APAC Gaming Market Outlook to 2030

Region:Asia

Author(s):Shubham Kashyap

Product Code:KROD3184

November 2024

98

About the Report

APAC Gaming Market Overview

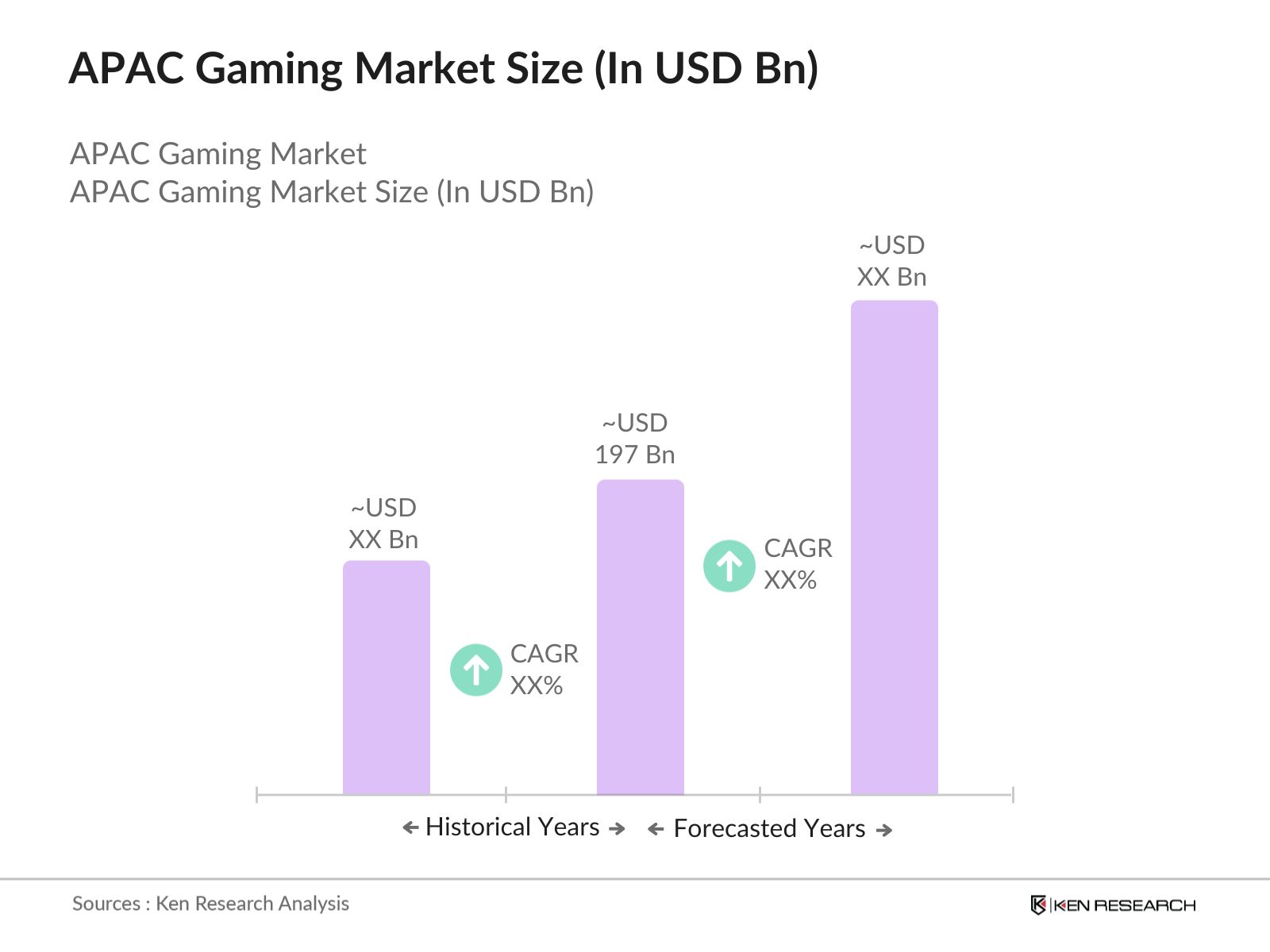

- The APAC Gaming market is currently valued at USD 197 billion, based on a five-year historical analysis. This market is primarily driven by the increasing popularity of online gaming across various platforms, including PC, console, and mobile. The rapid expansion of digital infrastructure, particularly with the rise of cloud gaming and 5G networks, has broadened the gaming ecosystem across the region. APAC, being home to the largest number of gamers globally, is witnessing strong growth, bolstered by high internet penetration and affordable access to gaming platforms.

- Market dominance is concentrated in key countries such as China, Japan, and South Korea, due to their well-established gaming industries, advanced technological frameworks, and strong governmental support. These countries serve as gaming powerhouses with contributions from mobile and console gaming markets. Meanwhile, Southeast Asian countries like Vietnam, Indonesia, and the Philippines are experiencing rapid growth, driven by a younger, tech-savvy population embracing mobile gaming at unprecedented rates.

- Government initiatives are also playing a critical role in the gaming industry's growth. For instance, China has implemented policies encouraging the development of the gaming industry, including tax incentives for gaming companies. South Korea, known for its strong gaming culture, continues to provide support through dedicated gaming venues and hosting international gaming events. Additionally, in 2023, Malaysia announced a USD 100 million fund dedicated to building gaming hubs, accelerating growth in the country's gaming sector.

APAC Gaming Market Segmentation

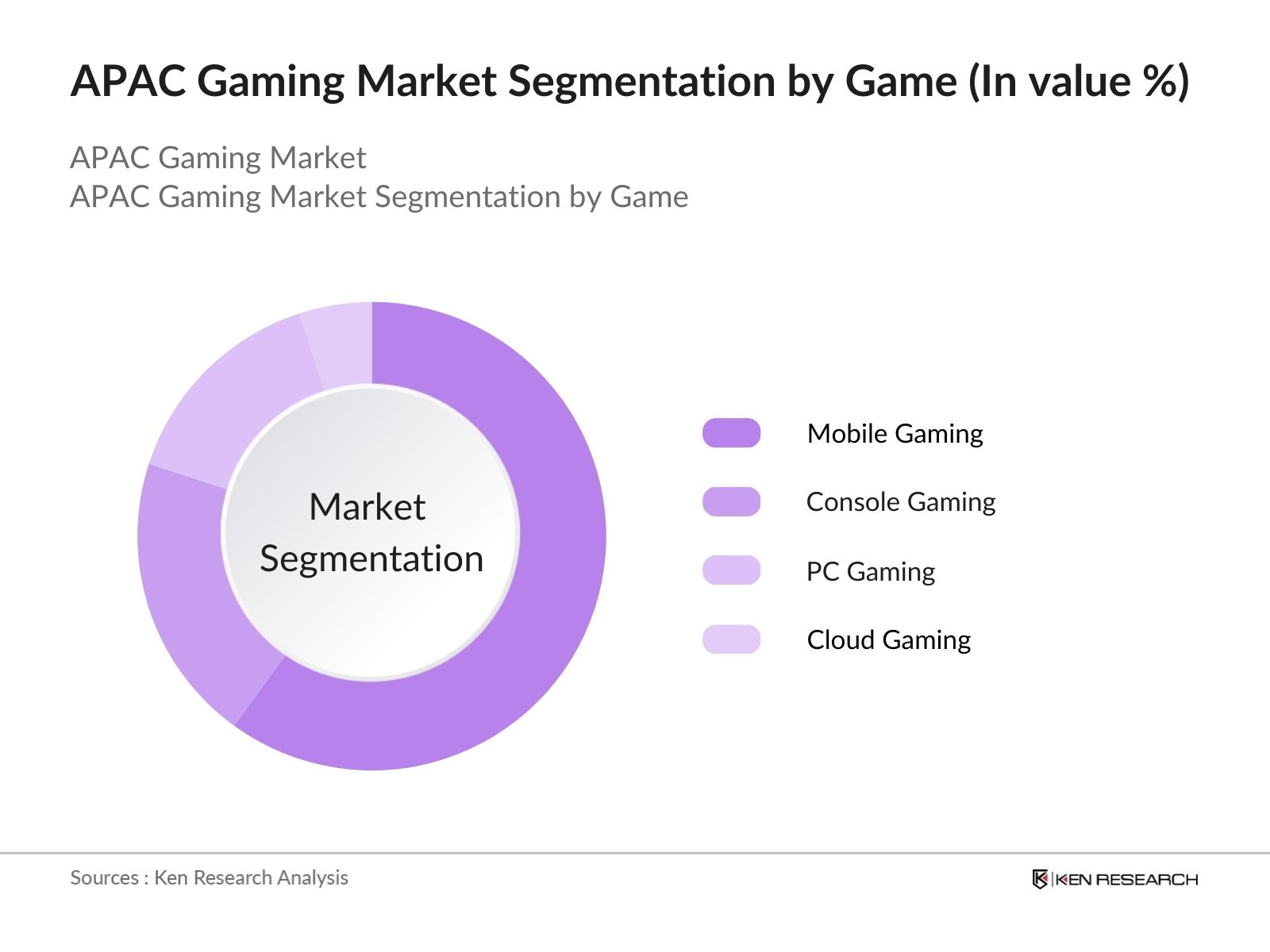

- By Game Type: The market is segmented by game type into mobile gaming, console gaming, and PC gaming. Mobile gaming, fueled by the widespread use of smartphones, dominates the market with a share, particularly in Southeast Asian countries where affordable mobile devices and strong internet penetration are driving mass adoption. Console gaming is popular in countries like Japan and South Korea, where legacy brands like Sony and Nintendo maintain a strong presence. PC gaming remains a cultural staple in countries like China, where internet cafes and professional gaming leagues contribute to its sustained growth.

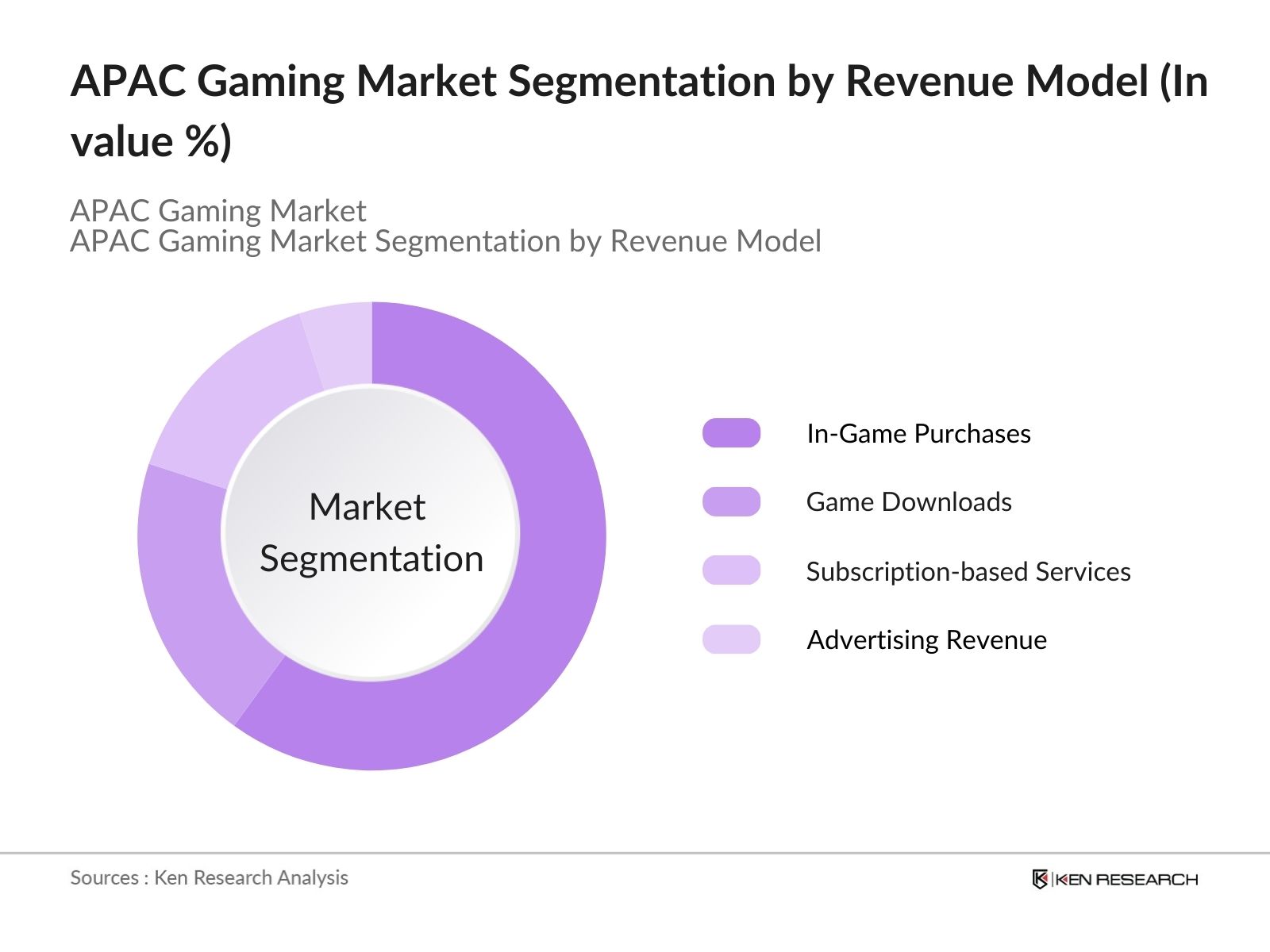

- By Revenue Model: The market is further segmented by revenue model into in-game purchases, game downloads, and subscription-based services. In-game purchases are the largest revenue contributor, especially in mobile games such as PUBG Mobile and Honor of Kings. Game downloads from platforms like Steam and PlayStation Store also generate revenue, while subscription-based services like Xbox Game Pass and PlayStation Plus are gaining traction as gamers shift towards recurring revenue models.

APAC Gaming Market Competitive Landscape

The APAC Gaming market is highly competitive, with global and regional companies vying for market dominance. Leading companies like Tencent, Sony Interactive Entertainment, and NetEase dominate the market through strong game portfolios and strategic partnerships.

|

Company Name |

Establishment Year |

Headquarters |

Key Games |

Revenue (2023) |

Major Platforms |

R&D Investment |

Key Regions |

Partnerships |

|

Tencent |

1998 |

Shenzhen, China |

||||||

|

Sony Interactive Entertainment |

1993 |

Tokyo, Japan |

||||||

|

NetEase |

1997 |

Hangzhou, China |

||||||

|

Garena |

2009 |

Singapore |

||||||

|

Nintendo |

1889 |

Kyoto, Japan |

APAC Gaming Industry Analysis

Growth Drivers

- Rise of Mobile Gaming: Mobile gaming continues to dominate the APAC gaming landscape, driven by an estimated 5.2 billion smartphone users in the region in 2024. With affordable data plans and mobile internet widely available, particularly in emerging markets like India and Indonesia, mobile gaming has become accessible to a broader audience. Games like PUBG Mobile and Free Fire are immensely popular, especially among younger players, contributing to the growth of mobile gaming tournaments and streaming platforms in countries like the Philippines and Malaysia.

- Growing Digital Infrastructure and 5G Networks: The expansion of 5G networks across key APAC markets is a growth driver for the gaming industry. South Korea, for instance, had 15.93 million 5G subscribers by 2023, enabling real-time multiplayer gaming experiences and cloud gaming. Similarly, Japan and China are expanding their 5G networks to cover the majority of their populations by 2024, further boosting the gaming sector. The rollout of 5G technology in Southeast Asia is also facilitating smoother gaming experiences for users in Vietnam, Thailand, and the Philippines.

- Increase in Streaming and Esports Viewership: The rising popularity of streaming platforms such as YouTube Gaming and Twitch is helping to foster a growing ecosystem of esports and game streaming in the APAC region. Streaming viewership is projected to reach 500 million in 2024, driven by the rise of mobile esports and online gaming communities in countries like India and Indonesia. Esports tournaments are increasingly gaining sponsorships from major brands, further driving the gaming industry's growth.

Market Challenges

- Regulatory Issues and Content Restrictions: The APAC gaming market faces regulatory hurdles, particularly in markets like China, where the government imposes strict regulations on gaming content and playing time for minors. In 2022, China introduced a new policy restricting under-18s to just three hours of gaming per week, impacting game developers. Countries like India also face regulatory challenges, with periodic bans on popular games such as PUBG Mobile due to concerns over data privacy and content moderation.

- High Development Costs for AAA Games: The cost of developing high-quality AAA games has increased , creating barriers for smaller game development companies. Large game studios such as Tencent and Sony are better positioned to invest in the development of new games, but indie developers in markets like Southeast Asia often struggle to compete with limited budgets and resources. The increasing demand for high-quality graphics and immersive gaming experiences places pressure on developers to invest heavily in research and development.

APAC Gaming Market Future Outlook

The APAC Gaming market is expected to witness sustained growth over the next five years, driven by rising mobile gaming penetration, expanding digital infrastructure, and growing participation in esports and online streaming. Countries like China, Japan, and South Korea will continue to dominate the market, while emerging markets such as Indonesia, Vietnam, and Thailand offer growth opportunities due to their youthful demographics and rapidly improving internet connectivity.

Future Market Opportunities

- Investment in Gaming Infrastructure: There is an opportunity for investment in gaming infrastructure across APAC. Countries like China and South Korea are leading the way with dedicated gaming arenas and esports venues. South Korea is building an esports stadium in Seoul, set to open by 2025. Southeast Asian nations like Vietnam and Indonesia are also making strides in building esports and gaming hubs to attract international tournaments and enhance their regional gaming capabilities.

- Cross-Platform Gaming and Cloud Gaming Expansion: Cross-platform gaming is another emerging opportunity in the APAC region, as gamers increasingly seek interoperability between consoles, PCs, and mobile devices. Cloud gaming services such as Google Stadia and Xbox Cloud Gaming are poised to gain traction as 5G becomes more widespread, providing seamless gaming experiences without the need for expensive hardware. Emerging markets like Malaysia and Thailand are expected to benefit from this trend as cloud gaming expands accessibility to a larger gaming audience.

Scope of the Report

|

By Game Type |

Mobile Gaming Console Gaming PC Gaming Cloud Gaming |

|

By Revenue Model |

In-Game Purchases Game Downloads Subscription Services Advertising Revenue |

|

By Genre |

Action Games Role-Playing Games Battle Royale Games Sports and Simulation Games |

|

By Platform |

PC Console Mobile Cloud |

|

By Region |

China Japan South Korea Rest of the APAC |

Products

Key Target Audience

Investors and Venture Capitalist Firms

Mobile Network Operators

Gaming Hardware Manufacturers

Game Publishers and Developers

Esports Organizations

Government and Regulatory Bodies (China's State Administration of Press and Publication, South Korea's Ministry of Culture, Sports and Tourism)

Cloud Service Providers

Digital Payment Platforms

Banks and Financial Institutions

Companies

Major Players Mentioned in the Report

Tencent

Sony Interactive Entertainment

NetEase

Garena

Moonton

Bandai Namco Entertainment

Activision Blizzard

Ubisoft

Pearl Abyss

Epic Games

Riot Games

Kakao Games

Nexon

Krafton

Square Enix

Table of Contents

01 APAC Gaming Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

02 APAC Gaming Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

03 APAC Gaming Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Mobile Gaming Penetration (Smartphone adoption, Mobile internet penetration)

3.1.2. Rise in Digital and Cloud Gaming (Cloud gaming services, Cross-platform gaming)

3.1.3. Expansion of Esports and Streaming (Esports viewership, Streaming platforms)

3.2. Market Challenges

3.2.1. Regulatory Restrictions and Content Moderation (Government regulations, Game bans)

3.2.2. High Development Costs for AAA Games (Budget constraints for indie developers)

3.3. Opportunities

3.3.1. Growth in Subscription-based Services (Game subscription models, Cloud gaming)

3.3.2. Emerging Markets in Southeast Asia (Vietnam, Indonesia, Thailand)

3.4. Trends

3.4.1. Integration of Blockchain and NFTs in Gaming (Play-to-earn, Game asset ownership)

3.4.2. Increasing Focus on AR/VR Gaming (Immersive gaming experiences, Hardware advancements)

3.5. Government Regulation

3.5.1. APAC Digital Gaming Policies (Tax incentives, Subsidies for game developers)

3.5.2. Data Privacy and Cybersecurity Regulations (Player data protection, Online security)

3.6. SWOT Analysis

3.7. Stake Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

04 APAC Gaming Market Segmentation

4.1. By Game Type (In Value %)

4.1.1. Mobile Gaming

4.1.2. Console Gaming

4.1.3. PC Gaming

4.1.4. Cloud Gaming

4.2. By Revenue Model (In Value %)

4.2.1. In-Game Purchases

4.2.2. Game Downloads

4.2.3. Subscription-based Services

4.2.4. Advertising Revenue

4.3. By Genre (In Value %)

4.3.1. Action Games

4.3.2. Role-Playing Games (RPG)

4.3.3. Battle Royale Games

4.3.4. Sports and Simulation Games

4.4. By Platform (In Value %)

4.4.1. PC

4.4.2. Console

4.4.3. Mobile

4.4.4. Cloud

4.5. By Region (In Value %)

4.5.1. China

4.5.2. Japan

4.5.3. South Korea

4.5.4. Southeast Asia (Vietnam, Indonesia, Thailand)

05 APAC Gaming Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Tencent

5.1.2. Sony Interactive Entertainment

5.1.3. NetEase

5.1.4. Garena

5.1.5. Nintendo

5.1.6. Bandai Namco Entertainment

5.1.7. Activision Blizzard

5.1.8. Moonton

5.1.9. Ubisoft

5.1.10. Pearl Abyss

5.1.11. Epic Games

5.1.12. Riot Games

5.1.13. Kakao Games

5.1.14. Nexon

5.1.15. Krafton

5.2. Cross Comparison Parameters (Inception Year, Revenue, Key Game Titles, R&D Investment, Player Base, Number of Employees, Global Reach, Strategic Partnerships)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

06 APAC Gaming Market Regulatory Framework

6.1. Gaming Content Regulation (Censorship Policies, Content Approval Processes)

6.2. Age Restriction Policies (Player Age Verification, Limits on Gaming Hours)

6.3. Game Monetization Regulation (Microtransactions, Loot Boxes Regulation)

6.4. Esports Governance (Tournament Rules, Anti-cheat Measures)

07 APAC Gaming Market Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

08 APAC Gaming Market Future Market Segmentation

8.1. By Game Type (In Value %)

8.2. By Revenue Model (In Value %)

8.3. By Genre (In Value %)

8.4. By Platform (In Value %)

8.5. By Region (In Value %)

09 APAC Gaming Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves mapping out the APAC Gaming Market ecosystem, identifying all major stakeholders, and analyzing market dynamics. This step relies on extensive desk research, supported by proprietary databases and secondary data sources.

Step 2: Market Analysis and Construction

This phase includes the compilation and evaluation of historical market data, such as gaming platform penetration, revenue generation models, and major game releases. Historical data is used to assess the market's performance and future growth potential.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed based on industry trends and validated through interviews with key stakeholders, including game developers, publishers, and digital infrastructure providers. These consultations provide firsthand insights into market operations and competitive positioning.

Step 4: Research Synthesis and Final Output

In the final step, data from primary and secondary sources is synthesized to provide a comprehensive analysis of the APAC Gaming Market. This stage ensures that the final report offers accurate and validated insights that align with the current market scenario.

Frequently Asked Questions

01. How big is the APAC Gaming Market?

The APAC gaming market, valued at USD 197 billion, is driven by the rapid growth of mobile gaming, cloud gaming, and esports, alongside advancements in digital infrastructure.

02. What are the challenges in the APAC Gaming Market?

Key challenges in the APAC gaming market include regulatory restrictions in markets like China, high development costs for AAA games, and the increasing complexity of game distribution across multiple platforms.

03. Who are the major players in the APAC Gaming Market?

Major players in the APAC gaming market include Tencent, Sony Interactive Entertainment, NetEase, Garena, and Moonton. These companies dominate the market through strong game portfolios and investments in digital infrastructure.

04. What are the growth drivers of the APAC Gaming Market?

The growth of the APAC gaming market is driven by rising mobile gaming adoption, the expansion of 5G networks, and the increasing popularity of esports and online game streaming platforms.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.