APAC Home Healthcare Market Outlook to 2030

Region:Asia

Author(s):Vijay Kumar

Product Code:KROD9073

November 2024

90

About the Report

APAC Home Healthcare Market Overview

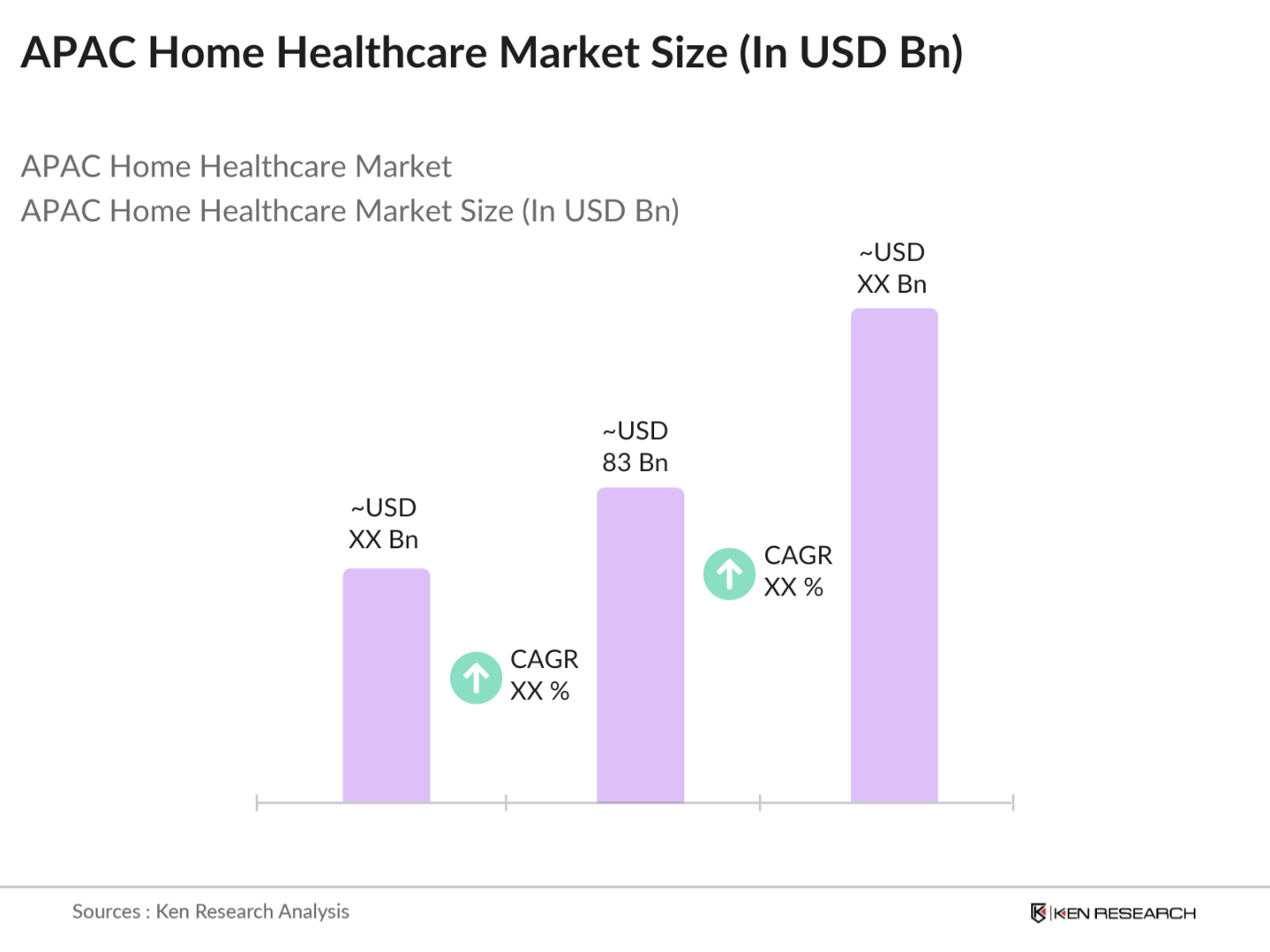

- The APAC Home Healthcare Market is valued at USD 83 billion, based on a five-year historical analysis. The market's growth is driven by an increasing aging population, high prevalence of chronic diseases, and technological advancements in telehealth and remote patient monitoring. With a strong demand for cost-effective healthcare solutions, home healthcare services have become vital for managing long-term care and ensuring patient convenience, especially in regions with rapidly aging demographics, such as Japan and South Korea.

- Countries such as China, Japan, and South Korea dominate the APAC Home Healthcare Market. These countries have implemented robust healthcare policies and exhibit high technology adoption rates. Chinas rapid urbanization and government backing for elderly care drive its prominence, while Japans established healthcare infrastructure and high elderly population accelerate demand. South Korea, with a focus on innovation and digital health, enhances market competitiveness in the region.

- Compliance with regional health standards varies, with countries like Japan and Singapore requiring strict adherence to medical protocols for home healthcare devices. Japans healthcare system, for instance, mandates robust regulatory processes for all home healthcare technology, impacting device approval timelines and distribution.

APAC Home Healthcare Market Segmentation

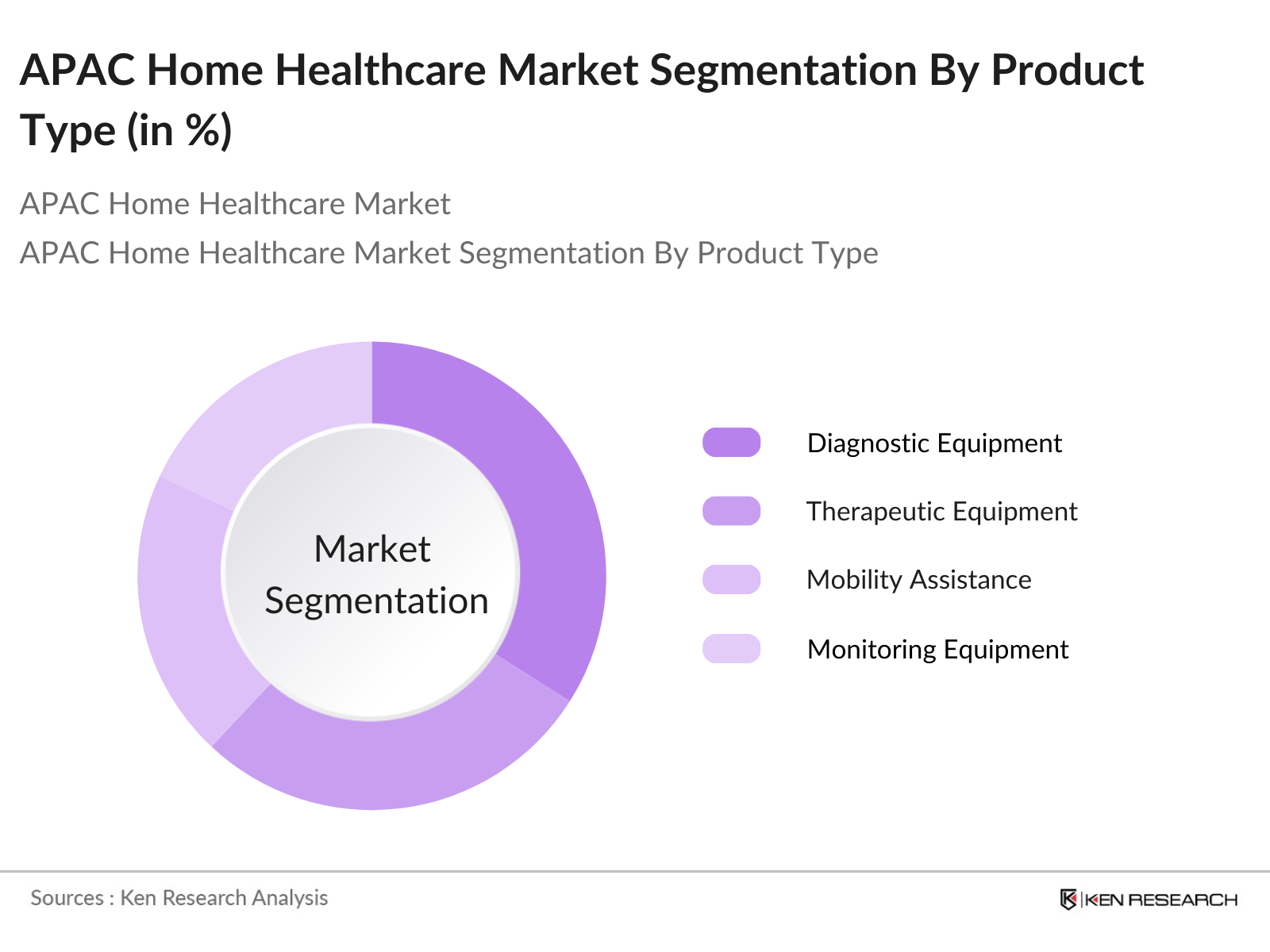

By Product Type: The APAC Home Healthcare Market is segmented by product type into Diagnostic Equipment, Therapeutic Equipment, Mobility Assistance, and Monitoring Equipment. Diagnostic Equipment has a dominant market share due to its vital role in home care for chronic disease management, especially for conditions like diabetes and cardiovascular diseases. Blood pressure monitors and glucose monitoring systems are widely adopted, driven by the need for consistent health tracking and easy access to diagnostics at home.

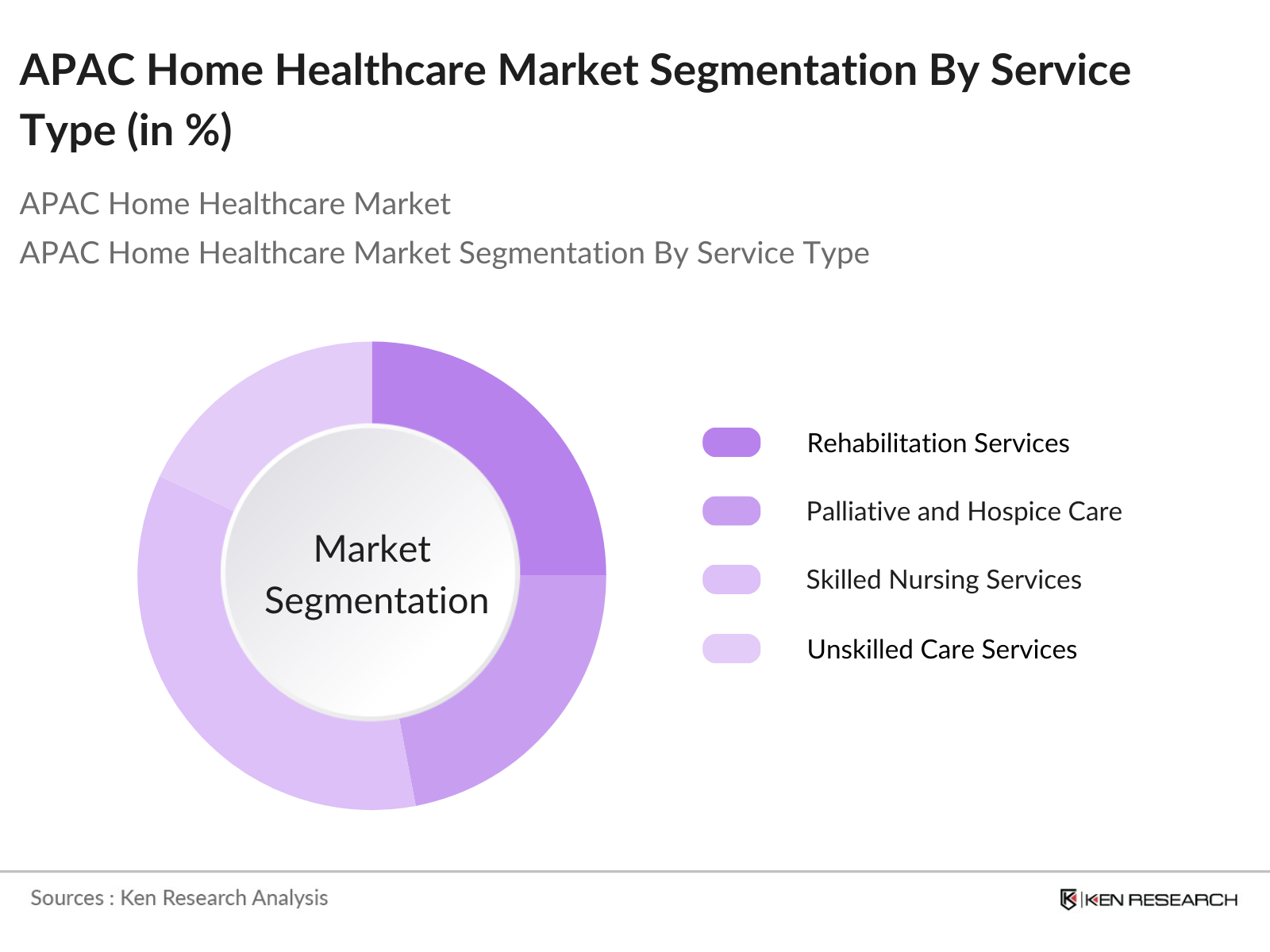

By Service Type: The market is further segmented by service type into Rehabilitation Services, Palliative and Hospice Care, Skilled Nursing Services, and Unskilled Care Services. Skilled Nursing Services hold a significant share within this segment, as they provide essential support for patients needing professional medical assistance at home. Chronic disease patients, post-operative individuals, and elderly patients increasingly rely on skilled nursing due to the personalized attention and reduced hospitalization rates.

APAC Home Healthcare Market Competitive Landscape

The APAC Home Healthcare Market is dominated by several key players, including both established global firms and strong regional companies. The competitive landscape is influenced by these companies investments in technology, customer reach, and their strategic partnerships to enhance product offerings.

APAC Home Healthcare Industry Analysis

Growth Drivers

- Aging Population (Elderly Population Metrics): The APAC region, particularly countries like Japan and South Korea, has one of the fastest-growing elderly populations globally. In 2024, Japans elderly demographic (65 years and older) reached 36.8 million, approximately 29% of its total population, while South Korea saw 17.5% of its population above 65, contributing to significant healthcare needs in home-based services. Rising life expectancy, which currently averages 80 years across high-income APAC countries, further intensifies the demand for home healthcare solutions. Access to age-appropriate healthcare and assisted living solutions is imperative to meet the needs of this demographic.

- Rising Incidence of Chronic Diseases (Chronic Disease Data): Chronic conditions such as diabetes, cardiovascular diseases, and respiratory issues are notably prevalent in the APAC region, impacting approximately 250 million people across China and India alone. Rising urbanization, changing dietary habits, and lifestyle factors contribute significantly to this figure. As of 2024, chronic diseases accounted for over 70% of the disease burden in APAC, escalating the requirement for home healthcare services tailored to chronic disease management.

- Technological Advancements in Remote Patient Monitoring (Technology Adoption Rate): The adoption of remote patient monitoring (RPM) technologies in APAC has surged, particularly in developed markets like Japan and Singapore, where approximately 20% of elderly patients currently benefit from RPM. Supported by expanding broadband and 5G coverage, this growth reflects a greater reliance on tech-based healthcare solutions. In Singapore, over 85% of households have high-speed internet, enabling more accessible remote patient monitoring.

Market Challenges

- High Cost of Home Healthcare Devices (Device Pricing): High pricing for home healthcare devices poses a significant barrier, particularly in developing APAC countries. Home dialysis machines and portable ECG monitors range from $500 to $1,200, limiting access for lower-income households. Countries like India, where the GDP per capita stands at around $2,300, face difficulties in widespread adoption of high-cost home healthcare solutions without government subsidies.

- Regulatory Compliance (Regulatory Barriers): Diverse regulatory frameworks across APAC countries create challenges for home healthcare providers, as each nation maintains distinct healthcare regulations. For instance, stringent medical device regulations in Japan and Singapore require manufacturers to undergo extensive approval processes, impacting market entry for new home healthcare devices. This regulatory complexity limits the speed and efficiency of technology distribution in the region.

APAC Home Healthcare Market Future Outlook

Over the next five years, the APAC Home Healthcare Market is expected to expand significantly, fueled by rising healthcare expenditures, government initiatives supporting home care, and increased adoption of remote care technology. Factors such as innovations in wearable health devices and the integration of artificial intelligence in diagnostics are set to boost the markets growth.

Market Opportunities

- Expansion of Telehealth Services (Telehealth Penetration): Telehealth services have expanded significantly across APAC, with countries like China witnessing a 25% increase in telehealth consultations. Approximately 200 million people in China used telehealth services in 2024, driven by growing internet penetration and an increasing focus on digital health. This expansion presents considerable opportunities for integrating telehealth with home healthcare for enhanced patient monitoring and consultation accessibility.

- Integration with AI and IoT (Smart Healthcare Innovations): The integration of AI and IoT within home healthcare is accelerating in APAC, with Japan leading in AI-based healthcare applications. In 2024, Japan reported over 1,500 registered AI-powered healthcare devices. AI and IoT integration support personalized care and real-time health tracking, improving outcomes for homebound patients.

Scope of the Report

|

Product Type |

Diagnostic Equipment Therapeutic Equipment Mobility Assistance Monitoring Equipment |

|

Service Type |

Rehabilitation Services Palliative and Hospice Care Skilled Nursing Services Unskilled Care Services |

|

Application |

Cardiovascular Diabetes Management Respiratory Therapy Cancer Care |

|

Mode of Delivery |

On-Premise Cloud-Based Hybrid Model |

|

Region |

China Japan India South Korea Australia New Zealand |

Products

Key Target Audience

Home Healthcare Service Providers

Hospitals and Clinics

Medical Device Manufacturers

Technology Solution Providers

Insurance Companies

Investment and Venture Capitalist Firms

Government and Regulatory Bodies (Ministry of Health, APAC Health Regulatory Agencies)

Home Care Product Distributors

Companies

Players Mentioned in the Report

Philips Healthcare

Omron Healthcare

GE Healthcare

Fresenius Medical Care

ResMed Inc.

Abbott Laboratories

A&D Company Ltd.

Bayer Healthcare

Braun Melsungen AG

Cardinal Health

Table of Contents

1. APAC Home Healthcare Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2. APAC Home Healthcare Market Size (In USD Bn)

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3. APAC Home Healthcare Market Analysis

3.1 Growth Drivers

3.1.1 Aging Population (Elderly Population Metrics)

3.1.2 Rising Incidence of Chronic Diseases (Chronic Disease Data)

3.1.3 Technological Advancements in Remote Patient Monitoring (Technology Adoption Rate)

3.1.4 Increased Healthcare Expenditure (Healthcare Expenditure per Capita)

3.1.5 Shift to Value-Based Care (Adoption of Value-Based Care Models)

3.2 Market Challenges

3.2.1 High Cost of Home Healthcare Devices (Device Pricing)

3.2.2 Regulatory Compliance (Regulatory Barriers)

3.2.3 Limited Awareness in Rural Areas (Awareness Penetration Rates)

3.2.4 Data Privacy and Security Concerns (Data Protection Challenges)

3.3 Opportunities

3.3.1 Expansion of Telehealth Services (Telehealth Penetration)

3.3.2 Integration with AI and IoT (Smart Healthcare Innovations)

3.3.3 Emerging Markets in Southeast Asia (Regional Growth Potentials)

3.3.4 Rising Demand for Personalized Home Care Solutions (Personalized Healthcare Demand)

3.4 Trends

3.4.1 Adoption of Wearable Health Monitoring Devices (Wearables Adoption)

3.4.2 Shift Toward Remote Patient Monitoring (Remote Monitoring Rate)

3.4.3 Integration with Smart Home Ecosystems (Smart Home Integration)

3.4.4 Increased Usage of AI in Home Diagnostics (AI Usage in Diagnostics)

3.5 Regulatory Overview

3.5.1 Compliance with APAC Health Standards (Regional Compliance Standards)

3.5.2 Data Privacy Regulations (HIPAA, GDPR Adaptations)

3.5.3 Insurance and Reimbursement Policies (Insurance Coverage Rates)

3.5.4 Licensing and Accreditation (Licensing Standards in APAC)

3.6 SWOT Analysis

3.7 Stake Ecosystem

3.8 Porters Five Forces Analysis

3.9 Competition Ecosystem

4. APAC Home Healthcare Market Segmentation

4.1 By Product Type (In Value %)

4.1.1 Diagnostic Equipment (Blood Pressure Monitors, Blood Glucose Monitors, etc.)

4.1.2 Therapeutic Equipment (Ventilators, Oxygen Therapy Equipment)

4.1.3 Mobility Assistance (Wheelchairs, Walkers)

4.1.4 Monitoring Equipment (Heart Rate Monitors, Oximeters)

4.2 By Service Type (In Value %)

4.2.1 Rehabilitation Services (Physical Therapy, Occupational Therapy)

4.2.2 Palliative and Hospice Care (End-of-Life Care)

4.2.3 Skilled Nursing Services (Nursing Care, Medical Care)

4.2.4 Unskilled Care Services (Assistance with Daily Living Activities)

4.3 By Application (In Value %)

4.3.1 Cardiovascular (Heart Disease Monitoring, Stroke Rehabilitation)

4.3.2 Diabetes Management (Blood Sugar Monitoring, Insulin Administration)

4.3.3 Respiratory Therapy (COPD, Asthma Treatment)

4.3.4 Cancer Care (Palliative Care, Chemotherapy Monitoring)

4.4 By Mode of Delivery (In Value %)

4.4.1 On-Premise (Home Visits)

4.4.2 Cloud-Based (Remote Monitoring Systems)

4.4.3 Hybrid Model (Integrated Care Delivery)

4.5 By Country (In Value %)

4.5.1 China

4.5.2 Japan

4.5.3 India

4.5.4 South Korea

4.5.5 Australia and New Zealand

5. APAC Home Healthcare Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1 Philips Healthcare

5.1.2 Omron Healthcare

5.1.3 GE Healthcare

5.1.4 Fresenius Medical Care

5.1.5 Medtronic PLC

5.1.6 ResMed Inc.

5.1.7 Abbott Laboratories

5.1.8 A&D Company Ltd.

5.1.9 Bayer Healthcare

5.1.10 Braun Melsungen AG

5.1.11 Cardinal Health

5.1.12 Becton Dickinson and Company

5.1.13 Baxter International Inc.

5.1.14 Nihon Kohden Corporation

5.1.15 Invacare Corporation

5.2 Cross Comparison Parameters (Revenue, Headquarters, Regional Presence, Product Portfolio, Patents Held, Partnerships, No. of Employees, Market Presence)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6. APAC Home Healthcare Market Regulatory Framework

6.1 Healthcare Compliance Standards (ISO, FDA, etc.)

6.2 Reimbursement Frameworks

6.3 Certification Processes

6.4 Insurance Policies and Coverage

7. APAC Home Healthcare Future Market Size (In USD Bn)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8. APAC Home Healthcare Future Market Segmentation

8.1 By Product Type (In Value %)

8.2 By Service Type (In Value %)

8.3 By Application (In Value %)

8.4 By Mode of Delivery (In Value %)

8.5 By Country (In Value %)

9. APAC Home Healthcare Market Analysts Recommendations

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The research begins with mapping the APAC Home Healthcare Market, examining stakeholders from device manufacturers to service providers. Extensive desk research and proprietary data sources are used to define the variables affecting market behavior, such as consumer demand and technology adoption rates.

Step 2: Market Analysis and Construction

This stage involves gathering historical data on market revenue, product demand, and service types. Analyzing the interaction between service providers and users, we assess market saturation levels, service quality, and the factors driving revenue growth.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses regarding market trends and growth are validated through expert interviews with industry stakeholders, offering direct insight into operational challenges and opportunities. These insights help refine our data models and ensure an accurate market assessment.

Step 4: Research Synthesis and Final Output

In this final phase, insights are gathered directly from home healthcare providers, offering data on product adoption and service demand. Combining these findings with our bottom-up approach ensures a well-rounded analysis of the APAC Home Healthcare Market.

Frequently Asked Questions

1. How big is the APAC Home Healthcare Market?

The APAC Home Healthcare Market is valued at USD 83 billion, based on a five-year historical analysis. The market's growth is driven by an increasing aging population, high prevalence of chronic diseases, and technological advancements in telehealth and remote patient monitoring.

2. What are the main challenges in the APAC Home Healthcare Market?

Key challenges include regulatory compliance, high device costs, and data privacy concerns, which can hinder adoption among new users and regions.

3. Who are the major players in the APAC Home Healthcare Market?

Leading players include Philips Healthcare, Omron Healthcare, GE Healthcare, Fresenius Medical Care, and ResMed Inc., known for their innovative product offerings.

4. What factors are driving growth in the APAC Home Healthcare Market?

Growth is propelled by increasing healthcare costs, patient preference for in-home care, and technological advancements in remote monitoring solutions.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.