APAC Farm Equipment Market Outlook to 2030

Region:Asia

Author(s):Shubham Kashyap

Product Code:KROD8078

December 2024

94

About the Report

APAC Farm Equipment Market Overview

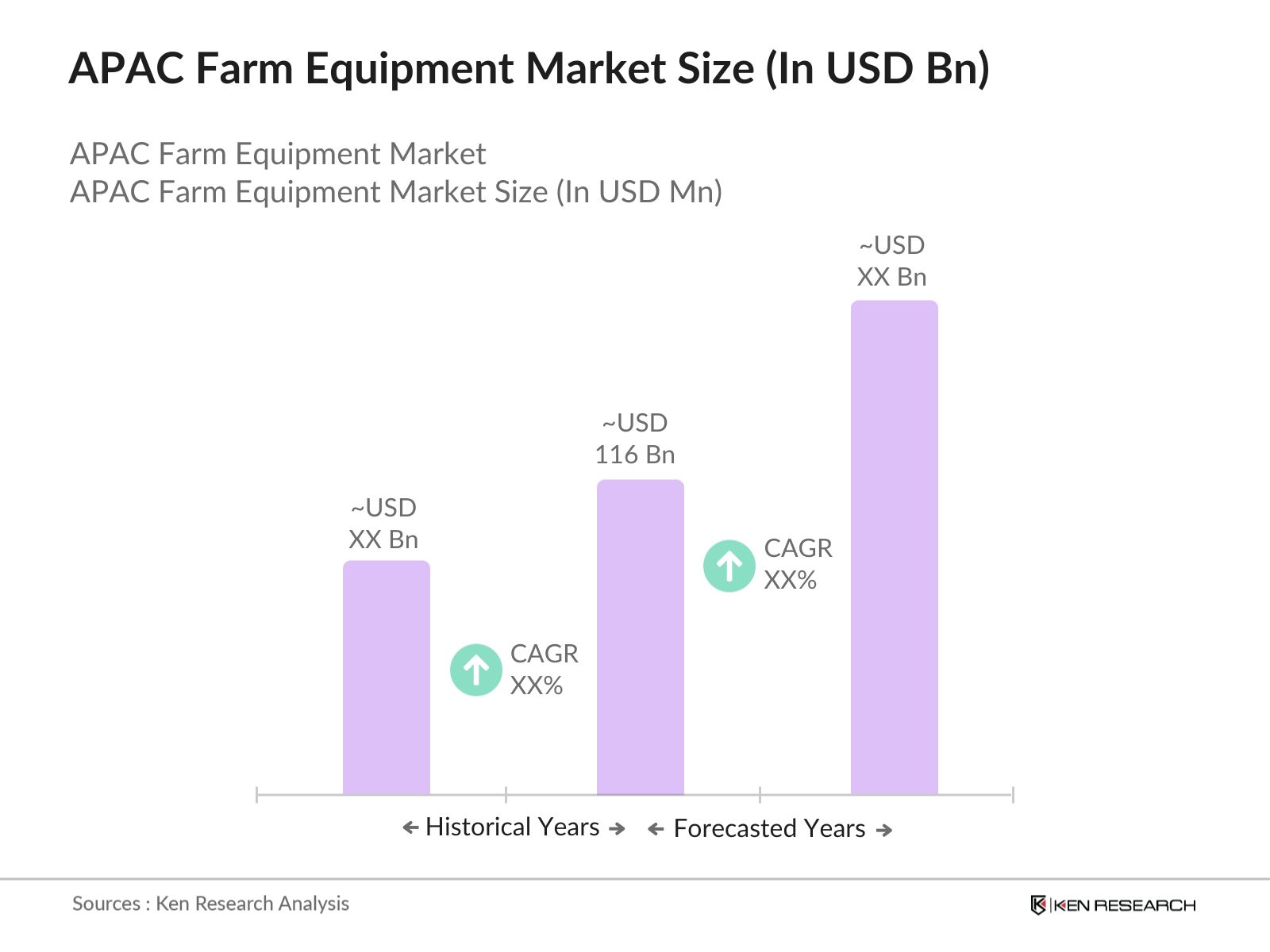

- The APAC farm equipment market is experiencing substantial growth, valued at USD 116 billion. The market expansion is driven by a heightened need for agricultural mechanization and the adoption of advanced farming technologies. As urban populations rise, so does the demand for food, requiring efficient farm operations that maximize productivity. Government initiatives across APAC countries aim to boost agricultural output by subsidizing farm equipment, fostering a robust demand for tractors, harvesters, and precision agriculture tools.

- China and India lead the APAC farm equipment market due to their extensive agricultural sectors. Chinas investments in high-tech mechanization and Indias substantial rural workforce relying on agriculture make them dominant markets. Additionally, Japan, with its focus on smart farming and automation, further enhances the regional market landscape. These nations benefit from strong government support, technological advancements, and established distribution networks for agricultural machinery.

- Several APAC governments have introduced stringent emission standards for farm machinery, aiming to reduce carbon emissions from diesel-powered equipment. Chinas "Stage IV" standards require 30% lower emissions, impacting equipment design and market availability. Such policies are driving demand for environmentally compliant machinery, encouraging manufacturers to innovate and align with regulatory compliance standards across the region.

APAC Farm Equipment Market Segmentation

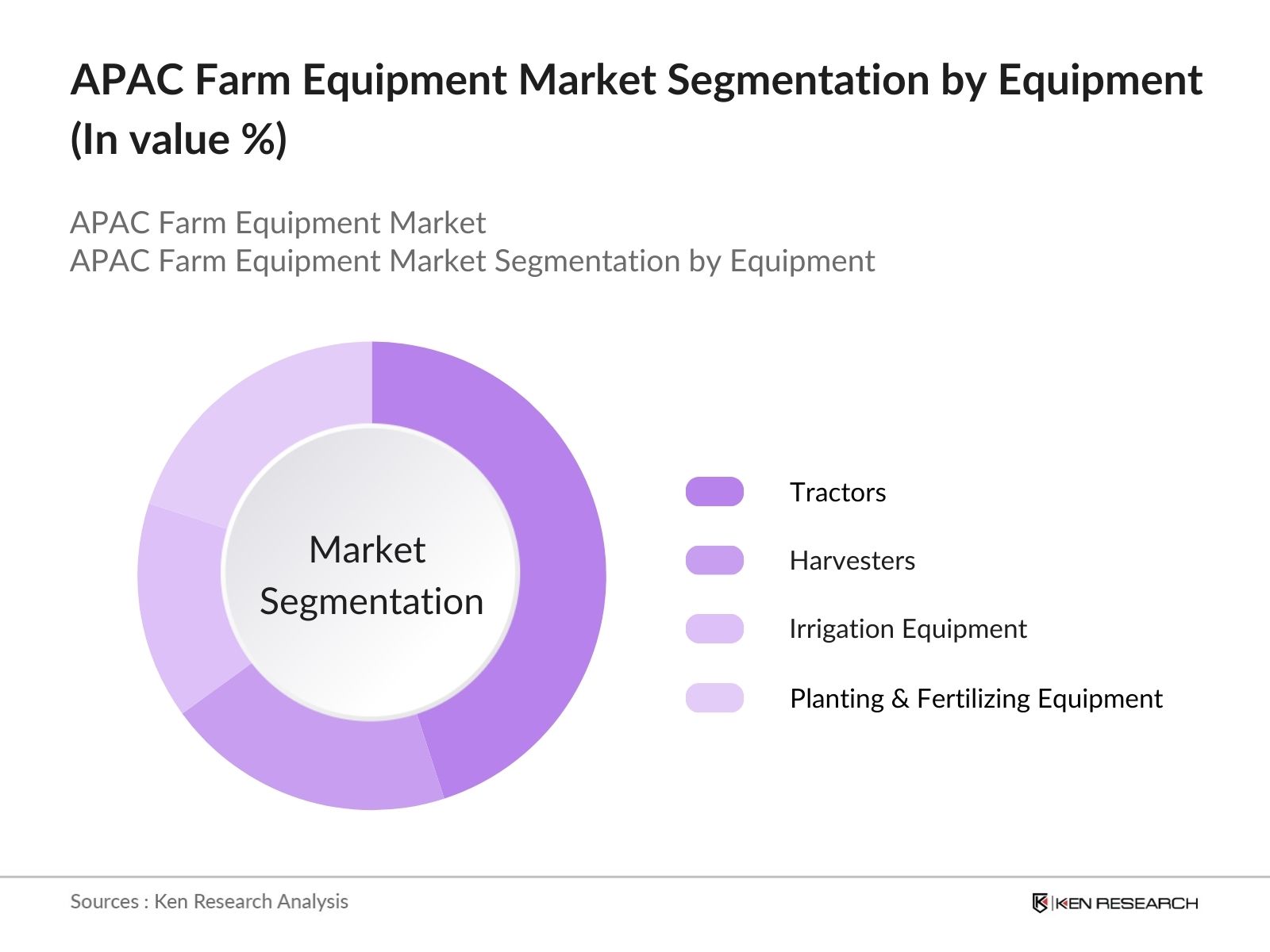

- By Equipment Type: The market is segmented by equipment type into tractors, harvesters, irrigation equipment, and planting & fertilizing equipment. Tractors hold a dominant share due to their versatility across various farming activities. In large-scale farming regions in China and India, tractors serve as essential machinery, offering high power and efficiency. This demand is bolstered by government support programs and availability of subsidies, which make tractors accessible to a broader range of farmers.

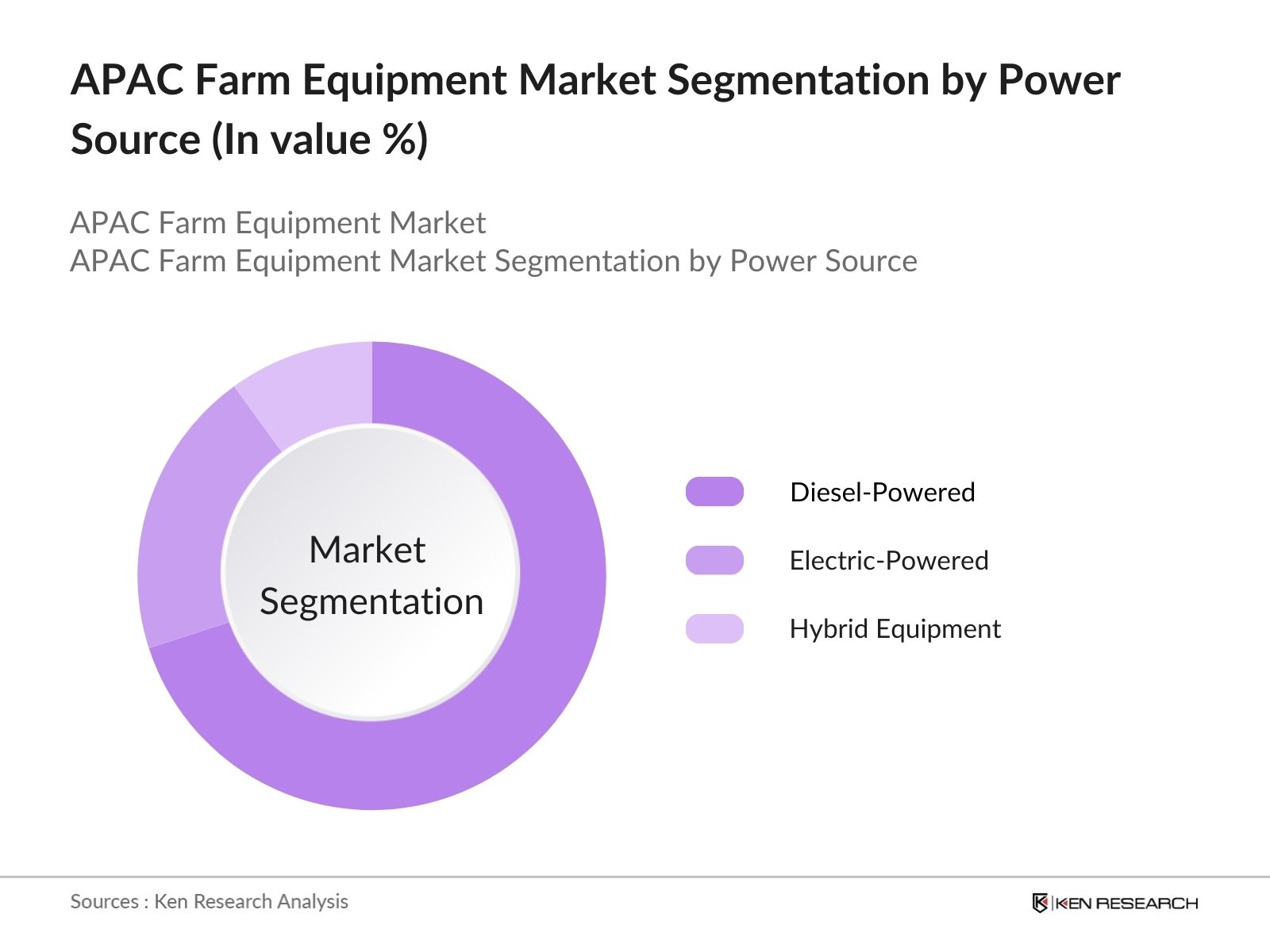

- By Power Source: The market is also segmented by power source into diesel-powered, electric-powered, and hybrid equipment. Diesel-powered equipment remains the most popular choice due to its reliability and availability in rural regions. Diesel-powered machinery, especially tractors and harvesters, continues to dominate due to the minimal infrastructure required for its operation and the high cost associated with electric-powered options in less developed areas of APAC.

APAC Farm Equipment Market Competitive Landscape

The APAC farm equipment market is highly competitive, with prominent players investing in product innovation and partnerships to strengthen their foothold. Key companies such as John Deere, CNH Industrial, and Kubota Corporation have a solid regional presence, underpinned by broad product portfolios and extensive dealer networks. Meanwhile, local firms in China and Japan capitalize on government partnerships and collaborative efforts to cater to specific market needs.

APAC Farm Equipment Market Analysis

Growth Drivers

- Rising Agricultural Mechanization: The adoption of mechanized farming in APAC countries has seen significant progress, particularly in emerging markets like India and Vietnam, where mechanization adoption rates have reached 45% and 40% respectively. The cost-effectiveness of mechanized farming is underscored by the increase in crop yield and reduction in manual labour, enabling an annual cost saving of around 50 tons of rice yield per 1,000 hectares. This is a vital factor for food security, particularly in densely populated regions, supported by policies incentivizing machinery use.

- Technological Advancements in Precision Agriculture: Technological advancements in APACs precision agriculture sector have enabled farmers to use resources more efficiently. In Japan, precision farming technologies have reduced water usage in rice paddies by up to 30,000 liters per hectare per growing season. Similarly, GPS-guided equipment in China is contributing to fertilizer savings of approximately 25 kg per hectare. These advancements, along with government incentives, have fostered a fertile environment for precision agriculture, increasing the demand for farm equipment that supports such technologies across APAC.

- Demand for High-Efficiency Equipment: High-efficiency farming equipment is increasingly sought after in APAC, especially in densely populated nations like China and India, where food production is critical. Efficient equipment like high-capacity harvesters has improved crop yield by an additional 10 tons per hectare, enhancing overall productivity and profitability. This equipment also reduces fuel consumption substantially per hectare, underscoring the environmental and cost benefits. The return on investment for such equipment is significant, with farmers achieving break-even within five years of usage due to yield increases and labor cost reductions.

Market Challenges

- High Cost of Advanced Equipment: The high cost of advanced farm equipment presents challenges for small and medium-sized farms in APAC. Equipment such as high-tech tractors is financially out of reach for many small-scale farmers who make up a significant portion of the regions agriculture sector. Even with government subsidies, affordability remains limited, restricting the ability of farmers to invest in technology that could boost productivity and operational efficiency. This affordability gap continues to be a major barrier to mechanization in the region.

- Availability of Skilled Labor: The shortage of skilled operators for advanced farm machinery is a considerable challenge in APAC. Many rural farm operators lack formal training in machinery usage, leading to under-utilization of available equipment. Governments across the region are working to bridge this gap through training programs aimed at building operator skills, though these efforts only address a portion of the demand. The skill gap limits the effective mechanization of agriculture, underscoring the need for comprehensive training initiatives to support equipment usage across the sector.

APAC Farm Equipment Market Future Outlook

The APAC farm equipment market is expected to see steady growth through 2028, supported by technological innovations, rising demand for sustainable farming, and governmental support for agricultural development. As economies focus on enhancing food security and modernizing agriculture, the demand for efficient farm equipment solutions will increase, especially in emerging economies across Southeast Asia and South Asia. In addition, advancements in autonomous machinery and precision farming tools are anticipated to drive future market growth.

Future Market Opportunities

- Expansion into Emerging Markets: Emerging markets in Southeast Asia, such as Myanmar and Cambodia, present significant potential for farm equipment expansion. With agricultural populations exceeding 15 million in these regions, the demand for mechanization is expected to grow as economies develop. Myanmar's agricultural penetration rate is relatively low, indicating considerable growth potential. Expanding distribution channels and addressing infrastructure challenges in these emerging markets will likely facilitate robust growth opportunities for the farm equipment market.

- Rental Equipment Demand: The rental market for farm equipment in the Asia-Pacific region is expanding rapidly, with demand increasing significantly in recent years. In India, a substantial portion of small farmers prefers renting equipment due to cost constraints, establishing a strong rental-to-purchase ratio. Rental services allow farmers access to advanced machinery without high upfront costs, driving increased mechanization adoption among smallholders and fueling growth within the APAC farm equipment market.

Scope of the Report

|

By Product Type |

Tractors, Harvesting Equipment Soil Preparation & Cultivation Equipment Irrigation & Crop Processing Equipment Others (Threshers, Sprayers) |

|

By Application |

Land Preparation Planting Crop Protection Irrigation Harvesting |

|

By Sales Channel |

Direct Sales Distributors & Dealers Online Retail |

|

By Power Output |

Low Power (Less than 40 HP) Medium Power (40100 HP) High Power (Above 100 HP) |

|

By Region |

China India Japan Southeast Asia Rest of APAC |

Products

Key Target Audience

Investors and Venture Capitalist Firms

Banks and Financial Institutions

Government and Regulatory Bodies (Ministry of Agriculture, APAC Development Bank)

Farm Equipment Distributors

Large-Scale Farmers and Agricultural Cooperatives

Technology Providers for Precision Farming

Farm Equipment Retailers

Agricultural Financing Institutions

Companies

Players Mentioned in the Report

John Deere

CNH Industrial

Kubota Corporation

Mahindra & Mahindra

Yanmar Co., Ltd.

CLAAS Group

Iseki & Co., Ltd.

Escorts Group

TAFE

SDF Group

Kverneland Group

Daedong Industrial

Massey Ferguson

SAME Deutz-Fahr

AGCO Corporation

Table of Contents

01 APAC Farm Equipment Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

02 APAC Farm Equipment Market Size (In USD Mn)

2.1 Historical Market Size

2.2 Year-on-Year Growth Analysis

2.3 Key Market Developments and Milestones

03 APAC Farm Equipment Market Analysis

3.1 Growth Drivers

3.1.1 Mechanization in Agriculture (Adoption Rate, Cost-Effectiveness)

3.1.2 Technological Advancements in Precision Agriculture

3.1.3 Government Subsidies & Policies (Policy Impact, Subsidy Levels)

3.1.4 Demand for High-Efficiency Equipment (Efficiency Metrics, ROI)

3.2 Market Challenges

3.2.1 High Cost of Advanced Equipment (Affordability Index)

3.2.2 Availability of Skilled Labor (Skill Gap, Training Programs)

3.2.3 Limited Financing Options (Loan Accessibility, Interest Rates)

3.3 Opportunities

3.3.1 Expansion into Emerging Markets (Market Penetration, Population Growth)

3.3.2 Rental Equipment Demand (Rental vs. Purchase Ratio)

3.3.3 Smart Farming and IoT Integration (IoT Readiness, Connectivity)

3.4 Trends

3.4.1 Increasing Adoption of Autonomous Equipment (Autonomy Level, Cost Benefits)

3.4.2 Rising Popularity of Electric Farm Equipment (Fuel Alternatives, Environmental Impact)

3.4.3 Digital Platforms for Equipment Financing (Digital Financing Penetration)

3.5 Government Regulations

3.5.1 Emission Standards (Emission Types, Regulatory Compliance)

3.5.2 Import Tariffs and Export Policies

3.5.3 Agricultural Mechanization Policies

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem

3.8 Porters Five Forces Analysis

3.9 Competitive Landscape

04 APAC Farm Equipment Market Segmentation

4.1 By Product Type (In Value %)

4.1.1 Tractors

4.1.2 Harvesting Equipment

4.1.3 Soil Preparation & Cultivation Equipment

4.1.4 Irrigation & Crop Processing Equipment

4.1.5 Others (Threshers, Sprayers)

4.2 By Application (In Value %)

4.2.1 Land Preparation

4.2.2 Planting

4.2.3 Crop Protection

4.2.4 Irrigation

4.2.5 Harvesting

4.3 By Sales Channel (In Value %)

4.3.1 Direct Sales

4.3.2 Distributors & Dealers

4.3.3 Online Retail

4.4 By Power Output (In Value %)

4.4.1 Low Power (Less than 40 HP)

4.4.2 Medium Power (40100 HP)

4.4.3 High Power (Above 100 HP)

4.5 By Region (In Value %)

4.5.1 China

4.5.2 India

4.5.3 Japan

4.5.4 Southeast Asia

4.5.5 Rest of APAC

05 APAC Farm Equipment Market Competitive Analysis

5.1 Detailed Profiles of Major Competitors

5.1.1 Kubota Corporation

5.1.2 Mahindra & Mahindra Ltd.

5.1.3 Deere & Company

5.1.4 CNH Industrial

5.1.5 Yanmar Holdings Co., Ltd.

5.1.6 AGCO Corporation

5.1.7 CLAAS KGaA mbH

5.1.8 Iseki & Co., Ltd.

5.1.9 Escorts Ltd.

5.1.10 Same Deutz-Fahr Group

5.1.11 Zetor Tractors A.S.

5.1.12 Horsch Maschinen GmbH

5.1.13 TAFE (Tractors and Farm Equipment Limited)

5.1.14 Massey Ferguson

5.1.15 Valmont Industries, Inc.

5.2 Cross-Comparison Parameters (Product Range, Market Reach, Revenue, R&D Investment, Pricing Strategy, Sustainability Initiatives, Technological Innovations, Customer Base)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital and Private Equity Funding

5.8 Government Grants

06 APAC Farm Equipment Market Regulatory Framework

6.1 Environmental Standards and Compliance

6.2 Certification Requirements for Equipment

6.3 Government Subsidy Programs

6.4 Import and Export Policies

07 APAC Farm Equipment Future Market Size (In USD Mn)

7.1 Future Market Size Projections

7.2 Key Drivers of Future Market Growth

08 APAC Farm Equipment Future Market Segmentation

8.1 By Product Type (In Value %)

8.2 By Application (In Value %)

8.3 By Sales Channel (In Value %)

8.4 By Power Output (In Value %)

8.5 By Region (In Value %)

09 APAC Farm Equipment Market Analysts Recommendations

9.1 Total Addressable Market (TAM) / Serviceable Available Market (SAM) / Serviceable Obtainable Market (SOM) Analysis

9.2 Customer Segmentation Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

In the first phase, we map the APAC Farm Equipment Market ecosystem, covering all major stakeholders, including manufacturers, distributors, and policymakers. This step involves comprehensive desk research and data analysis to identify critical market drivers and constraints.

Step 2: Market Analysis and Construction

Historical data on equipment usage, revenue generation, and adoption patterns is compiled. Market analysis involves examining the impact of factors like mechanization and subsidies to understand current and future trends across key APAC regions.

Step 3: Hypothesis Validation and Expert Consultation

Our team conducts consultations with industry experts and executives across the APAC region to validate market hypotheses. This step enhances data reliability and offers valuable insights into market dynamics, supported by firsthand information from stakeholders.

Step 4: Research Synthesis and Final Output

This phase consolidates data from primary and secondary research, refining findings to produce a thorough market report. Final insights include projections and recommendations, providing an actionable roadmap for market participants.

Frequently Asked Questions

01. How big is the APAC Farm Equipment Market?

The APAC farm equipment market is valued at USD 116 billion, driven by increasing mechanization and government support for the agricultural sector.

02. What are the main challenges in the APAC Farm Equipment Market?

Key challenges in the APAC farm equipment market include the high initial cost of equipment, skill gaps among users, and limited infrastructure for maintenance in rural regions, affecting market accessibility.

03. Who are the major players in the APAC Farm Equipment Market?

Leading players in the APAC farm equipment market include John Deere, CNH Industrial, Kubota Corporation, Mahindra & Mahindra, and Yanmar Co., Ltd., recognized for their extensive product offerings and market reach.

04. What drives the growth of the APAC Farm Equipment Market?

The APAC farm equipment market is primarily driven by rising agricultural mechanization, governmental subsidies, and the adoption of advanced technology in farming practices across APAC.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.