APAC Solar Powered Cars Market Outlook to 2030

Region:Asia

Author(s):Shambhavi

Product Code:KROD5890

Region:Asia

Author(s):Shambhavi

Product Code:KROD5890

November 2024

85

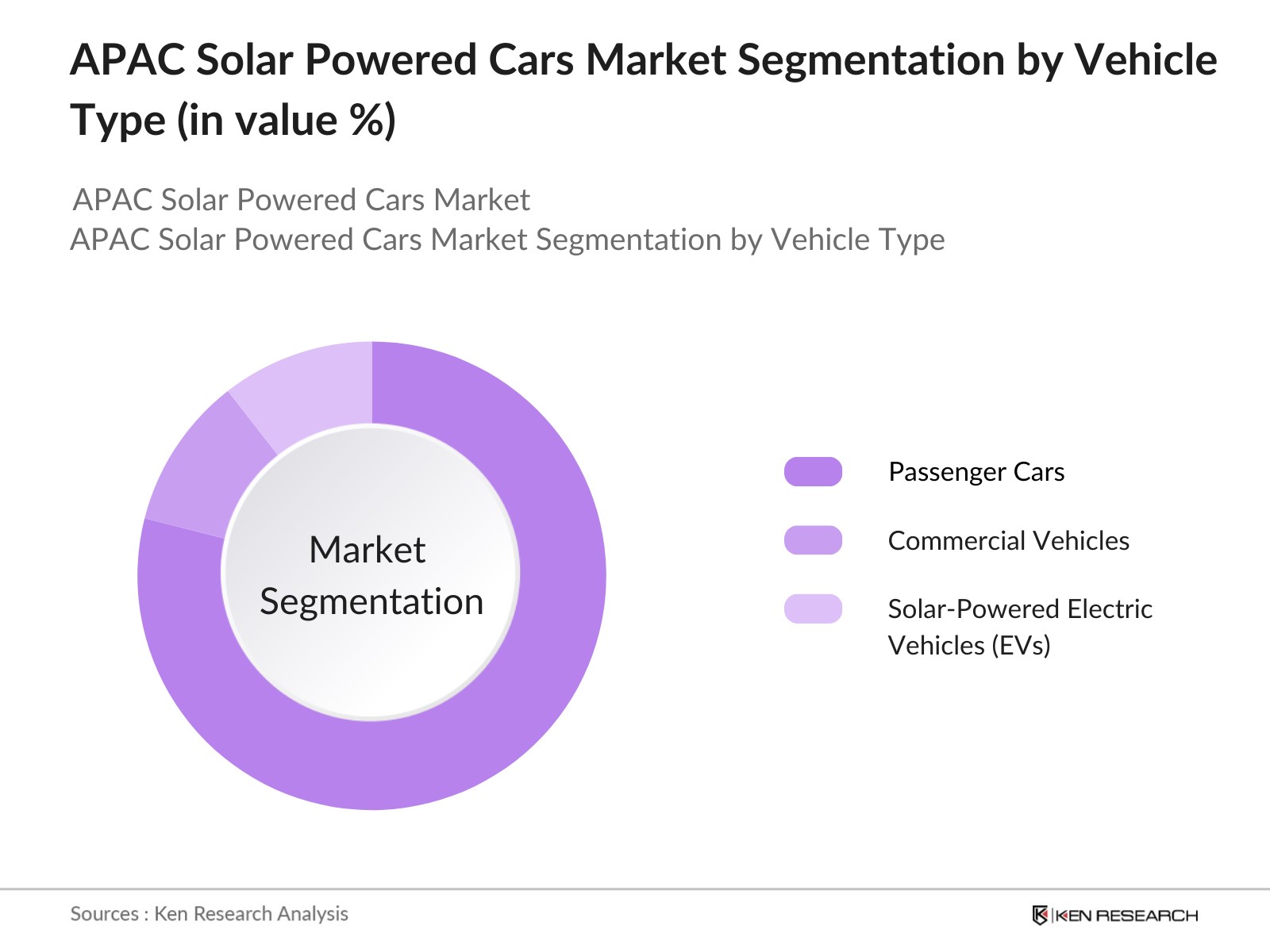

By Vehicle Type: The APAC Solar Powered Cars market is segmented by vehicle type into Passenger Cars, Commercial Vehicles, and Solar-Powered Electric Vehicles (EVs). Among these, Passenger Cars hold a dominant market share due to the high demand for personal mobility solutions and increasing consumer preference for eco-friendly transportation. The growing interest in reducing dependence on fossil fuels and reducing vehicle emissions has further driven the demand for solar-powered passenger cars, especially in urban areas.

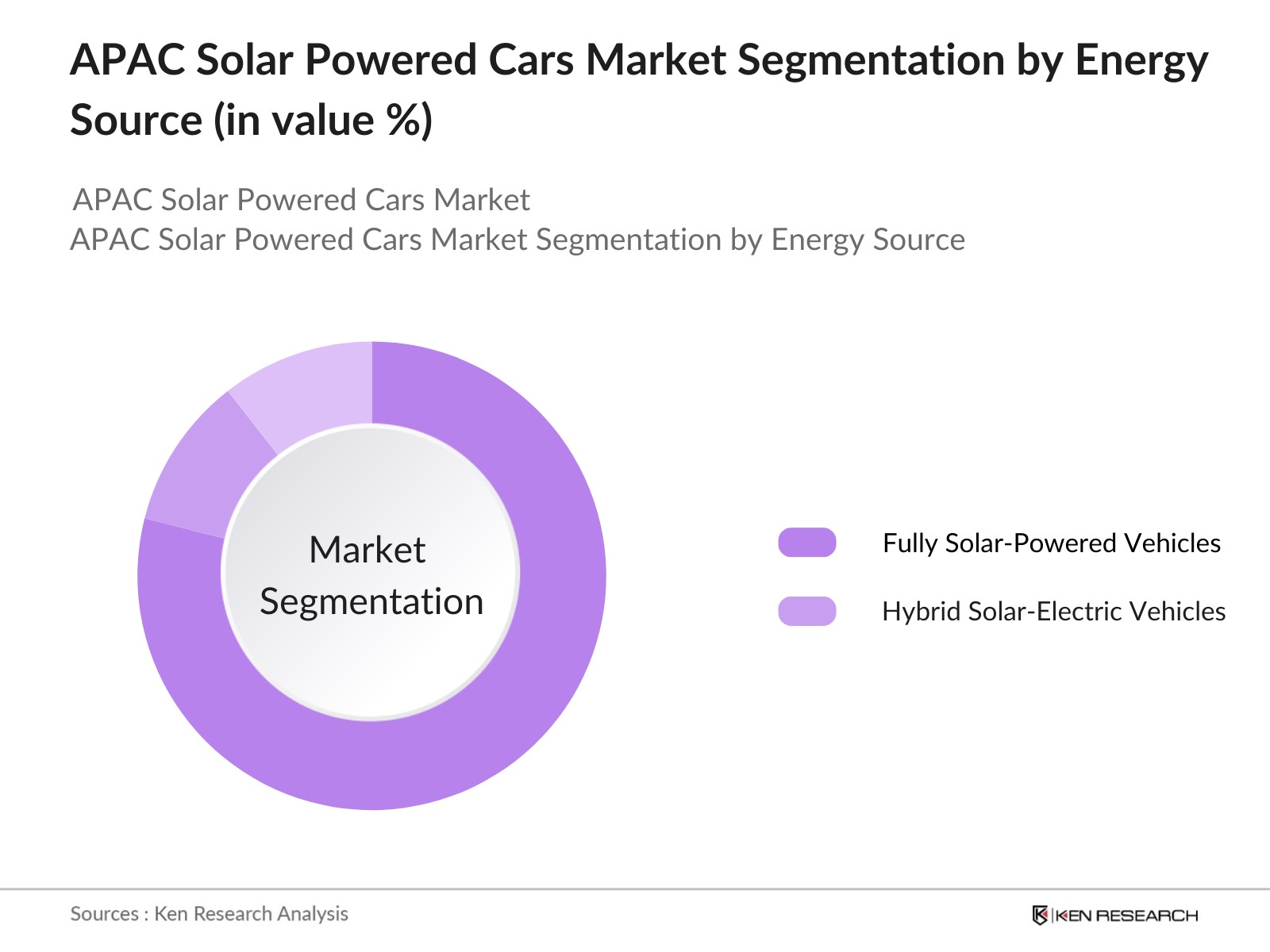

By Energy Source: The market is further segmented by energy source into Fully Solar-Powered Vehicles and Hybrid Solar-Electric Vehicles. Hybrid Solar-Electric Vehicles dominate this segment as they offer a balance between solar energy and electric charging, ensuring more practical usability in regions where sunlight is not always abundant. The combination of solar power with electric battery storage enables longer travel ranges, making hybrid vehicles a preferred option for consumers and fleet operators alike.

The APAC Solar Powered Cars market is dominated by both local and global players. The presence of key automotive manufacturers and the rising investments in solar technology R&D have led to intense competition within the market. Companies are focusing on enhancing vehicle performance through innovations in solar panel efficiency and battery storage. Partnerships and collaborations with solar panel manufacturers have also become common, allowing automakers to integrate advanced solar technologies into their vehicles.

Over the next five years, the APAC Solar Powered Cars market is expected to experience substantial growth, driven by continuous advancements in solar panel technologies, government initiatives supporting green mobility, and increasing consumer demand for eco-friendly vehicles. The market will also benefit from the expansion of EV infrastructure, which is essential for the wider adoption of solar-powered cars. As battery storage systems improve, the practicality of solar-powered vehicles will increase, further boosting market growth.

|

Segments |

Sub-Segments |

|

Vehicle Type |

Passenger Cars Commercial Vehicles Solar-Powered Electric Vehicles (EVs) |

|

Technology |

Solar Cells Efficiency Technology Battery Storage Systems Photovoltaic (PV) Integration |

|

Application |

Personal Mobility Urban Mobility Services Commercial Fleet Deployment |

|

Energy Source |

Fully Solar-Powered Vehicles Hybrid Solar-Electric Vehicles |

|

Region |

China Japan South Korea Australia Southeast Asia |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate (Solar car adoption rate, EV market penetration, solar energy harnessing technology, sustainable mobility demand)

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones (Technology integration, new product launches, infrastructure expansion)

3.1. Growth Drivers

3.1.1. Increasing Demand for Sustainable Mobility

3.1.2. Government Policies Promoting Clean Energy (Incentives, subsidies, green mobility targets)

3.1.3. Technological Advancements in Solar Energy and Battery Efficiency

3.1.4. Rising Investments in Electric Vehicle Infrastructure

3.2. Market Challenges

3.2.1. High Initial Cost of Solar Cars

3.2.2. Limited Solar Energy Capture Efficiency

3.2.3. Lack of Standardized Charging Infrastructure

3.2.4. Dependency on Weather Conditions

3.3. Opportunities

3.3.1. Growth of Solar-Powered Charging Stations

3.3.2. Expansion into Developing Economies

3.3.3. Innovations in Solar Panel Efficiency

3.3.4. Integration with Autonomous Vehicles

3.4. Trends

3.4.1. Increased Focus on Solar-EV Hybrids

3.4.2. Collaboration between Automakers and Solar Panel Manufacturers

3.4.3. Growth of Battery Storage Solutions

3.4.4. Adoption of Solar Cars for Urban Mobility

3.5. Government Regulations

3.5.1. Emission Reduction Targets

3.5.2. Renewable Energy Quotas for Automakers

3.5.3. Carbon Tax Incentives

3.5.4. Vehicle Safety Standards for Solar Cars

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competitive Landscape

4.1. By Vehicle Type (In Value %)

4.1.1. Passenger Cars

4.1.2. Commercial Vehicles

4.1.3. Solar-Powered Electric Vehicles (EVs)

4.2. By Technology (In Value %)

4.2.1. Solar Cells Efficiency Technology

4.2.2. Battery Storage Systems

4.2.3. Photovoltaic (PV) Integration

4.3. By Application (In Value %)

4.3.1. Personal Mobility

4.3.2. Urban Mobility Services (Ride-hailing, car sharing)

4.3.3. Commercial Fleet Deployment

4.4. By Energy Source (In Value %)

4.4.1. Fully Solar-Powered Vehicles

4.4.2. Hybrid Solar-Electric Vehicles

4.5. By Region (In Value %)

4.5.1. China

4.5.2. Japan

4.5.3. South Korea

4.5.4. Australia

4.5.5. Southeast Asia

5.1 Detailed Profiles of Major Companies

5.1.1. Tesla, Inc.

5.1.2. Toyota Motor Corporation

5.1.3. Lightyear

5.1.4. Sono Motors

5.1.5. Hyundai Motor Company

5.1.6. Nissan Motor Co., Ltd.

5.1.7. Aptera Motors

5.1.8. Fisker Inc.

5.1.9. Mahindra Electric

5.1.10. Ford Motor Company

5.1.11. General Motors

5.1.12. Audi AG

5.1.13. BYD Auto

5.1.14. Volkswagen AG

5.1.15. Honda Motor Co., Ltd.

5.2 Cross Comparison Parameters (No. of Employees, Headquarters, Solar-Powered Car Models, Revenue, Market Share, Technological Collaborations, R&D Investment, Global Reach)

5.3. Market Share Analysis

5.4. Strategic Initiatives (Joint Ventures, Product Launches, Technological Partnerships)

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Government Grants and Funding

5.8. Venture Capital Investments

5.9. Private Equity Investments

6.1. Environmental Standards for Solar Vehicles

6.2. Compliance Requirements for Solar Car Manufacturing

6.3. Certification Processes for Solar-Powered Vehicles

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth (Solar energy developments, government push for sustainability, EV market expansion)

8.1. By Vehicle Type (In Value %)

8.2. By Technology (In Value %)

8.3. By Application (In Value %)

8.4. By Energy Source (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives for Solar Car Adoption

9.4. White Space Opportunity Analysis

The initial phase involves constructing a detailed ecosystem map, identifying all key stakeholders in the APAC Solar Powered Cars market. This step utilizes both primary and secondary research, relying on a combination of databases and proprietary resources to gather industry-specific data.

This phase involves analyzing historical data, including solar car production and sales statistics, to generate a comprehensive market picture. Key metrics such as vehicle penetration, regional adoption rates, and solar energy integration into vehicles are evaluated.

Hypotheses derived from market analysis are validated through consultations with industry experts. CATIS and one-on-one interviews provide direct insights from automakers, solar technology companies, and infrastructure providers, ensuring the accuracy of the data.

The final phase involves synthesizing all collected data into actionable insights. The bottom-up approach, combined with real-world data from vehicle manufacturers, provides a robust analysis of the APAC Solar Powered Cars market.

The APAC Solar Powered Cars market is valued at USD 1.8 billion, driven by technological advancements in solar energy and increasing consumer demand for sustainable mobility solutions.

Challenges include high initial vehicle costs, limited solar energy capture efficiency, and a lack of widespread charging infrastructure, which affects the broader adoption of solar-powered cars in the region.

Key players include Tesla, Toyota Motor Corporation, Lightyear, Sono Motors, and Hyundai Motor Company, all of which dominate through technological innovations and strong market presence.

The market is propelled by the rising adoption of electric vehicles, government incentives for clean energy, and advancements in solar panel and battery technologies, making solar-powered vehicles more feasible for mass production.

The market is set to grow significantly due to increasing investments in EV infrastructure, improvements in solar power efficiency, and the growing consumer preference for eco-friendly transport options.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.