Asia Pacific Artificial Tears Market Outlook to 2030

Region:Asia

Author(s):Vijay Kumar

Product Code:KROD4069

December 2024

94

About the Report

Asia Pacific Artificial Tears Market Overview

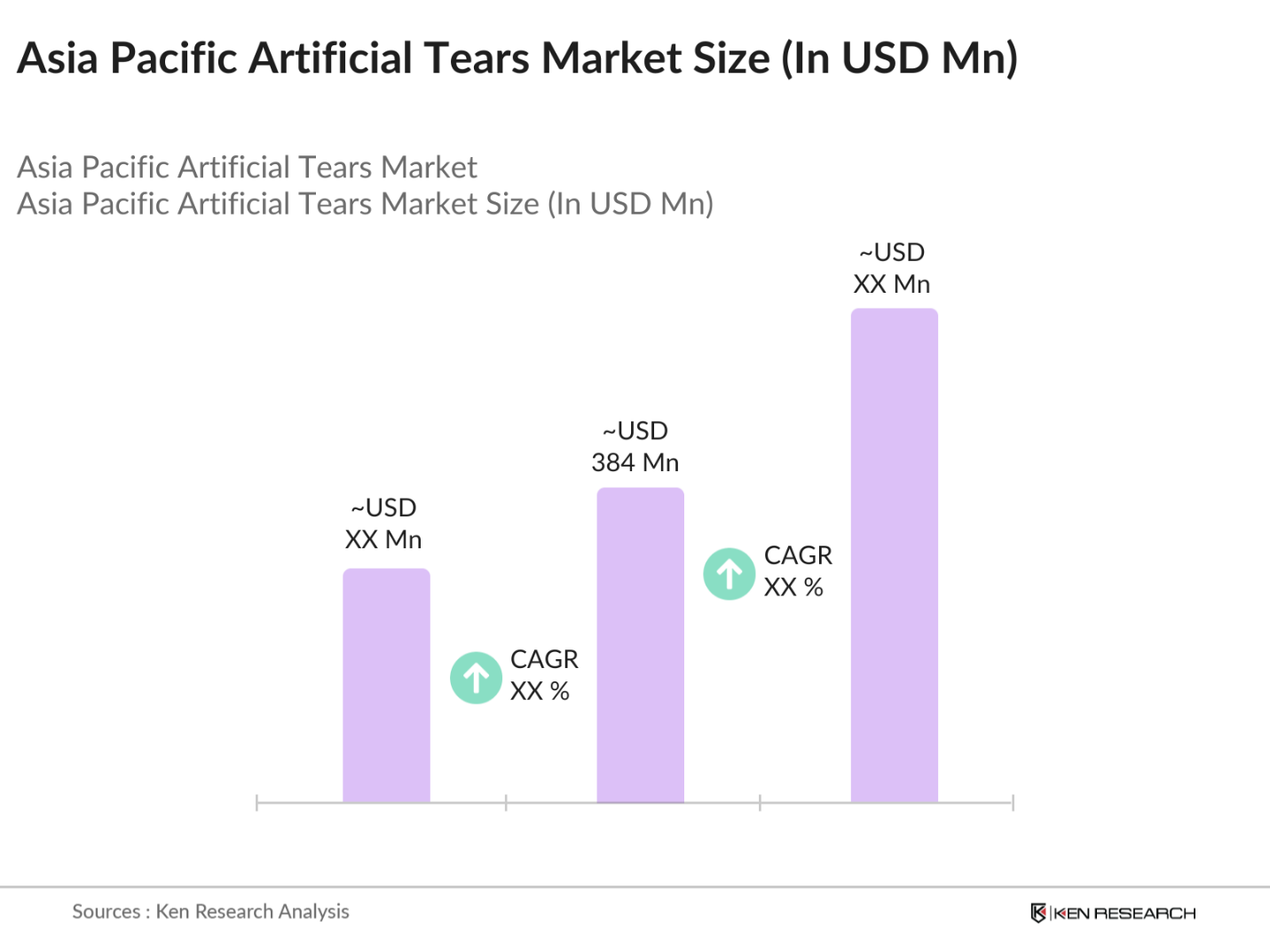

- The Asia Pacific Artificial Tears Market is valued at USD 384 million, based on a five-year historical analysis. This market growth is fueled by the increasing prevalence of dry eye syndrome, primarily driven by lifestyle changes, prolonged digital screen exposure, and rising pollution levels in urban centers. Moreover, the demand for preservative-free and advanced formulation artificial tears has surged, supported by the growing awareness of eye health among the aging population and patients with chronic conditions such as diabetes.

- China, Japan, and India are the dominant markets within the Asia Pacific region due to their large patient base and increasing awareness of eye health. China, for instance, has seen rapid growth in the elderly population, who are more prone to dry eye conditions. Similarly, Japan's high adoption of advanced healthcare solutions and India's expanding pharmaceutical industry make these countries crucial players in the market. These nations also have a robust retail pharmacy network and well-established distribution channels that support the widespread availability of artificial tears.

- Each country in the Asia Pacific region has distinct registration and compliance requirements for artificial tear products. For instance, in China, companies must navigate complex regulatory frameworks that involve multiple government agencies for product approval. Compliance costs have been reported to be a significant burden for smaller firms, impacting their ability to compete with established players.

Asia Pacific Artificial Tears Market Segmentation

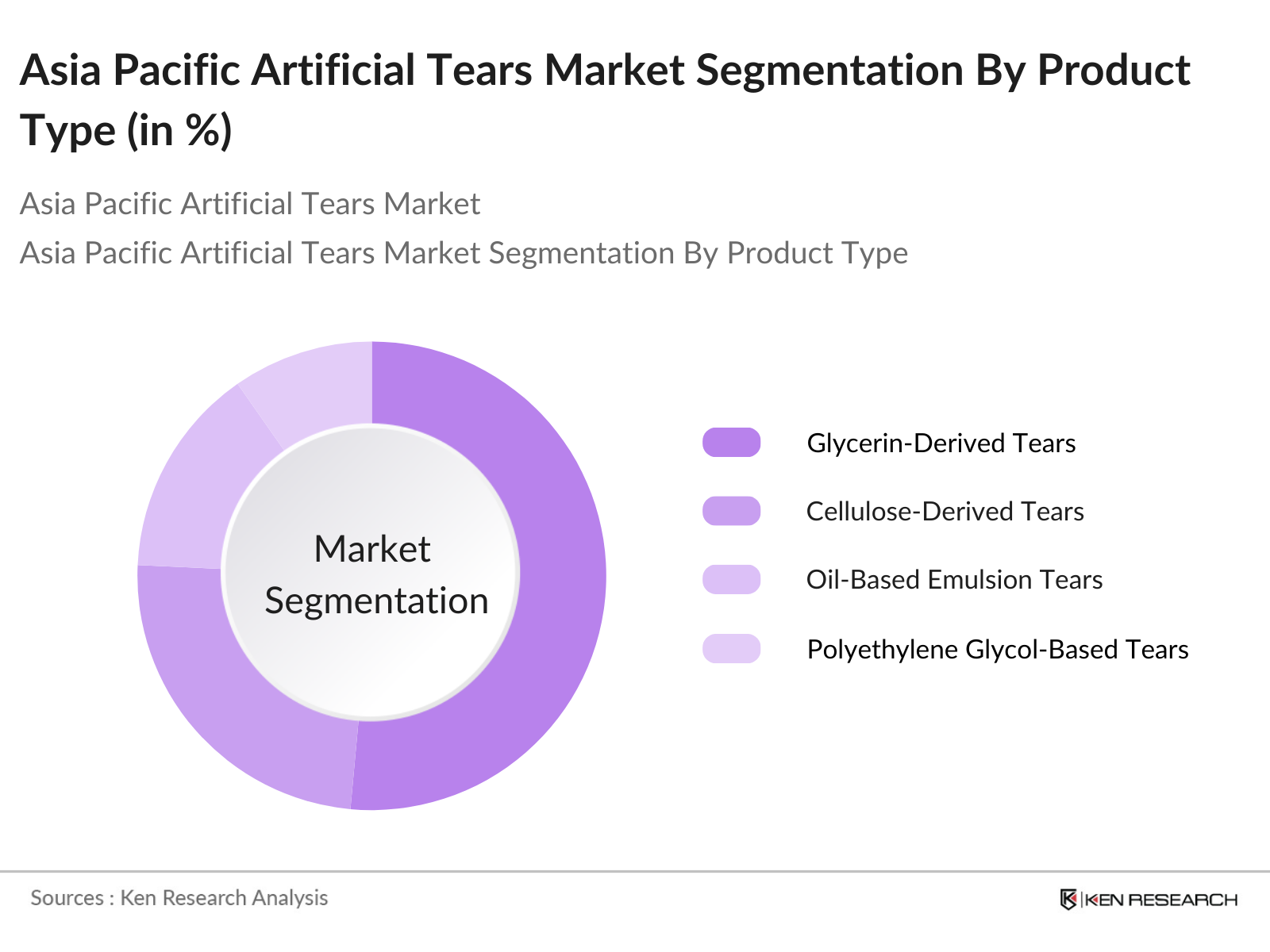

By Product Type: The market is segmented by product type into glycerin-derived tears, cellulose-derived tears, oil-based emulsion tears, polyethylene glycol-based tears, propylene glycol-based tears, and sodium hyaluronate-based tears. In 2023, glycerin-derived tears held a dominant market share due to their effective lubrication properties and ability to provide long-lasting relief for dry eyes.

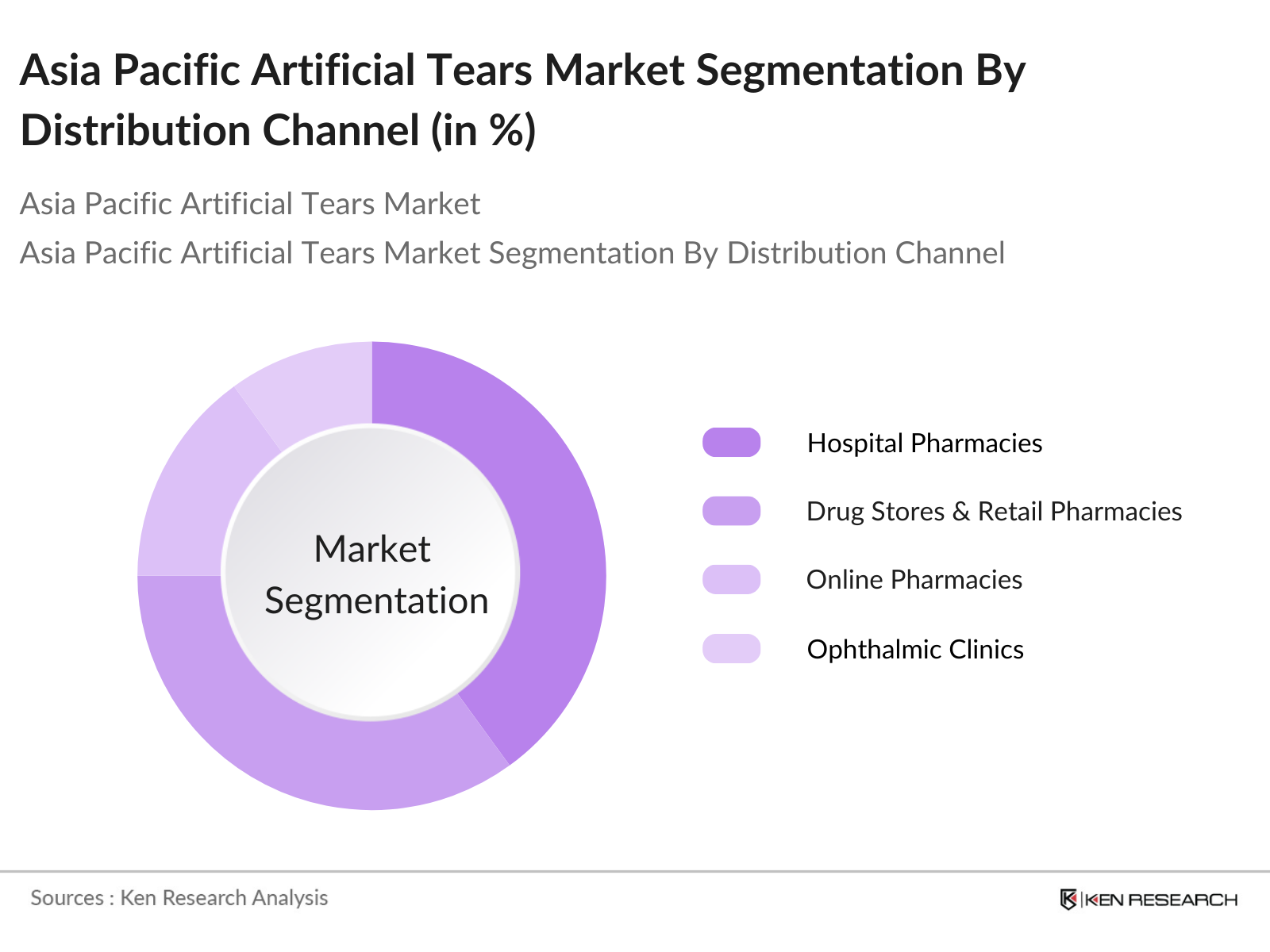

By Distribution Channel: The market is segmented by distribution channel into hospital pharmacies, drug stores & retail pharmacies, online pharmacies, and ophthalmic clinics. Hospital pharmacies dominated the market share in 2023, accounting for approximately 40% of sales. This is primarily due to the increasing number of ophthalmic consultations and surgical procedures, which often require the use of artificial tears as a complementary treatment.

Asia Pacific Artificial Tears Market Competitive Landscape

The Asia Pacific Artificial Tears Market is highly consolidated, with key players holding a significant market share. The market is characterized by strong competition among established players, with a focus on product innovation, partnerships, and regional expansions. The presence of local manufacturers and the increasing influence of global pharmaceutical companies further intensify competition.

Asia Pacific Artificial Tears Industry Analysis

Growth Drivers

- Rising Prevalence of Dry Eye Syndrome: The Asia Pacific region is experiencing a surge in cases of dry eye syndrome, driven by an aging population and increased exposure to environmental pollutants. In countries like Japan, the elderly population (65 years and above) constitutes over 28% of the total population as of 2024, which increases the risk of dry eye syndrome due to decreased tear production. Furthermore, environmental factors such as urban pollution contribute to the rising prevalence.

- Increasing Screen Time and Digital Device Use: The average daily screen time for adults in the Asia Pacific region has reached approximately 7 hours in 2024, up from 5.5 hours in 2020, primarily due to remote work and increased digital consumption. This excessive use of screens has led to a significant increase in eye strain and dry eye syndrome, especially in younger demographics. In South Korea, a survey conducted in 2022 found that over 80% of adults aged 18-35 reported symptoms related to digital eye strain, highlighting the link between digital device usage and eye health.

- Aging Population in Key Markets: The Asia Pacific region is home to some of the worlds fastest-aging populations. For instance, in South Korea and Japan, the proportion of the population aged 65 and above has surpassed 20% in 2024. This demographic shift has increased the prevalence of dry eye syndrome, as aging reduces tear production. Additionally, in China, where over 200 million people are aged 60 and above, the demand for ocular health solutions, including artificial tears, has seen a steady increase due to age-related eye conditions.

Market Challenges

- High Cost of Specialty Formulations: Specialty formulations of artificial tears, such as those with advanced ingredients like hyaluronic acid, remain expensive and less accessible to lower-income segments in Asia Pacific countries. The World Bank notes that the average annual per capita healthcare expenditure in countries like Indonesia and Vietnam is below $200, limiting the affordability of high-cost formulations for many. This financial barrier restricts the wider adoption of premium artificial tear products.

- Product Safety and Regulatory Barriers: Regulatory requirements across the Asia Pacific region, particularly in countries like Japan and Australia, present barriers to market entry for new players in the artificial tears segment. Stringent safety and efficacy testing standards mean that new products can face delays of up to 2 years before gaining approval. This slows down the introduction of innovative formulations, potentially stalling market growth.

Asia Pacific Artificial Tears Market Future Outlook

Over the next five years, the Asia Pacific Artificial Tears Market is expected to experience substantial growth driven by increasing healthcare expenditure, the rising prevalence of dry eye syndrome, and a greater focus on eye health in the region. Additionally, advancements in product formulations, such as the introduction of preservative-free and biocompatible artificial tears, will further support market expansion.

Market Opportunities

- Technological Advancements in Formulations: Innovative formulations, such as preservative-free and lipid-enhanced artificial tears, are gaining traction in the Asia Pacific market. A 2023 report indicated that countries like South Korea are investing heavily in R&D for ocular health, with government-backed projects receiving funding of up to $500 million to support research in advanced eye care formulations. These advancements are expected to cater to the growing demand for biocompatible and long-lasting eye care solutions.

- Expansion in Untapped Regional Markets: Southeast Asian countries like the Philippines and Vietnam represent untapped markets with potential for growth in the artificial tears segment. In these regions, the percentage of the population aged 50 and above is steadily increasing, reaching 15% in 2024, which indicates a growing need for eye care products. Furthermore, recent economic growth and rising disposable incomes in these countries are expected to support the increased adoption of healthcare products, including artificial tears.

Scope of the Report

|

Product Type |

Glycerin-Derived Tears Cellulose-Derived Tears Oil-Based Emulsion Tears Polyethylene Glycol-Based Tears Propylene Glycol-Based Tears Sodium Hyaluronate-Based Tears |

|

Application |

Dry Eye Syndrome Allergies & Infections UV and Blue Light Protection Contact Lens Moisture Retentio Post-Surgery Applications |

|

Delivery Mode |

Eye Drops Ointments |

|

Distribution Channel |

Hospital Pharmacies Drug Stores & Retail Pharmacies Online Pharmacies Ophthalmic Clinics and Stores |

|

Region |

China Japan India Australia South Korea Southeast Asia (Malaysia, Thailand, Singapore, Indonesia, Vietnam) |

Products

Key Target Audience

Pharmaceutical Manufacturers

Hospital Pharmacies

Online Pharmacies

Drug Stores & Retail Pharmacies

Ophthalmic Clinics and Eye Hospitals

Investment and Venture Capitalist Firms

Government and Regulatory Bodies (e.g., Japan Pharmaceuticals and Medical Devices Agency, China Food and Drug Administration)

Healthcare Providers and Practitioners

Companies

Players Mentioned in the Report

Johnson & Johnson Vision Care

Allergan (AbbVie Inc.)

Alcon

Bausch & Lomb Incorporated

Santen Pharmaceutical

URSAPHARM Arzneimittel

Rohto Pharmaceutical

Novartis AG

Abbott Laboratories

Nicox S.A.

Table of Contents

1. Asia Pacific Artificial Tears Market Overview

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

1.5 Key Market Indicators (e.g., Dry Eye Prevalence, Population Demographics, Health Expenditure)

2. Asia Pacific Artificial Tears Market Size (in USD Billion)

2.1 Historical Market Size

2.2 Year-on-Year Growth Analysis

2.3 Key Market Developments and Milestones

3. Asia Pacific Artificial Tears Market Analysis

3.1 Growth Drivers

3.1.1 Rising Prevalence of Dry Eye Syndrome

3.1.2 Increasing Screen Time and Digital Device Use

3.1.3 Aging Population in Key Markets

3.1.4 Expansion of Online and Retail Pharmacies

3.2 Market Challenges

3.2.1 High Cost of Specialty Formulations

3.2.2 Product Safety and Regulatory Barriers

3.2.3 Limited Access to Healthcare in Rural Areas

3.3 Opportunities

3.3.1 Technological Advancements in Formulations

3.3.2 Expansion in Untapped Regional Markets

3.3.3 Strategic Partnerships and Mergers

3.4 Trends

3.4.1 Preference for Preservative-Free Products

3.4.2 Growth of E-Commerce Channels

3.4.3 Focus on Biocompatible and Biodegradable Products

3.5 Government Regulations and Policies

3.5.1 Asia Pacific Healthcare Regulatory Overview

3.5.2 Regional Registration and Compliance Requirements

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem Analysis

3.8 Porters Five Forces Analysis

3.9 Competition Ecosystem Analysis

4. Asia Pacific Artificial Tears Market Segmentation

4.1 By Product Type (in Value %) [6]

4.1.1 Glycerin-Derived Tears

4.1.2 Cellulose-Derived Tears

4.1.3 Oil-Based Emulsion Tears

4.1.4 Polyethylene Glycol-Based Tears

4.1.5 Propylene Glycol-Based Tears

4.1.6 Sodium Hyaluronate-Based Tears

4.2 By Application (in Value %) [7]

4.2.1 Dry Eye Syndrome

4.2.2 Allergies & Infections

4.2.3 UV and Blue Light Protection

4.2.4 Contact Lens Moisture Retention

4.2.5 Post-Surgery Applications

4.3 By Delivery Mode (in Value %) [8]

4.3.1 Eye Drops

4.3.2 Ointments

4.4 By Distribution Channel (in Value %) [9]

4.4.1 Hospital Pharmacies

4.4.2 Drug Stores & Retail Pharmacies

4.4.3 Online Pharmacies

4.4.4 Ophthalmic Clinics and Stores

4.5 By Region (in Value %) [10]

4.5.1 China

4.5.2 Japan

4.5.3 India

4.5.4 Australia

4.5.5 South Korea

4.5.6 Southeast Asia (Malaysia, Thailand, Singapore, Indonesia, Vietnam)

5. Asia Pacific Artificial Tears Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1 Johnson & Johnson Vision Care

5.1.2 Allergan (AbbVie Inc.)

5.1.3 Alcon

5.1.4 Bausch & Lomb Incorporated

5.1.5 Santen Pharmaceutical

5.1.6 URSAPHARM Arzneimittel

5.1.7 ROHTO Pharmaceutical

5.1.8 Novartis AG

5.1.9 Abbott Laboratories

5.1.10 Nicox S.A.

5.1.11 Sun Pharmaceutical Industries

5.1.12 Similasan Corporation

5.1.13 Wuhan Yuanda

5.1.14 Jiangxi Zhenshiming

5.1.15 Entod Research Cell

5.2 Cross Comparison Parameters (No. of Employees, Headquarters, R&D Expenditure, Revenue, Product Portfolio, Market Presence, Strategic Initiatives, Manufacturing Capacity)

5.3 Market Share Analysis

5.4 Strategic Initiatives and Developments

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6. Asia Pacific Artificial Tears Market Regulatory Framework

6.1 Healthcare Standards and Compliance

6.2 Environmental Regulations for Production

6.3 Certification and Quality Control Processes

7. Asia Pacific Artificial Tears Market Future Market Size (in USD Billion)

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8. Asia Pacific Artificial Tears Market Future Market Segmentation

8.1 By Product Type (in Value %)

8.2 By Application (in Value %)

8.3 By Delivery Mode (in Value %)

8.4 By Distribution Channel (in Value %)

8.5 By Region (in Value %)

9. Asia Pacific Artificial Tears Market Analysts Recommendations

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 Market Expansion Strategies

9.4 White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The initial step involved mapping the entire ecosystem of stakeholders in the Asia Pacific Artificial Tears Market. This phase was driven by comprehensive desk research, utilizing secondary data sources and proprietary databases to gather accurate and reliable market-level information. The objective was to define and identify critical market variables influencing the sector.

Step 2: Market Analysis and Construction

During this phase, historical data on the market was compiled and analyzed. This included assessing market penetration rates, evaluating the revenue generated across different segments, and understanding the demand-supply dynamics. A detailed analysis was conducted to ensure the accuracy of revenue estimates and growth forecasts.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses were developed and validated through interviews with industry experts. These consultations provided valuable insights into the operational and strategic aspects of the market, aiding in the refinement and corroboration of key data points.

Step 4: Research Synthesis and Final Output

The final phase involved direct interaction with artificial tear manufacturers and distributors to obtain detailed insights into their product segments, sales performance, and customer preferences. This data was then synthesized to create a holistic, accurate, and validated analysis of the Asia Pacific Artificial Tears Market.

Frequently Asked Questions

01. How big is the Asia Pacific Artificial Tears Market?

The Asia Pacific Artificial Tears Market is valued at USD 384 million, based on a five-year historical analysis. This market growth is fueled by the increasing prevalence of dry eye syndrome, primarily driven by lifestyle changes, prolonged digital screen exposure, and rising pollution levels in urban centers.

02. What are the challenges in the Asia Pacific Artificial Tears Market?

Key challenges include the high cost of specialty products, stringent regulatory requirements, and competition from alternative treatment options. Additionally, product safety concerns and the risk of contamination are significant barriers to market growth.

03. Who are the major players in the Asia Pacific Artificial Tears Market?

Major players include Johnson & Johnson Vision Care, Allergan (AbbVie Inc.), Alcon, Bausch & Lomb Incorporated, and Santen Pharmaceutical. These companies have strong brand presence and extensive distribution networks across the region.

04. What are the growth drivers of the Asia Pacific Artificial Tears Market?

The market is driven by factors such as increased screen time leading to dry eye conditions, an aging population, and rising healthcare expenditure. Additionally, advancements in product formulations, such as preservative-free and biocompatible solutions, are fueling market growth.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.