- Cost Reduction in Hydrogen Production: By 2029, advancements in electrolyzer technology and government subsidies are expected to reduce hydrogen production costs to around $3 per kilogram, making fuel cell vehicles more competitive with traditional fuel sources. This cost reduction is anticipated to boost consumer demand and market penetration for fuel cell vehicles.

Scope of the Report

|

Vehicle Type |

Passenger Cars |

|

Power Output |

Less than 100 kW |

|

Electrolyte Type |

Proton Exchange Membrane Fuel Cell (PEMFC) |

|

Application |

Transportation |

|

Region |

Northeast |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Automotive Manufacturers

Fuel Cell Technology Providers

Hydrogen Fueling Infrastructure Developers

Federal and State Government Agencies (e.g., U.S. Department of Energy)

Environmental Regulatory Bodies (e.g., Environmental Protection Agency)

Investor and Venture Capitalist Firms

Public Transportation Authorities

Hydrogen Distribution and Logistics Companies

Companies

Players Mentioned in the Report:

Toyota Motor Corporation

Hyundai Motor Company

Honda Motor Co., Ltd.

General Motors

Nikola Corporation

BMW AG

Ford Motor Company

Stellantis N.V.

Ballard Power Systems

Plug Power Inc.

Table of Contents

1. USA Fuel Cell Vehicle Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. USA Fuel Cell Vehicle Market Size (In USD Million)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. USA Fuel Cell Vehicle Market Analysis

3.1. Growth Drivers

3.1.1. Stringent Emission Regulations

3.1.2. Advancements in Fuel Cell Technology

3.1.3. Government Incentives and Subsidies

3.1.4. Increasing Consumer Awareness

3.2. Market Challenges

3.2.1. High Initial Costs

3.2.2. Limited Hydrogen Refueling Infrastructure

3.2.3. Competition from Battery Electric Vehicles

3.3. Opportunities

3.3.1. Expansion of Hydrogen Infrastructure

3.3.2. Collaborations and Partnerships

3.3.3. Technological Innovations

3.4. Trends

3.4.1. Integration with Renewable Energy Sources

3.4.2. Development of Heavy-Duty Fuel Cell Vehicles

3.4.3. Adoption in Public Transportation

3.5. Government Regulations

3.5.1. Federal Emission Standards

3.5.2. State-Level Incentives

3.5.3. Hydrogen Fueling Infrastructure Policies

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porter’s Five Forces Analysis

4. USA Fuel Cell Vehicle Market Segmentation

4.1. By Vehicle Type (In Value %)

4.1.1. Passenger Cars

4.1.2. Light Commercial Vehicles (LCVs)

4.1.3. Heavy Commercial Vehicles (HCVs)

4.1.4. Buses

4.1.5. Trucks

4.2. By Power Output (In Value %)

4.2.1. Less than 100 kW

4.2.2. 100–200 kW

4.2.3. Above 200 kW

4.3. By Electrolyte Type (In Value %)

4.3.1. Proton Exchange Membrane Fuel Cell (PEMFC)

4.3.2. Phosphoric Acid Fuel Cell (PAFC)

4.4. By Application (In Value %)

4.4.1. Transportation

4.4.2. Material Handling

4.4.3. Auxiliary Power Units

4.5. By Region (In Value %)

4.5.1. Northeast

4.5.2. Midwest

4.5.3. South

4.5.4. West

5. USA Fuel Cell Vehicle Market Competitive Landscape

5.1. Detailed Profiles of Major Companies

5.1.1. Toyota Motor Corporation

5.1.2. Hyundai Motor Company

5.1.3. Honda Motor Co., Ltd.

5.1.4. General Motors

5.1.5. Nikola Corporation

5.1.6. Daimler AG

5.1.7. Ballard Power Systems

5.1.8. Plug Power Inc.

5.1.9. Cummins Inc.

5.1.10. BMW AG

5.1.11. Ford Motor Company

5.1.12. Stellantis N.V.

5.1.13. Volvo Group

5.1.14. Hyundai Mobis

5.1.15. Bosch GmbH

5.2. Cross Comparison Parameters (Number of Employees, Headquarters Location, Year of Establishment, Revenue, Market Share, Product Portfolio, R&D Expenditure, Strategic Initiatives)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. USA Fuel Cell Vehicle Market Regulatory Framework

6.1. Environmental Standards

6.2. Compliance Requirements

6.3. Certification Processes

7. USA Fuel Cell Vehicle Future Market Size (In USD Billion)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. USA Fuel Cell Vehicle Future Market Segmentation

8.1. By Vehicle Type (In Value %)

8.2. By Power Output (In Value %)

8.3. By Electrolyte Type (In Value %)

8.4. By Application (In Value %)

8.5. By Region (In Value %)

9. USA Fuel Cell Vehicle Market Analysts Recommendations

9.1. Total Addressable Market (TAM), Serviceable Available Market (SAM), and Serviceable Obtainable Market (SOM) Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer

Contact Us

Research Methodology

Step 1: Identification of Key Variables

The research began with constructing an ecosystem map of major stakeholders within the USA fuel cell vehicle market. This process included comprehensive desk research to identify and define variables influencing market growth, such as production capacity, technological developments, and regulatory impacts.

Step 2: Market Analysis and Construction

Historical data was collected to analyze trends in market adoption and the penetration of fuel cell vehicles across regions. Additionally, metrics such as sales volume and infrastructure development were assessed to create a reliable foundation for market projections.

Step 3: Hypothesis Validation and Expert Consultation

Research hypotheses were validated through expert interviews, providing valuable insights into market dynamics and company-specific strategies. Input from these interviews helped refine and validate collected data, ensuring accuracy.

Step 4: Research Synthesis and Final Output

The research culminated with synthesizing data from diverse sources, including industry reports and government publications. A bottom-up approach was applied to verify data accuracy, resulting in a comprehensive and validated analysis of the USA fuel cell vehicle market.

Frequently Asked Questions

01. How big is the USA Fuel Cell Vehicle Market?

The USA fuel cell vehicle market is valued at USD 3.8 billion, with growth driven by government support, advancements in hydrogen infrastructure, and increasing consumer demand for eco-friendly transportation.

02. What are the challenges in the USA Fuel Cell Vehicle Market?

Challenges in the USA fuel cell vehicle market include the high initial cost of fuel cell vehicles, limited hydrogen refueling infrastructure, and competition from battery electric vehicles, which impact consumer adoption rates.

03. Who are the major players in the USA Fuel Cell Vehicle Market?

Key players in the USA fuel cell vehicle market include Toyota, Hyundai, Honda, General Motors, and Nikola, each leveraging advanced fuel cell technology, established brand presence, and hydrogen partnerships to secure a market foothold.

04. What are the growth drivers of the USA Fuel Cell Vehicle Market?

Growth drivers in the USA fuel cell vehicle market include stringent emission regulations, federal incentives, technological advancements in fuel cell technology, and consumer interest in zero-emission vehicles.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.