Asia-Pacific AI Chip Market Outlook to 2030

Region:Afganistan

Author(s):Naman Rohilla

Product Code:KROD2727

Region:Afganistan

Author(s):Naman Rohilla

Product Code:KROD2727

November 2024

90

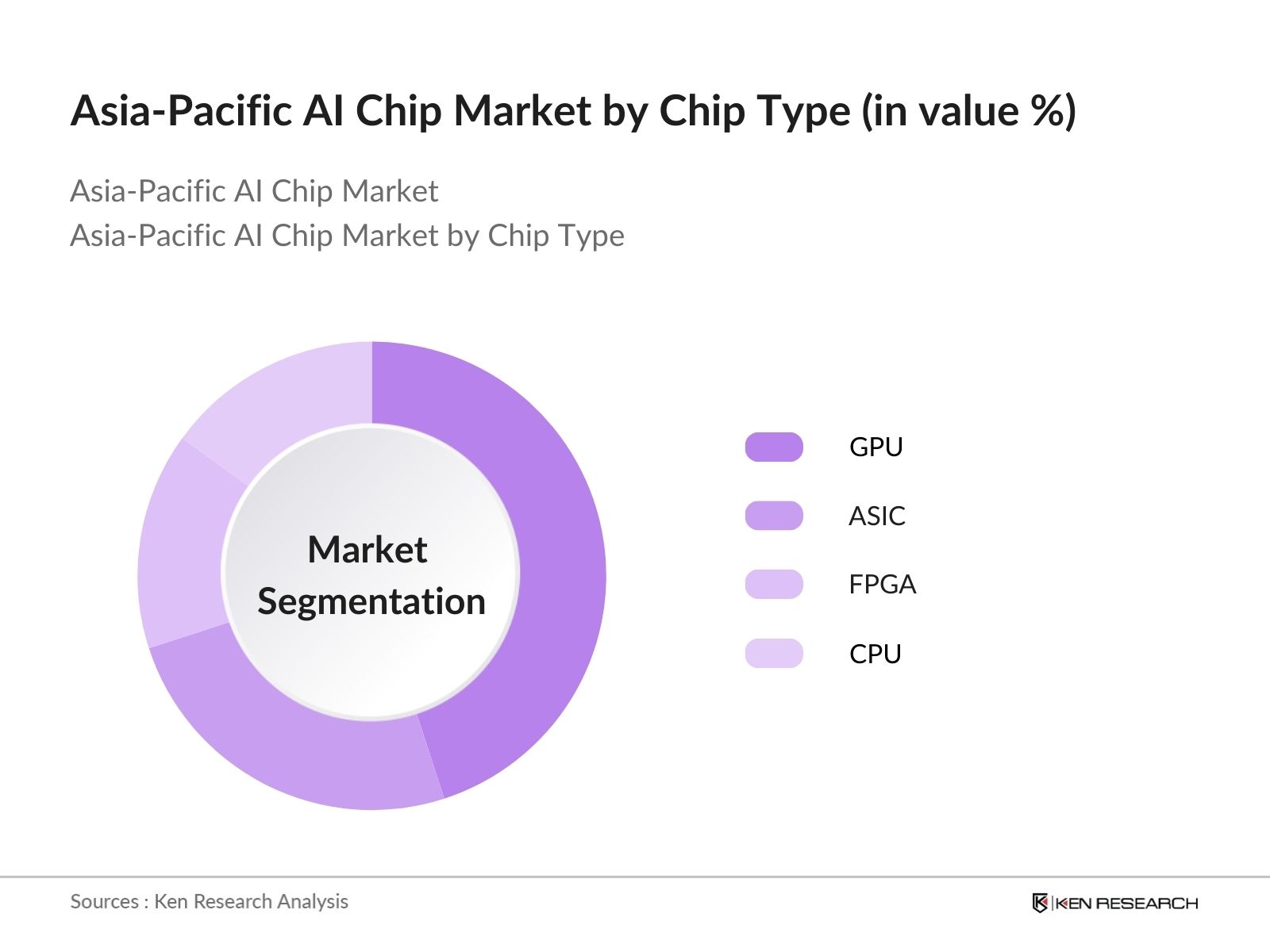

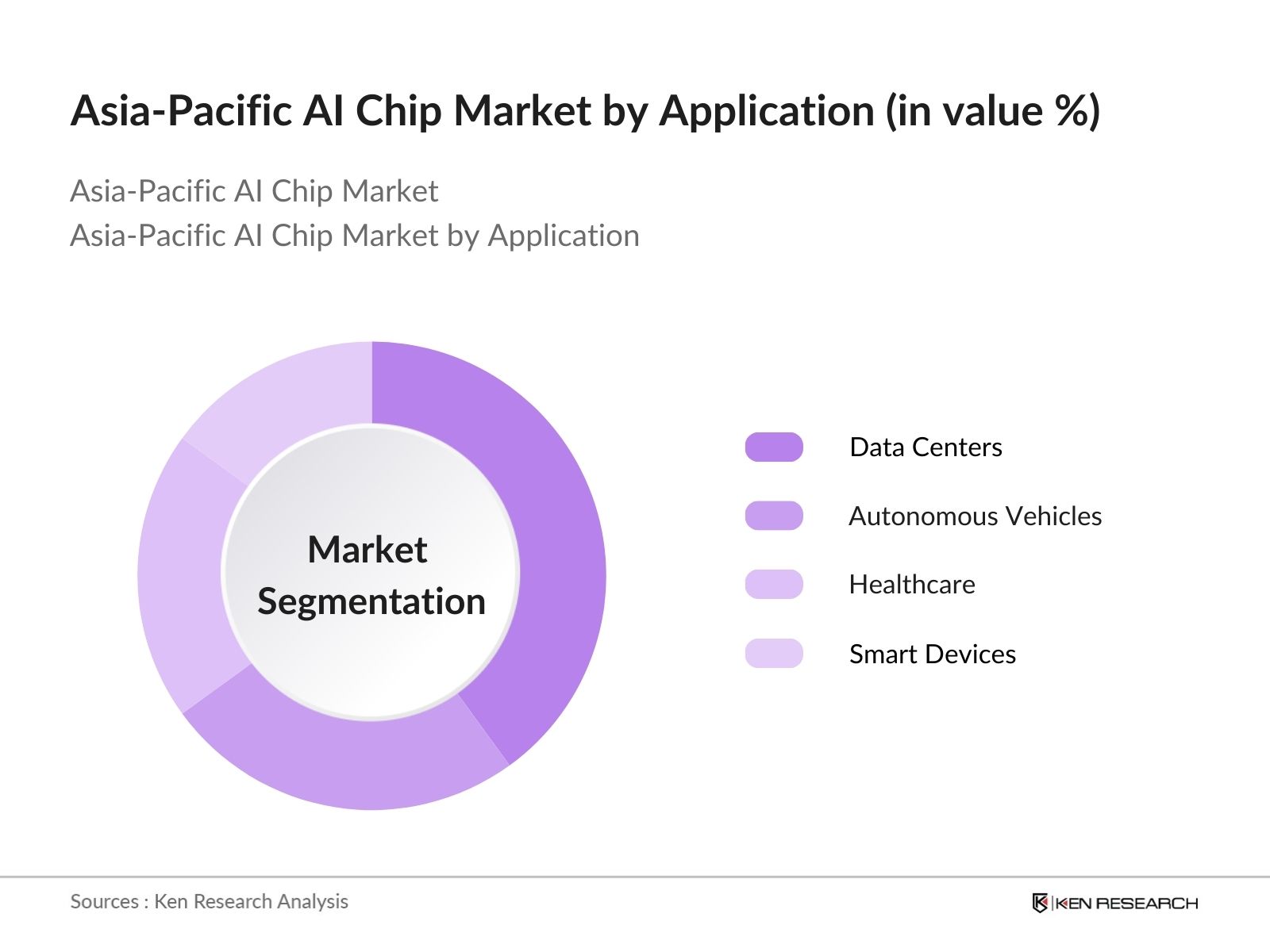

The Asia-Pacific AI Chip Market is segmented by chip type, application, and region.

|

Company |

Establishment Year |

Headquarters |

|

NVIDIA Corporation |

1993 |

Santa Clara, USA |

|

Intel Corporation |

1968 |

Santa Clara, USA |

|

Qualcomm Technologies Inc. |

1985 |

San Diego, USA |

|

Huawei Technologies Co., Ltd. |

1987 |

Shenzhen, China |

|

MediaTek Inc. |

1997 |

Hsinchu, Taiwan |

The Asia-Pacific AI Chip Market is expected to grow steadily over the next five years, driven by the continued adoption of AI and cloud computing technologies. SaaS is predicted to dominate the market, with companies increasingly opting for subscription-based AI chip services. The rise of edge computing, 5G, and the Internet of Things (IoT) will further propel market growth.

|

By Chip Type |

GPU ASIC FPGA CPU |

|

By Application |

Data Centers Autonomous Vehicles Healthcare Smart Devices |

|

By Region |

China Japan South Korea India Australia Rest of APAC |

1.1 Definition and Scope of the Asia-Pacific AI Chip Market

1.2 Market Taxonomy (Chip Type, Application, Region)

1.3 Market Growth Rate and Trends

1.4 Market Drivers (Rising AI Adoption, Government Initiatives, Expansion of AI Infrastructure)

1.5 Market Restraints (High Manufacturing Costs, Data Privacy Concerns)

2.1 Historical Market Size Analysis (2018-2023)

2.2 Year-on-Year Growth Analysis

2.3 Forecast Market Size and Growth Projections (2023-2028)

2.4 Key Market Milestones and Developments

3.1 Growth Drivers

3.1.1 Increasing AI Adoption Across Sectors

3.1.2 Expansion of AI Infrastructure and Government Support

3.1.3 Demand for Edge Computing and AI Chips

3.2 Market Challenges

3.2.1 High Costs of AI Chip Development and Manufacturing

3.2.2 Data Privacy and Security Concerns

3.3 Opportunities

3.3.1 Expansion in Autonomous Vehicles

3.3.2 Development of AI Chips for Healthcare Applications

3.4 Market Trends

3.4.1 Adoption of AI Chips for Edge Computing

3.4.2 Advancements in Quantum AI Chips

4.1 By Chip Type (in Value %)

4.1.1 GPU (Graphics Processing Units)

4.1.2 ASIC (Application-Specific Integrated Circuit)

4.1.3 FPGA (Field-Programmable Gate Array)

4.1.4 CPU (Central Processing Unit)

4.2 By Application (in Value %)

4.2.1 Data Centers

4.2.2 Autonomous Vehicles

4.2.3 Healthcare

4.2.4 Smart Devices

4.3 By Region (in Value %)

4.3.1 China

4.3.2 Japan

4.3.3 South Korea

4.3.4 India

4.3.5 Australia

4.3.6 Rest of APAC

5.1 Competitive Market Share Analysis

5.2 Company Profiles

5.2.1 NVIDIA Corporation (Established 1993, Headquarters: Santa Clara, USA)

5.2.2 Intel Corporation (Established 1968, Headquarters: Santa Clara, USA)

5.2.3 Qualcomm Technologies Inc. (Established 1985, Headquarters: San Diego, USA)

5.2.4 Huawei Technologies Co., Ltd. (Established 1987, Headquarters: Shenzhen, China)

5.2.5 MediaTek Inc. (Established 1997, Headquarters: Hsinchu, Taiwan)

5.2.6 AMD (Advanced Micro Devices, Inc.)

5.2.7 Samsung Electronics Co., Ltd.

5.2.8 Xilinx Inc. (Acquired by AMD)

5.2.9 Graphcore

5.2.10 Cerebras Systems

5.2.11 Cambricon Technologies Corporation

5.2.12 Baidu Inc.

5.2.13 Alibaba Group Holding Ltd. (T-Head)

5.2.14 Fujitsu Limited

5.2.15 Renesas Electronics Corporation

5.3 Strategic Initiatives and Investments

5.4 Recent Mergers and Acquisitions

5.5 Technological Innovations and R&D Investments

6.1 Chinas AI Development Plan for AI Chip Industry

6.2 Japans AI Innovation Strategy (AI Society 5.0)

6.3 South Koreas AI Infrastructure Investment Plans

6.4 Indias AI Policy and Innovation Support

7.1 Market Segmentation by Chip Type (2023-2028)

7.2 Market Segmentation by Application (2023-2028)

7.3 Market Segmentation by Region (2023-2028)

7.4 Future Market Trends (Edge Computing, Quantum Computing, Autonomous Vehicles)

8.1 Advancements in High-Efficiency AI Chips for Edge Computing

8.2 Development of AI Chips for Autonomous Vehicles

8.3 Innovations in Quantum AI Chip Technology

9.1 Key Investments in AI Chip Manufacturing Facilities

9.2 Mergers and Acquisitions in the AI Chip Market

9.3 Government Grants and Funding for AI Infrastructure

9.4 Private Equity and Venture Capital Funding in AI Chip Startups

10.1 Strengths (High Demand in Key Sectors, Government Support for AI Infrastructure)

10.2 Weaknesses (High Manufacturing Costs, Data Privacy Concerns)

10.3 Opportunities (Expansion in Autonomous Vehicles and Smart Devices, Advancements in AI Chip Technology)

10.4 Threats (Global Supply Chain Disruptions, Competitive Market Dynamics)

11.1 Strategic Market Entry and Expansion Opportunities

11.2 Collaboration with AI and Semiconductor Companies

11.3 Innovative Product Development (Advanced AI Chips for Edge Computing and Quantum Computing)

11.4 Market Positioning Strategies for Key Players

Disclaimer Contact UsEcosystem creation for all the major entities and referring to multiple secondary and proprietary databases to perform desk research around the market to collate market-level information.

Collating statistics on the Asia-Pacific AI Chip Market over the years and analyzing the penetration of products as well as the ratio of suppliers to compute the revenue generated for the market. We will also review product quality statistics to ensure accuracy behind the data points shared.

Building market hypotheses and conducting CATIs with market experts from different companies to validate statistics and seek operational and financial information from company representatives.

Our research team approaches multiple AI Chip manufacturers to understand product segments, sales trends, consumer preferences, and other parameters. This approach supports us in validating the statistics derived from the bottom-up approach of these AI Chip manufacturers.

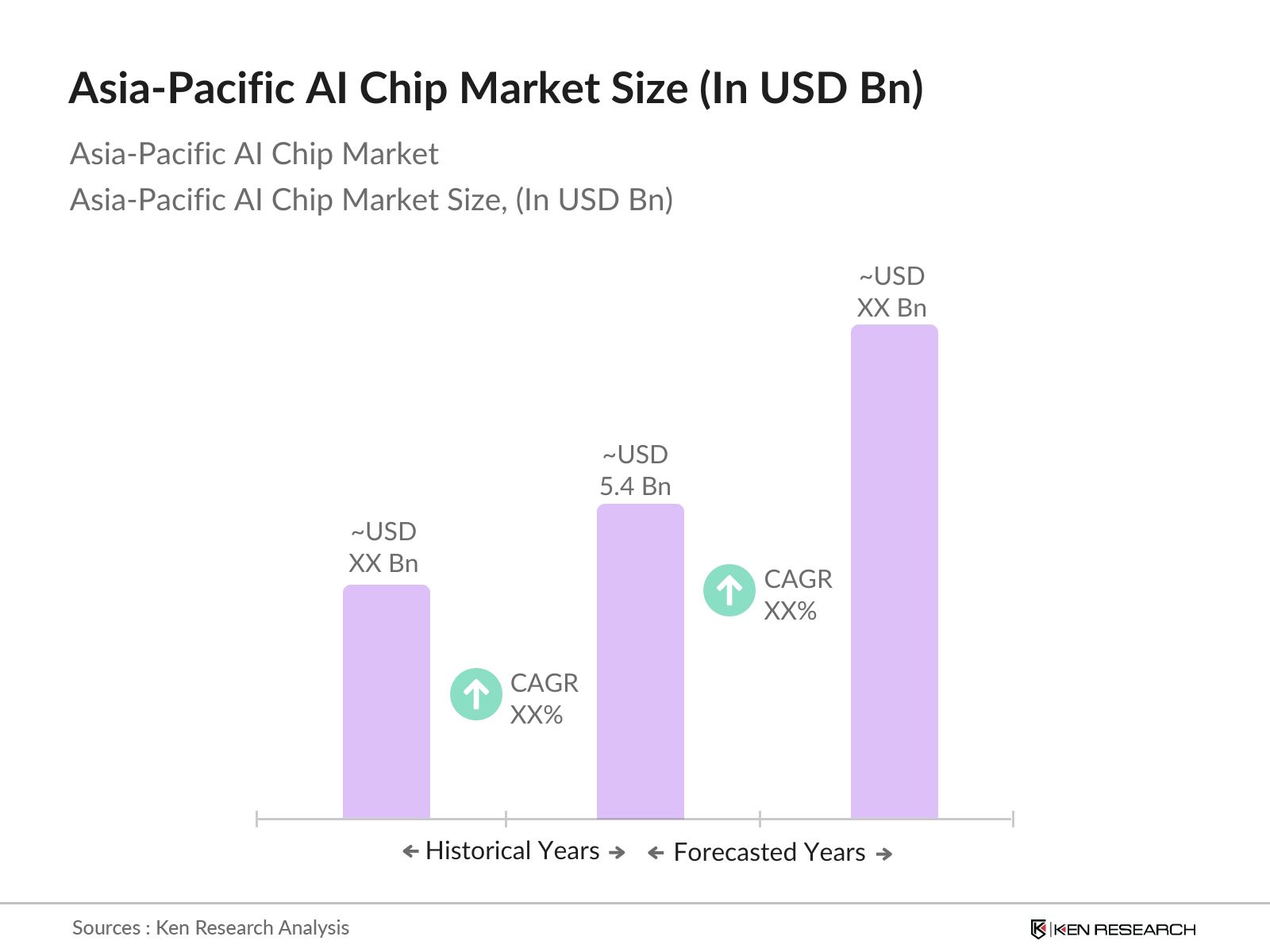

The Asia-Pacific AI Chip Market was valued at USD 5.4 billion, driven by the increasing adoption of AI across industries and substantial investments in AI infrastructure.

Major players in the Asia-Pacific AI Chip Market include NVIDIA Corporation, Intel Corporation, Qualcomm Technologies Inc., Huawei Technologies Co., Ltd., and MediaTek Inc., focusing on AI chip innovation and performance enhancement.

Key growth drivers in the Asia-Pacific AI Chip Market include rising adoption of AI across sectors, government support for AI innovation, and advancements in AI chip technologies for edge computing.

Challenges in the Asia-Pacific AI Chip Market include high manufacturing costs of AI chips and data privacy concerns, particularly in highly regulated markets like Japan and South Korea.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.