APAC GPS Market Outlook to 2030

Region:Asia

Author(s):Meenakshi Bisht

Product Code:KROD6994

December 2024

85

About the Report

APAC GPS Market Overview

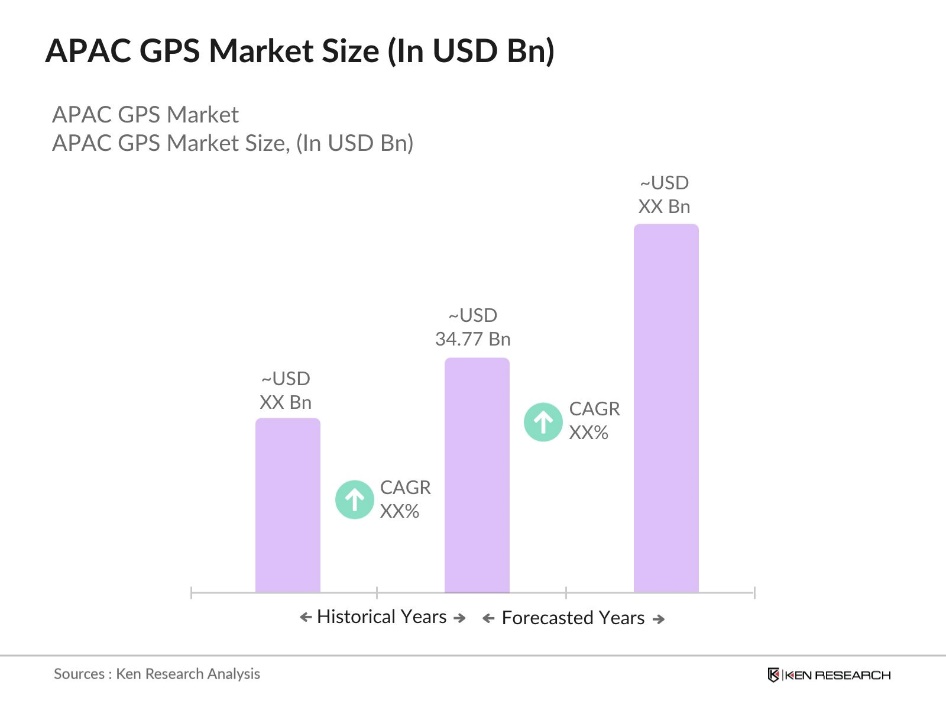

- The APAC GPS Market is valued at USD 34.77 billion, driven by rapid adoption across transportation, logistics, defense, and consumer electronics sectors. The demand for precise navigation and tracking solutions has risen, especially with the increasing urbanization in key economies like China and India. The rise in automotive production, coupled with the growing use of GPS in smartphones, wearable devices, and IoT applications, has also propelled market growth. Government initiatives to improve satellite infrastructure, such as Chinas BeiDou system, are further fueling this expansion.

- China and Japan dominate the APAC GPS market, largely due to their advanced technological infrastructure and significant investments in GPS-enabled applications. Chinas BeiDou Navigation Satellite System (BDS) offers a strong alternative to the U.S. GPS system, which strengthens the country's position. Japans leadership in automotive technology, especially in GPS-enabled vehicles, also contributes to its dominance. Furthermore, the robust defense sectors in these countries leverage GPS for precision targeting and communications, driving the market's leadership.

- Governments in APAC are enforcing stricter compliance standards for GPS systems in fleet management. South Korea now mandates GPS tracking for commercial fleets to meet road safety and emissions regulations, while Australia has implemented GPS-based monitoring for long-haul trucks to ensure safety compliance. These measures aim to enhance operational efficiency, improve safety, and reduce environmental impact in the transportation sector.

APAC GPS Market Segmentation

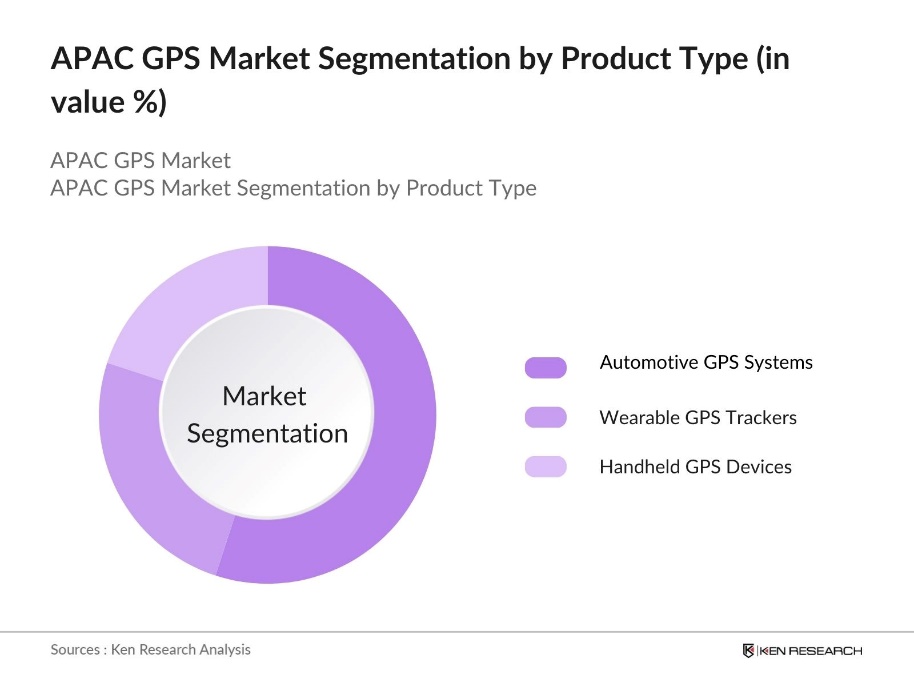

By Product Type: The APAC GPS market is segmented by product type into handheld GPS devices, automotive GPS systems, and wearable GPS trackers. Recently, automotive GPS systems have gained a dominant market share due to the increasing demand for in-car navigation systems and the rise in autonomous vehicle technologies. Major automotive manufacturers in the APAC region are integrating advanced GPS systems into their vehicles to enhance user experience and safety. This trend is supported by governments, which are promoting smart transportation systems, further driving the growth of automotive GPS systems.

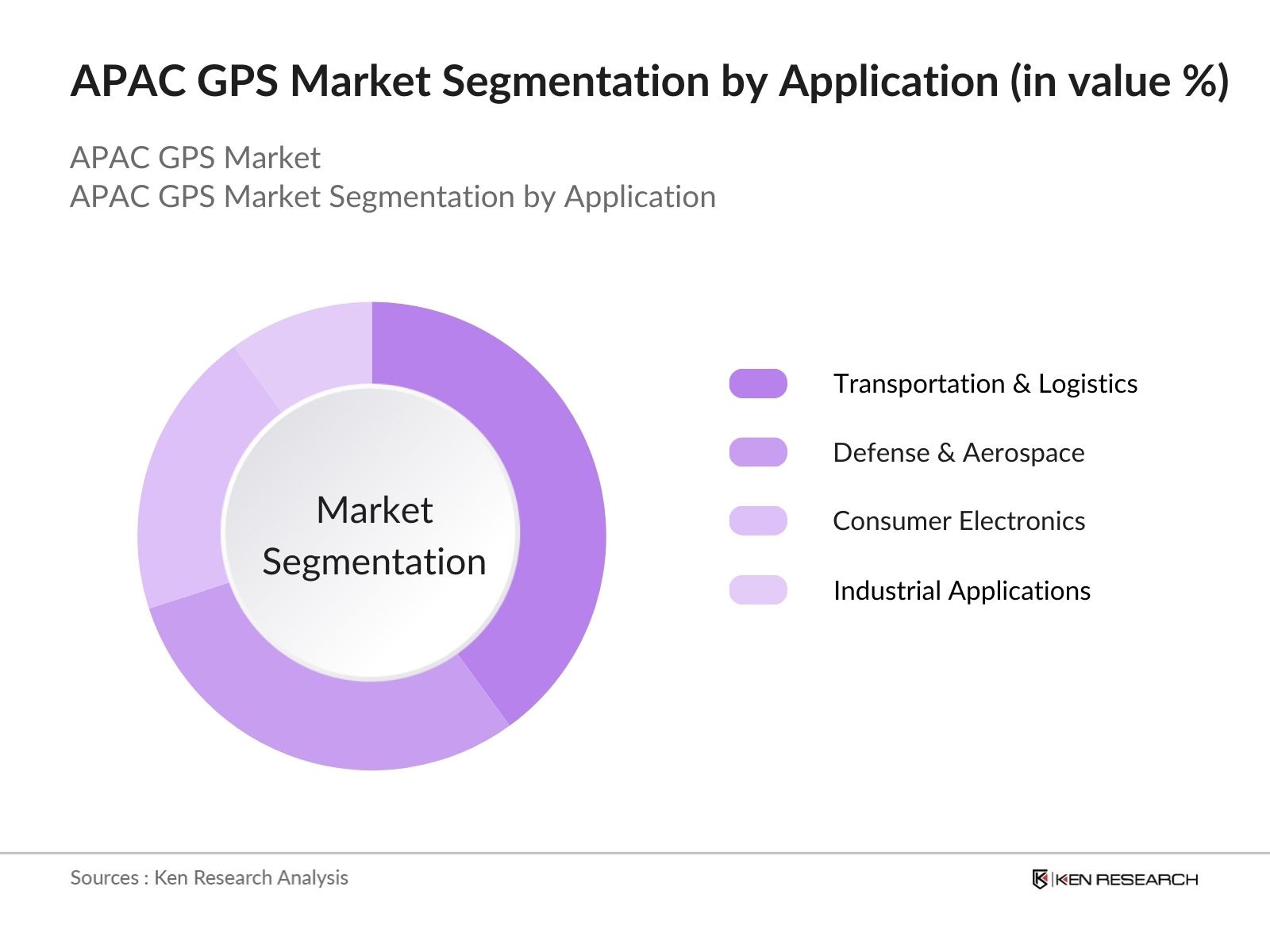

By Application: The APAC GPS market is also segmented by application into transportation & logistics, defense & aerospace, consumer electronics, and industrial applications. The transportation & logistics segment holds a dominant position, driven by the increasing need for efficient fleet management, route optimization, and cargo tracking. Companies across the APAC region are utilizing GPS systems to reduce operational costs and enhance productivity. The rapid growth of e-commerce in countries like China and India further boosts the demand for GPS-enabled tracking systems.

APAC GPS Market Competitive Landscape

The market is dominated by key players who are investing in technological advancements and expanding their geographic presence. The market is characterized by intense competition, with global companies like Garmin Ltd. and TomTom competing against local manufacturers such as u-blox and MiTAC. This consolidation underscores the influence of these major companies in shaping the market.

|

Company |

Establishment Year |

Headquarters |

Market Reach |

Revenue (2023) |

No. of Employees |

R&D Spend |

Satellites Supported |

Technological Focus |

Key Clients |

|

Garmin Ltd. |

1989 |

Switzerland |

|||||||

|

TomTom International BV |

1991 |

Netherlands |

|||||||

|

u-blox AG |

1997 |

Switzerland |

|||||||

|

MiTAC Digital Technology Corp. |

1982 |

Taiwan |

|||||||

|

Trimble Inc. |

1978 |

United States |

APAC GPS Industry Analysis

Growth Drivers

- Increasing Demand for Navigation Solutions (Transportation and Logistics Sectors): The APAC region is experiencing rapid growth in demand for GPS-based navigation solutions, particularly in transportation and logistics. The Indian government has mandated that all goods vehicles transporting hazardous materials must be equipped with location tracking devices, effective from September 1, 2022. This regulation reflects a broader push towards integrating advanced technologies like GPS into fleet management practices. With growing international trade in APAC, GPS technology plays a crucial role in enhancing logistics efficiency and reducing delays.

- Government Investments in Satellite Navigation Infrastructure: Countries across APAC are investing heavily in satellite navigation infrastructure to enhance GPS capabilities. In India, the government is making significant investments in its own satellite navigation system, known as NavIC (Navigation with Indian Constellation). Its aiming to ensure that it provides indigenous GPS capabilities for both civilian and military applications by 2025.

- Expansion in Wearable Technology and IoT Applications: The wearable technology market in APAC has seen substantial growth, with countries like China and Japan experiencing increasing adoption of devices such as fitness trackers and smartwatches. These wearables often feature GPS for enhanced tracking capabilities, particularly in health and fitness. Additionally, the rapid deployment of IoT across the region is contributing to the rise in GPS usage. IoT devices are being utilized in various sectors, including healthcare, smart cities, and agriculture, where GPS plays a critical role in providing location-based services and improving overall efficiency in real-time data processing.

Market Challenges

- High Operational Costs of GPS Systems: The operational costs of GPS systems remain a significant barrier, especially for small and medium-sized enterprises. These costs include hardware, software, and maintenance expenses, making it difficult for SMEs to adopt and sustain GPS technology. Additionally, maintaining satellite infrastructure is expensive, which further limits smaller nations from investing in their own GPS systems, creating a challenge for broader GPS adoption.

- Privacy and Security Concerns Related to Data Usage: GPS systems are vulnerable to data breaches, raising privacy concerns. Inadequate regulations governing location-based data collection in many APAC countries heighten these risks. While governments are increasingly focusing on cybersecurity, the region still lacks standardized measures to protect users' data, creating ongoing privacy and security challenges.

APAC GPS Market Future Outlook

The APAC GPS market is poised for significant growth over the coming years, driven by continuous technological advancements, increased adoption in autonomous vehicles, and the expansion of 5G networks. Governments across the APAC region are actively investing in satellite navigation systems, ensuring that local economies remain competitive on a global scale. The integration of AI and machine learning into GPS systems will also boost accuracy, making them indispensable for smart city projects and IoT ecosystems.

Market Opportunities

- Integration with AI for Autonomous Vehicles: The growth of autonomous vehicle technology in APAC creates significant opportunities for GPS systems. The integration of GPS with artificial intelligence improves vehicle performance by providing real-time data on traffic, road conditions, and optimal routing. As the region advances toward autonomous mobility solutions, GPS will play a crucial role in ensuring safe and efficient operations, becoming a foundational technology in the development of self-driving vehicles.

- Expansion of 5G Infrastructure and GPS Accuracy Enhancement: The expansion of 5G infrastructure across APAC is poised to significantly enhance GPS accuracy. With faster data transmission and reduced latency, 5G enables more precise real-time GPS tracking, crucial for sectors like logistics, autonomous vehicles, and smart cities. The integration of 5G and GPS is expected to improve overall user experience, driving innovation and expanding the potential applications of GPS technology across various industries.

Scope of the Report

|

Product Type |

Handheld GPS Devices Automotive GPS Systems Wearable GPS Trackers |

|

Application |

Transportation & Logistics Defense & Aerospace Consumer Electronics Industrial Applications Agriculture |

|

Technology |

Assisted GPS (A-GPS) Standalone GPS GPS with GNSS Real-Time Kinematic (RTK) GPS |

|

End-User Industry |

Automotive Government & Defense Commercial Consumer Electronics |

|

Region |

China South Korea Japan India Australia Rest of APAC |

Products

Key Target Audience

Automotive Manufacturers

Satellite Communication Providers

GPS Device Manufacturers

Telecommunication Companies

Government and Regulatory Bodies (e.g., China Satellite Navigation Office)

Investors and venture capital Firms

Banks and Financial Institutions

Companies

Players Mentioned in the Report

Garmin Ltd.

TomTom International BV

Trimble Inc.

u-blox AG

MiTAC Digital Technology Corporation

Qualcomm Technologies, Inc.

Broadcom Inc.

HERE Technologies

SkyTraq Technology Inc.

STMicroelectronics

Table of Contents

1. APAC GPS Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (based on adoption in transportation, logistics, defense, and consumer electronics)

1.4. Market Segmentation Overview

2. APAC GPS Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones (penetration in automotive and smartphone markets)

3. APAC GPS Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Demand for Navigation Solutions (transportation and logistics sectors)

3.1.2. Government Investments in Satellite Navigation Infrastructure

3.1.3. Expansion in Wearable Technology and IoT Applications

3.2. Market Challenges

3.2.1. High Operational Costs of GPS Systems

3.2.2. Privacy and Security Concerns Related to Data Usage

3.2.3. Competition from Alternative Positioning Technologies (Bluetooth and Wi-Fi)

3.3. Opportunities

3.3.1. Integration with AI for Autonomous Vehicles

3.3.2. Expansion of 5G Infrastructure and GPS Accuracy Enhancement

3.3.3. Rise in Smart City Projects across APAC

3.4. Trends

3.4.1. Adoption of Multi-Constellation Systems (GPS, GLONASS, Beidou)

3.4.2. Growth of GNSS Augmentation Services

3.4.3. Integration with Augmented Reality (AR)

3.5. Government Regulation

3.5.1. National GPS Regulatory Policies (APAC region-specific)

3.5.2. Subsidies for GPS-Integrated Agricultural Solutions

3.5.3. Compliance Standards for Fleet Management GPS Systems

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.7.1. Suppliers, Distributors, and Service Providers

3.8. Porters Five Forces

3.8.1. Bargaining Power of Suppliers

3.8.2. Bargaining Power of Buyers

3.8.3. Threat of New Entrants

3.8.4. Threat of Substitutes

3.8.5. Competitive Rivalry

3.9. Competition Ecosystem

4. APAC GPS Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Handheld GPS Devices

4.1.2. Automotive GPS Systems

4.1.3. Wearable GPS Trackers

4.2. By Application (In Value %)

4.2.1. Transportation & Logistics

4.2.2. Defense & Aerospace

4.2.3. Consumer Electronics

4.2.4. Industrial Applications

4.2.5. Agriculture

4.3. By Technology (In Value %)

4.3.1. Assisted GPS (A-GPS)

4.3.2. Standalone GPS

4.3.3. GPS with GNSS

4.3.4. Real-Time Kinematic (RTK) GPS

4.4. By End-User Industry (In Value %)

4.4.1. Automotive

4.4.2. Government & Defense

4.4.3. Commercial

4.4.4. Consumer Electronics

4.5. By Region (In Value %)

4.5.1. China

4.5.2. South Korea

4.5.3. Japan

4.5.4. India

4.5.5. Australia

4.5.6. Rest of APAC

5. APAC GPS Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Garmin Ltd.

5.1.2. TomTom International BV

5.1.3. Trimble Inc.

5.1.4. MiTAC Digital Technology Corporation

5.1.5. u-blox AG

5.1.6. Qualcomm Technologies, Inc.

5.1.7. Broadcom Inc.

5.1.8. Hexagon AB

5.1.9. HERE Technologies

5.1.10. SkyTraq Technology Inc.

5.1.11. STMicroelectronics

5.1.12. Honeywell International Inc.

5.1.13. Orbcomm Inc.

5.1.14. Navinfo Co., Ltd.

5.1.15. Alps Alpine Co., Ltd.

5.2. Cross Comparison Parameters (No. of Satellites, Market Penetration, Inception Year, Headquarters, Revenue, Workforce, R&D Spend, Global Reach)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Government Grants and Collaborations

5.8. Private Equity Investments

6. APAC GPS Market Regulatory Framework

6.1. Regional GPS Regulations (APAC-specific)

6.2. Satellite Launch Approvals

6.3. Data Privacy and Security Laws

7. APAC GPS Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. APAC GPS Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By Technology (In Value %)

8.4. By End-User Industry (In Value %)

8.5. By Region (In Value %)

9. APAC GPS Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

In the initial phase, the key variables influencing the APAC GPS Market were identified, including market growth rates, key stakeholders, and emerging technologies. Desk research and proprietary databases were employed to gather this information.

Step 2: Market Analysis and Construction

Historical market data was compiled to analyze the development of the GPS market. Specific attention was paid to market penetration in industries such as automotive and defense, providing a clear picture of revenue generation across sectors.

Step 3: Hypothesis Validation and Expert Consultation

Hypotheses regarding the APAC GPS market were formulated based on industry trends and validated through consultations with industry experts. This process ensured the accuracy of the gathered data and provided insights into the operational aspects of the market.

Step 4: Research Synthesis and Final Output

The final phase involved synthesizing the research into actionable insights, confirming data points through direct consultations with key GPS manufacturers, and ensuring all aspects of the market were covered comprehensively.

Frequently Asked Questions

01. How big is the APAC GPS Market?

The APAC GPS Market is valued at USD 34.77 billion, driven by its application in industries such as automotive, logistics, and defense, along with the expansion of GPS-based wearable technology.

02. What are the challenges in the APAC GPS Market?

Key in challenges in the APAC GPS market include high operational costs, security concerns over GPS data, and competition from alternative positioning technologies such as Wi-Fi and Bluetooth.

03. Who are the major players in the APAC GPS Market?

Major players in APAC GPS market include Garmin Ltd., TomTom International BV, Trimble Inc., MiTAC Digital Technology Corporation, and u-blox AG, who lead the market through continuous innovation and strategic partnerships.

04. What are the growth drivers of the APAC GPS Market?

The growth of the APAC GPS market is driven by advancements in autonomous vehicle technology, the rise in e-commerce logistics, and government investments in satellite navigation systems like Chinas BeiDou.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.