APAC Automotive Cybersecurity Market Outlook to 2030

Region:Afganistan

Author(s):Shubham Kashyap

Product Code:KROD3535

Region:Afganistan

Author(s):Shubham Kashyap

Product Code:KROD3535

November 2024

87

The APAC Automotive Cybersecurity Market is highly competitive, with global and regional players striving to secure their positions through partnerships, acquisitions, and technological advancements. Leading companies such as Harman International, NXP Semiconductors, and Continental AG dominate the market with their cutting-edge cybersecurity solutions for connected vehicles and autonomous systems.

|

Company Name |

Establishment Year |

Headquarters |

Key Solutions |

Revenue (2023) |

Major Partnerships |

Cybersecurity Focus |

Key Markets |

|

Harman International |

1980 |

Stamford, USA |

|||||

|

NXP Semiconductors |

2006 |

Eindhoven, Netherlands |

|||||

|

Continental AG |

1871 |

Hanover, Germany |

|||||

|

Denso Corporation |

1949 |

Kariya, Japan |

|||||

|

Argus Cyber Security |

2013 |

Tel Aviv, Israel |

Growth Drivers

Market Challenges

The APAC Automotive Cybersecurity Market is expected to witness significant growth over the next five years, driven by the rising adoption of connected vehicles, stringent government regulations, and the increasing threat of cyberattacks. As the automotive industry continues to evolve, with more advanced technologies being integrated into vehicles, the need for robust cybersecurity solutions will only grow. The expansion of electric and autonomous vehicles will also create new opportunities for cybersecurity providers, as these vehicles rely heavily on digital systems that require protection from cyber threats.

Future Market Opportunities

|

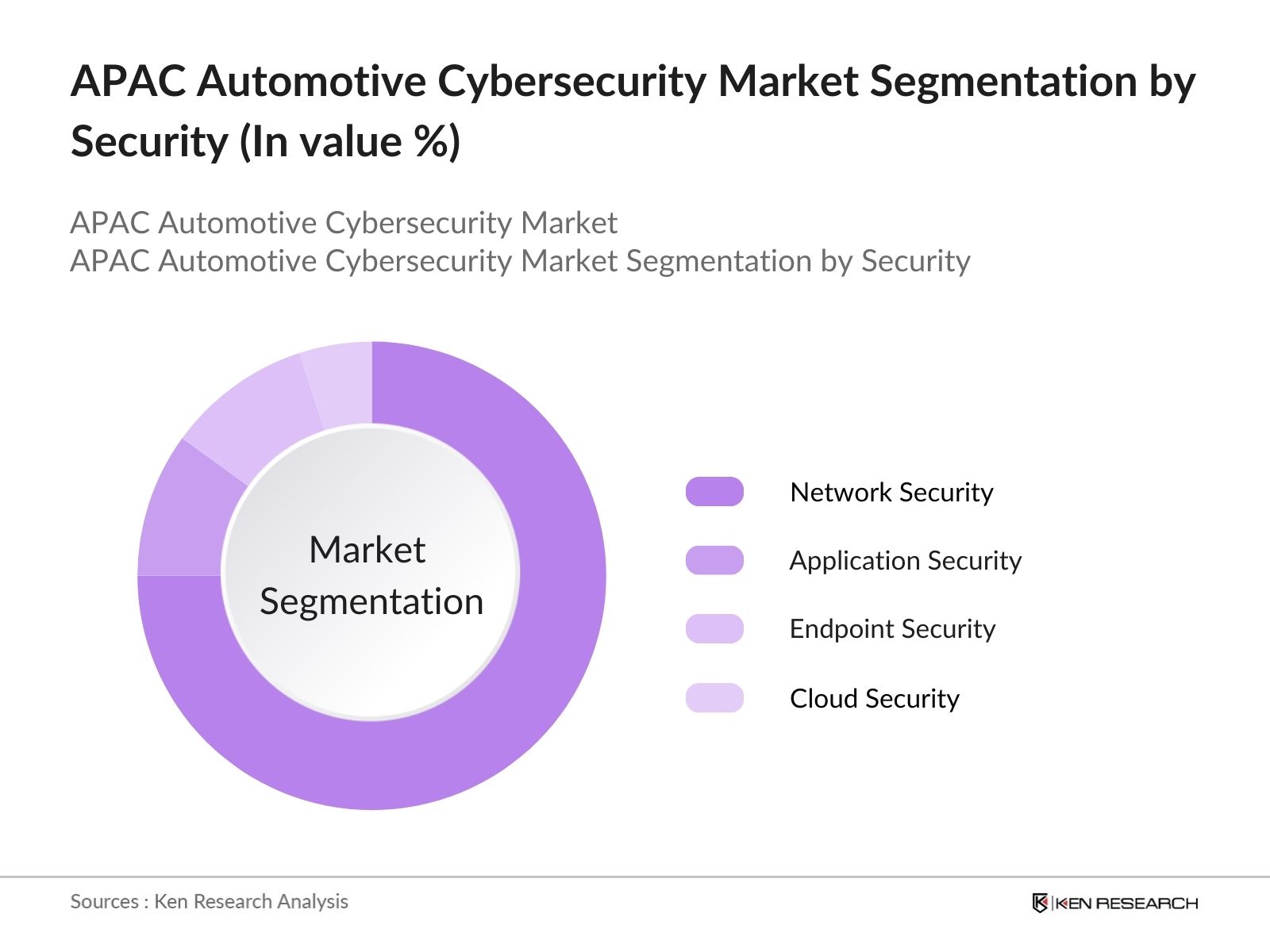

By Security |

Network Security Endpoint Security Application Security Cloud Security |

|

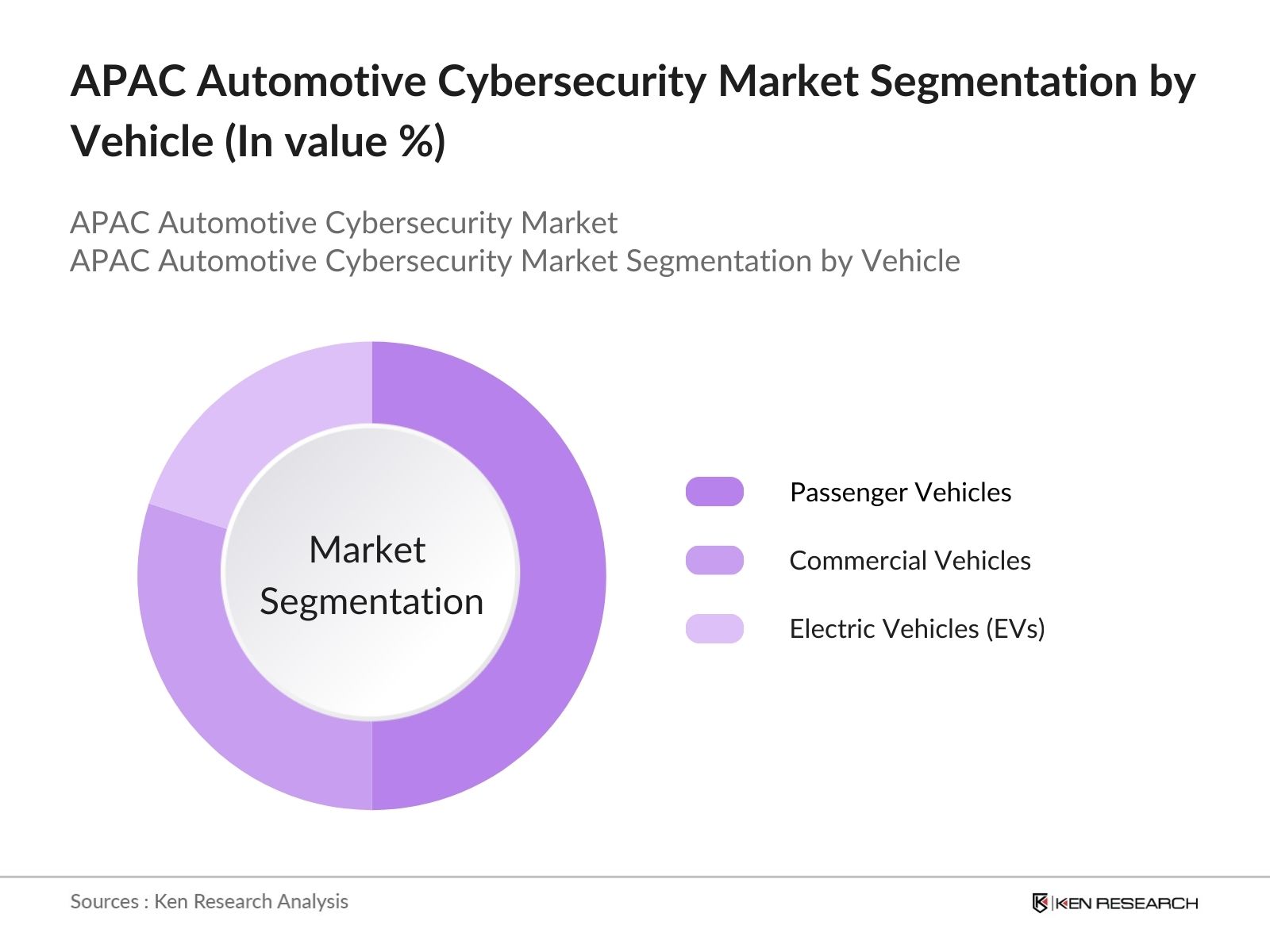

By Vehicle |

Passenger Vehicles Commercial Vehicles Electric Vehicles (EVs) |

|

By Application |

ADAS and Autonomous Systems Infotainment Systems Telematics and Vehicle-to-Vehicle Communication |

|

By Technology |

Intrusion Detection Systems Blockchain-based Solutions Secure OTA (Over-the-Air) Updates |

|

By Region |

China |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (Cybersecurity growth due to connected cars, ADAS, V2X)

1.4. Market Segmentation Overview

2.1. Historical Market Size (Connected vehicles, cybersecurity spending)

2.2. Year-On-Year Growth Analysis (Cyber incidents in automotive industry, data breaches)

2.3. Key Market Developments and Milestones (Vehicle security regulations, cybersecurity standards)

3.1. Growth Drivers

3.1.1. Increase in connected vehicle adoption (Vehicle-to-everything technology)

3.1.2. Rising cybersecurity regulations (APAC-specific government policies)

3.1.3. Increasing threat of automotive cyberattacks (Incidents of hacking, software breaches)

3.1.4. Advancements in autonomous driving technologies (Impact on cybersecurity requirements)

3.2. Market Challenges

3.2.1. High implementation costs for automotive cybersecurity solutions

3.2.2. Lack of skilled cybersecurity professionals (Industry talent gap, training needs)

3.2.3. Varying regulatory landscapes across APAC countries (China, Japan, South Korea)

3.3. Opportunities

3.3.1. Emergence of electric vehicles (New opportunities for cybersecurity in EV systems)

3.3.2. Growth of cybersecurity R&D investments (Japan, South Korea, regional initiatives)

3.3.3. Expansion of connected vehicle infrastructure in emerging markets (India, Southeast Asia)

3.4. Trends

3.4.1. Adoption of blockchain technology for vehicle cybersecurity

3.4.2. Integration of cybersecurity solutions with telematics and ADAS

3.4.3. Increasing focus on cloud-based security solutions for connected vehicles

3.5. Government Regulation (Country-Specific Regulations)

3.5.1. Chinas automotive cybersecurity mandates

3.5.2. Japans Ministry of Economy, Trade and Industry (METI) cybersecurity protocols

3.5.3. South Koreas vehicle cybersecurity policies (Focus on autonomous driving)

3.5.4. Indias vehicle data protection regulations

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4.1. By Security Type (In Value %)

4.1.1. Network Security

4.1.2. Endpoint Security

4.1.3. Application Security

4.1.4. Cloud Security

4.2. By Vehicle Type (In Value %)

4.2.1. Passenger Vehicles

4.2.2. Commercial Vehicles

4.2.3. Electric Vehicles (EVs)

4.3. By Application (In Value %)

4.3.1. ADAS and Autonomous Systems

4.3.2. Infotainment Systems

4.3.3. Telematics and Vehicle-to-Vehicle Communication

4.4. By Technology (In Value %)

4.4.1. Intrusion Detection Systems

4.4.2. Blockchain-based Solutions

4.4.3. Secure OTA (Over-the-Air) Updates

4.5. By Region (In Value %)

4.5.1. China

4.5.2. Japan

4.5.3. South Korea

4.5.4. India

4.5.5. Southeast Asia (Vietnam, Thailand, Malaysia)

5.1. Detailed Profiles of Major Companies

5.1.1. Harman International

5.1.2. NXP Semiconductors

5.1.3. Continental AG

5.1.4. Denso Corporation

5.1.5. Argus Cyber Security

5.1.6. Infineon Technologies

5.1.7. Karamba Security

5.1.8. Trillium Secure

5.1.9. Vector Informatik

5.1.10. Irdeto

5.1.11. Symantec (NortonLifeLock)

5.1.12. Synopsys

5.1.13. SafeRide Technologies

5.1.14. Upstream Security

5.1.15. Trend Micro Inc.

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue, Market Share, Key Partnerships, Key Regions, Cybersecurity R&D Investments)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers And Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Data Privacy Laws (Cybersecurity regulations across APAC regions)

6.2. Compliance Requirements for Connected Vehicles

6.3. Certification and Standardization Processes for Cybersecurity

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth (Autonomous vehicle cybersecurity, rising cyberattacks)

8.1. By Security Type (In Value %)

8.2. By Vehicle Type (In Value %)

8.3. By Application (In Value %)

8.4. By Technology (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis (Automotive OEMs, Tier 1 Suppliers)

9.3. Marketing Initiatives (Cybersecurity Adoption Campaigns)

9.4. White Space Opportunity Analysis (Emerging markets, EV cybersecurity)

The first step involves identifying the critical variables that shape the APAC Automotive Cybersecurity Market. This process includes extensive desk research to understand the key stakeholders, from automotive OEMs to cybersecurity providers, as well as the technologies driving the market.

In this phase, we analyze historical data on the market, including adoption rates of connected vehicles, cybersecurity spending by automotive companies, and the impact of government regulations. This step helps build a robust understanding of market dynamics, which is crucial for forecasting future trends.

We develop market hypotheses based on the data gathered and validate them through interviews with industry experts. This includes consultations with key stakeholders such as automotive cybersecurity solution providers, OEMs, and government bodies.

The final step involves synthesizing the insights gained from secondary research, expert consultations, and data analysis to produce a comprehensive report. This report provides a detailed and validated outlook on the APAC Automotive Cybersecurity Market, ensuring accuracy and reliability.

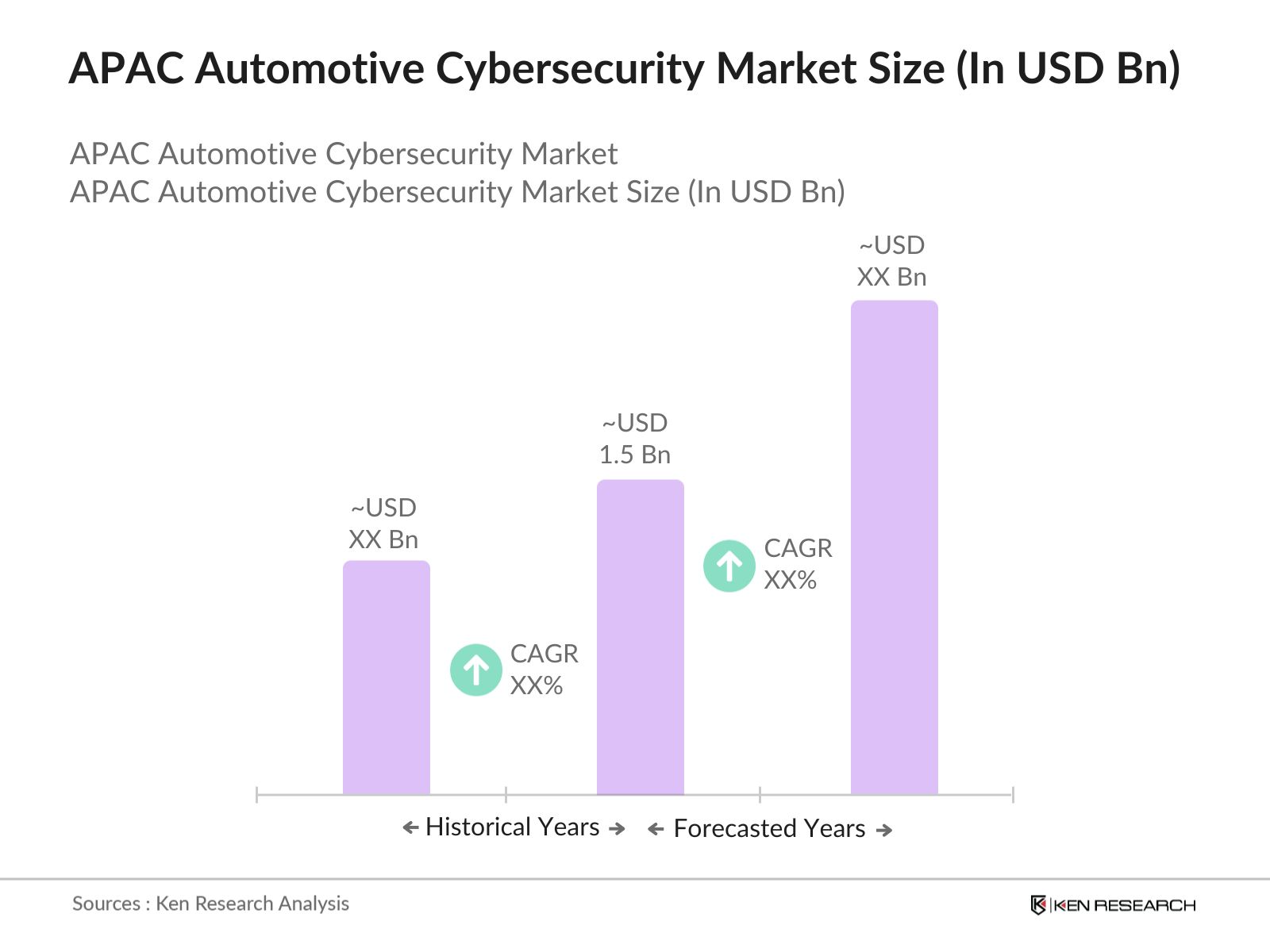

The APAC automotive cybersecurity market is valued at USD 1.5 billion, driven by the increasing integration of connected vehicle technologies and the growing need for secure vehicle communication systems.

Challenges in the APAC automotive cybersecurity market include high implementation costs of cybersecurity solutions, a shortage of skilled cybersecurity professionals, and inconsistent regulatory frameworks across APAC countries, which can hinder market growth.

Key players in the APAC automotive cybersecurity market include Harman International, NXP Semiconductors, Continental AG, Denso Corporation, and Argus Cyber Security. These companies dominate the market due to their strong product offerings and strategic partnerships.

The APAC automotive cybersecurity market is driven by the rising adoption of connected vehicles, the increasing threat of cyberattacks, and the growing regulatory focus on vehicle cybersecurity across major economies like China and Japan.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.