Asia Pacific Aircraft Engine Market Outlook to 2030

Region:Asia

Author(s):Shreya

Product Code:KROD2894

October 2024

99

About the Report

Asia Pacific Aircraft Engine Market Overview

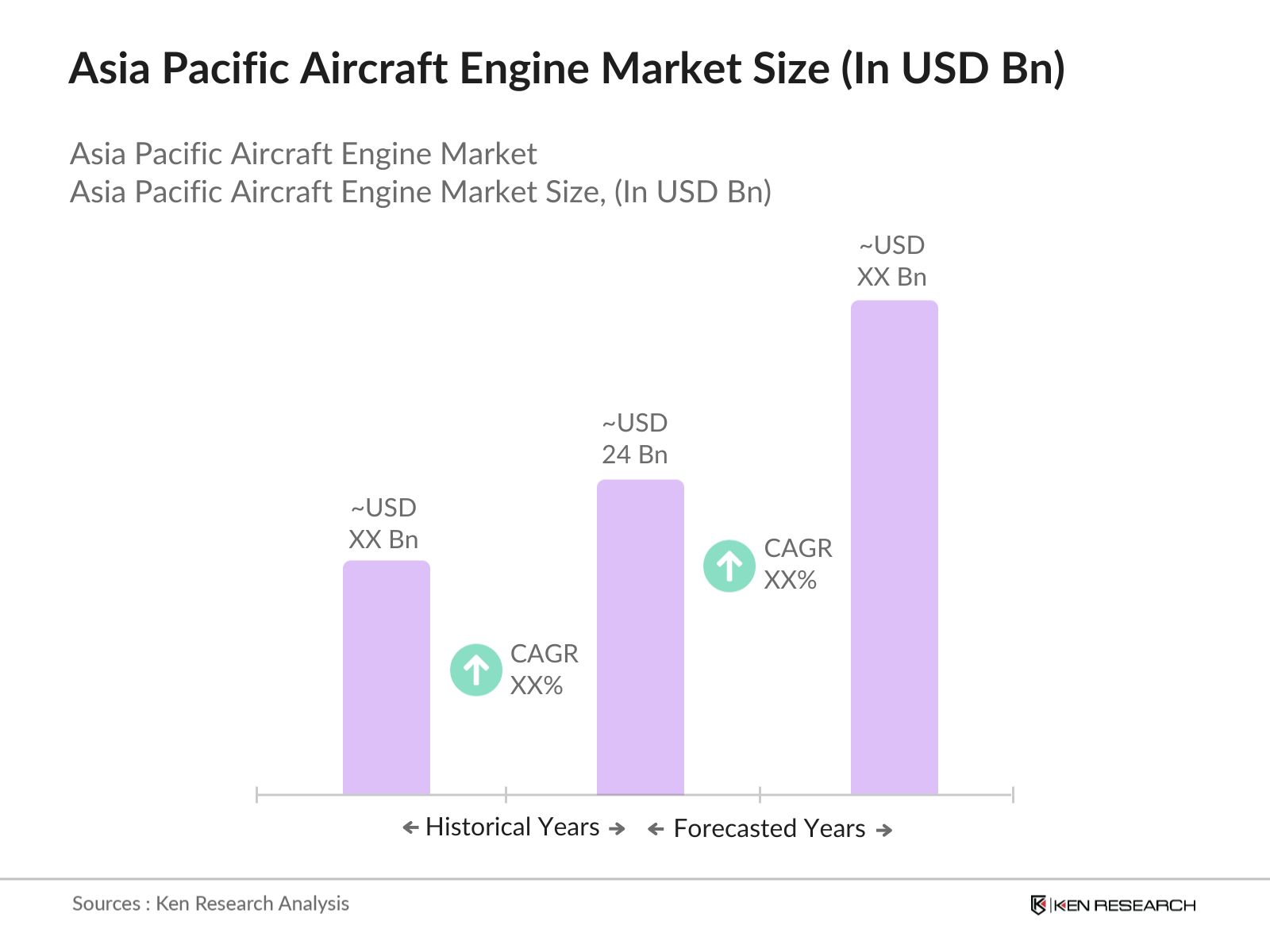

The Asia Pacific aircraft engine market was valued at USD 24 billion in 2023. The growth is primarily driven by the increasing demand for commercial aircraft due to the rise in air travel across key economies such as China and India. Moreover, the growing defense expenditure by countries in the region to upgrade their military aircraft fleets is contributing to the demand for more advanced and efficient aircraft engines.

Major players in the Asia Pacific aircraft engine market include Rolls-Royce Holdings, GE Aviation, Pratt & Whitney, Safran Aircraft Engines, and MTU Aero Engines. These companies dominate the market due to their long-standing expertise in engine manufacturing, extensive R&D investments, and established partnerships with key aircraft manufacturers like Boeing and Airbus.

In 2023, Pratt & Whitney announced its collaboration with Indias Hindustan Aeronautics Limited (HAL) for manufacturing key engine components. This collaboration aims to enhance Pratt & Whitneys supply chain in the Asia Pacific region, addressing growing demand for aircraft engines. HAL is expected to produce over 200 engine components annually, supporting the rise in demand from both civil and military aviation sectors.

China dominated the Asia Pacific aircraft engine total market share. This dominance is primarily due to the country's rapidly growing civil aviation sector, which, in 2023, added over 400 new aircraft to its fleet. The expansion of low-cost carriers and substantial investment in military aviation has positioned China as the leading player in the region.

Asia Pacific Aircraft Engine Market Segmentation

The Asia Pacific Aircraft Engine market is segmented into engine type, application and region etc.

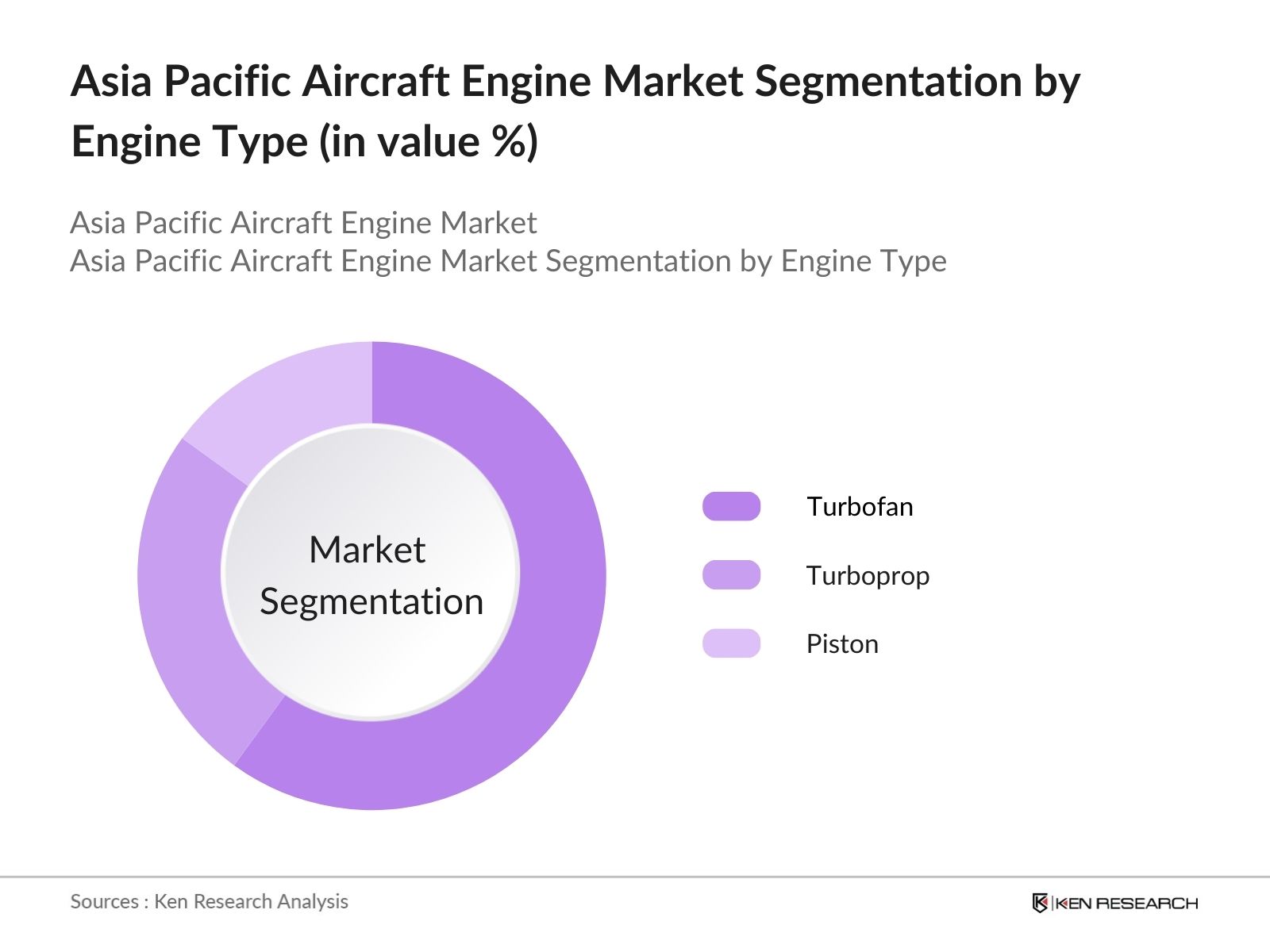

By Engine Type: The market is segmented into Turbofan, Turboprop, and Piston engines. Turbofan engines held the dominant market share in the Asia Pacific aircraft engine market. The dominance of this segment is due to their extensive use in commercial aircraft, which makes up a significant portion of the regions aviation fleet. With increasing fuel efficiency and reduced carbon emissions, airlines are increasingly opting for modern turbofan engines to cut operational costs.

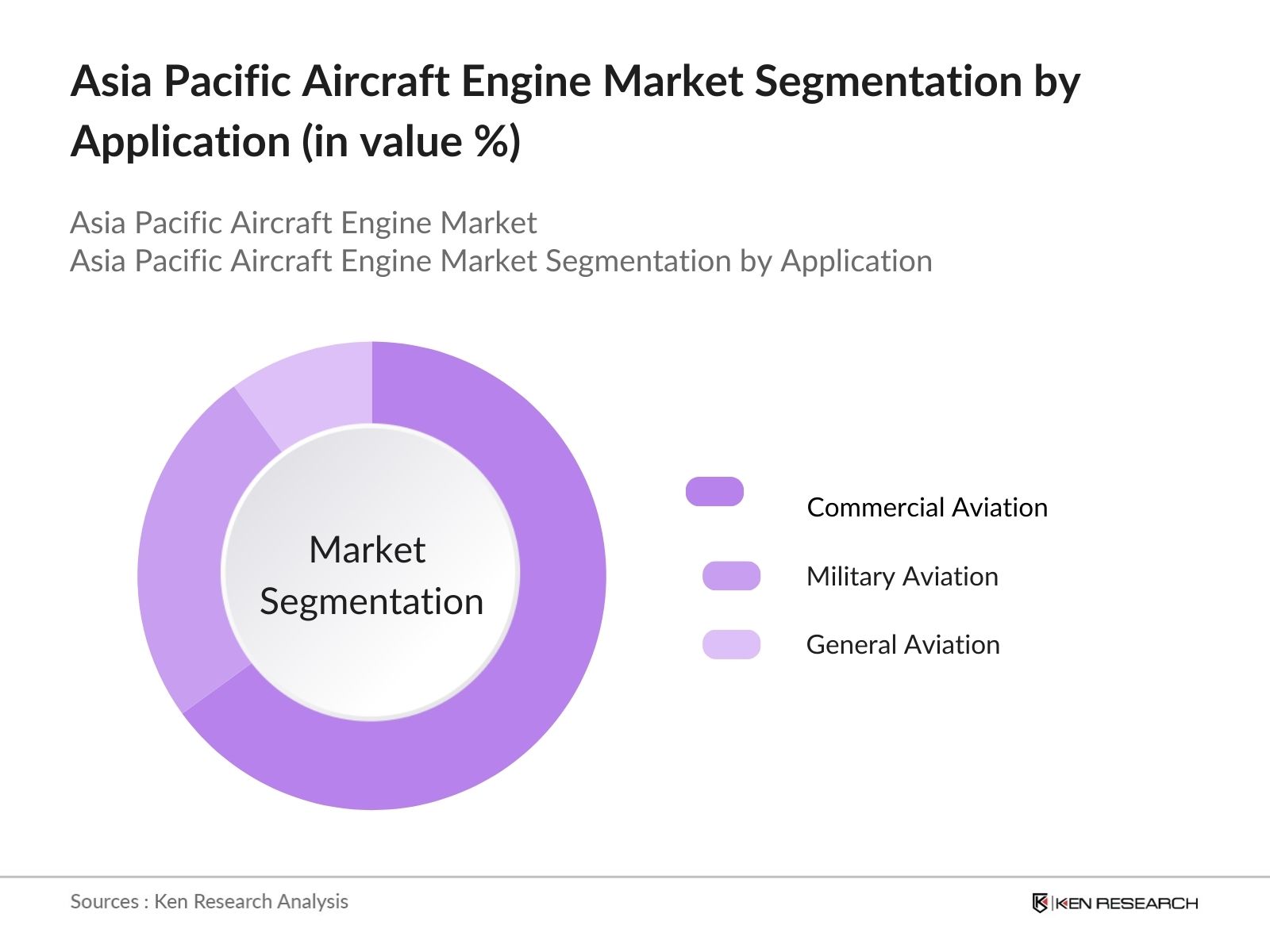

By Application: The market is segmented into commercial, military, and general aviation. Commercial aviation held the highest share, driven by the increasing number of low-cost carriers and rising demand for air travel in emerging markets like India and China. The demand for fuel-efficient and lightweight engines in commercial fleets is a key factor contributing to the dominance of this segment.

By Region The market is segmented into China, South Korea, Japan, India, Australia and Rest of APAC. China dominates the Asia Pacific aircraft engine market share, primarily driven by its large-scale commercial aviation sector, substantial defense investments, and rapid expansion of domestic low-cost carriers. China's focus on increasing self-reliance in aircraft engine production also contributes to its market dominance.

Asia Pacific Aircraft Engine Market Competitive Landscape

|

Company |

Establishment Year |

Headquarters |

|---|---|---|

|

Rolls-Royce Holdings |

1906 |

London, UK |

|

GE Aviation |

1917 |

Ohio, USA |

|

Pratt & Whitney |

1925 |

Connecticut, USA |

|

Safran Aircraft Engines |

1905 |

Paris, France |

|

MTU Aero Engines |

1934 |

Munich, Germany |

- Safran Aircraft Engines Invests in India: In 2023, Safran Aircraft Engines announced an investment of USD 200 million in a new facility in India to manufacture parts for commercial aircraft engines. This facility, located in Hyderabad, will cater to both the domestic market and export requirements. The investment aligns with Indias goal of becoming a global aerospace manufacturing hub under its "Make in India" program.

- Rolls-Royce Collaboration with Singapore Airlines: Rolls-Royce has secured a contract to supply engines for Singapore Airlines' fleet, specifically for 50 Boeing Dreamliner jets, valued at over USD 4 billion. The deal includes the delivery of engines and support services, with the engines expected to be delivered by 2028.

Asia Pacific Aircraft Engine Industry Analysis

Growth Drivers

-

-

Rise in Air Passenger Traffic: The Asia Pacific region has seen an increase in air passenger traffic, with China and India leading in numbers. In 2024, China is expected to cater to over 800 million domestic air passengers, driven by the expansion of budget airlines and increased flight connectivity. India's air traffic has also grown, reaching 175 million passengers, supported by growing middle-class travel habits.

- Fleet Expansion by Regional Airlines: Airlines across the region are rapidly expanding their fleets. In 2024, budget carriers like AirAsia and Indigo are expected to collectively add over 400 aircraft to their fleets to accommodate the surge in demand for domestic and regional flights. This expansion is directly increasing the demand for aircraft engines, especially fuel-efficient models that are crucial for keeping operational costs manageable amid rising fuel prices.

- Increased Defense Spending: Countries like India and Japan are substantially increasing their defense budgets to modernize their military aircraft fleets. In 2024, India invested for its Air Force upgrades, with a portion directed toward acquiring modern aircraft and high-performance engines. This defense modernization is driving the demand for military-grade aircraft engines designed for advanced fighter jets and transport aircraft.

-

Challenges

-

Rising Raw Material Costs: In 2024, the cost of key raw materials for engine production, such as nickel and titanium, has surged. The price of nickel alone has increased to USD 25,000 per metric ton, driven by limited supply and increased demand for electric vehicle batteries. This spike in material costs is affecting the profit margins of aircraft engine manufacturers, forcing them to adjust pricing strategies to maintain profitability.

- Skilled Labor Shortages: Aircraft engine manufacturing requires a highly skilled workforce, but the industry is facing a shortage of such talent in the Asia Pacific region. In 2024, the shortfall of skilled labor in the aerospace sector across China, India, and Japan professionals, impacting production timelines and the ability to meet growing demand for aircraft engines. This shortage is exacerbating delays in engine manufacturing and delivery.

Government Initiatives

-

Make in India for Aerospace: The Indian governments "Make in India" initiative has significantly impacted the aerospace industry. In 2024, this initiative attracted over USD 1.5 billion in foreign direct investment (FDI) for aircraft engine manufacturing, with global companies like Rolls-Royce and Pratt & Whitney setting up local production facilities. This initiative is reducing Indias reliance on imported engines and boosting domestic manufacturing capacity.

- Chinas Aircraft Engine R&D Investments

In 2024, the Chinese government announced a USD 2 billion investment in the development of advanced aircraft engines as part of its Made in China 2025 strategy. This investment aims to reduce Chinas dependence on foreign engine suppliers and increase its self-reliance in producing engines for both commercial and military aircraft. The government also launched new aerospace research centers to foster innovation.

Asia Pacific Aircraft Engine Market Future Outlook

The Asia Pacific aircraft engine market is expected to grow exponentially. The market will continue to grow due to the surge in low-cost carriers (LCCs) in countries like India, China, and Southeast Asia, coupled with advancements in fuel-efficient and sustainable aircraft engine technologies. Military demand for advanced aircraft engines will also boost the markets future outlook.

Future Trends

-

Rising Demand for Sustainable Aviation Fuels (SAF): The adoption of sustainable aviation fuels is projected to rise significantly. Governments are setting stricter regulations on carbon emissions, and airlines are increasingly looking toward SAF-compatible engines to meet these requirements. Engine manufacturers will continue to invest in developing SAF-compatible models to cater to this demand.

- Advanced Military Aircraft Engine Technologies: The demand for advanced military aircraft engines will surge, particularly in response to geopolitical tensions in the Asia Pacific region. Countries like India, Japan, and Australia are expected to upgrade their military fleets, with a focus on acquiring next-generation engines for fighter jets and reconnaissance aircraft. This will drive innovation and R&D in military-grade engine technologies.

Scope of the Report

|

By Engine Type |

Turbofan Turboprop Piston Engines |

|

By Application |

Commercial Military General Aviation |

|

By Region |

China South Korea Japan India Australia Rest of APAC |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Aviation industry associations

Aircraft manufacturers

Military defense departments

Aerospace component suppliers

Airline operators

Engine manufacturers

Investors and VC Firms

Banks and Financial Institutions

Civil Aviation Administration of China

Ministry of National Defense South Korea

Time Period Captured in the Report:

Historical Period: 2018-2023

Base Year: 2023

Forecast Period: 2023-2028

Companies

Players Mentioned in the Report:

Rolls-Royce Holdings

GE Aviation

Pratt & Whitney

Safran Aircraft Engines

MTU Aero Engines

Honeywell Aerospace

IHI Corporation

Kawasaki Heavy Industries

CFM International

Hitachi Ltd.

Aero Engine Corporation of China

United Technologies Corporation

Samsung Aerospace

Mahindra Aerospace

Avio Aero

Table of Contents

Asia Pacific Aircraft Engine Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

Asia Pacific Aircraft Engine Market Size (in USD Bn), 2018-2023

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

Asia Pacific Aircraft Engine Market Analysis

3.1. Growth Drivers

3.1.1. Rise in Air Passenger Traffic

3.1.2. Fleet Expansion by Regional Airlines

3.1.3. Increased Defense Spending

3.1.4. Investment in Sustainable Aviation

3.2. Restraints

3.2.1. Supply Chain Disruptions

3.2.2. Rising Raw Material Costs

3.2.3. Environmental Regulations

3.2.4. Skilled Labor Shortages

3.3. Opportunities

3.3.1. Development of Hybrid and Electric Engines

3.3.2. Expansion of Aircraft Engine Production Facilities

3.3.3. Growth in Regional Low-Cost Carriers

3.3.4. Increased Government Support for Aerospace Manufacturing

3.4. Trends

3.4.1. Adoption of Sustainable Aviation Fuels

3.4.2. Demand for Fuel-Efficient Engines

3.4.3. Expansion of Military Aircraft Fleets

3.4.4. Focus on Carbon-Emission-Reduction Technologies

3.5. Government Regulations

3.5.1. Indias Make in India Initiative

3.5.2. Chinas Aerospace Self-Reliance Program

3.5.3. South Koreas Green Aviation Initiative

3.5.4. Japans Defense Modernization Program

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Competition Ecosystem

Asia Pacific Aircraft Engine Market Segmentation, 2023

4.1. By Engine Type (in Value %)

4.1.1. Turbofan Engines

4.1.2. Turboprop Engines

4.1.3. Piston Engines

4.2. By Application (in Value %)

4.2.1. Commercial Aviation

4.2.2. Military Aviation

4.2.3. General Aviation

4.3. By Region (in Value %)

4.3.1. China

4.3.2. South Korea

4.3.3. South Korea

4.3.4. Japan

4.3.5. India

4.3.6. Australia

4.3.7. Rest of APAC

Asia Pacific Aircraft Engine Market Cross Comparison

5.1. Detailed Profiles of Major Companies

5.1.1. Rolls-Royce Holdings

5.1.2. GE Aviation

5.1.3. Pratt & Whitney

5.1.4. Safran Aircraft Engines

5.1.5. MTU Aero Engines

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue)

Asia Pacific Aircraft Engine Market Competitive Landscape

6.1. Market Share Analysis

6.2. Strategic Initiatives

6.3. Mergers and Acquisitions

6.4. Investment Analysis

6.4.1. Venture Capital Funding

6.4.2. Government Grants

6.4.3. Private Equity Investments

Asia Pacific Aircraft Engine Market Regulatory Framework

7.1. Environmental Standards

7.2. Compliance Requirements

7.3. Certification Processes

Asia Pacific Aircraft Engine Future Market Size (in USD Bn), 2023-2028

8.1. Future Market Size Projections

8.2. Key Factors Driving Future Market Growth

Asia Pacific Aircraft Engine Future Market Segmentation, 2028

9.1. By Engine Type (in Value %)

9.2. By Application (in Value %)

9.3. By Region (in Value %)

Asia Pacific Aircraft Engine Market Analysts Recommendations

10.1. TAM/SAM/SOM Analysis

10.2. Customer Cohort Analysis

10.3. Marketing Initiatives

10.4. White Space Opportunity Analysis

Research Methodology

Step: 1 Identifying Key Variables:

Ecosystem creation for all the major entities and referring to multiple secondary and proprietary databases to perform desk research around market to collate industry level information.

Step: 2 Market Building:

Collating statistics on Asia Pacific Aircraft Engine market over the years, penetration of marketplaces and service providers ratio to compute revenue generated for Asia Pacific Aircraft Engine market. We will also review service quality statistics to understand revenue generated which can ensure accuracy behind the data points shared.

Step: 3 Validating and Finalizing:

Building market hypothesis and conducting CATIs with industry experts belonging to different Aircraft engine companies to validate statistics and seek operational and financial information from company representatives.

Step: 4 Research Output:

Our team will approach multiple aircraft engine manufacturers and understand nature of product segments and sales, consumer preference and other parameters, which will support us validate statistics derived through bottom to top approach from aircraft engine companies.

Frequently Asked Questions

How big is Asia Pacific Aircraft Engine Market?

The Asia Pacific aircraft engine market, valued at USD 24 billion in 2023, is driven by the expansion of commercial and military aviation, fleet modernization, and advancements in sustainable engine technologies.

What are the challenges in the Asia Pacific Aircraft Engine Market?

Challenges in the Asia Pacific aircraft engine market include rising raw material costs, supply chain disruptions, environmental regulations, and a shortage of skilled labor in the aircraft manufacturing sector. These issues contribute to production delays and increased costs for manufacturers.

Who are the major players in the Asia Pacific Aircraft Engine Market?

Key players in the Asia Pacific aircraft engine market include Rolls-Royce Holdings, GE Aviation, Pratt & Whitney, Safran Aircraft Engines, and MTU Aero Engines. These companies lead due to their advanced technologies, strong partnerships with aircraft manufacturers, and robust R&D investments.

What are the growth drivers of the Asia Pacific Aircraft Engine Market?

The Asia Pacific aircraft engine market is driven by the rise in air passenger traffic, expansion of regional airlines' fleets, increased defense spending, and significant investments in sustainable aviation technologies by governments in the region.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.