APAC Frozen Food Market Outlook to 2030

Region:Asia

Author(s):Shubham Kashyap

Product Code:KROD3808

Region:Asia

Author(s):Shubham Kashyap

Product Code:KROD3808

November 2024

100

The APAC Frozen Food market is highly competitive, with both international and regional players competing for market share through product innovation and expansion of distribution channels. Leading companies such as Nestl, McCain Foods, and Ajinomoto dominate the market with their extensive portfolios of frozen food products. These companies are continually investing in product development to cater to changing consumer preferences and expanding their presence in emerging markets across APAC.

|

Company Name |

Establishment Year |

Headquarters |

Key Frozen Food Products |

Revenue (2023) |

R&D Investment |

Key Markets |

Global Presence |

|

Nestl |

1866 |

Vevey, Switzerland |

|||||

|

McCain Foods |

1957 |

Florenceville, Canada |

|||||

|

Ajinomoto |

1909 |

Tokyo, Japan |

|||||

|

Simplot |

1929 |

Boise, USA |

|||||

|

Nichirei Foods |

1942 |

Tokyo, Japan |

Growth Drivers

Market Challenges

The APAC frozen food market is expected to continue growing over the next five years, driven by rising urbanization, growing e-commerce penetration, and increasing consumer preference for convenience. As more consumers across the region shift towards healthier eating habits, there will be an increasing demand for organic, plant-based, and low-calorie frozen food options. Additionally, advancements in freezing technology and cold storage infrastructure are expected to further support the markets growth.

Future Market Opportunities

|

By Product Type |

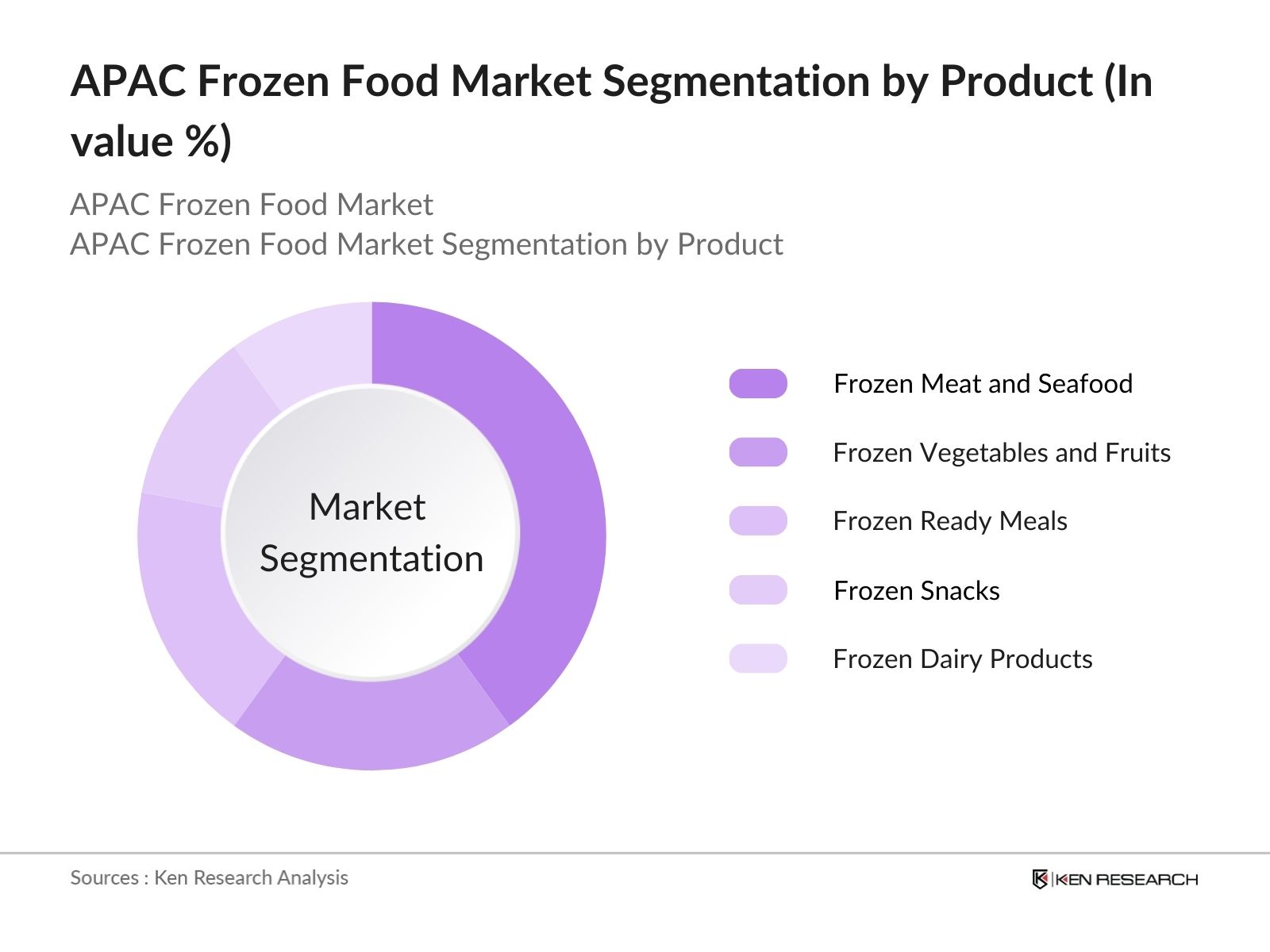

Frozen Vegetables and Fruits Frozen Meat and Seafood Frozen Ready Meals Frozen Snacks Frozen Dairy Products |

|

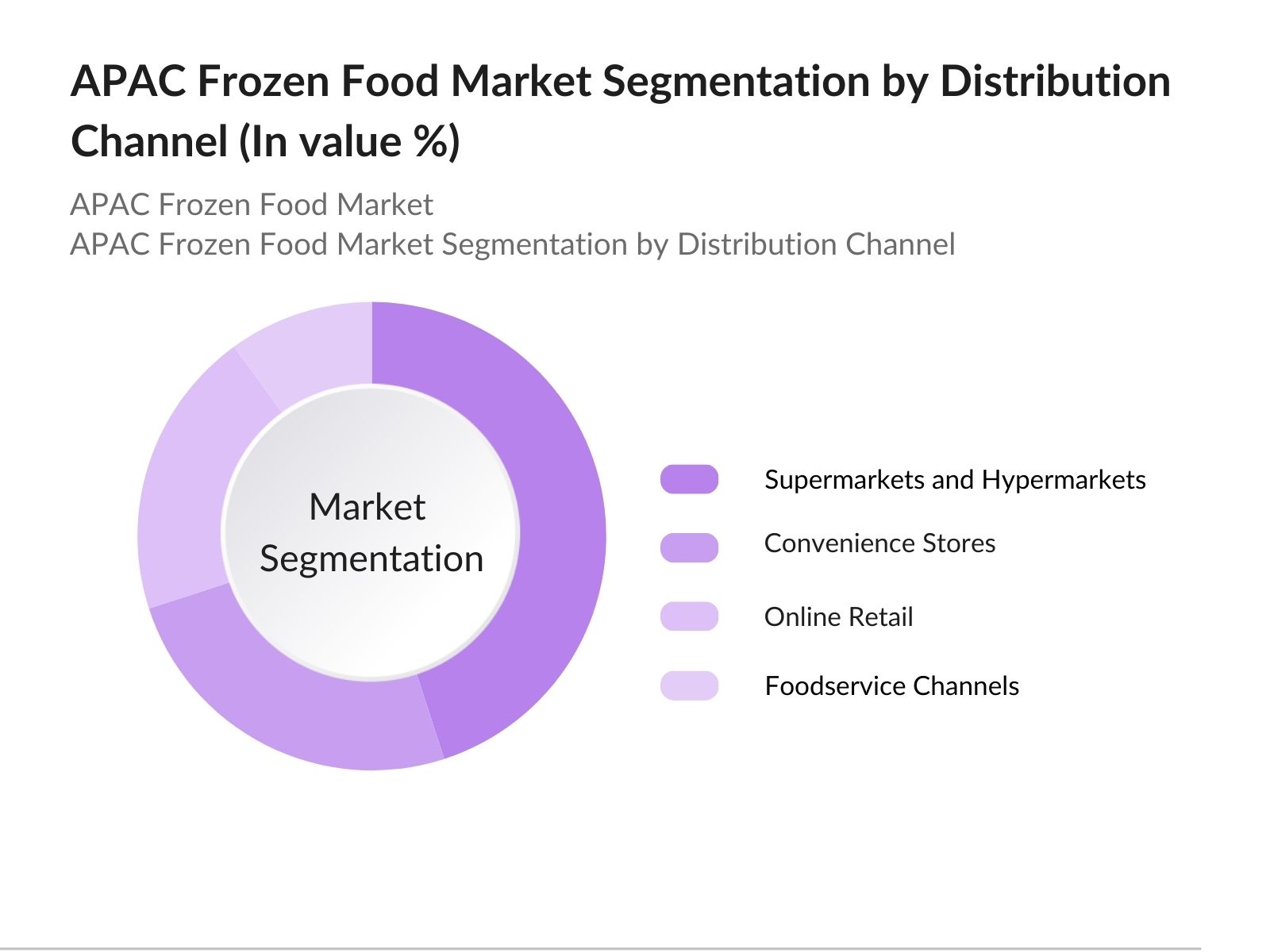

By Distribution Channel |

Supermarkets and Hypermarkets Convenience Stores Online Retail Foodservice Channels |

|

By Consumer Type |

Retail Consumers Institutional Buyers B2B Buyers |

|

By Freezing Technology |

Individual Quick Freezing (IQF) Blast Freezing Cryogenic Freezing Other Technologies |

|

By Region |

China Japan South Korea Indonesia Rest of APAC |

1.1 Definition and Scope

1.2 Market Taxonomy (Frozen Foods, Supply Chain, Logistics, Cold Storage)

1.3 Market Growth Rate (Market Demand, Consumption, Urbanization)

1.4 Market Segmentation Overview

2.1 Historical Market Size (Consumer Preferences, Retail Growth)

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones (Distribution Expansion, E-Commerce Penetration)

3.1 Growth Drivers

3.1.1 Urbanization and Changing Lifestyles

3.1.2 Expansion of Retail and E-commerce

3.1.3 Technological Advancements in Freezing and Cold Chain Logistics

3.1.4 Increasing Health-Conscious Consumer Preferences

3.2 Market Challenges

3.2.1 Cold Chain Infrastructure Gaps

3.2.2 Regulatory and Trade Barriers

3.2.3 Consumer Perception of Frozen vs. Fresh Food

3.3 Opportunities

3.3.1 Growing Demand for Premium and Organic Frozen Food

3.3.2 Emerging Markets (Indonesia, Vietnam, Thailand)

3.3.3 Innovations in Packaging and Sustainable Practices

3.4 Trends

3.4.1 Rising Demand for Plant-Based Frozen Foods

3.4.2 Growth in Ready-to-Eat Meal Segment

3.4.3 Health & Wellness-Driven Product Development

3.5 Government Regulations

3.5.1 Cold Storage and Food Safety Standards

3.5.2 Import and Export Regulations for Frozen Foods

3.5.3 Public-Private Partnerships for Cold Chain Infrastructure Development

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem

3.8 Porters Five Forces Analysis (Suppliers, Buyers, Competition, New Entrants, Substitutes)

3.9 Competitive Landscape

4.1 By Product Type (In Value %)

4.1.1 Frozen Vegetables and Fruits

4.1.2 Frozen Meat and Seafood

4.1.3 Frozen Ready Meals

4.1.4 Frozen Snacks

4.1.5 Frozen Dairy Products

4.2 By Distribution Channel (In Value %)

4.2.1 Supermarkets and Hypermarkets

4.2.2 Convenience Stores

4.2.3 Online Retail

4.2.4 Foodservice Channels

4.3 By Consumer Type (In Value %)

4.3.1 Retail Consumers

4.3.2 Institutional Buyers (Hotels, Restaurants, Cafes)

4.3.3 B2B Buyers (Foodservice Distributors, Manufacturers)

4.4 By Freezing Technology (In Value %)

4.4.1 Individual Quick Freezing (IQF)

4.4.2 Blast Freezing

4.4.3 Cryogenic Freezing

4.4.4 Other Technologies

4.5 By Region (In Value %)

4.5.1 China

4.5.2 Japan

4.5.3 South Korea

4.5.4 Indonesia

4.5.5 Rest of APAC

5.1 Detailed Profiles of Major Competitors

5.1.1 Nestl

5.1.2 McCain Foods

5.1.3 Ajinomoto Co., Inc.

5.1.4 Simplot Foods

5.1.5 Nichirei Foods

5.1.6 CPF Group (Charoen Pokphand Foods)

5.1.7 Conagra Brands, Inc.

5.1.8 General Mills

5.1.9 Greenyard

5.1.10 Heinz Frozen Foods

5.1.11 Kraft Heinz

5.1.12 Nomad Foods

5.1.13 FRoSTA AG

5.1.14 JBS Foods International

5.1.15 Tyson Foods

5.2 Cross Comparison Parameters (Revenue, Headquarters, Market Share, Product Portfolio, Innovation Focus, Freezing Technology Used, Geographic Reach, Expansion Strategies)

5.3 Market Share Analysis (Top 10 Competitors)

5.4 Strategic Initiatives (New Product Launches, Partnerships, Market Expansion)

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding in Frozen Food Industry

5.8 Government Grants for Cold Chain Infrastructure

5.9 Private Equity Investments

6.1 Cold Chain Storage Standards and Food Safety Regulations

6.2 Compliance Requirements for Imported Frozen Food Products

6.3 Certification Processes for Frozen Food Exports

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth (Changing Dietary Preferences, Retail Expansion, Health-Conscious Products)

8.1 By Product Type (In Value %)

8.2 By Distribution Channel (In Value %)

8.3 By Consumer Type (In Value %)

8.4 By Freezing Technology (In Value %)

8.5 By Region (In Value %)

9.1 TAM/SAM/SOM Analysis

9.2 Market Penetration Strategies

9.3 White Space Opportunity Analysis

9.4 Consumer Behavior Trends in APAC

The initial phase involves constructing a detailed ecosystem of stakeholders within the APAC Frozen Food Market. This step utilizes a combination of secondary research from proprietary databases and primary interviews to gather comprehensive data on market drivers, supply chains, and distribution networks.

We gather and analyze historical market data, identifying key trends in frozen food consumption, penetration of modern retail, and cold chain infrastructure development. This step also includes the analysis of retail growth in urban and semi-urban regions across APAC.

Market hypotheses will be validated through consultations with key players in the frozen food industry. These interviews with manufacturers, retailers, and logistic providers offer insights into sales trends, production capacities, and market challenges, ensuring a reliable data set for further analysis.

In the final phase, comprehensive data from industry sources will be synthesized to produce actionable insights. The data will be cross-verified with market participants to ensure accuracy in reporting. The final output will include detailed market forecasts, key player strategies, and potential opportunities for investment.

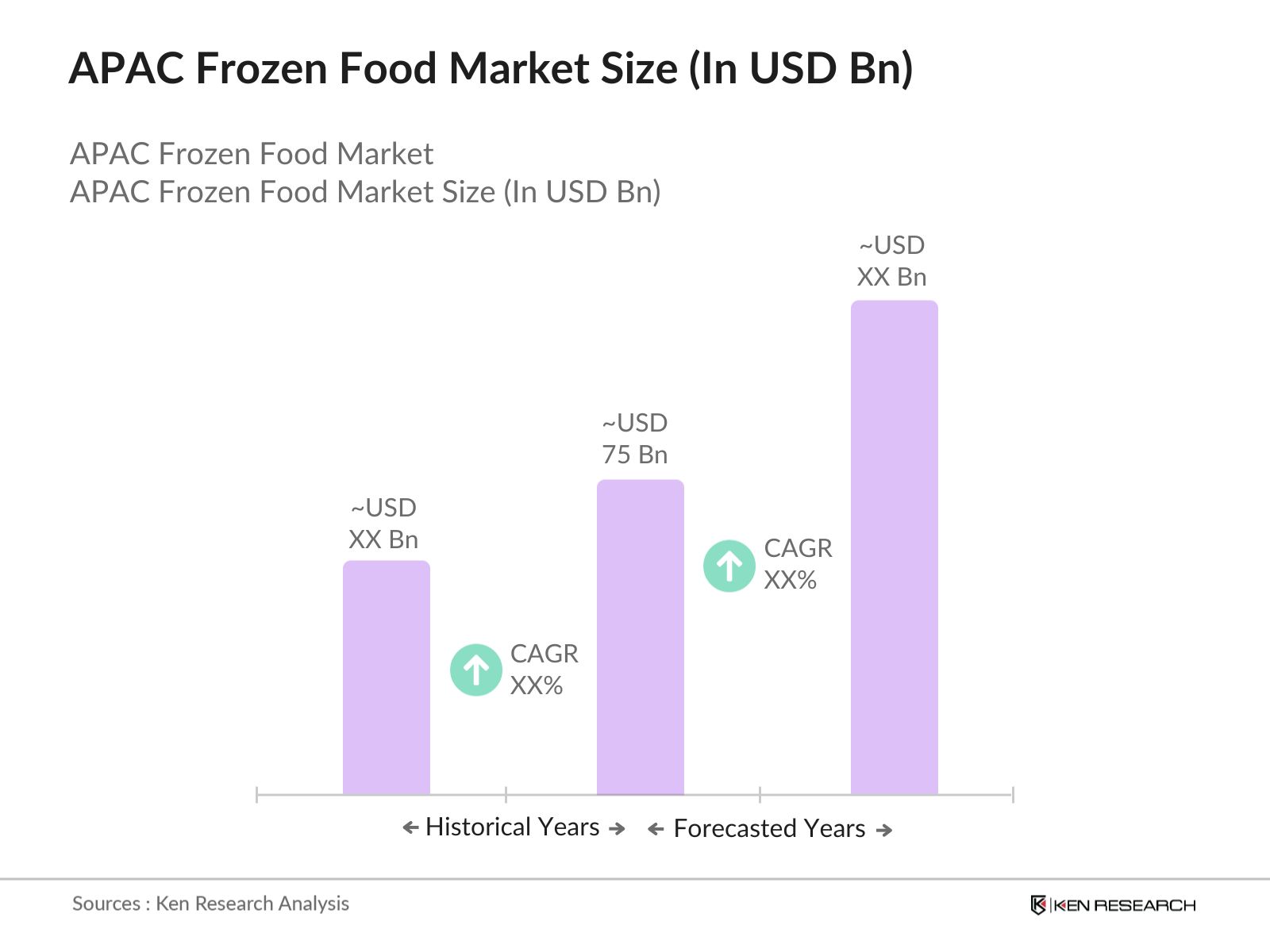

The APAC Frozen Food Market was valued at USD 75 billion, driven by rising consumer demand for convenience and long shelf-life food products. The market has seen a robust increase in adoption across urban centers, where consumers seek easy meal solutions.

Challenges in the APAC Frozen Food Market include underdeveloped cold chain infrastructure in certain Southeast Asian countries and consumer skepticism regarding the freshness of frozen products compared to fresh alternatives. Regulatory compliance for frozen food imports also poses barriers for smaller players.

Key players in the APAC Frozen Food market include Nestl, Ajinomoto Co., McCain Foods, Nichirei Foods, and Conagra Brands. These companies dominate the market due to their extensive distribution networks and innovative product offerings that cater to diverse consumer tastes.

The growth of the frozen food market is driven by increasing urbanization, rising disposable incomes, and the expansion of retail infrastructure across the region. Additionally, growing consumer awareness of the health benefits and convenience of frozen foods contributes to market growth.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.