APAC Surgical Drains Market Outlook to 2030

Region:Asia

Author(s):Meenakshi Bisht

Product Code:KROD8561

December 2024

99

About the Report

APAC Surgical Drains Market Overview

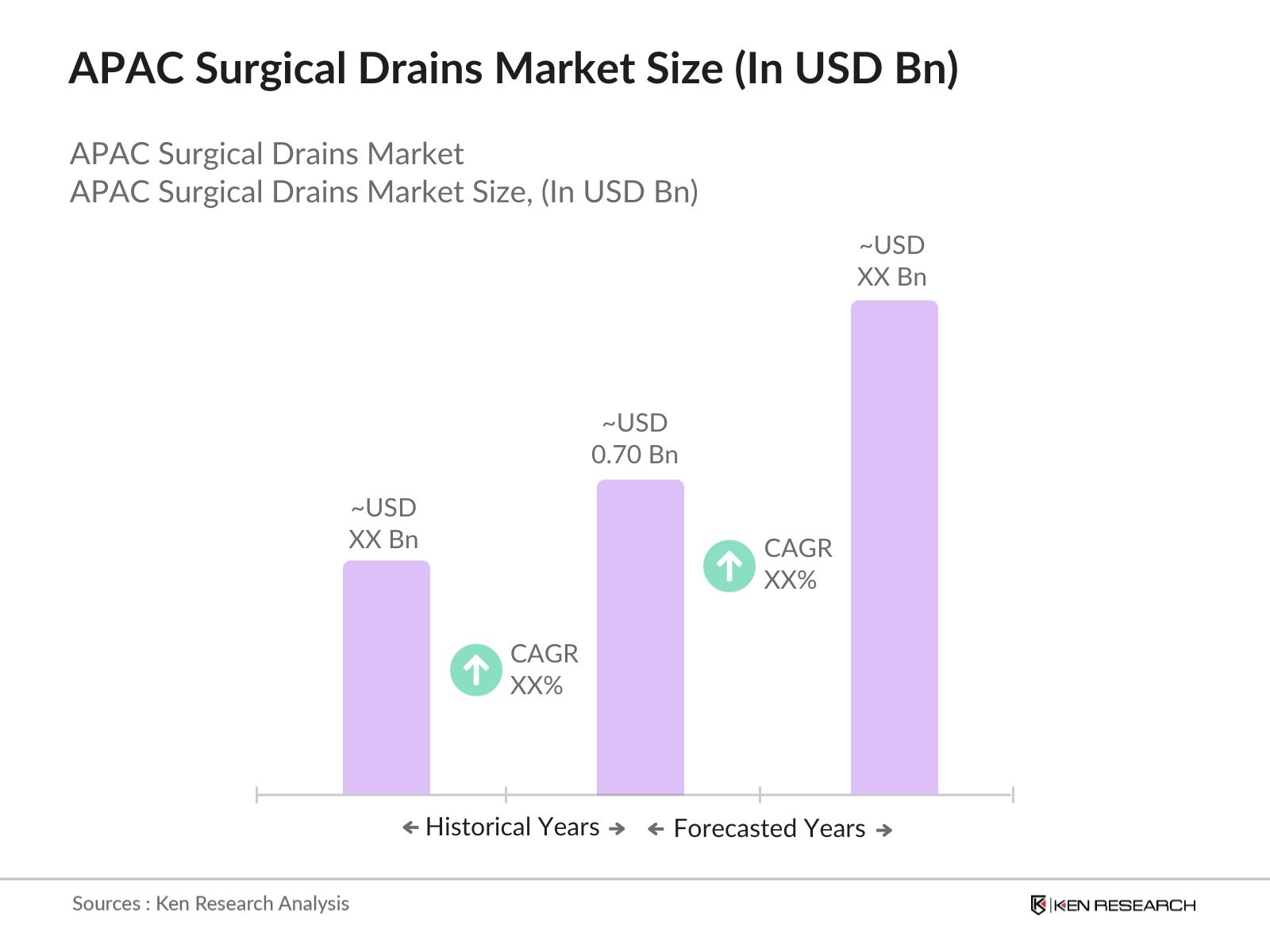

- The APAC Surgical Drains Market is valued at USD 0.70 billion, based on a five-year historical analysis. The market's growth is primarily driven by the increasing number of surgical procedures across the region, driven by a growing aging population, advancements in healthcare infrastructure, and rising awareness about post-surgical complications. The adoption of advanced surgical technologies and innovations in drainage systems, such as closed suction drains, has enhanced patient recovery rates, which further fuels market demand.

- China and India dominate the APAC Surgical Drains Market due to their large population bases and rapidly expanding healthcare infrastructure. China's dominance is attributed to its robust hospital networks and government investment in healthcare. India, on the other hand, benefits from its growing medical tourism industry, which attracts patients from around the world for complex surgical procedures. Additionally, Japan is a key player owing to its advanced medical technology and a high focus on R&D in surgical care.

- APAC countries have implemented stringent health and safety standards for medical devices, impacting the surgical drains market. Australia, through the TGA, enforced compliance with ISO 13485 standards for surgical drains in 2023, ensuring high quality and safety. These standards are crucial for maintaining patient safety but can delay the introduction of new products.

APAC Surgical Drains Market Segmentation

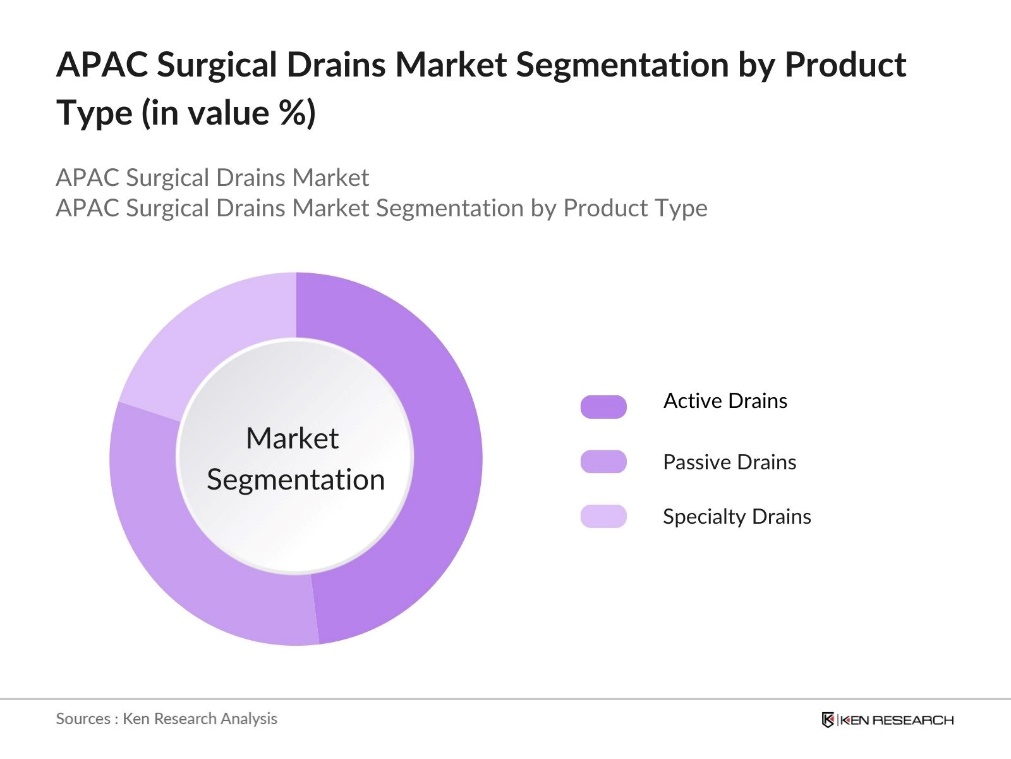

By Product Type: The APAC Surgical Drains Market is segmented by product type into active drains, passive drains, and specialty drains, such as hemostatic, biliary, and chest drains. Active drains hold a dominant market share under this segmentation due to their ability to provide consistent negative pressure, which aids in effective fluid removal. This reduces the risk of infections and accelerates healing, making them highly preferred in complex surgeries like cardiac and neurosurgery. Active drains are widely adopted in countries like Japan and South Korea, where precision in post-operative care is paramount.

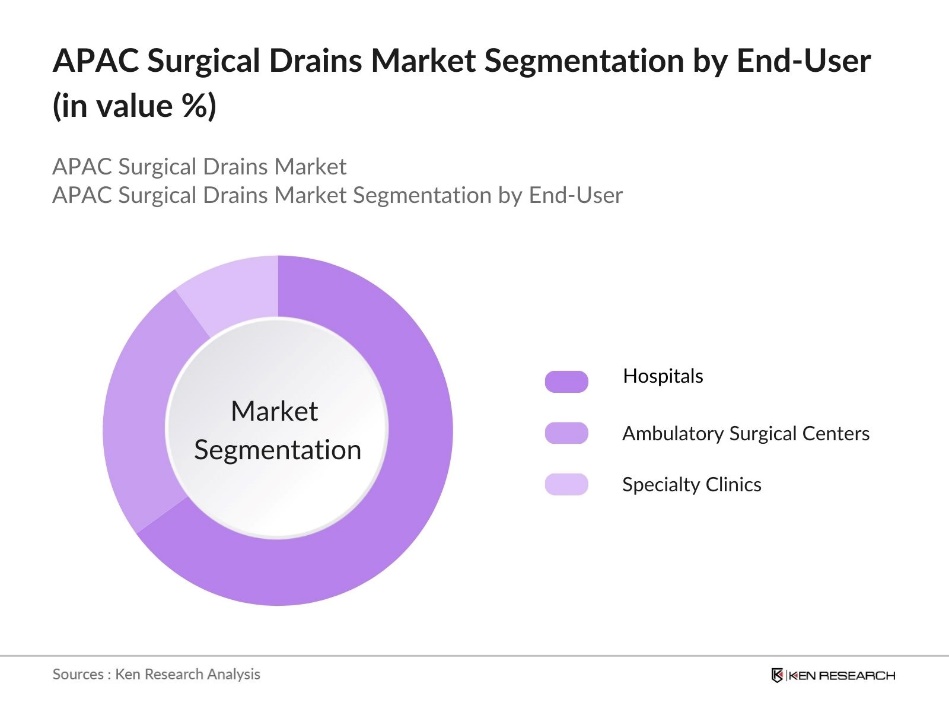

By End-User: The APAC Surgical Drains Market is segmented by end-user into hospitals, ambulatory surgical centers, and specialty clinics. Hospitals account for the largest market share in this segment, driven by their ability to handle complex surgical procedures and provide intensive post-operative care. Hospitals in major cities like Beijing, Tokyo, and Mumbai have state-of-the-art facilities and are equipped with advanced surgical drainage systems. The comprehensive care provided in these settings makes them the preferred choice for patients undergoing major surgeries, further bolstering the demand for surgical drains.

APAC Surgical Drains Market Competitive Landscape

The market is characterized by a blend of global medical device giants and regional manufacturers. The competitive landscape is shaped by product innovation, strategic partnerships with hospitals, and localized production facilities that cater to specific regional needs.

|

Company |

Establishment Year |

Headquarters |

Product Range |

R&D Focus |

Revenue (USD Bn) |

Market Penetration |

Local Partnerships |

Product Launches |

Manufacturing Facilities |

|

B. Braun Melsungen AG |

1839 |

Germany |

|||||||

|

Johnson & Johnson (Ethicon) |

1886 |

USA |

|||||||

|

Medtronic Plc |

1949 |

Ireland |

|||||||

|

Stryker Corporation |

1941 |

USA |

|||||||

|

Romsons Group |

1952 |

India |

APAC Surgical Drains Industry Analysis

Growth Drivers

- Increasing Number of Surgeries: The demand for surgical drains in the APAC region is driven by the rising number of surgeries. The aging population in countries like Japan, where 29.1% of the population is above 65 years, is further driving surgical procedures. India, with its expanding healthcare infrastructure in 2023, supported by increasing health insurance coverage and government initiatives to boost healthcare access.

- Rising Awareness of Post-Surgical Care: Awareness campaigns regarding post-surgical care have led to the adoption of surgical drains to prevent complications. In South Korea, new surgical guidelines introduced by the Korean Society of Surgery in 2023 emphasize the importance of effective drainage systems in reducing recovery time. These initiatives have played a crucial role in improving patient outcomes and driving the market for surgical drains in the region.

- Growth in Healthcare Infrastructure in APAC: The APAC region has seen significant expansion in healthcare infrastructure, leading to increased demand for surgical drains. Investments in new hospitals, modernization of existing facilities, and cross-border initiatives are enhancing the regions capacity for advanced surgical care. These efforts are focused on improving access to healthcare and adopting modern medical technologies, creating opportunities for the adoption of advanced surgical drainage solutions across the region.

Market Challenges

- High Cost of Advanced Surgical Drains:The adoption of advanced surgical drains in the APAC region is limited due to high costs. The expense of advanced closed drainage systems can restrict their availability, particularly in smaller healthcare centers and rural areas. These financial barriers often result in the continued use of traditional systems, as many healthcare providers face budget constraints, limiting the widespread adoption of newer, more effective drainage solutions.

- Stringent Regulatory Approvals: Strict regulatory frameworks in APAC countries create challenges for introducing new surgical drain technologies. Lengthy approval processes and requirements for extensive clinical trials can delay market entry for manufacturers. These regulations ensure product safety but often slow the availability of innovative devices to healthcare providers, impacting the speed at which new technologies can reach the market and improve patient care.

APAC Surgical Drains Market Future Outlook

The APAC Surgical Drains Market is expected to witness significant growth over the next five years, driven by a combination of rising surgical procedures, technological advancements in surgical drainage systems, and increased healthcare spending across the region. Governments in major APAC countries are making substantial investments in healthcare infrastructure, particularly in rural areas, which is expected to improve access to surgical care. Additionally, the focus on minimally invasive surgeries, which often require specialized drainage systems, will further drive demand in the market.

Market Opportunities

- Expansion into Emerging Markets: Emerging markets in the APAC region offer significant growth opportunities for the surgical drains market. With large populations and evolving healthcare systems, these markets present a demand for improved surgical care. Government initiatives aimed at expanding access to healthcare and increasing the number of healthcare facilities are driving this demand. As healthcare infrastructure continues to develop, the need for advanced surgical drainage systems is expected to rise.

- Innovative Drainage Solutions: The development of smart and antimicrobial surgical drains provides new opportunities for manufacturers in the APAC region. These innovative products aim to enhance patient care by reducing infection risks and shortening recovery times. Investments in technology, such as sensors for real-time monitoring, are being integrated into drainage systems, aligning with the regions focus on adopting advanced medical solutions and improving post-operative outcomes.

Scope of the Report

|

By Product Type |

Active Drains Passive Drains Specialty Drains (Hemostatic, Biliary, Chest) |

|

By Application |

General Surgery Cardiac Surgery Orthopedic Surgery Neurosurgery Plastic and Reconstructive Surgery |

|

By Material |

Silicone PVC Latex |

|

By End-User |

Hospitals Ambulatory Surgical Centers Specialty Clinics |

|

By Region |

China India Japan South Korea ASEAN |

Products

Key Target Audience

Hospitals and Healthcare Facilities

Ambulatory Surgical Centers

Surgical Equipment manufacture

Medical Device Manufacturers

Government and Regulatory Bodies (e.g., National Medical Products Administration, Ministry of Health and Family Welfare)

Investors and venture capital Firms

Banks and Financial Institutions

Companies

Players Mentioned in the Report

B. Braun Melsungen AG

Cardinal Health

ConvaTec Group

Medtronic Plc

Johnson & Johnson (Ethicon)

Stryker Corporation

Cook Medical

Redax S.p.A.

Romsons Group

Zimmer Biomet

Table of Contents

1. APAC Surgical Drains Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. APAC Surgical Drains Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. APAC Surgical Drains Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Number of Surgeries (surgery statistics, healthcare expansion, aging population)

3.1.2. Advances in Surgical Drainage Technologies (technological innovation, R&D focus)

3.1.3. Rising Awareness of Post-Surgical Care (health awareness programs, surgical guidelines)

3.1.4. Growth in Healthcare Infrastructure in APAC (public and private investments, government support)

3.2. Market Challenges

3.2.1. High Cost of Advanced Surgical Drains (cost analysis, impact on small healthcare centers)

3.2.2. Stringent Regulatory Approvals (market entry barriers, compliance requirements)

3.2.3. Low Adoption Rates in Developing Countries (market penetration, accessibility issues)

3.3. Opportunities

3.3.1. Expansion into Emerging Markets (regional insights, potential growth)

3.3.2. Innovative Drainage Solutions (smart drains, antimicrobial technologies)

3.3.3. Collaborations Between Medical Device Companies and Healthcare Providers (strategic partnerships)

3.4. Trends

3.4.1. Increased Adoption of Closed Drain Systems (market shift, patient outcomes)

3.4.2. Integration of AI in Post-Surgical Care (predictive analytics, monitoring devices)

3.4.3. Customizable Drainage Solutions (patient-specific products, personalized healthcare)

3.5. Government Regulations

3.5.1. Medical Device Regulations in APAC (country-specific regulations, compliance timelines)

3.5.2. Trade Policies and Tariffs (impact on imports/exports, APAC free trade agreements)

3.5.3. Health and Safety Standards (ISO standards, surgical safety protocols)

3.5.4. Market Entry Regulations (local market access, approval processes)

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (hospital networks, surgeons, medical device manufacturers)

3.8. Porters Five Forces (market competitiveness, supplier power, buyer influence)

3.9. Competitive Ecosystem

4. APAC Surgical Drains Market Segmentation

4.1. By Product Type (In Value %)

4.1.1. Active Drains

4.1.2. Passive Drains

4.1.3. Specialty Drains (Hemostatic, Biliary, Chest)

4.2. By Application (In Value %)

4.2.1. General Surgery

4.2.2. Cardiac Surgery

4.2.3. Orthopedic Surgery

4.2.4. Neurosurgery

4.2.5. Plastic and Reconstructive Surgery

4.3. By Material (In Value %)

4.3.1. Silicone

4.3.2. PVC

4.3.3. Latex

4.4. By End-User (In Value %)

4.4.1. Hospitals

4.4.2. Ambulatory Surgical Centers

4.4.3. Specialty Clinics

4.5. By Region (In Value %)

4.5.1. China

4.5.2. India

4.5.3. Japan

4.5.4. South Korea

4.5.5. ASEAN

5. APAC Surgical Drains Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. B. Braun Melsungen AG

5.1.2. Cardinal Health

5.1.3. ConvaTec Group

5.1.4. Medtronic Plc

5.1.5. Johnson & Johnson (Ethicon)

5.1.6. Stryker Corporation

5.1.7. Cook Medical

5.1.8. Redax S.p.A.

5.1.9. Romsons Group

5.1.10. Zimmer Biomet

5.1.11. Merit Medical Systems

5.1.12. Medline Industries

5.1.13. Smith & Nephew

5.1.14. Integra LifeSciences

5.1.15. BD (Becton, Dickinson and Company)

5.2. Cross Comparison Parameters (Product Portfolio, R&D Investment, Geographical Presence, Production Capacity, Market Share, Strategic Partnerships, Acquisition History, Market Leadership)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. APAC Surgical Drains Market Regulatory Framework

6.1. Device Registration and Approval (APAC focus, regulatory bodies)

6.2. Compliance Requirements (CE Marking, FDA Approvals, APAC-specific approvals)

6.3. Certification Processes (quality assurance, ISO standards)

7. APAC Surgical Drains Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth (surgical demand forecasts, innovations in wound care, expanding healthcare access)

8. APAC Surgical Drains Future Market Segmentation

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By Material (In Value %)

8.4. By End-User (In Value %)

8.5. By Region (In Value %)

9. APAC Surgical Drains Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the APAC Surgical Drains Market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, we will compile and analyze historical data pertaining to the APAC Surgical Drains Market. This includes assessing market penetration, the ratio of marketplaces to service providers, and the resultant revenue generation. Furthermore, an evaluation of service quality statistics will be conducted to ensure the reliability and accuracy of the revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses will be developed and subsequently validated through computer-assisted telephone interviews (CATIs) with industry experts representing a diverse array of companies. These consultations will provide valuable operational and financial insights directly from industry practitioners, which will be instrumental in refining and corroborating the market data.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with multiple surgical drain manufacturers to acquire detailed insights into product segments, sales performance, consumer preferences, and other pertinent factors. This interaction will serve to verify and complement the statistics derived from the bottom-up approach, thereby ensuring a comprehensive, accurate, and validated analysis of the APAC Surgical Drains Market.

Frequently Asked Questions

01. How big is the APAC Surgical Drains Market?

The APAC Surgical Drains Market is valued at USD 0.70 billion, driven by a surge in surgical procedures and advancements in drainage technology that improve patient recovery rates.

02. What are the challenges in the APAC Surgical Drains Market?

Challenges in APAC Surgical Drains Market include high regulatory hurdles, especially for new product approvals, and the high costs associated with advanced surgical drain systems that limit accessibility in developing countries.

03. Who are the major players in the APAC Surgical Drains Market?

Key players in APAC Surgical Drains Market include B. Braun Melsungen AG, Johnson & Johnson (Ethicon), Medtronic Plc, Stryker Corporation, and Romsons Group. These companies leverage their R&D capabilities and extensive distribution networks.

04. What drives the growth of the APAC Surgical Drains Market?

The APAC Surgical Drains Market growth is propelled by increasing surgical procedures, growing healthcare awareness, and improvements in post-operative care in emerging economies like China, India, and Japan.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.