APAC Automotive Parts and Components Market Outlook to 2030

Region:Afganistan

Author(s):Shubham

Product Code:KROD6035

Region:Afganistan

Author(s):Shubham

Product Code:KROD6035

November 2024

90

Listen to the audio summary

APAC Automotive Parts and Components Market Overview

APAC Automotive Parts and Components Market Segmentation

APAC Automotive Parts and Components Market Competitive Landscape

The APAC Automotive Parts and Components market is competitive, dominated by key international and regional players focusing on innovations in fuel efficiency, safety, and electric vehicle components. Leading companies such as Denso Corporation, Bosch Limited, Hyundai Mobis, and Aisin Seiki Co., Ltd. hold substantial market shares, supported by their extensive R&D investments and established partnerships with global and local manufacturers. This competition emphasizes the innovation-driven approach taken by key players to meet rising demands in both conventional and electric vehicle markets.

APAC Automotive Parts and Components Market Industry Analysis

Growth Drivers

Market Challenges

APAC Automotive Parts and Components Market Future Outlook

The APAC Automotive Parts and Components market is expected to experience considerable growth over the next five years, fueled by increasing demand for EVs, government policies supporting the automotive sector, and continuous advancements in automotive technologies. As major APAC countries prioritize sustainable transportation solutions and low-emission vehicles, the market will likely see a rise in demand for high-efficiency components.

Future Market Opportunities

|

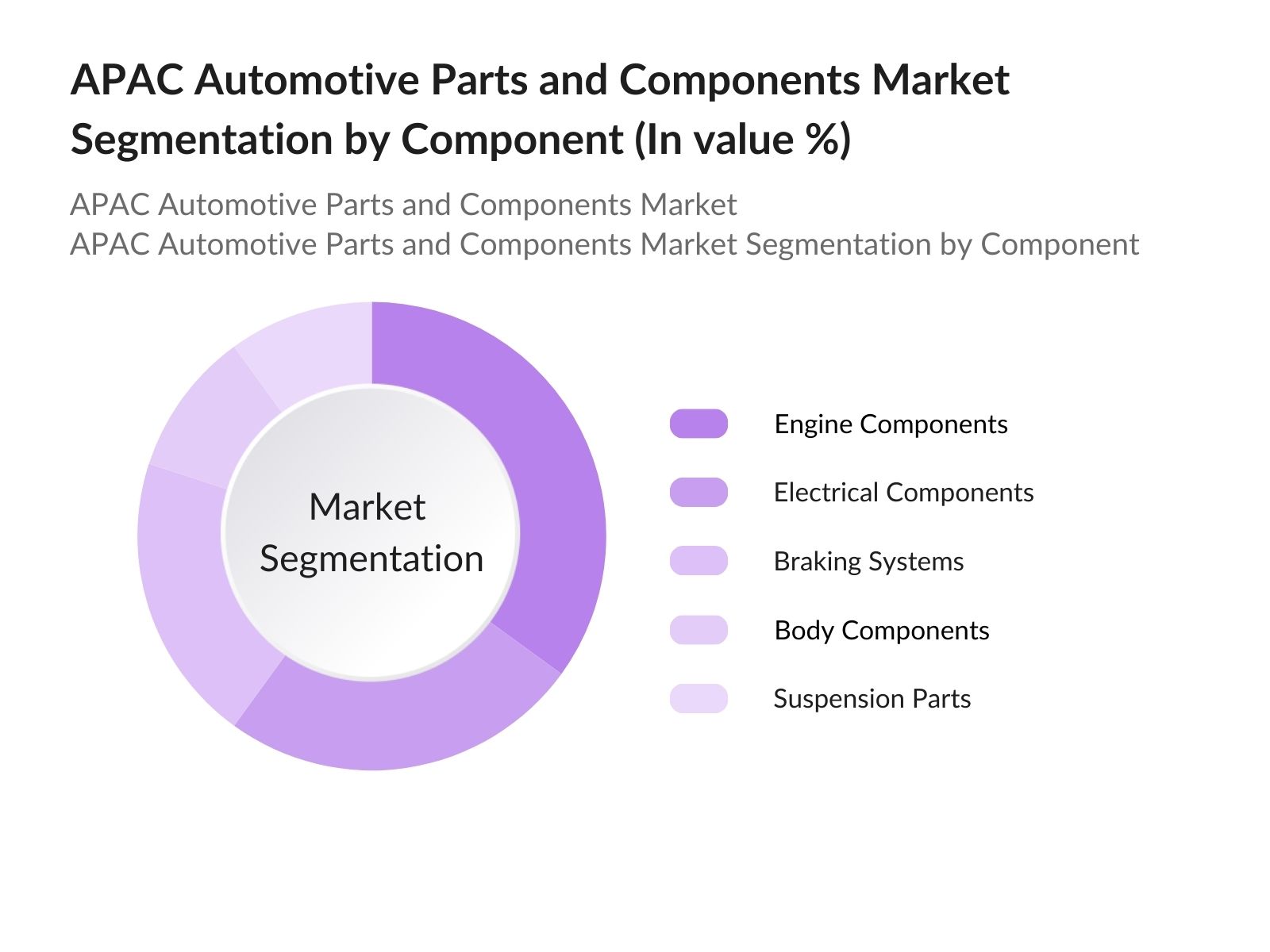

By Component Type |

Engine Components Electrical Components Suspension and Braking Components Body Components Interior Components |

|

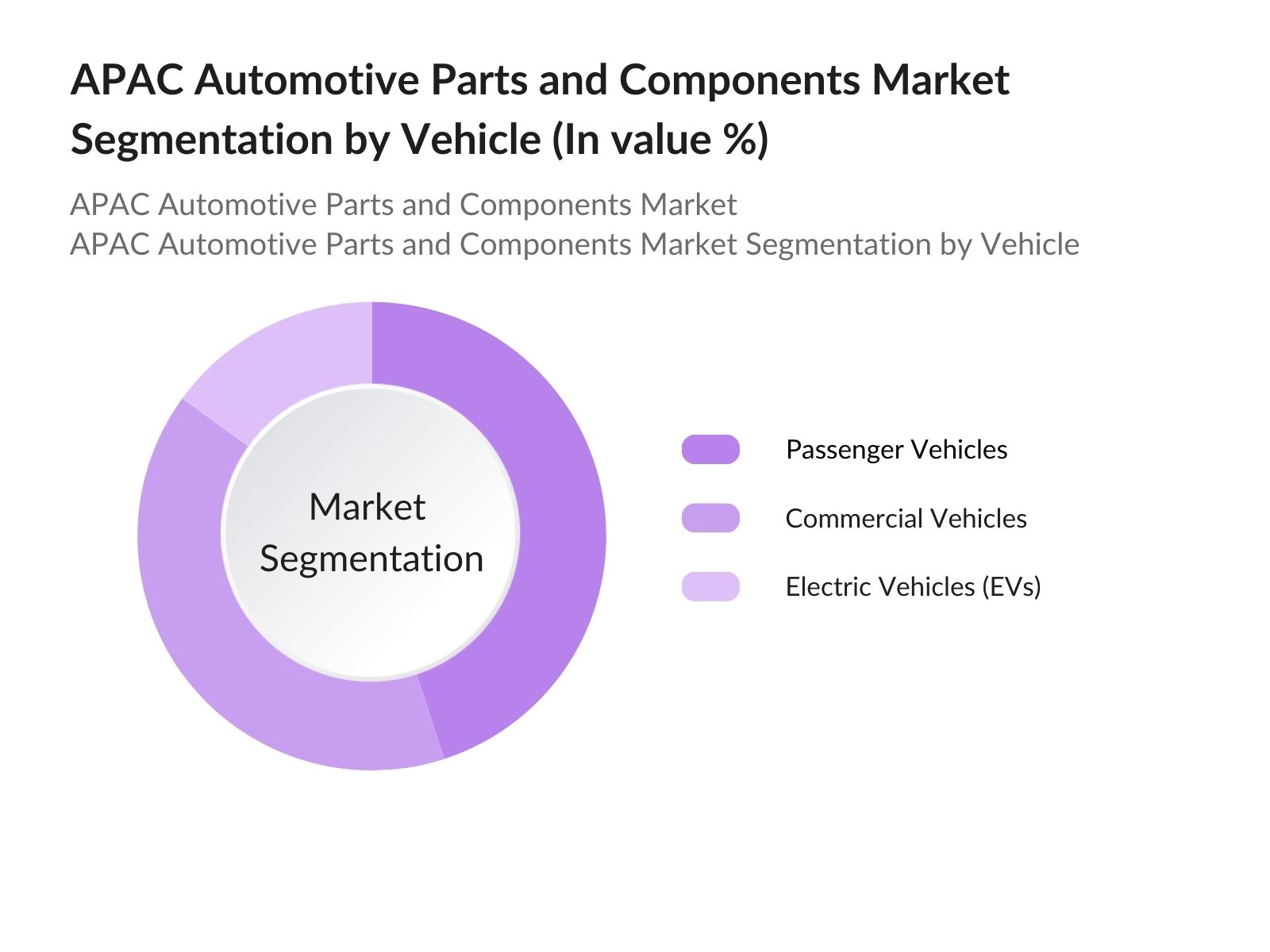

By Vehicle Type |

Passenger Vehicles Commercial Vehicles Electric Vehicles |

|

By Distribution Channel |

OEMs Aftermarket |

|

By Technology Type |

Conventional Technology Advanced Electronics Hybrid/Electric Vehicle Components |

|

By Region |

China Japan India South Korea Rest of the APAC |

Key Target Audience

Players Mentioned in the Report

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Industry Ecosystem and Stakeholders

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers [Economic Growth, Industrialization, Technological Advancements]

3.1.1. Economic and Industrial Expansion in Key APAC Countries

3.1.2. Advancements in Automotive Technologies

3.1.3. Rising Investments in Auto Component Manufacturing

3.1.4. Growth in Vehicle Production and Sales

3.2. Market Challenges [Supply Chain Vulnerabilities, Regulatory Compliance, Volatile Raw Material Prices]

3.2.1. Logistics and Distribution Complexities

3.2.2. High Cost of Compliance with Environmental Regulations

3.2.3. Dependency on Key Raw Materials

3.3. Opportunities [Electrification, Aftermarket Expansion, Digitalization in Manufacturing]

3.3.1. Growth of EV Components Market

3.3.2. Rising Demand for Aftermarket Products

3.3.3. Adoption of Advanced Digital Manufacturing Processes

3.4. Trends [Automation, Lightweight Materials, Focus on Sustainability]

3.4.1. Increased Adoption of Robotics in Manufacturing

3.4.2. Shift Towards Lightweight Composite Materials

3.4.3. Growing Focus on Eco-Friendly Components and Processes

3.5. Government Regulations [Emission Norms, Safety Standards, Localization Policies]

3.5.1. Adoption of Stringent Emission Standards

3.5.2. Implementation of Vehicle Safety Protocols

3.5.3. Localization and Manufacturing Incentives

3.6. SWOT Analysis

3.7. Porters Five Forces [Supplier Power, Buyer Power, Competitive Rivalry, Threat of Substitution, Threat of New Entrants]

3.8. Industry Ecosystem Analysis

3.9. Competition Ecosystem

4.1. By Component Type (In Value %)

4.1.1. Engine Components

4.1.2. Electrical Components

4.1.3. Suspension and Braking Components

4.1.4. Body Components

4.1.5. Interior Components

4.2. By Vehicle Type (In Value %)

4.2.1. Passenger Vehicles

4.2.2. Commercial Vehicles

4.2.3. Electric Vehicles

4.3. By Distribution Channel (In Value %)

4.3.1. OEMs

4.3.2. Aftermarket

4.4. By Technology Type (In Value %)

4.4.1. Conventional Technology

4.4.2. Advanced Electronics

4.4.3. Hybrid/Electric Vehicle Components

4.5. By Region (In Value %)

4.5.1. China

4.5.2. Japan

4.5.3. India

4.5.4. South Korea

4.5.5. ASEAN Countries

5.1. Detailed Profiles of Major Companies

5.1.1. Denso Corporation

5.1.2. Bosch Limited

5.1.3. Hyundai Mobis

5.1.4. Aisin Seiki Co., Ltd.

5.1.5. Continental AG

5.1.6. Magna International Inc.

5.1.7. Yazaki Corporation

5.1.8. Faurecia SA

5.1.9. Valeo SA

5.1.10. Toyota Boshoku Corporation

5.1.11. ZF Friedrichshafen AG

5.1.12. Panasonic Automotive Systems

5.1.13. Sumitomo Electric Industries, Ltd.

5.1.14. Mitsubishi Electric Corporation

5.1.15. Lear Corporation

5.2. Cross Comparison Parameters [Revenue, Market Share, Product Portfolio, Innovation Index, Manufacturing Facilities, Regional Presence, Strategic Partnerships, Workforce Size]

5.3. Market Share Analysis

5.4. Strategic Initiatives and Partnerships

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Research and Development Focus

5.8. Product Launches and Innovations

6.1. Emission Control Standards

6.2. Automotive Safety Regulations

6.3. Import and Export Regulations

6.4. Industry Certification Standards

7.1. Future Market Size Projections

7.2. Key Factors Influencing Future Growth

8.1. By Component Type (In Value %)

8.2. By Vehicle Type (In Value %)

8.3. By Distribution Channel (In Value %)

8.4. By Technology Type (In Value %)

8.5. By Region (In Value %)

9.1. Market Expansion Strategies

9.2. Risk Mitigation Strategies

9.3. White Space Opportunities

9.4. Regional Investment Prospects

Disclaimer Contact Us

The research process initiates with identifying critical factors impacting the APAC Automotive Parts and Components market. Comprehensive desk research is conducted using industry databases and proprietary sources, mapping stakeholder influence on market trends.

Historical data on market performance, production volume, and component adoption is analyzed to assess growth trends. This data-driven analysis aids in segmenting the market by component type and vehicle category.

Through expert interviews and consultations, market assumptions are validated. These insights from industry experts provide further clarity on market trends, opportunities, and challenges.

The final phase consolidates data from various sources, offering a comprehensive overview of the market. A synthesis of findings ensures a validated analysis, grounded in robust methodology.

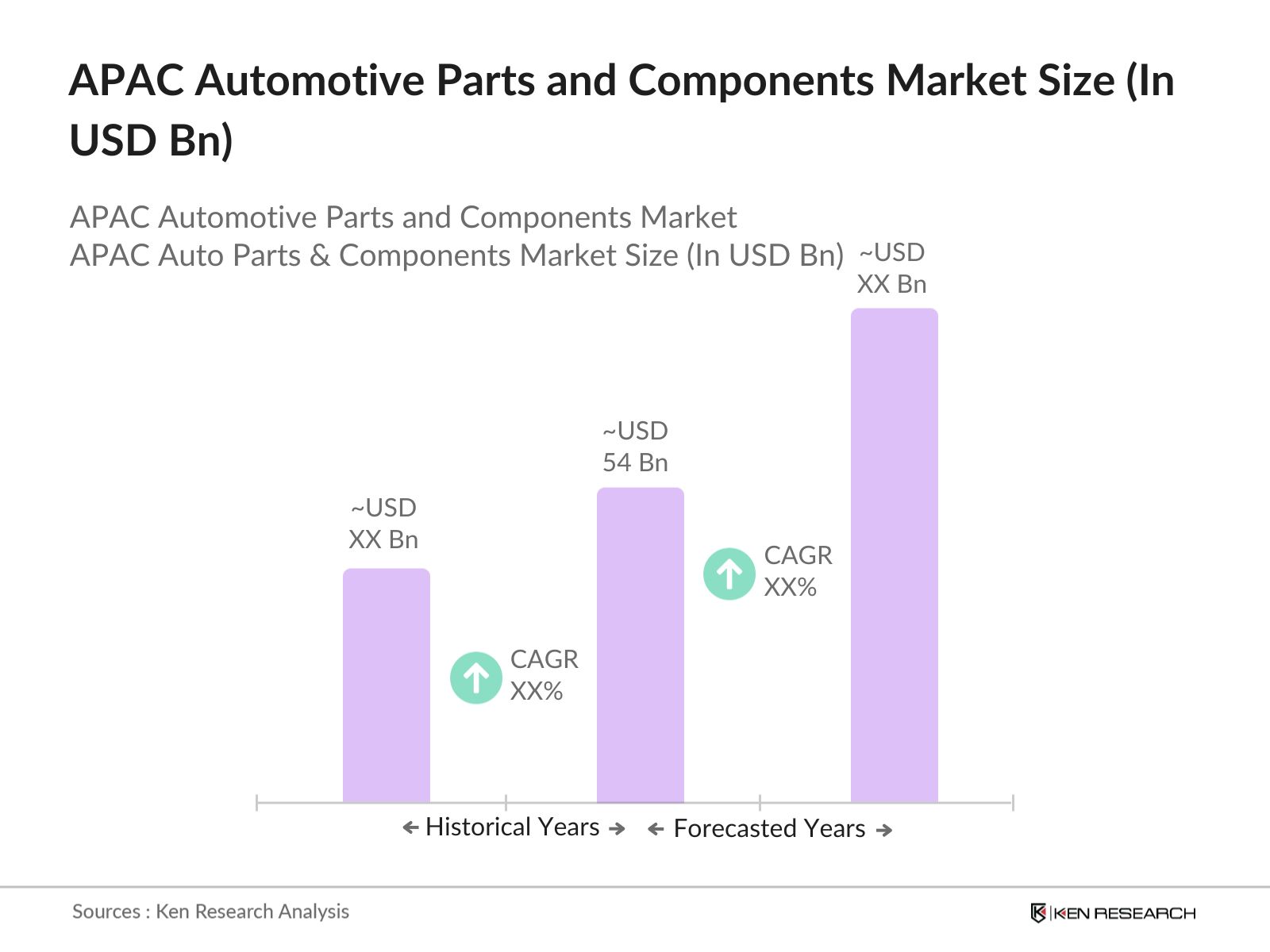

The APAC Automotive Parts and Components market was valued at USD 54 billion, with growth driven by demand for automotive and EV components across the region.

Key growth drivers in the APAC Automotive Parts and Components market include increasing EV demand, government incentives, and technological advancements in automotive components.

Major companies in the APAC Automotive Parts and Components market include Denso Corporation, Bosch Limited, Hyundai Mobis, Aisin Seiki Co., Ltd., and Continental AG, known for their R&D and partnerships with OEMs.

Challenges in the APAC Automotive Parts and Components market include high production costs for advanced components and supply chain constraints impacting raw material availability.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.