APAC Solar Control Window Films Market Outlook to 2030

Region:Afganistan

Author(s):Meenakshi Bisht

Product Code:KROD9228

Region:Afganistan

Author(s):Meenakshi Bisht

Product Code:KROD9228

December 2024

98

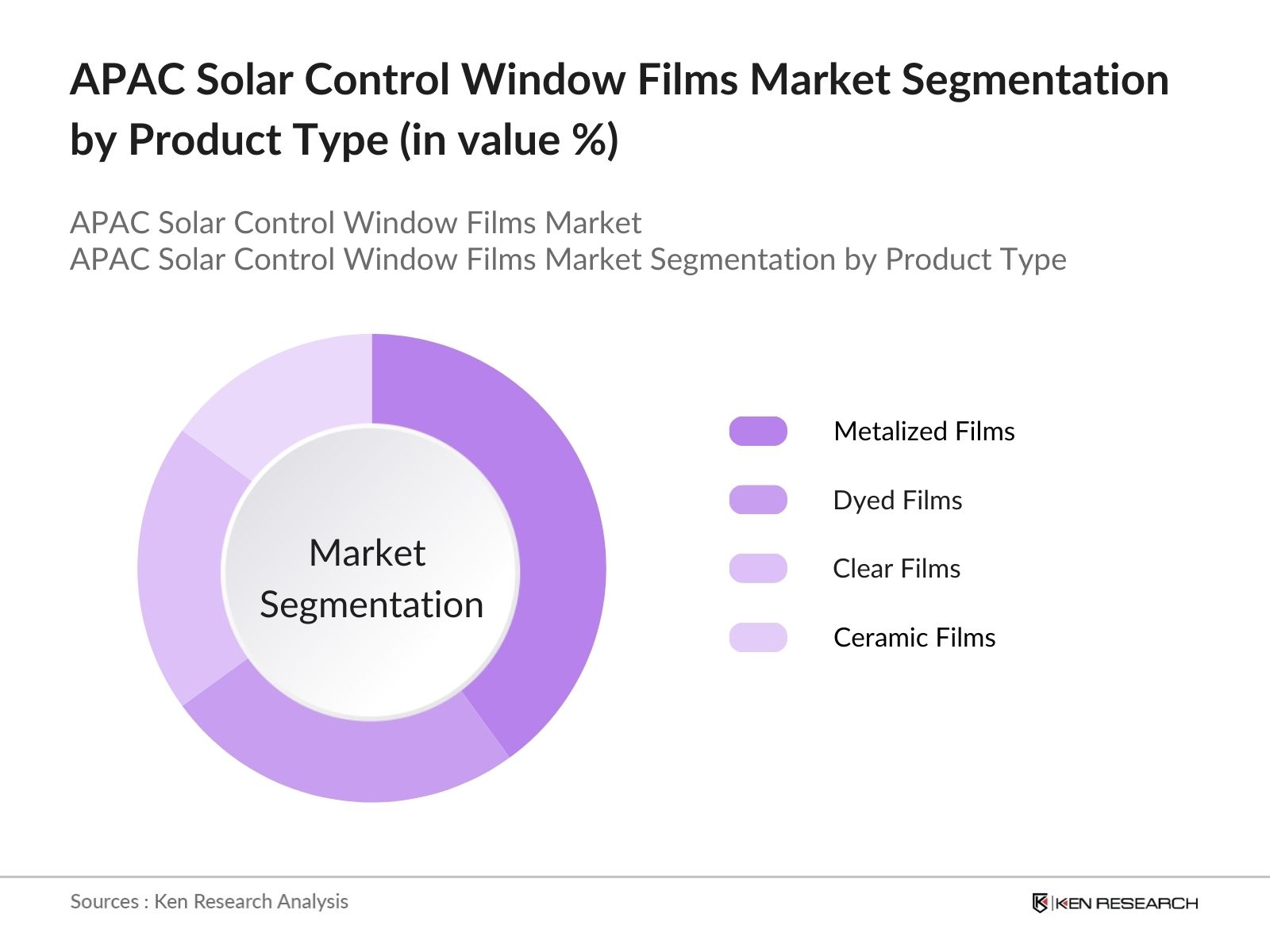

By Product Type: The market is segmented by product type into dyed films, clear films, metalized films, and ceramic films. Among these, metalized films hold a dominant market share due to their superior heat rejection properties and cost-effectiveness. These films reflect solar energy while maintaining optical clarity, making them popular for both residential and commercial buildings. Additionally, metalized films are widely used in the automotive industry, especially in countries like Japan and China, where regulatory frameworks emphasize energy efficiency.

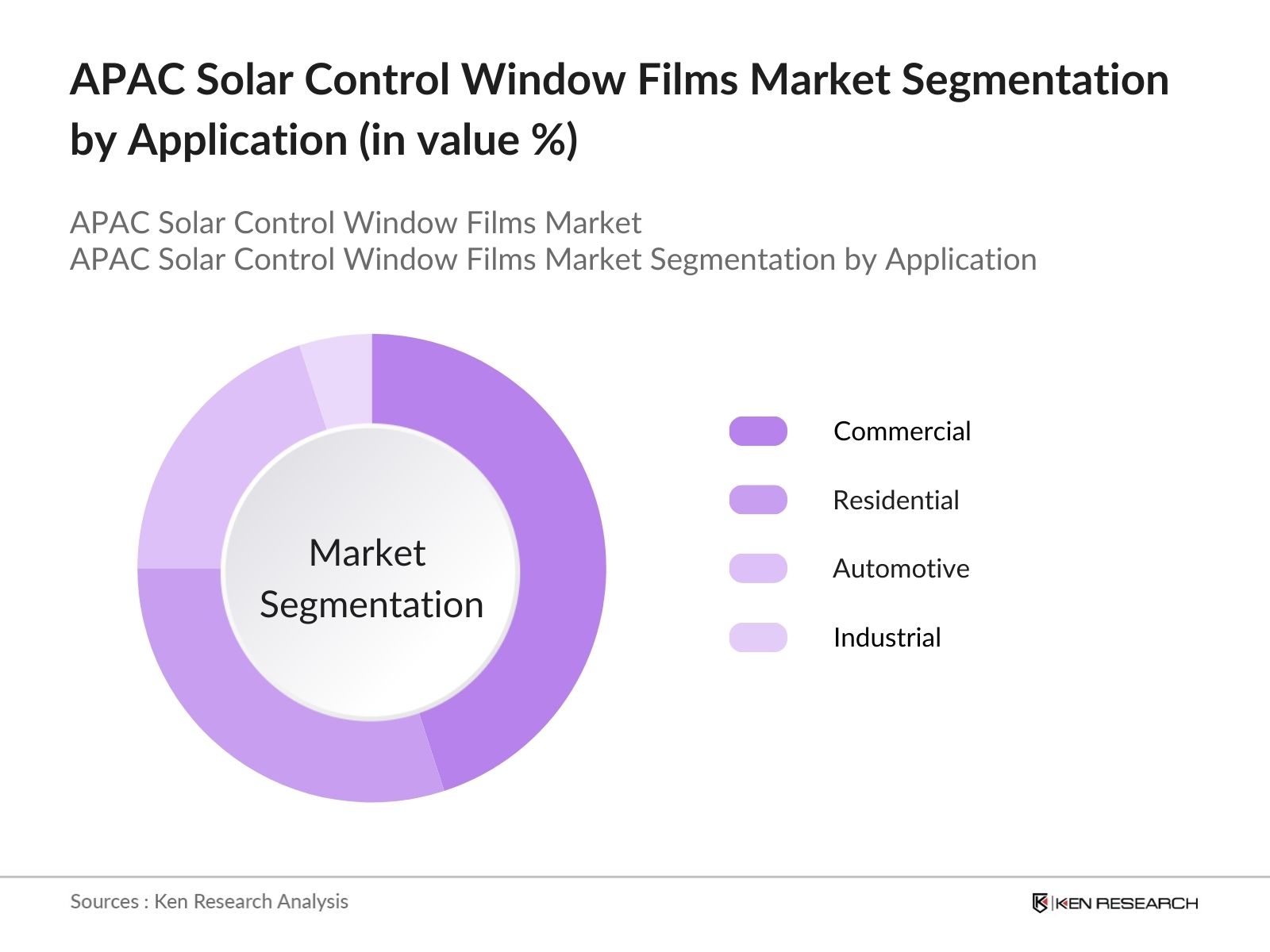

By Application: The market is segmented by application into residential, commercial, automotive, and industrial. The commercial sector currently dominates the market, accounting for a significant portion of the market share. This is due to the large-scale adoption of energy-efficient solutions in office buildings, malls, and other commercial infrastructures. The increasing number of skyscrapers and high-rise buildings in urban centers across China, Japan, and India, along with growing awareness of environmental sustainability, have significantly boosted the demand for solar control window films in this segment.

The market is dominated by companies like 3M and Eastman Chemical Company, which have a global presence and a strong foothold in the APAC region. Other significant players include Garware Suncontrol, Avery Dennison Corporation, and Saint-Gobain, which offer a variety of solar control window films catering to different market segments. These companies leverage their extensive distribution networks and partnerships with contractors and builders to maintain their competitive edge.

The APAC solar control window films market is set to witness considerable growth, driven by ongoing urbanization, the increasing adoption of green building initiatives, and rising consumer awareness regarding energy efficiency. Government policies promoting the reduction of carbon footprints and incentivizing the use of energy-saving materials in the construction and automotive sectors will further fuel demand for solar control window films. Additionally, the rapid growth of electric vehicles in countries like China and Japan is expected to drive the demand for solar films in the automotive sector.

|

Product Type |

Dyed Films Clear Films Metalized Films Ceramic Films |

|

Application |

Residential Commercial Automotive Industrial |

|

Technology |

Passive Films Smart Films |

|

Installation Type |

Retrofit New Construction |

|

Region |

China Japan South Korea India Australia Southeast Asia |

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2.1 Historical Market Size

2.2 Year-on-Year Growth Analysis

2.3 Key Market Developments and Milestones

3.1 Growth Drivers

3.1.1 Increasing Energy Efficiency Demands (Energy savings and environmental impact)

3.1.2 Rising Construction and Infrastructure Projects (Building and automotive sectors)

3.1.3 Government Regulations on Energy Consumption (Sustainability, green building codes)

3.1.4 Consumer Awareness Regarding UV Protection

3.2 Market Challenges

3.2.1 High Initial Installation Costs (Price sensitivity, cost of retrofitting)

3.2.2 Compatibility Issues with Low-E Windows (Compatibility with new construction standards)

3.2.3 Limited Awareness in Emerging Markets (Market penetration challenges)

3.3 Opportunities

3.3.1 Technological Advancements in Film Manufacturing (Innovations in nanotechnology, multi-layer films)

3.3.2 Expanding Applications in the Automotive Industry (Solar control film adoption in EVs)

3.3.3 Increasing Adoption in Commercial Buildings (Green building initiatives, corporate demand)

3.4 Trends

3.4.1 Rising Adoption of Smart Window Films (Integration with smart homes, IoT-enabled films)

3.4.2 Eco-friendly Window Films (Development of biodegradable and recyclable films)

3.4.3 Advanced Anti-Glare and UV Rejection Films (Health benefits and skin protection focus)

3.5 Government Regulation

3.5.1 Energy Efficiency Building Codes (Standards for solar control, LEED certifications)

3.5.2 Import and Export Tariffs on Solar Films (Trade regulations and international policies)

3.5.3 Renewable Energy Incentives (Government grants for energy-saving retrofits)

3.6 SWOT Analysis

3.7 Stake Ecosystem (Raw material suppliers, distributors, installers, end-users)

3.8 Porters Five Forces Analysis

3.9 Competitive Landscape (Competitive pricing strategies, innovation, market share)

4.1 By Product Type (in Value %)

4.1.1 Dyed Films

4.1.2 Clear Films

4.1.3 Metalized Films

4.1.4 Ceramic Films

4.2 By Application (in Value %)

4.2.1 Residential

4.2.2 Commercial

4.2.3 Automotive

4.2.4 Industrial

4.3 By Technology (in Value %)

4.3.1 Passive Films

4.3.2 Smart Films

4.4 By Installation Type (in Value %)

4.4.1 Retrofit

4.4.2 New Construction

4.5 By Region (in Value %)

4.5.1 China

4.5.2 Japan

4.5.3 South Korea

4.5.4 India

4.5.5 Australia

4.5.6 Southeast Asia

5.1 Detailed Profiles of Major Companies

5.1.1 3M Company

5.1.2 Eastman Chemical Company

5.1.3 Saint-Gobain Performance Plastics

5.1.4 Avery Dennison Corporation

5.1.5 Johnson Window Films

5.1.6 Garware Suncontrol

5.1.7 Polytronix Inc.

5.1.8 Madico Inc.

5.1.9 Solar Gard (a division of Saint-Gobain)

5.1.10 LINTEC Corporation

5.1.11 V-KOOL International

5.1.12 Hanita Coatings (Avery Dennison)

5.1.13 Huper Optik USA

5.1.14 Global Window Films

5.1.15 Armolan USA

5.2 Cross Comparison Parameters (Headquarters, Inception Year, Product Portfolio, Revenue, Market Share)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Private Equity and Venture Capital Funding

5.8 Government Grants and Subsidies

5.9 Research and Development (Innovation and product enhancements)

6.1 Energy Efficiency Standards (Building and construction)

6.2 Automotive Solar Film Regulations (Vehicle safety and certification standards)

6.3 Compliance with Environmental Laws (Waste reduction and sustainability)

6.4 Certification and Licensing Processes

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8.1 By Product Type (in Value %)

8.2 By Application (in Value %)

8.3 By Technology (in Value %)

8.4 By Installation Type (in Value %)

8.5 By Region (in Value %)

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 Marketing and Distribution Initiatives

9.4 White Space Opportunity Analysis

Disclaimer Contact UsIn this phase, we conducted a thorough analysis of historical data related to the solar control window films market, focusing on the construction and automotive industries. Revenue generation, penetration rates, and other market dynamics were evaluated to construct reliable estimates.

Market hypotheses were developed based on the data collected and validated through interviews with industry experts from leading solar control window film manufacturers. These consultations provided operational and financial insights crucial to refining the market analysis.

The final phase involved direct engagement with manufacturers and distributors to validate product-level data. This step ensured that the market report was comprehensive, accurate, and reflective of the current market scenario in the APAC region.

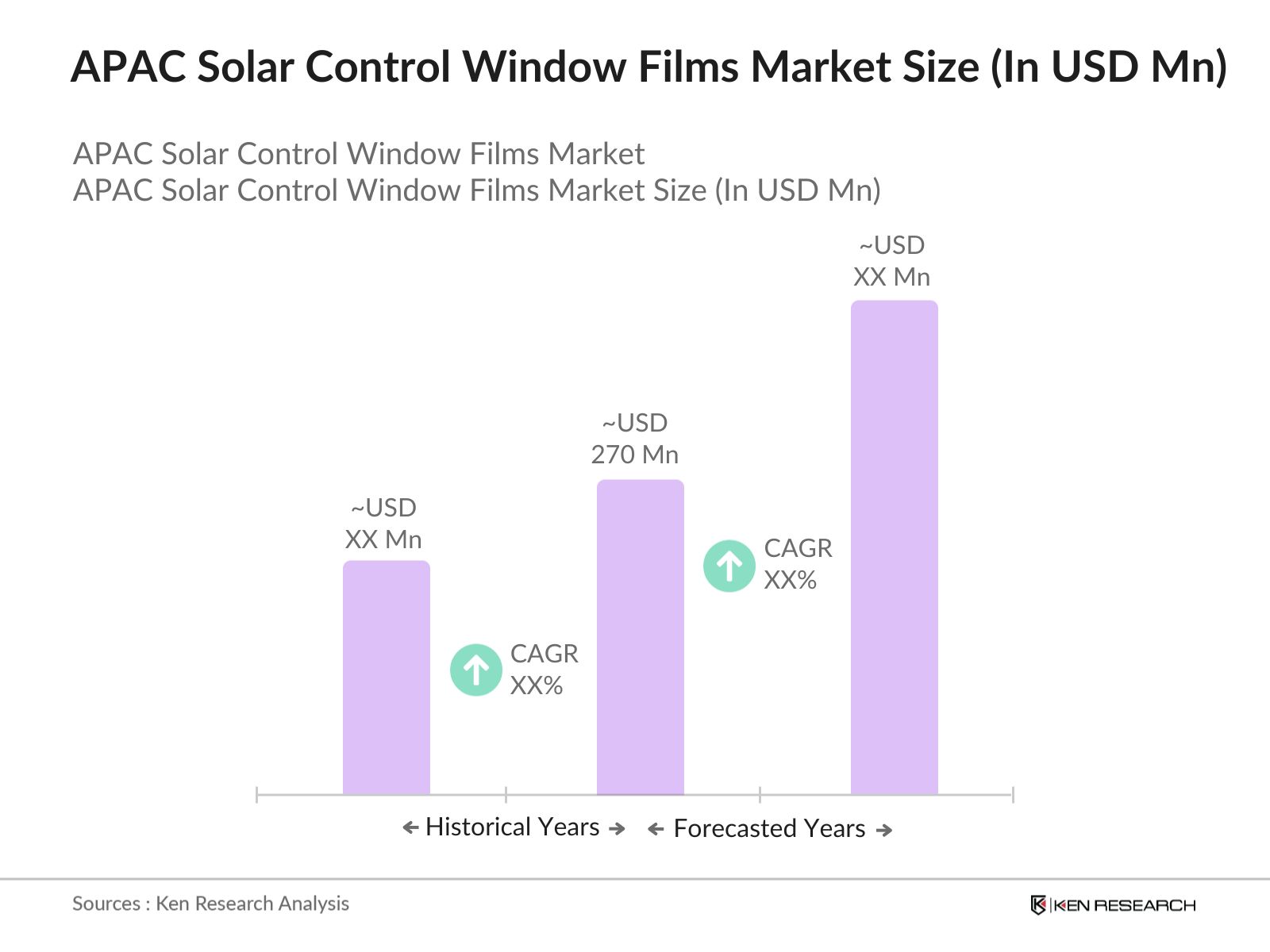

The APAC solar control window films market is valued at USD 270 million, driven by increasing demand for energy-efficient solutions in construction and automotive sectors across the region.

Key challenges in APAC solar control window films market include high initial installation costs and the limited awareness of solar control window films in emerging markets, particularly in Southeast Asia.

Leading players in APAC solar control window films market include 3M Company, Eastman Chemical Company, Saint-Gobain Performance Plastics, Garware Suncontrol, and Avery Dennison Corporation. These companies dominate due to their strong distribution networks and innovation in solar control technology.

The APAC solar control window films market is driven by the rising need for energy efficiency in buildings, government policies promoting sustainability, and the increasing use of solar films in the automotive industry.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.