APAC GPU Market Outlook to 2030

Region:Afganistan

Author(s):Shubham Kashyap

Product Code:KROD3704

Region:Afganistan

Author(s):Shubham Kashyap

Product Code:KROD3704

November 2024

83

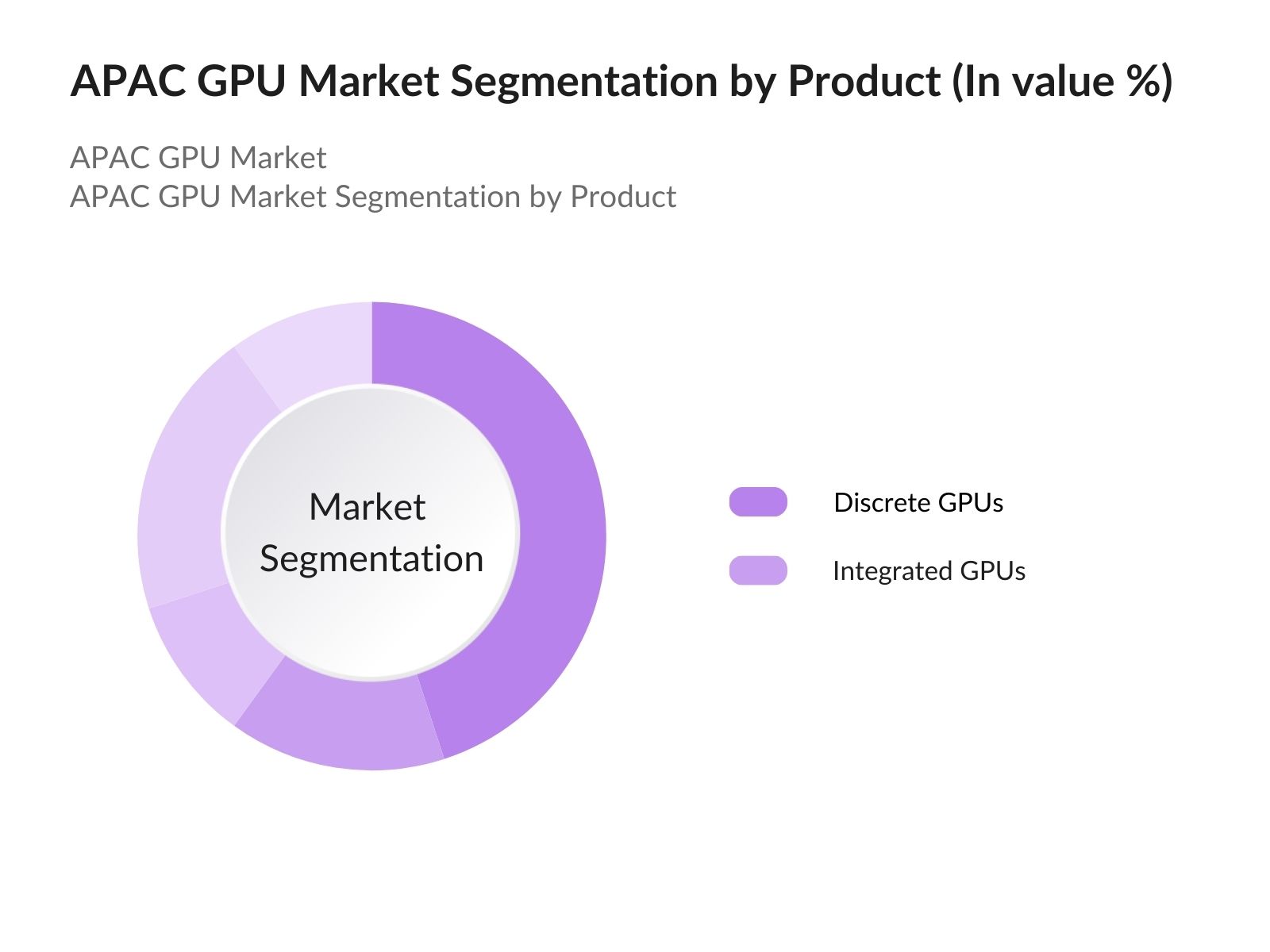

By Product Type: The market is segmented into discrete GPUs and integrated GPUs. Discrete GPUs dominate the market, especially in gaming, automotive, and data center applications, where high computational power is essential. Integrated GPUs are popular in mobile devices and entry-level computing systems due to their power efficiency and cost-effectiveness. However, the rise of AI-driven applications is pushing discrete GPUs as they offer superior performance in parallel computing and data processing tasks.

The APAC GPU market is highly competitive, with several key players continuously innovating and expanding their product offerings. Major players include NVIDIA Corporation, AMD (Advanced Micro Devices), Intel Corporation, and Samsung Electronics, all of which are involved in large-scale production and distribution of GPUs for gaming, AI, and data center applications. These companies are actively investing in research and development to enhance GPU performance, power efficiency, and compatibility with emerging technologies like AI and 5G.

|

Company Name |

Establishment Year |

Headquarters |

R&D Investment (USD Mn) |

No. of Employees |

Key Product Offerings |

Market Presence |

Recent Innovations |

Partnership Deals |

AI/ML Integration |

|

NVIDIA Corporation |

1993 |

Santa Clara, USA |

|||||||

|

AMD (Advanced Micro Devices) |

1969 |

Santa Clara, USA |

|||||||

|

Intel Corporation |

1968 |

Santa Clara, USA |

|||||||

|

Samsung Electronics |

1938 |

Suwon, South Korea |

|||||||

|

Qualcomm Incorporated |

1985 |

San Diego, USA |

The APAC GPU market is poised for significant growth over the next five years, driven by the rise of gaming, AI, and data center applications. The integration of GPUs in emerging technologies such as autonomous driving, robotics, and 5G networks is expected to further boost demand. Moreover, the expansion of cloud gaming services and AI-driven industries will open new growth avenues for GPU manufacturers.

|

By End-User |

Gaming |

|

By Product Type |

Discrete GPUs |

|

By Technology |

AI/ML-Powered GPUs |

|

By Application |

Video Processing & Rendering |

|

By Region |

China Rest of the APAC |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Rising Demand for Gaming and Esports (Gaming, AR/VR Adoption, and Esports Influence)

3.1.2. Expansion of AI and Machine Learning Applications (AI Integration, Cloud Computing, Data Processing)

3.1.3. Technological Advancements in Autonomous Vehicles (Automotive Sector GPU Adoption)

3.1.4. Surge in Data Center and Cloud Computing Investments (Cloud Services, GPU-Accelerated Data Centers)

3.2. Market Challenges

3.2.1. High Costs of High-Performance GPUs (Pricing Constraints, Affordability in Emerging Markets)

3.2.2. Semiconductor Supply Chain Disruptions (Raw Material Shortages, Production Delays)

3.2.3. Regulatory and Environmental Concerns (Energy Consumption, Environmental Regulations)

3.2.4. Limited Access to GPUs in Developing Markets (Regional Disparities, Import Regulations)

3.3. Opportunities

3.3.1. Rising Cloud Gaming Adoption (Cloud-Based Gaming Platforms, Internet Infrastructure Expansion)

3.3.2. Growth in GPU Applications in Healthcare (AI-Driven Diagnostics, Medical Imaging)

3.3.3. Expansion into Southeast Asian Markets (Emerging Economies, Market Penetration)

3.3.4. Government Support for Digital Infrastructure (Government Investments in Technology, AI Initiatives)

3.4. Trends

3.4.1. Integration of AI and GPUs for Enhanced Computing (AI-GPU Synergy, Improved Data Processing)

3.4.2. Adoption of GPUs in Edge Computing (IoT Applications, Low-Latency Processing)

3.4.3. Growth in Gaming GPUs (Competitive Gaming, Advanced Graphics)

3.4.4. GPU-Powered Innovations in Virtual and Augmented Reality (VR/AR Developments)

3.5. Government Regulation

3.5.1. Policies for AI and GPU Infrastructure (AI Policies, GPU in National Development Plans)

3.5.2. Semiconductor Manufacturing Policies (National Production Incentives, GPU Chip Manufacturing)

3.5.3. Data Security Regulations (Compliance with Data Protection Laws, GPU in Secure Processing)

3.5.4. Environmental Standards for Data Centers (Energy Efficiency, GPU Power Consumption)

3.6. SWOT Analysis

3.7. Stake Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

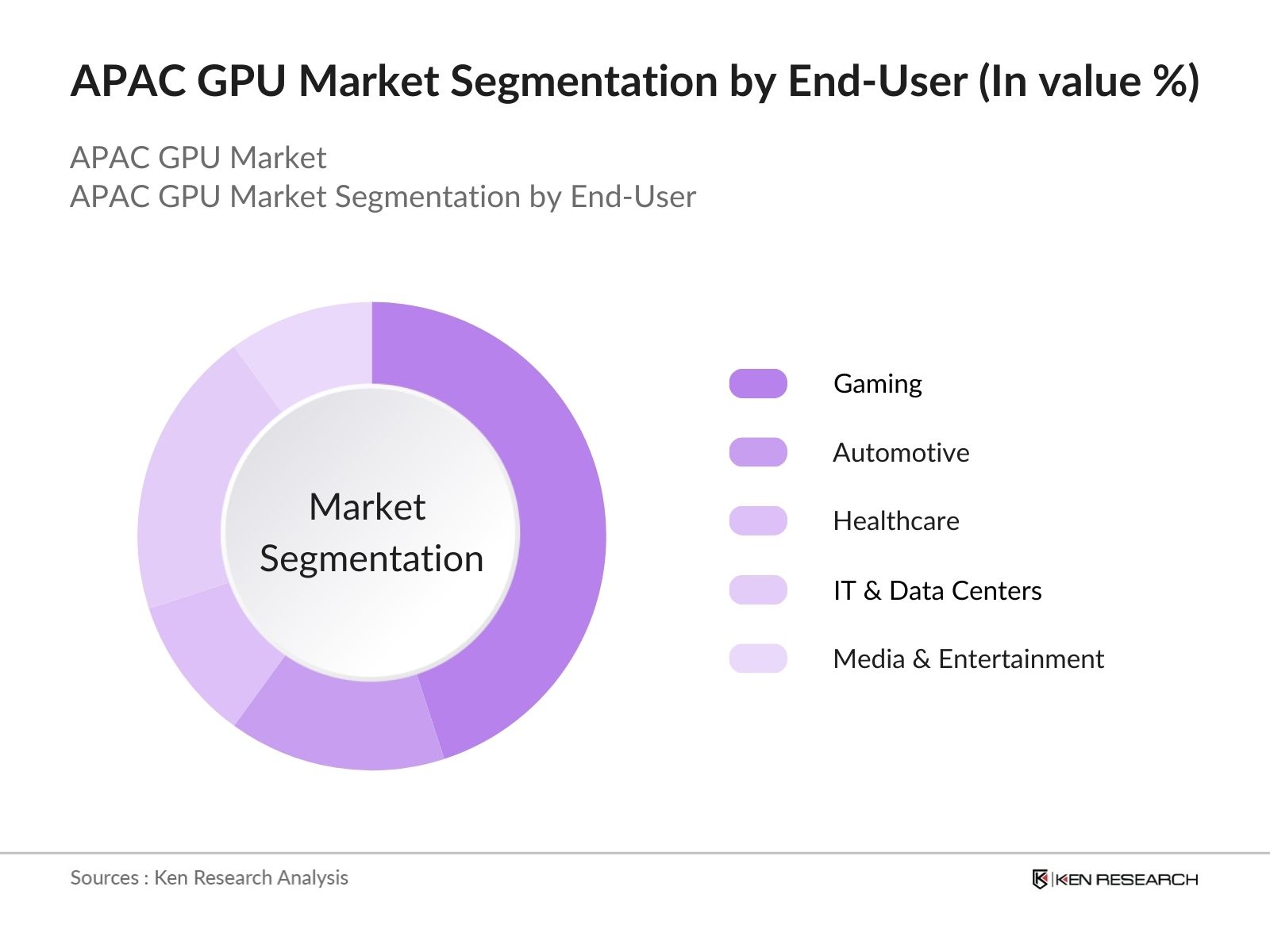

4.1. By End-Use Industry (In Value %)

4.1.1. Gaming

4.1.2. Automotive

4.1.3. Healthcare

4.1.4. IT & Data Centers

4.1.5. Media & Entertainment

4.2. By Product Type (In Value %)

4.2.1. Discrete GPUs

4.2.2. Integrated GPUs

4.3. By Technology (In Value %)

4.3.1. AI/ML-Powered GPUs

4.3.2. Virtualization & Cloud GPUs

4.3.3. 4K and 8K Rendering GPUs

4.4. By Application (In Value %)

4.4.1. Video Processing & Rendering

4.4.2. AI & Machine Learning

4.4.3. High-Performance Computing

4.4.4. Autonomous Driving

4.5. By Region (In Value %)

4.5.1. China

4.5.2. Japan

4.5.3. South Korea

4.5.4. Southeast Asia

4.5.5. India

5.1 Detailed Profiles of Major Companies

5.1.1. NVIDIA Corporation

5.1.2. AMD (Advanced Micro Devices)

5.1.3. Intel Corporation

5.1.4. Samsung Electronics

5.1.5. Qualcomm Incorporated

5.1.6. ARM Holdings

5.1.7. Imagination Technologies

5.1.8. MediaTek Inc.

5.1.9. Broadcom Inc.

5.1.10. ASUSTek Computer Inc.

5.1.11. ZTE Corporation

5.1.12. Huawei Technologies Co., Ltd.

5.1.13. Gigabyte Technology

5.1.14. Lenovo Group Limited

5.1.15. Acer Inc.

5.2 Cross Comparison Parameters

5.2.1. No. of Employees

5.2.2. Headquarters

5.2.3. Inception Year

5.2.4. Revenue

5.2.5. R&D Investments

5.2.6. Geographical Reach

5.2.7. Product Range

5.2.8. Technology Adoption

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Environmental Standards

6.2. Compliance Requirements

6.3. Certification Processes

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By End-Use Industry (In Value %)

8.2. By Product Type (In Value %)

8.3. By Technology (In Value %)

8.4. By Application (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the APAC GPU Market. Extensive desk research is conducted using secondary and proprietary databases to gather comprehensive market data. The primary objective is to identify critical variables, including technological advancements and key end-use industries.

In this phase, we compile and analyze historical data, focusing on GPU penetration in gaming, AI, and data centers. The evaluation includes performance statistics, revenue generation, and market dynamics. This ensures a robust understanding of how the market has evolved and current growth trends.

Market hypotheses are validated through interviews with industry experts, including representatives from major GPU manufacturers. These interviews provide critical insights into market strategies, sales performance, and technological adoption, which are key to corroborating market data.

In the final phase, direct engagement with GPU manufacturers and AI-driven companies provides deeper insights into product segmentation, consumer preferences, and market forecasts. This helps refine the data and ensure a comprehensive, accurate, and validated analysis of the APAC GPU market.

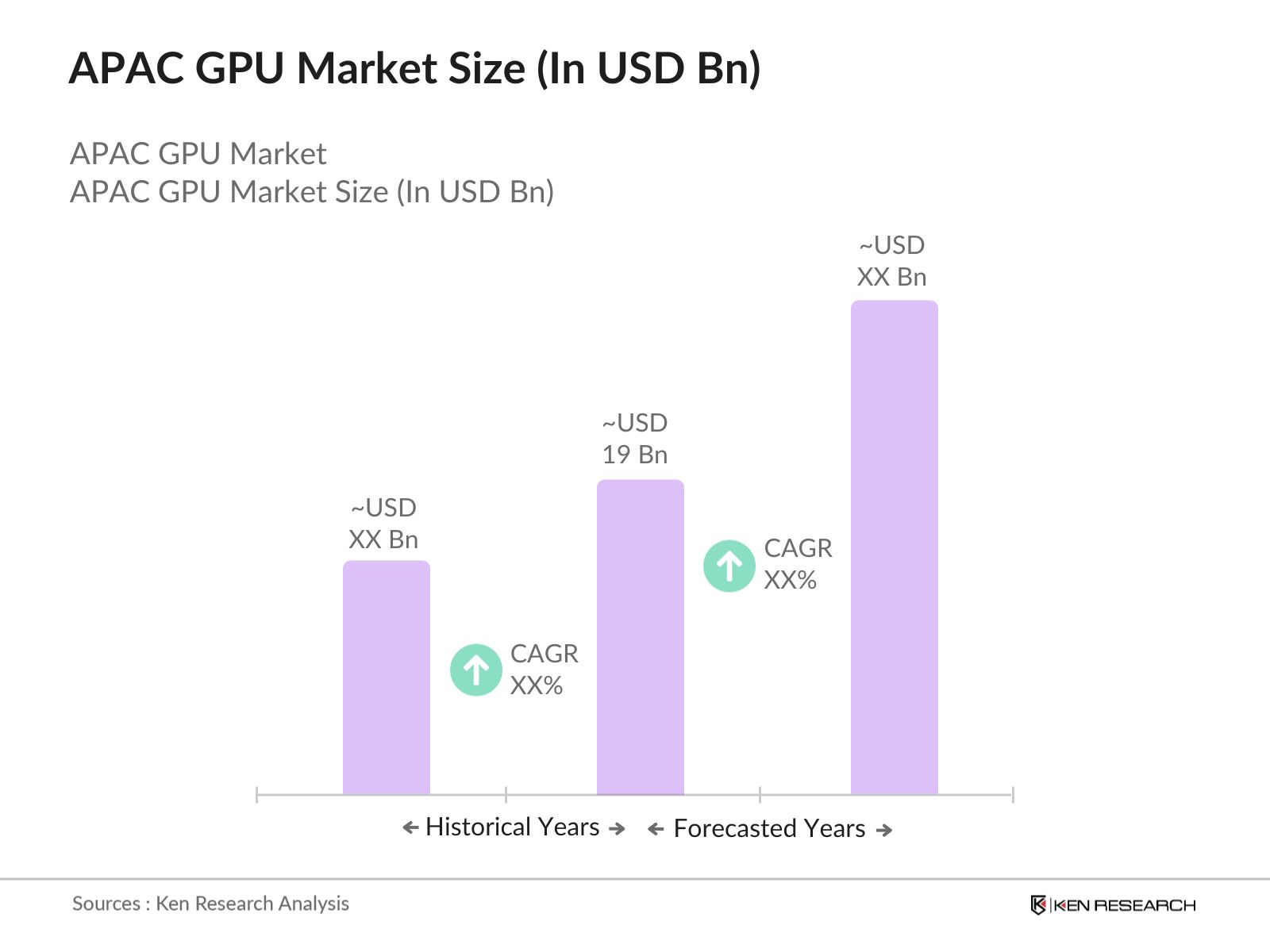

The APAC GPU market was valued at USD 19 billion, driven by the increasing adoption of gaming, AI, and data center applications. Major players like NVIDIA and AMD continue to dominate this rapidly growing market.

Challenges in the APAC GPU market include the high cost of high-performance GPUs, semiconductor supply chain disruptions, and regulatory concerns regarding energy consumption in data centers. These challenges are affecting the scalability of GPU deployment across key industries.

Key players in the APAC GPU market include NVIDIA Corporation, AMD, Intel, Samsung Electronics, and Qualcomm. These companies dominate due to their innovative product portfolios, extensive R&D investments, and partnerships with AI and gaming companies.

The APAC GPU market is driven by the increasing demand for high-performance GPUs in gaming, AI, and cloud computing. The adoption of advanced technologies such as autonomous driving and AI-based analytics is further fueling market growth.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.