APAC Polysilicon Market Outlook to 2030

Region:Asia

Author(s):Shubham Kashyap

Product Code:KROD11315

We use cookies and similar technologies to improve your experience, analyze website traffic, and personalize content. By clicking Accept All, you consent to our use of cookies and analytics tracking.

Privacy PolicyRegion:Asia

Author(s):Shubham Kashyap

Product Code:KROD11315

November 2024

94

The APAC Polysilicon Market features several leading players, leveraging advanced manufacturing technologies and government partnerships to maintain a competitive edge. Chinese manufacturers dominate through large-scale production and export capabilities, while South Korean and Japanese companies focus on high-purity polysilicon for electronics.

The APAC Polysilicon Market is poised for substantial growth, driven by expanding renewable energy projects and the increasing importance of semiconductors in consumer electronics and automotive applications. Technological advancements in production processes and growing investment in research and development are expected to further enhance market dynamics. The integration of AI and IoT in polysilicon applications presents additional opportunities for the industry.

|

By Application |

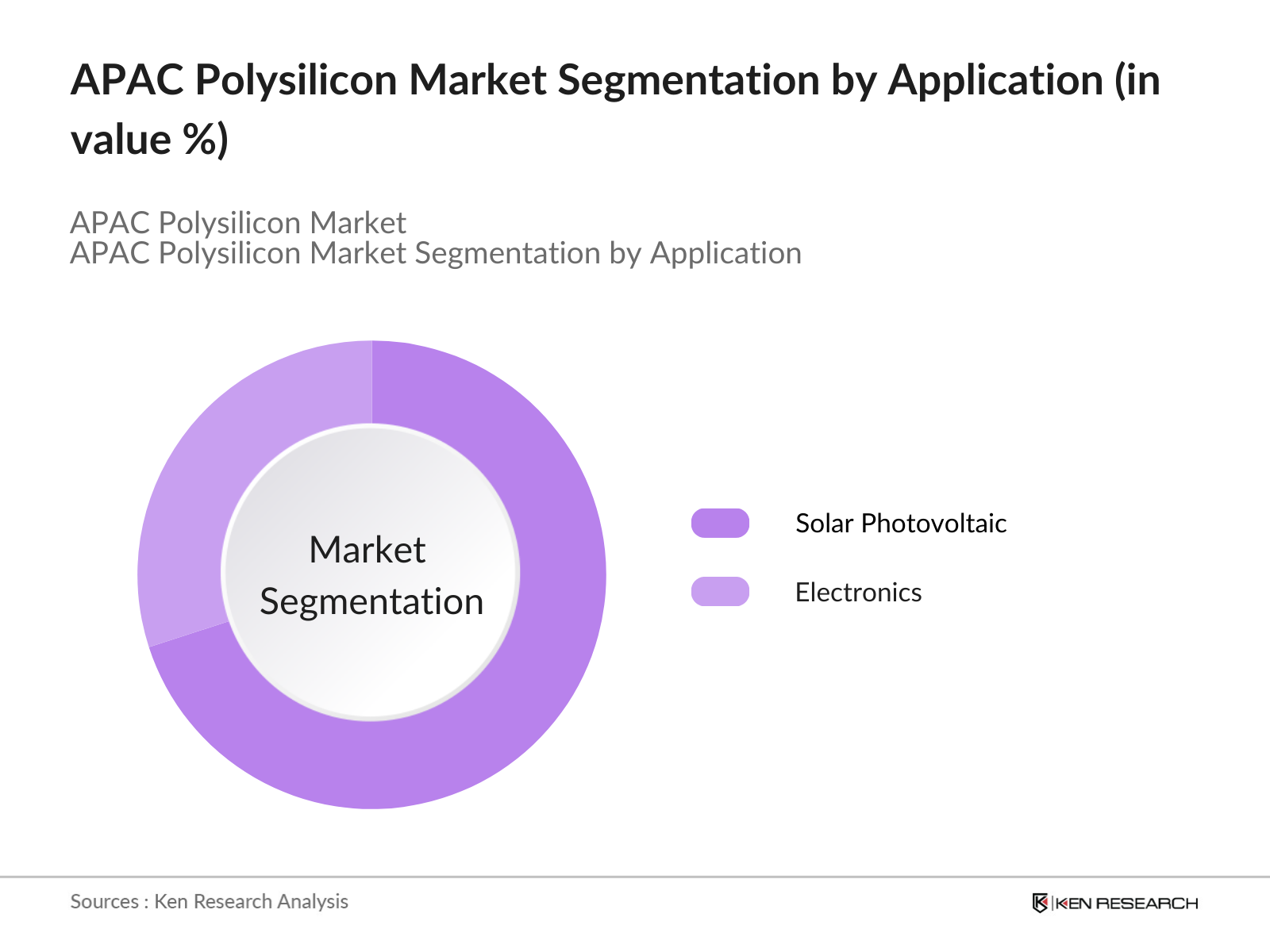

Solar Photovoltaics Electronics |

|

By Manufacturing Technology |

Siemens Process Fluidized Bed Reactor (FBR) Process Upgraded Metallurgical Grade (UMG) Process |

|

By Purity Level |

Electronic Grade Solar Grade |

|

By Geography |

China South Korea Japan |

|

By End-Use Industry |

Renewable Energy Semiconductor Manufacturing |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Expansion of Solar Photovoltaic Installations

3.1.2. Advancements in Semiconductor Manufacturing

3.1.3. Government Incentives for Renewable Energy

3.1.4. Technological Innovations in Polysilicon Production

3.2. Market Challenges

3.2.1. High Capital Expenditure for Production Facilities

3.2.2. Volatility in Raw Material Prices

3.2.3. Environmental and Regulatory Compliance

3.3. Opportunities

3.3.1. Emerging Markets in Southeast Asia

3.3.2. Development of High-Purity Polysilicon for Electronics

3.3.3. Integration of Polysilicon in Advanced Energy Storage Solutions

3.4. Trends

3.4.1. Shift Towards Monocrystalline Solar Panels

3.4.2. Adoption of Energy-Efficient Production Technologies

3.4.3. Strategic Partnerships and Joint Ventures

3.5. Government Regulations

3.5.1. Renewable Energy Targets and Policies

3.5.2. Import and Export Tariffs

3.5.3. Environmental Standards and Emission Norms

3.5.4. Subsidies and Tax Incentives

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competitive Landscape

4.1. By Form (Value %)

4.1.1. Chunks

4.1.2. Granules

4.1.3. Rods

4.2. By Application (Value %)

4.2.1. Solar Photovoltaics

4.2.1.1. Monocrystalline Solar Panels

4.2.1.2. Multicrystalline Solar Panels

4.2.2. Electronics

4.2.2.1. Semiconductors

4.2.2.2. Integrated Circuits

4.3. By Manufacturing Technology (Value %)

4.3.1. Siemens Process

4.3.2. Fluidized Bed Reactor (FBR) Process

4.3.3. Upgraded Metallurgical Grade (UMG) Process

4.4. By Purity Level (Value %)

4.4.1. Electronic Grade

4.4.2. Solar Grade

4.5. By Country (Value %)

4.5.1. China

4.5.2. Japan

4.5.3. South Korea

4.5.4. India

4.5.5. Rest of Asia-Pacific

5.1. Detailed Profiles of Major Companies

5.1.1. GCL-Poly Energy Holdings Limited

5.1.2. Wacker Chemie AG

5.1.3. OCI Company Ltd.

5.1.4. Daqo New Energy Corp.

5.1.5. Tongwei Co., Ltd.

5.1.6. Xinte Energy Co., Ltd.

5.1.7. Hemlock Semiconductor Operations LLC

5.1.8. REC Silicon ASA

5.1.9. Mitsubishi Materials Corporation

5.1.10. Tokuyama Corporation

5.1.11. Hanwha Solutions Corporation

5.1.12. East Hope Group

5.1.13. Sichuan Yongxiang Co., Ltd.

5.1.14. Asia Silicon (Qinghai) Co., Ltd.

5.1.15. Qatar Solar Technologies

5.2. Cross Comparison Parameters

5.2.1. Production Capacity (Metric Tons)

5.2.2. Revenue (USD Billion)

5.2.3. Market Share (%)

5.2.4. Number of Employees

5.2.5. Headquarters Location

5.2.6. Year of Establishment

5.2.7. R&D Investment (% of Revenue)

5.2.8. Key Clients and Partnerships

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.6.1. Venture Capital Funding

5.6.2. Government Grants

5.6.3. Private Equity Investments

6.1. Environmental Standards

6.2. Compliance Requirements

6.3. Certification Processes

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Form (Value %)

8.2. By Application (Value %)

8.3. By Manufacturing Technology (Value %)

8.4. By Purity Level (Value %)

8.5. By Country (Value %)

9.1. Total Addressable Market (TAM) Analysis

9.2. Serviceable Available Market (SAM) Analysis

9.3. Serviceable Obtainable Market (SOM) Analysis

9.4. Customer Cohort Analysis

9.5. Marketing Initiatives

9.6. White Space Opportunity Analysis

Disclaimer Contact Us

The first step involved mapping the key stakeholders in the APAC Polysilicon Market, focusing on manufacturers, end-users, and regulatory bodies. Secondary data sources, including industry reports and company publications, were extensively utilized.

Historical data on production volumes, revenues, and trade flows were analyzed to construct a robust market model. This process included evaluating cost structures and market dynamics influencing demand across key applications.

Insights were validated through interviews with industry experts from leading companies like GCL-Poly and OCI Company Ltd. These discussions provided clarity on emerging trends and key operational challenges.

Comprehensive data analysis was conducted to deliver actionable insights. The findings were corroborated with primary data to ensure accuracy and relevancy in the final report.

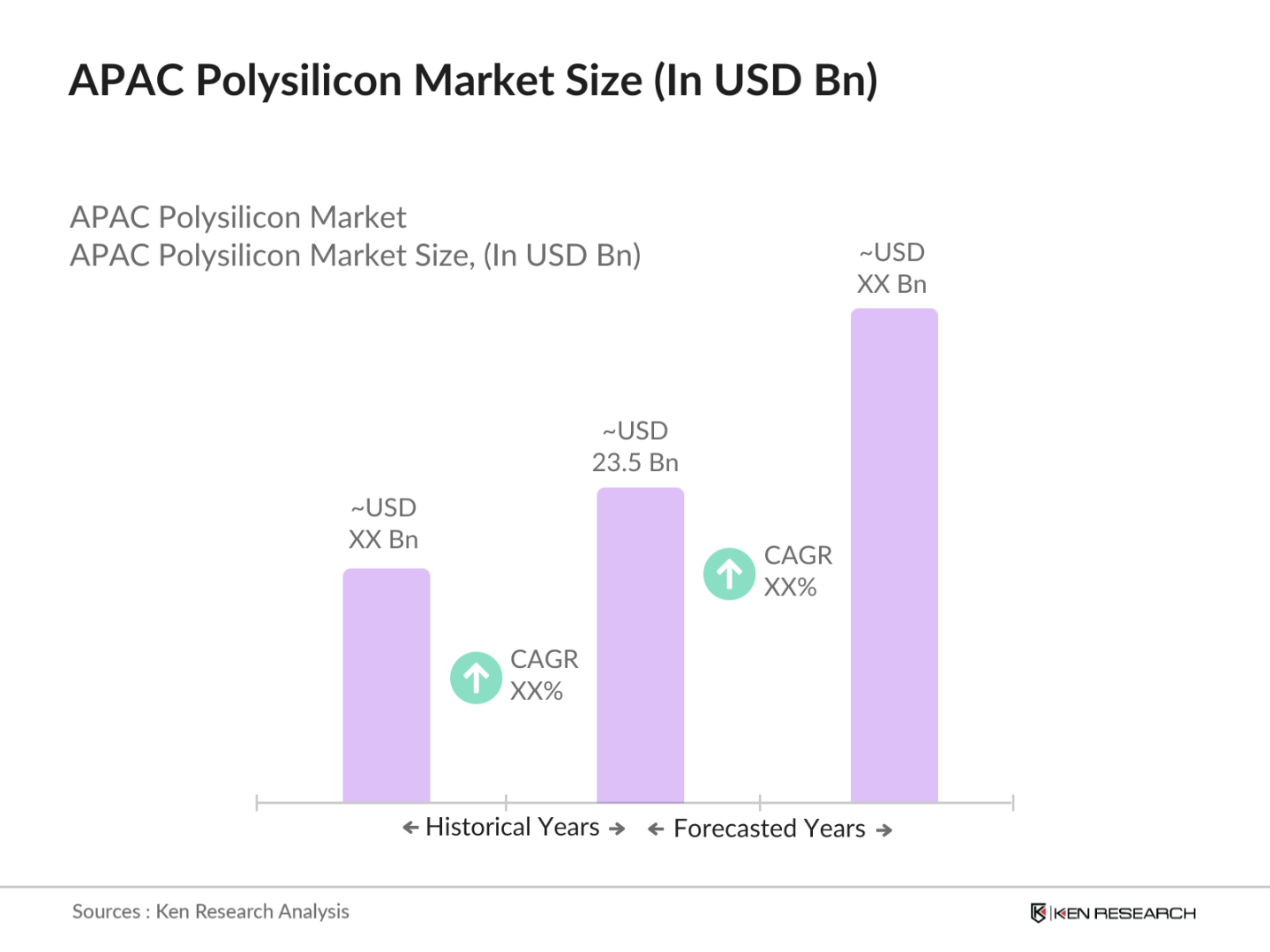

The APAC Polysilicon Market is valued at USD 23.5 billion, driven by demand from the solar PV and semiconductor sectors.

Challenges in the APAC Polysilicon Market include high initial investment costs, regulatory compliance for emissions, and fluctuating raw material prices.

Key players in the APAC Polysilicon Market include GCL-Poly Energy, OCI Company Ltd., Wacker Chemie, Daqo New Energy, and Tokuyama Corporation.

The APAC Polysilicon Market is propelled by government support for renewable energy, growth in the solar PV sector, and increasing semiconductor demand.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.