Asia- Pacific 5G Small Cell Market Outlook to 2030

Region:Asia

Author(s):Naman Rohilla

Product Code:KROD2883

November 2024

86

About the Report

Asia-Pacific 5G Small Cell Market Overview

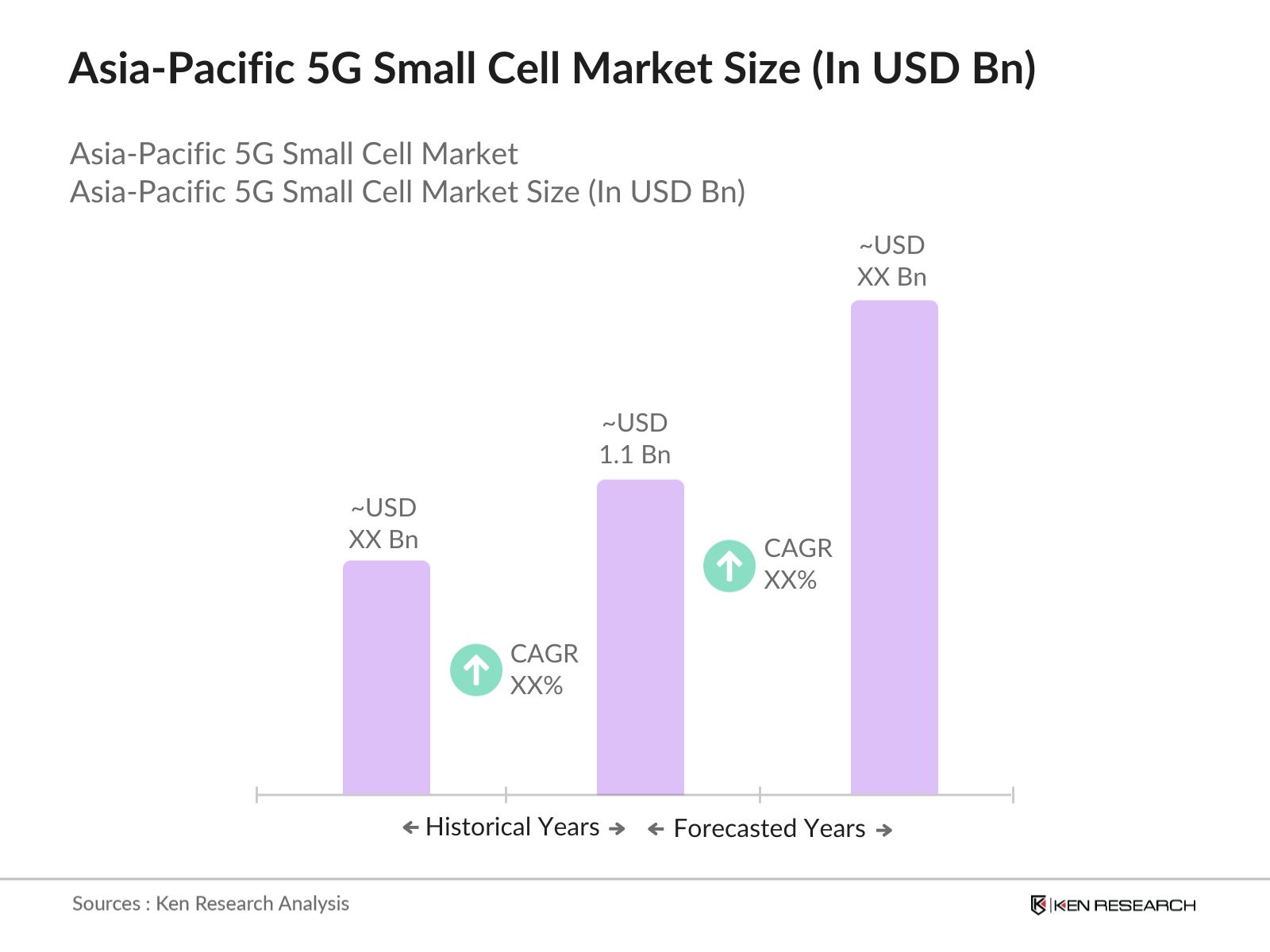

- The Asia-Pacific 5G small cell market is valued at USD 1.1 billion, based on a five-year historical analysis. This market growth is driven by the rapid expansion of 5G network infrastructure across key economies like China, Japan, and South Korea, which have heavily invested in 5G small cell deployments to ensure wider coverage, especially in dense urban areas. The rising demand for enhanced data services, low latency applications, and advanced technologies like IoT and AI integration into industrial automation are also significant market drivers.

- Key countries like China, Japan, and South Korea dominate the 5G small cell market due to their technological advancements and early adoption of 5G infrastructure. China, in particular, leads the charge with massive state-backed investments in 5G infrastructure and aggressive network expansion strategies, making it the largest market in the region. South Korea and Japan follow closely, with a strong focus on smart city projects and telecom collaborations, positioning them as leading players in the market.

- In 2024, Nokia entered discussions with Bharti Airtel to secure a multi-billion dollar contract for supplying 5G telecom equipment in India. This potential deal aims to enhance Airtel's 5G network expansion, reflecting the growing demand for small cell 5G solutions in the Asia-Pacific region. Nokia's AirScale mobile radios, which support 5G-Advanced and reduce energy costs, are central to this agreement. This development underscores the accelerating deployment of 5G infrastructure across Asia-Pacific.

Asia-Pacific 5G Small Cell Market Segmentation

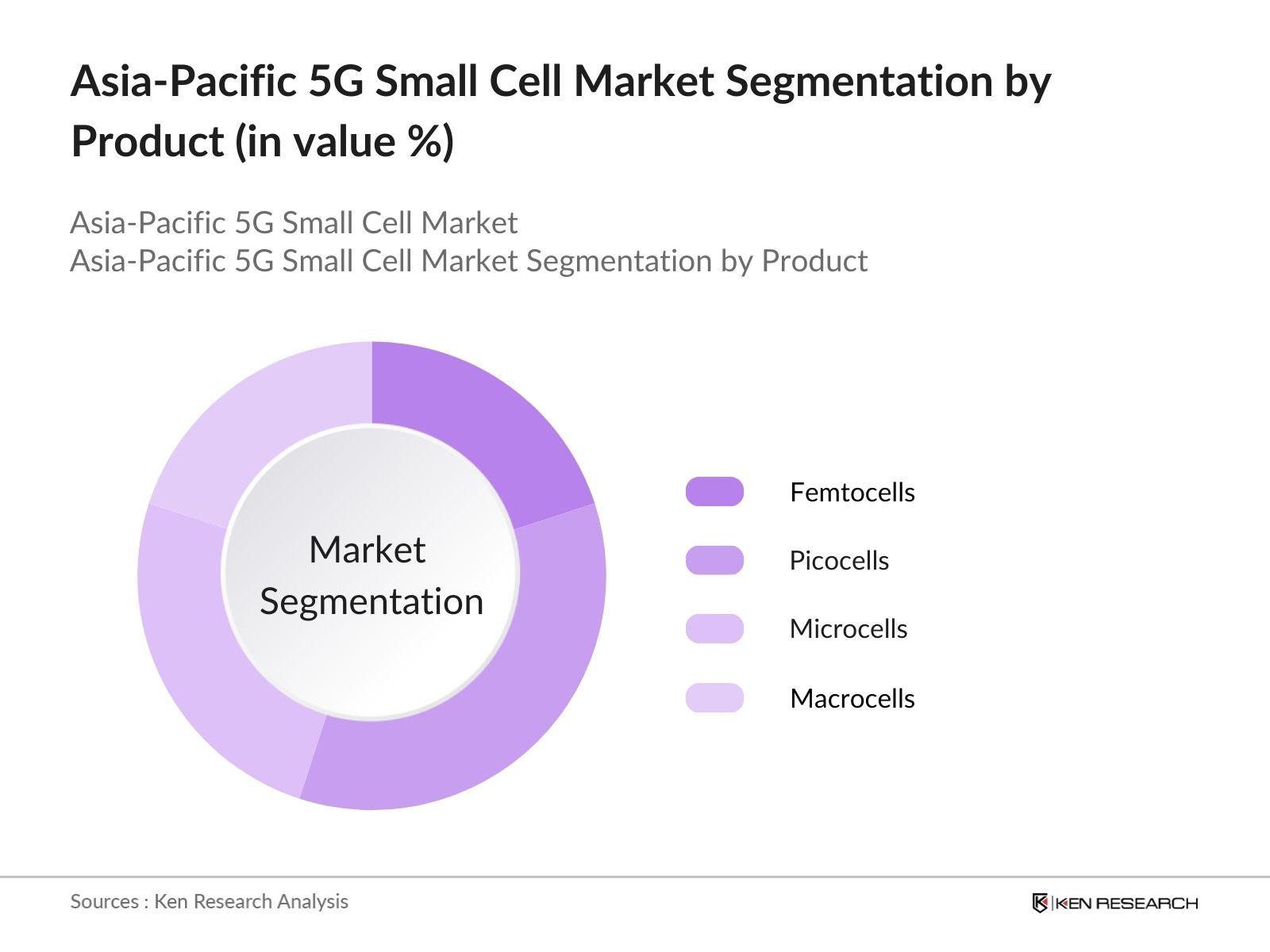

By Product: The Asia-Pacific 5G small cell market is segmented by Product into femtocells, picocells, microcells, and macrocells. Recently, picocells have a dominant market share under the Product segmentation due to their extensive use in indoor coverage solutions, such as offices and enterprise buildings. With the rise in demand for better indoor connectivity and their small form factor, picocells offer a cost-effective solution for mobile operators looking to enhance network capacity in high-density areas.

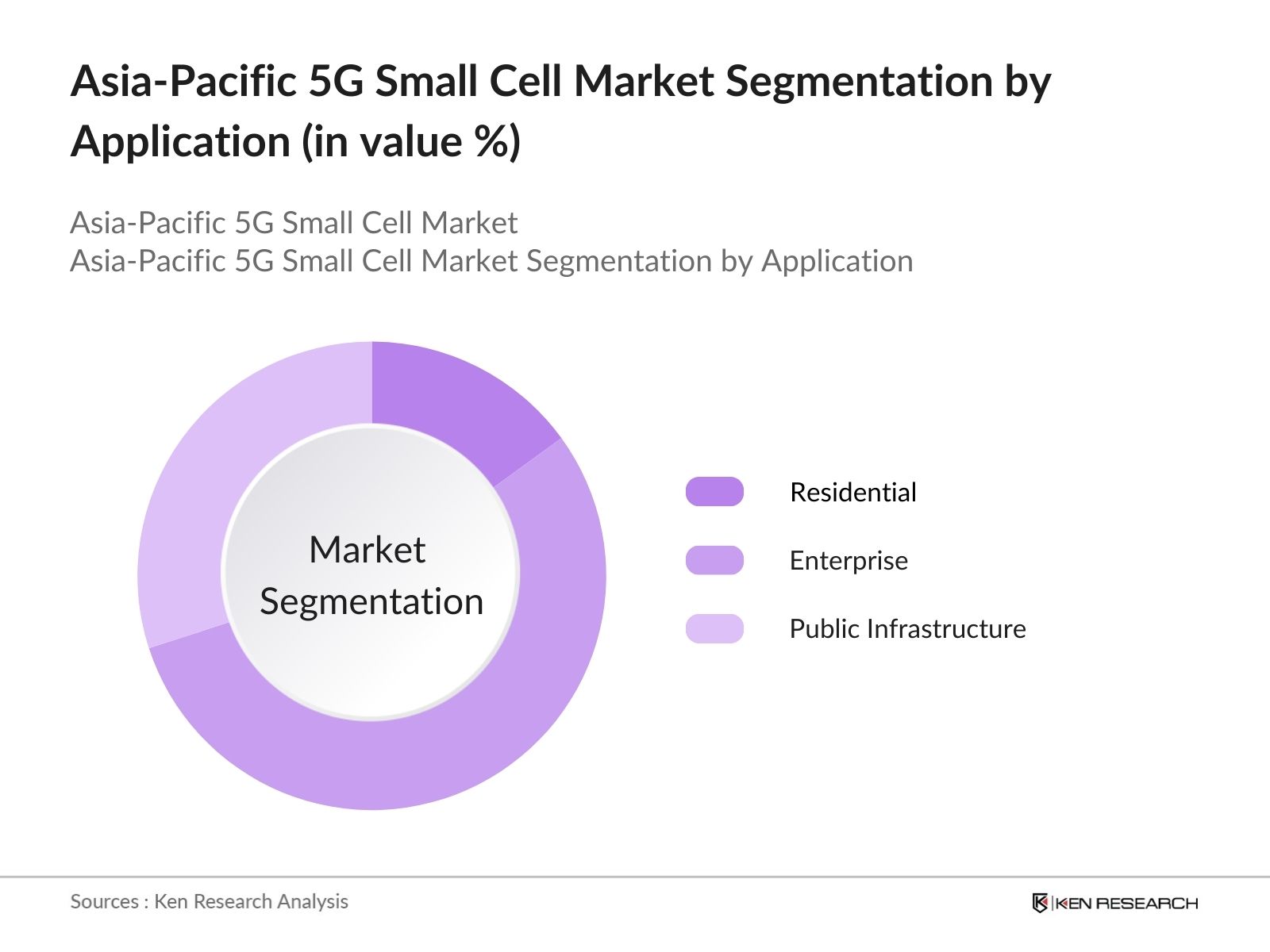

By Application: The Asia-Pacific 5G small cell market is also segmented by application into residential, enterprise, and public infrastructure (including smart city deployments and transport hubs). The enterprise segment dominates the market, as enterprises are increasingly investing in private 5G networks to support automation, IoT applications, and improved internal communications. This trend is particularly strong in the manufacturing and logistics sectors, where ultra-low latency and high-speed networks are essential for operational efficiency.

Asia-Pacific 5G Small Cell Market Competitive Landscape

The Asia-Pacific 5G small cell market is characterized by a concentration of both regional and international players. Key companies in this space include large telecom equipment manufacturers and network solution providers that have established themselves through strong partnerships with mobile network operators and government bodies. The market sees consolidation driven by a few major players, with ongoing efforts to capture market share through product innovations and aggressive 5G deployment strategies.

|

Company Name |

Establishment Year |

Headquarters |

5G Product Portfolio |

R&D Investments (USD Mn) |

Key Telecom Partnerships |

Market Presence |

Patent Holdings |

Company Name |

|

Huawei Technologies Co., Ltd. |

1987 |

Shenzhen, China |

- |

- |

- |

- |

- |

- |

|

Nokia Corporation |

1865 |

Espoo, Finland |

- |

- |

- |

- |

- |

- |

|

Ericsson AB |

1876 |

Stockholm, Sweden |

- |

- |

- |

- |

- |

- |

|

Samsung Electronics Co., Ltd. |

1938 |

Suwon, South Korea |

- |

- |

- |

- |

- |

- |

|

ZTE Corporation |

1985 |

Shenzhen, China |

- |

- |

- |

- |

- |

- |

Asia-Pacific 5G Small Cell Market Analysis

Asia-Pacific 5G Small Cell Market Growth Drivers:

- Increasing Data Traffic Demand: The exponential rise in data traffic is one of the key drivers for the 5G small cell market in Asia-Pacific. As of 2023, global mobile data traffic reached approximately 93 exabytes per month, driven by higher video consumption and the growth of cloud-based applications. This surge in data demand is particularly significant in urban regions, where 5G small cells are essential to boost network capacity. According to the International Telecommunication Union (ITU), Asia-Pacific alone is expected to account for more than 50% of global mobile data consumption by 2025, emphasizing the need for small-cell infrastructure.

- Growing 5G Infrastructure Investments: Asia-Pacific nations are significantly increasing their investments in 5G infrastructure, driven by the need for enhanced connectivity. According to the World Bank, countries such as China and South Korea allocated over $20 billion in 2023 to support 5G network deployments. China's "New Infrastructure Plan" aims to install over 3 million 5G base stations by 2025, boosting the demand for small cells to complement macro towers in dense urban environments. South Korea's similar investments in 5G-related projects further underline the regions strong push towards next-gen network infrastructure.

- Adoption of IoT and Smart Cities Initiatives: The growing adoption of IoT technologies and smart city initiatives is bolstering the demand for 5G small cells. Governments across Asia-Pacific are actively promoting smart cities to enhance urban living and boost economic growth. By 2024, the Asia-Pacific region is expected to account for over 40% of global IoT connections, with countries like Japan, China, and Singapore leading the way in smart city development. The deployment of 5G small cells is crucial for managing the increased data loads and ensuring the reliable connectivity required by IoT devices.

Asia-Pacific 5G Small Cell Market Challenges:

- High Deployment Costs: The deployment of 5G small cells comes with significant financial challenges due to the need for dense infrastructure and additional components. According to the World Bank, deploying 5G small cells in urban environments can cost telecom operators around $25,000 per site, including equipment, site acquisition, and power supply. High deployment costs remain a major barrier, especially for operators in developing regions of Asia-Pacific, where financial resources may be limited. Despite these costs, the demand for robust 5G networks in densely populated areas pushes the deployment forward, albeit at a slower pace.

- Limited Fiber Infrastructure in Rural Areas: Rural areas across Asia-Pacific face limited fiber infrastructure, creating challenges for 5G small cell deployment. Fiber-optic backhaul is essential for the efficient functioning of 5G small cells, yet many developing nations in the region have insufficient fiber coverage. According to the Asian Development Bank, as of 2023, less than 35% of rural regions in Southeast Asia have access to high-speed fiber networks. This lack of connectivity hinders the extension of 5G services beyond urban centers, creating a digital divide that slows overall regional growth.

Asia-Pacific 5G Small Cell Market Future Market Outlook

Over the next five years, the Asia-Pacific 5G small cell market is expected to witness growth, driven by the expansion of 5G networks, continuous infrastructure investments, and the increasing adoption of IoT applications. The integration of 5G with cloud computing, AI, and edge technologies will further enhance its utility across multiple sectors, including healthcare, manufacturing, and smart cities. Additionally, the support of government initiatives aimed at boosting 5G penetration in rural and urban areas will fuel future growth.

Asia-Pacific 5G Small Cell Market Opportunities:

- Integration with Edge Computing and Cloud Infrastructure: The integration of 5G small cells with edge computing and cloud infrastructure presents a significant opportunity for growth. As of 2023, over 30% of businesses in Asia-Pacific are adopting edge computing solutions to support latency-sensitive applications such as autonomous vehicles and industrial automation. This trend is driving the demand for small cell deployments to provide localized, high-speed connectivity. Governments are also investing in edge computing infrastructure, with China alone allocating $1 billion in 2024 for edge network expansion. This creates a strong foundation for future 5G small cell installations.

- 5G Use Cases in Autonomous Vehicles and Industry 4.0: The expanding use of 5G in autonomous vehicles and Industry 4.0 applications provides substantial market opportunities for 5G small cells. By 2023, Asia-Pacific had over 50,000 autonomous vehicles in testing, particularly in China, Japan, and South Korea. Industry 4.0 initiatives, especially in manufacturing hubs like South Korea, are further pushing the adoption of 5G networks to facilitate machine-to-machine communication. The deployment of small cells is critical for ensuring the ultra-low latency required in these applications, providing enhanced connectivity solutions for these emerging sectors.

Scope of the Report

|

By Product |

Femtocells Pico Cells Micro Cells Macro Cells |

|

By Application |

Residential Enterprise Public Infrastructure |

|

By Frequency Band |

Sub-6 GHz mmWave |

|

By Deployment Mode |

Indoor Outdoor |

|

By Region |

China South Korea Japan India Australia Rest of APAC |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Government and Regulatory Bodies

Banks and Financial Institutes

Investors and Venture Capitalists

Mobile Network Operators (MNOs) Companies

5G Equipment Manufacturers

Telecom Infrastructure Providing Companies

IoT Solution Providing Companies

Time Period Captured in the Report

Historical Period: 2018-2023

Base Year: 2023

Forecast Period: 2023-2028

Companies

Players Mentioned in the Report:

Huawei Technologies Co., Ltd.

Nokia Corporation

Ericsson AB

Samsung Electronics Co., Ltd.

ZTE Corporation

Cisco Systems, Inc.

CommScope Inc.

NEC Corporation

Fujitsu Ltd.

Airspan Networks Inc.

Ceragon Networks Ltd.

Alpha Wireless Ltd.

BLiNQ Networks Inc.

Parallel Wireless Inc.

Baicells Technologies Co., Ltd.

Table of Contents

1. Asia-Pacific 5G Small Cell Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Asia-Pacific 5G Small Cell Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis (Based on 5G Network Deployments)

2.3. Key Market Developments and Milestones (5G Spectrum Allocation, Small Cell Rollout)

3. Asia-Pacific 5G Small Cell Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Data Traffic Demand

3.1.2. Growing 5G Infrastructure Investments

3.1.3. Adoption of IoT and Smart Cities Initiatives

3.1.4. Supportive Government Policies (5G Spectrum Licensing, Infrastructure Subsidies)

3.2. Market Challenges

3.2.1. High Deployment Costs

3.2.2. Limited Fiber Infrastructure in Rural Areas

3.2.3. Complex Regulatory Environment (Permitting and Zoning Regulations)

3.3. Opportunities

3.3.1. Integration with Edge Computing and Cloud Infrastructure

3.3.2. 5G Use Cases in Autonomous Vehicles and Industry 4.0

3.3.3. Expansion in Developing Economies

3.4. Trends

3.4.1. Deployment of mmWave Small Cells

3.4.2. Collaboration Between Telecom and Smart City Ecosystems

3.4.3. Growing Demand for Ultra-Low Latency Solutions

3.5. Government Initiatives (Spectrum Auctions, Infrastructure Support Programs)

3.5.1. National 5G Strategies (Key Countries: China, Japan, South Korea)

3.5.2. Public-Private Partnerships (PPP) in Small Cell Infrastructure

3.5.3. Incentives for 5G Network Expansion

3.6. SWOT Analysis (Specific to Small Cell Adoption)

3.7. Stake Ecosystem (Including Mobile Network Operators, Equipment Manufacturers)

3.8. Porters Five Forces (Focus on Telecom and Infrastructure Equipment Vendors)

3.9. Competition Ecosystem (Competitive Dynamics of Major Telecom Providers and Infrastructure Suppliers)

4. Asia-Pacific 5G Small Cell Market Segmentation

4.1. By Product (In Value %)

4.1.1. Femtocells

4.1.2. Pico Cells

4.1.3. Micro Cells

4.1.4. Macro Cells

4.2. By Application (In Value %)

4.2.1. Residential

4.2.2. Enterprise

4.2.3. Public Infrastructure (Smart Cities, Transport Hubs)

4.3. By Frequency Band (In Value %)

4.3.1. Sub-6 GHz

4.3.2. mmWave

4.4. By Deployment Mode (In Value %)

4.4.1. Indoor

4.4.2. Outdoor

4.5. By Region (In Value %)

4.5.1. China

4.5.2. Japan

4.5.3. South Korea

4.5.4. India

4.5.5. Australia

5. Asia-Pacific 5G Small Cell Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Huawei Technologies Co., Ltd.

5.1.2. Nokia Corporation

5.1.3. Ericsson AB

5.1.4. Samsung Electronics Co., Ltd.

5.1.5. ZTE Corporation

5.1.6. Cisco Systems, Inc.

5.1.7. CommScope Inc.

5.1.8. NEC Corporation

5.1.9. Fujitsu Ltd.

5.1.10. Airspan Networks Inc.

5.1.11. Ceragon Networks Ltd.

5.1.12. Alpha Wireless Ltd.

5.1.13. BLiNQ Networks Inc.

5.1.14. Parallel Wireless Inc.

5.1.15. Baicells Technologies Co., Ltd.

5.2. Cross Comparison Parameters (Market Share, 5G Product Portfolio, Deployment Capabilities, R&D Investments)

5.3. Market Share Analysis (By Key Player and Region)

5.4. Strategic Initiatives (Partnerships, Alliances, Joint Ventures)

5.5. Mergers and Acquisitions (Impact on Small Cell Ecosystem)

5.6. Investment Analysis (Capex on 5G Small Cell Rollouts)

5.7. Venture Capital Funding (Start-ups in Small Cell and 5G Technologies)

5.8. Government Grants (Subsidies for 5G Infrastructure Development)

5.9. Private Equity Investments (Infrastructure Funds for 5G Networks)

6. Asia-Pacific 5G Small Cell Market Regulatory Framework

6.1. Telecom Regulations for Small Cell Deployment

6.2. Compliance Requirements (Telecom Equipment Standards)

6.3. Certification Processes (For Small Cell Equipment and Deployment)

7. Asia-Pacific 5G Small Cell Future Market Size (In USD Bn)

7.1. Future Market Size Projections (Forecast Based on 5G Adoption Rate and Capex Plans)

7.2. Key Factors Driving Future Market Growth (AI and IoT Integration, New Use Cases)

8. Asia-Pacific 5G Small Cell Future Market Segmentation

8.1. By Product (In Value %)

8.2. By Application (In Value %)

8.3. By Frequency Band (In Value %)

8.4. By Deployment Mode (In Value %)

8.5. By Region (In Value %)

9. Asia-Pacific 5G Small Cell Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis (Specific to 5G Small Cell Market)

9.2. Customer Cohort Analysis (Enterprise, Consumer, Government Segments)

9.3. Marketing Initiatives (Targeting Telecom Operators, Smart City Planners)

9.4. White Space Opportunity Analysis (Untapped Markets for Small Cells)

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The first phase involved mapping the 5G small cell ecosystem in the Asia-Pacific region. Secondary research using credible sources such as government reports and industry databases helped in identifying the major stakeholders, market influencers, and critical success factors.

Step 2: Market Analysis and Construction

This phase analyzed historical data for the Asia-Pacific 5G small cell market, focusing on deployment trends and market penetration. The collected data was used to estimate market revenues and assess the deployment of 5G small cell solutions across different geographies.

Step 3: Hypothesis Validation and Expert Consultation

Industry experts from telecom companies, network equipment manufacturers, and government bodies were consulted through structured interviews. These interviews provided operational insights and validated market assumptions, ensuring the accuracy of the collected data.

Step 4: Research Synthesis and Final Output

In the final phase, detailed market models were created, incorporating both top-down and bottom-up approaches. These models helped verify the market data across product segments, regional markets, and application areas to deliver an accurate market forecast.

Frequently Asked Questions

01. How big is the Asia-Pacific 5G Small Cell Market?

The Asia-Pacific 5G small cell market is valued at USD 1.1 billion, driven by investments in 5G infrastructure and the growing demand for low-latency applications.

02. What are the challenges in the Asia-Pacific 5G Small Cell Market?

The Asia-Pacific 5G small cell market challenges include the high cost of deployment, regulatory barriers in certain countries, and the need for extensive fibre infrastructure in rural areas.

03. Who are the major players in the Asia-Pacific 5G Small Cell Market?

The Asia-Pacific 5G small cell market key players include Huawei, Nokia, Ericsson, Samsung, and ZTE, all of which have extensive 5G product portfolios and strategic partnerships with telecom operators.

04. What are the growth drivers of the Asia-Pacific 5G Small Cell Market?

The Asia-Pacific 5G small cell market is driven by the growing demand for better network coverage, increased 5G deployment in urban areas, and government support for smart city projects.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.