APAC Automotive Diagnostics Market Outlook to 2030

Region:Afganistan

Author(s):Shambhavi

Product Code:KROD4605

Region:Afganistan

Author(s):Shambhavi

Product Code:KROD4605

November 2024

92

Listen to the audio summary

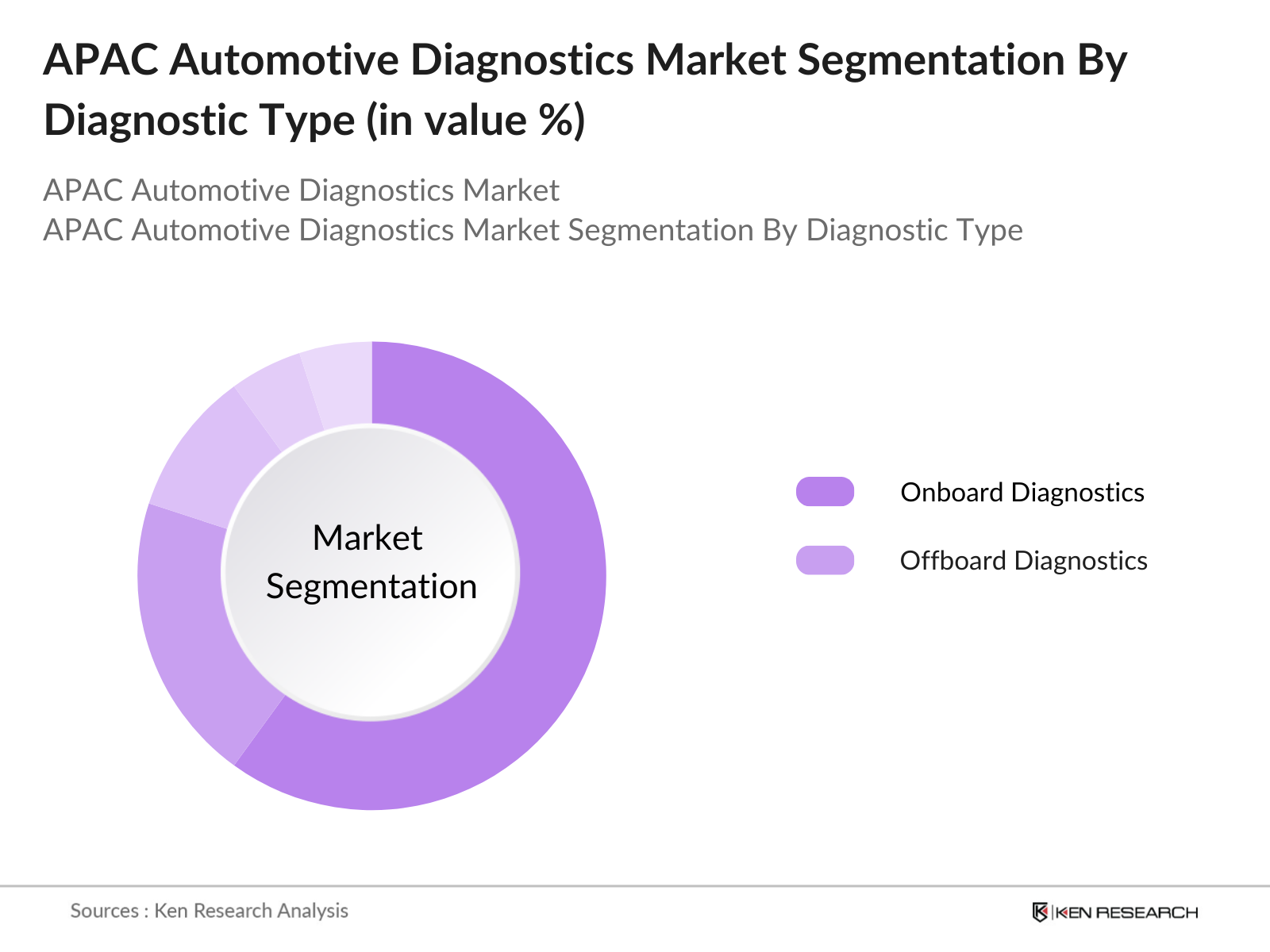

By Diagnostic Type: The APAC automotive diagnostics market is segmented by diagnostic type into onboard diagnostics and offboard diagnostics. Onboard diagnostics hold a dominant market share in this category due to their growing integration in modern vehicles for real-time vehicle health monitoring and emission tracking. Automakers are increasingly embedding advanced onboard diagnostic systems to comply with stringent emission regulations and provide drivers with better insights into vehicle performance.

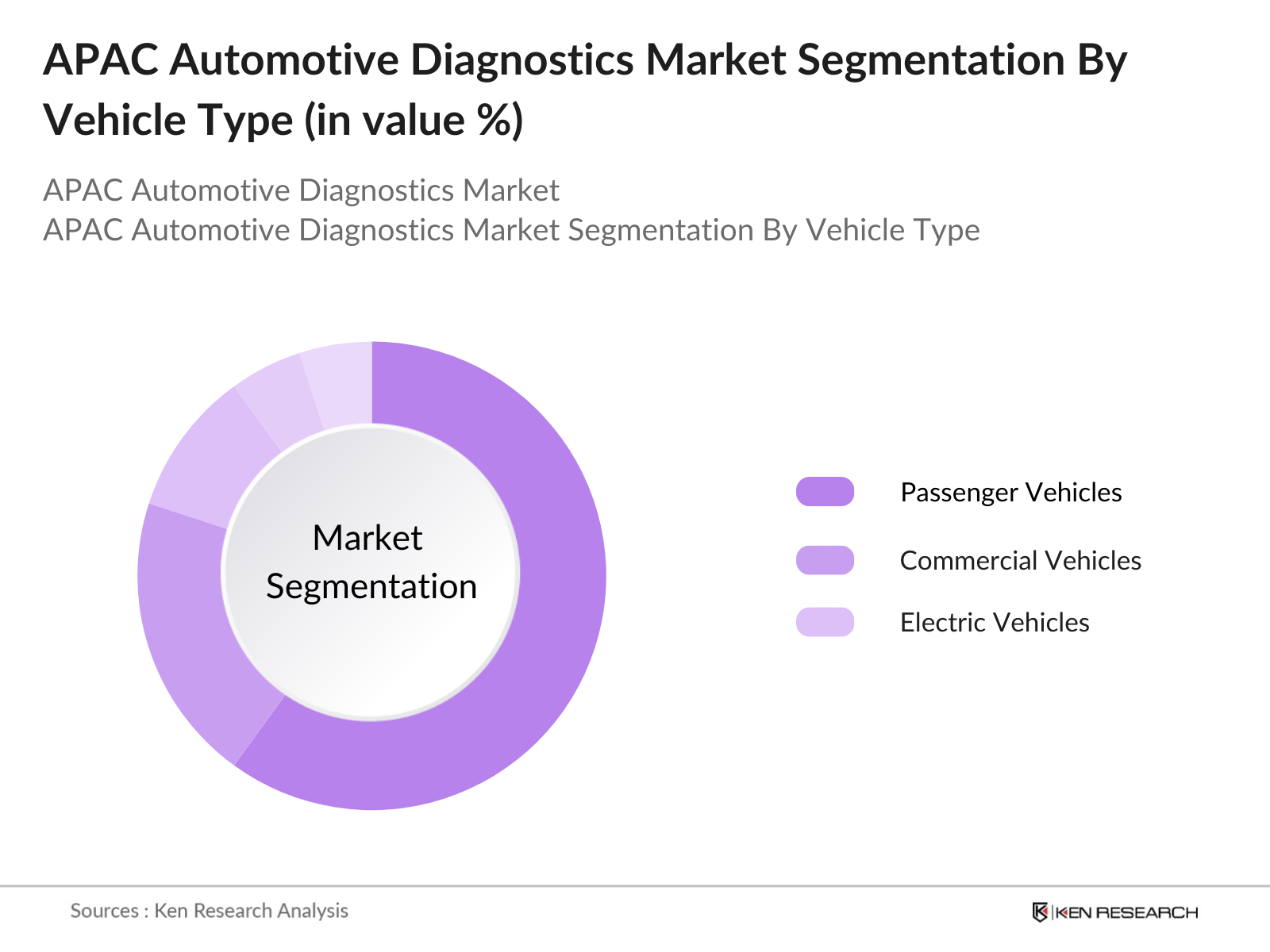

By Vehicle Type: The market is also segmented by vehicle type into passenger vehicles, commercial vehicles, and electric vehicles. Passenger vehicles dominate the market under this segmentation, largely due to the high volume of passenger car sales in China and India. The increasing use of diagnostics to enhance vehicle safety and comply with emission norms has further boosted the dominance of this segment.

The APAC automotive diagnostics market is dominated by a mix of global and regional players that compete on innovation, service quality, and technology integration. Key players are investing in R&D and strategic partnerships to expand their market presence. The APAC automotive diagnostics market is characterized by the presence of major global corporations like Bosch and Continental, alongside regional players such as Denso and Hitachi. These companies are focusing on developing new diagnostic tools and platforms to support electric and autonomous vehicles, which are key drivers of future market growth. Their extensive distribution networks and technological expertise enable them to maintain their leadership positions in the market.

Over the next five years, the APAC automotive diagnostics market is expected to experience significant growth driven by the rise of electric vehicles (EVs) and the increased adoption of advanced diagnostics for connected cars. The region's automotive industry is increasingly focused on complying with stringent emission regulations, further encouraging the adoption of onboard diagnostics. Additionally, the rapid advancements in artificial intelligence (AI) and machine learning (ML) are set to revolutionize vehicle diagnostics, enabling predictive maintenance and more accurate fault detection. As governments across APAC enforce stricter vehicle safety and emission norms, the market will continue to expand, presenting lucrative opportunities for key players.

|

Segments |

Sub-segments |

|

By Vehicle Type |

Passenger Vehicles |

|

Commercial Vehicles |

|

|

Electric Vehicles |

|

|

By Diagnostic Type |

Onboard Diagnostics |

|

Off-Board Diagnostics |

|

|

By Product Type |

Scanners and Testers |

|

Software Solutions |

|

|

Repair and Maintenance Tools |

|

|

By Application |

Preventive Maintenance |

|

Repair and Service |

|

|

Inspection and Testing |

|

|

By Country |

China |

|

Japan |

|

|

India |

|

|

South Korea |

|

|

Australia |

APAC Automotive Diagnostics Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

APAC Automotive Diagnostics Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

APAC Automotive Diagnostics Market Analysis

3.1. Growth Drivers

3.1.1. Increased Vehicle Production and Sales (Automotive Production Data)

3.1.2. Growing Adoption of Connected Vehicles (Telematics Integration)

3.1.3. Stringent Emission Regulations (Emission Control Standards)

3.1.4. Rising Demand for Electric Vehicles (EV Growth Data)

3.2. Market Challenges

3.2.1. High Cost of Advanced Diagnostic Tools (Cost Analysis)

3.2.2. Shortage of Skilled Technicians (Workforce Shortage Data)

3.2.3. Data Security Concerns with Connected Diagnostics (Cybersecurity Issues)

3.3. Opportunities

3.3.1. Advancements in Artificial Intelligence for Diagnostics (AI Integration in Automotive Diagnostics)

3.3.2. Expansion in Emerging APAC Markets (Geographic Expansion Trends)

3.3.3. Growing Aftermarket Segment (Aftermarket Expansion Data)

3.4. Trends

3.4.1. Integration of Cloud-Based Diagnostics (Cloud Computing)

3.4.2. Increasing Role of Predictive Maintenance (Predictive Analytics in Automotive)

3.4.3. Use of Mobile Diagnostics Solutions (Mobile Diagnostics Data)

3.5. Government Regulations

3.5.1. Vehicle Safety Inspection Standards (Inspection Policy)

3.5.2. Emission Testing Regulations (Emission Test Requirements)

3.5.3. OBD (Onboard Diagnostics) Compliance Regulations (OBD Compliance Framework)

3.5.4. EV Charging Infrastructure Initiatives (Government EV Support Programs)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

APAC Automotive Diagnostics Market Segmentation

4.1. By Vehicle Type (In Value %) 4.1.1. Passenger Vehicles

4.1.2. Commercial Vehicles

4.1.3. Electric Vehicles

4.2. By Diagnostic Type (In Value %) 4.2.1. Onboard Diagnostics

4.2.2. Off-Board Diagnostics

4.3. By Product Type (In Value %) 4.3.1. Scanners and Testers

4.3.2. Software Solutions

4.3.3. Repair and Maintenance Tools

4.4. By Application (In Value %) 4.4.1. Preventive Maintenance

4.4.2. Repair and Service

4.4.3. Inspection and Testing

4.5. By Country (In Value %) 4.5.1. China

4.5.2. Japan

4.5.3. India

4.5.4. South Korea

4.5.5. Australia

APAC Automotive Diagnostics Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Bosch Automotive Service Solutions

5.1.2. Denso Corporation

5.1.3. Continental AG

5.1.4. Delphi Technologies

5.1.5. Snap-On Incorporated

5.1.6. Autel Intelligent Technology Corp., Ltd.

5.1.7. Siemens AG

5.1.8. Launch Tech Co., Ltd.

5.1.9. Actia Group

5.1.10. Softing AG

5.1.11. KPIT Technologies Ltd.

5.1.12. AVL List GmbH

5.1.13. Hella Gutmann Solutions

5.1.14. Mahle GmbH

5.1.15. Bertrandt AG

5.2. Cross Comparison Parameters (Number of Employees, Revenue, Global Presence, R&D Investment, Diagnostic Solution Portfolio, Market Share, Strategic Alliances, Partnerships)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

APAC Automotive Diagnostics Market Regulatory Framework 6.1. Diagnostic Tool Certification Processes

6.2. Safety and Compliance Standards for Diagnostics

6.3. Vehicle Emission Testing Guidelines

6.4. EV Diagnostic Standards

APAC Automotive Diagnostics Future Market Size (In USD Mn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

APAC Automotive Diagnostics Future Market Segmentation

8.1. By Vehicle Type (In Value %)

8.2. By Diagnostic Type (In Value %)

8.3. By Product Type (In Value %)

8.4. By Application (In Value %)

8.5. By Country (In Value %)

APAC Automotive Diagnostics Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

The initial stage of research involves identifying critical market variables, including technological advancements, government regulations, and vehicle production rates. We utilize secondary research methods, including reviewing automotive production statistics, emission control standards, and proprietary databases to establish a comprehensive market understanding.

In this phase, we analyze historical market data on automotive diagnostics, considering market penetration rates, diagnostic tool adoption across different vehicle segments, and revenue generated from key diagnostic solutions. Data from governmental reports and industry associations will be factored in to ensure the reliability of the market forecasts.

Our research hypotheses, based on historical data and market trends, are validated through interviews with industry experts and stakeholders. This allows us to refine our analysis and confirm market predictions with the help of primary insights from key players in the automotive diagnostics sector.

The final step includes synthesizing the gathered data and expert insights to produce a cohesive and comprehensive market report. A thorough review of automotive diagnostic tools, market drivers, and regulatory factors is conducted to ensure the accuracy and completeness of the final analysis.

The APAC automotive diagnostics market is valued at USD 6.5 billion, driven by the increasing integration of onboard diagnostics in modern vehicles, the rise of electric vehicles, and stringent emission regulations across major countries like China and Japan.

Key challenges include the high cost of advanced diagnostic tools and the shortage of skilled technicians capable of using these tools. Furthermore, data privacy concerns associated with connected diagnostics systems also pose a challenge for market adoption.

Major players in the APAC automotive diagnostics market include Bosch Automotive Service Solutions, Denso Corporation, Continental AG, Delphi Technologies, and Autel Intelligent Technology Corp., Ltd. These companies dominate the market due to their extensive product portfolios and global distribution networks.

The market is driven by the increasing production of vehicles across APAC, growing adoption of electric vehicles, and stringent emission and safety regulations that require the use of advanced diagnostic tools for compliance.

Trends such as the integration of cloud-based diagnostics, the growing use of predictive maintenance solutions, and the rising role of artificial intelligence (AI) in automotive diagnostics are shaping the future of the market.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.