Asia Pacific Automotive ECU Market Outlook to 2030

Region:Asia

Author(s):Yogita Sahu

Product Code:KROD3094

November 2024

98

About the Report

Asia Pacific Automotive ECU Market Overview

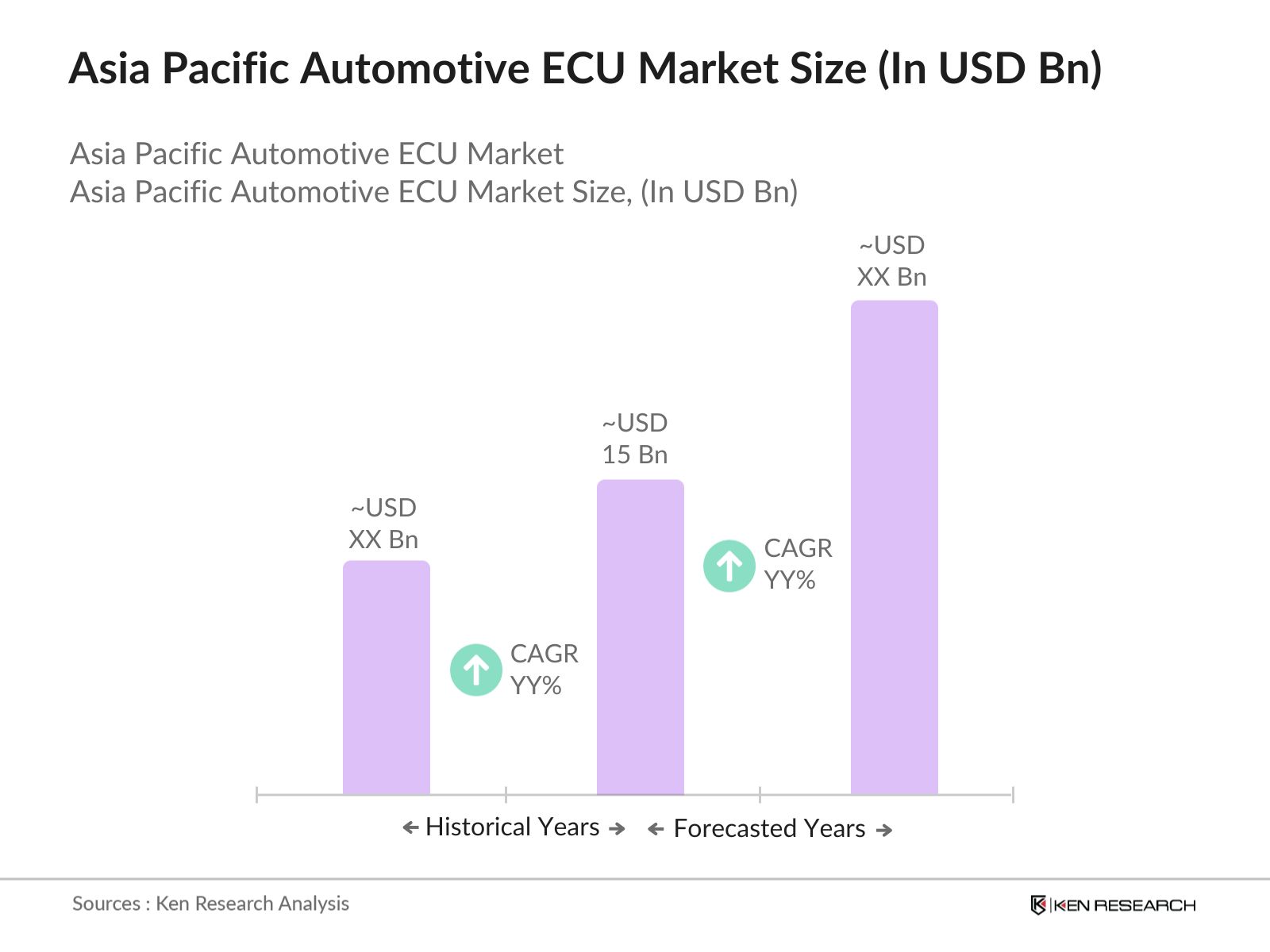

- The Asia Pacific Automotive ECU (Electronic Control Unit) market is valued at USD 15 billion based on a five-year historical analysis. The growth of this market is primarily driven by the rising electrification of vehicles, increased demand for advanced driver assistance systems (ADAS), and stringent emission control regulations across the region.

- Countries like China, Japan, and South Korea dominate the market due to their strong automotive manufacturing base, extensive investment in R&D, and early adoption of advanced automotive technologies. Chinas booming electric vehicle production, Japan's expertise in precision electronics, and South Koreas focus on ADAS and smart vehicle infrastructure contribute to the dominance of these countries in the market.

- The European Commission launched an anti-subsidy investigation in September 2023 targeting Chinese electric vehicles (EVs), examining the impact of China's state subsidies on European markets. The investigation, expected to last up to 13 months, aims to assess the imposition of additional tariffs to protect European manufacturers from the influx of lower-cost EVs, which make up 8% of the EU market.

Asia Pacific Automotive ECU Market Segmentation

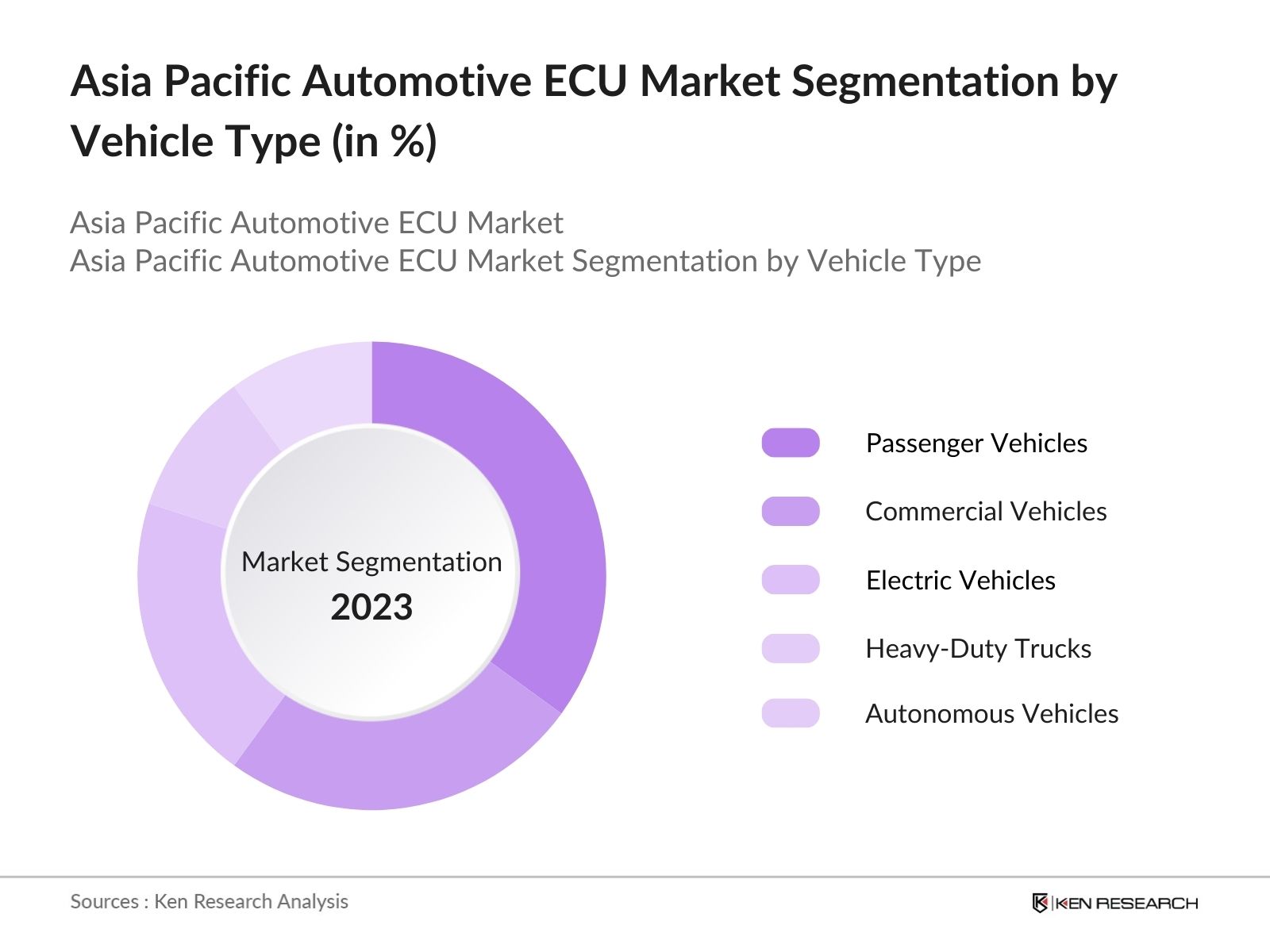

By Vehicle Type: The market is segmented by vehicle type into passenger vehicles, commercial vehicles, electric vehicles, heavy-duty trucks, and autonomous vehicles. Passenger vehicles have a dominant market share in the region under this segmentation. This dominance is due to the massive demand for personal vehicles in urban areas, driven by rising disposable incomes and the increasing need for advanced safety and infotainment systems in these vehicles.

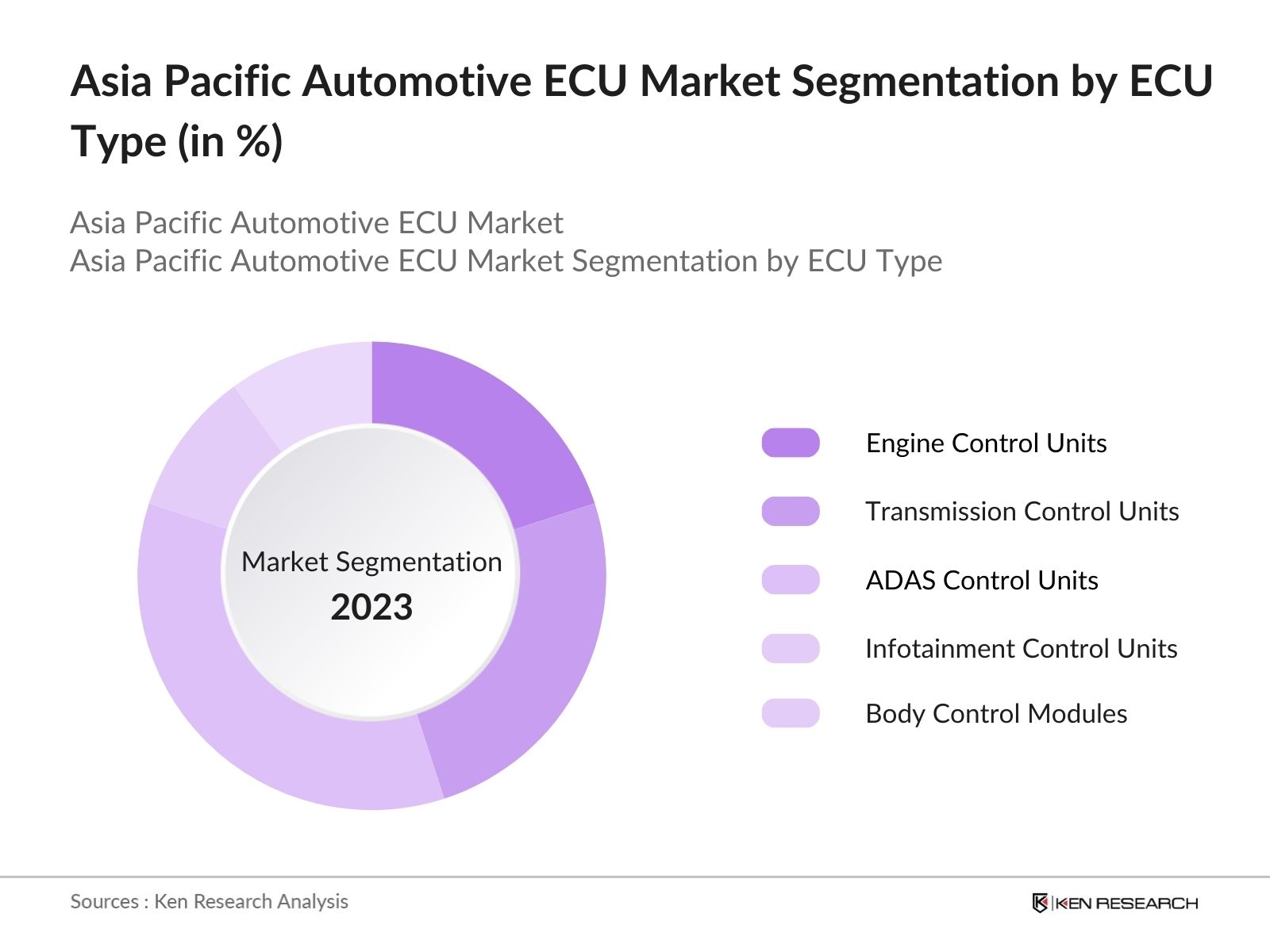

By ECU Type: The market is also segmented by ECU type into engine control units, transmission control units, ADAS control units, infotainment control units, and body control modules. ADAS control units hold a dominant share, owing to the rapid integration of advanced safety features such as adaptive cruise control, lane-keeping assistance, and parking assistance.

Asia Pacific Automotive ECU Market Competitive Landscape

The market is dominated by several key players who have established themselves through technological innovation, extensive R&D investment, and strong partnerships with original equipment manufacturers (OEMs). This consolidation highlights the critical role these companies play in the development of ECUs for electric and autonomous vehicles.

|

Company |

Establishment Year |

Headquarters |

R&D Spending |

Key Markets |

Partnerships |

Product Focus |

Innovation Strategy |

Revenue |

|

Robert Bosch GmbH |

1886 |

Stuttgart, Germany |

||||||

|

Continental AG |

1871 |

Hanover, Germany |

||||||

|

Denso Corporation |

1949 |

Kariya, Japan |

||||||

|

Aptiv PLC |

1994 |

Dublin, Ireland |

||||||

|

Mitsubishi Electric Corp. |

1921 |

Tokyo, Japan |

Asia Pacific Automotive ECU Market Analysis

Market Growth Drivers

- Increased Electrification in Vehicles: The market is experiencing growth due to the increased electrification of vehicles. Governments in countries like China, Japan, and South Korea are pushing for electric vehicle (EV) adoption to reduce dependency on fossil fuels. In 2024, the Chinese government supports electric vehicle infrastructure and development, propelling demand for advanced ECUs.

- Stringent Emission Norms: Governments in the Asia Pacific region is enforcing strict emission regulations, which are driving the adoption of automotive ECUs. India implemented Bharat Stage VI (BS6) norms, requiring upgrades in vehicle emission systems to reduce air pollutants. This has led to a surge in demand for ECUs that control emissions through advanced engine management systems.

- Growth in Connected Vehicle Ecosystems: The Asia Pacific region is seeing a rapid rise in the deployment of connected vehicle ecosystems, which is driving ECU demand. As of 2024, Japan alone had over 12 million connected cars on its roads, all relying on ECUs for functions such as remote diagnostics, vehicle-to-infrastructure communication, and in-car connectivity. These connected vehicles require sophisticated ECUs to manage data from sensors and ensure seamless integration with external systems.

Market Challenges

- Supply Chain Disruptions: The global semiconductor shortage has severely impacted the automotive ECU market in Asia Pacific. Semiconductors are essential components in ECU production, and the ongoing supply chain issues have led to delays in vehicle manufacturing across the region. In 2023, automobile production in Japan was reduced by nearly 500,000 units due to the unavailability of semiconductors.

- Technical Complexity and Compatibility Issues: The increasing complexity of modern vehicle systems presents challenges for ECU integration. Automakers often face difficulties in ensuring seamless communication between different ECUs in vehicles that require multiple units for different functions like engine management, infotainment, and safety systems.

Asia Pacific Automotive ECU Market Future Outlook

Over the next five years, the Asia Pacific Automotive ECU industry is expected to show growth driven by the increasing penetration of electric vehicles, advancements in autonomous driving technology, and government regulations promoting vehicle safety and emission reduction. The growing demand for connected vehicles and the trend toward software-defined vehicles will further enhance the role of ECUs in the automotive industry.

Future Market Opportunities

- Rising Integration of Artificial Intelligence in ECUs: Over the next five years, artificial intelligence (AI) will play a major role in the evolution of automotive ECUs in Asia Pacific. Automakers are expected to integrate AI-based ECUs for autonomous driving, predictive maintenance, and real-time vehicle diagnostics. For instance, Japans government has already support AI research in automotive technology, which will drive advancements in AI-powered ECUs, enhancing vehicle performance and safety features.

- Growth of Autonomous Vehicles: The Asia Pacific region is set to become a hub for autonomous vehicle development, with countries like China and Japan leading the way. By 2029, China is expected to have over 5 million autonomous vehicles on its roads, requiring advanced ECUs to handle tasks like navigation, safety control, and real-time data processing.

Scope of the Report

|

Vehicle Type |

Passenger Vehicles Commercial Vehicles Electric Vehicles Heavy-Duty Trucks Autonomous Vehicles |

|

ECU Type |

Engine Control Units Transmission Control Units ADAS Control Units Infotainment Control Units Body Control Modules |

|

Application |

Powertrain Chassis Electronics Safety and Security Communication and Infotainment Autonomous Driving |

|

Technology |

Traditional ECUs Hybrid ECUs Domain Control ECUs Centralized ECUs |

|

Region |

China South Korea Japan India Australia Rest of APAC |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Automotive OEMs

Electric Vehicle Manufacturers

Autonomous Vehicle Technology Providers

Government and Regulatory Bodies (e.g., National Highway Traffic Safety Administration)

Investments and Venture Capitalist Firms

Infotainment System Providers

Companies

Players Mentioned in the Report:

Robert Bosch GmbH

Continental AG

Denso Corporation

Aptiv PLC

Mitsubishi Electric Corporation

NXP Semiconductors

ZF Friedrichshafen AG

Valeo

Marelli

Hitachi Astemo

Renesas Electronics Corporation

Infineon Technologies AG

Hella GmbH & Co. KGaA

Panasonic Automotive Systems

Hyundai Mobis

Table of Contents

1. Asia Pacific Automotive ECU Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Dynamics

1.4. Market Segmentation Overview

2. Asia Pacific Automotive ECU Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Market Growth Rate

2.3. Key Milestones and Developments

3. Asia Pacific Automotive ECU Market Analysis

3.1. Growth Drivers (Automotive Electrification, Demand for ADAS, Emission Regulations)

3.1.1. Rise in Automotive Electrification

3.1.2. Growing Adoption of Advanced Driver Assistance Systems (ADAS)

3.1.3. Stringent Emission Regulations

3.1.4. Increasing Production of Autonomous Vehicles

3.2. Market Challenges (Chip Shortage, High R&D Costs, Complex Software Integration)

3.2.1. Ongoing Semiconductor Chip Shortages

3.2.2. High Research and Development Costs

3.2.3. Complex Software Integration Issues

3.2.4. Growing Cybersecurity Threats

3.3. Opportunities (Connected Vehicles, OTA Updates, Rising Demand for EVs)

3.3.1. Emergence of Connected and Smart Vehicles

3.3.2. Increasing Over-the-Air (OTA) Updates for ECUs

3.3.3. Rising Demand for Electric Vehicles (EVs)

3.3.4. Expansion of Aftermarket ECU Tuning

3.4. Trends (Shift Toward Centralized ECUs, Software-Defined Vehicles)

3.4.1. Transition Toward Centralized ECU Architecture

3.4.2. Growth of Software-Defined Vehicles

3.4.3. ECU Miniaturization and Power Efficiency

3.4.4. Increased Integration of Artificial Intelligence in ECUs

3.5. Government Regulations (Safety Mandates, Emission Standards)

3.5.1. Regional Safety Mandates for ADAS Integration

3.5.2. CO2 Emission Standards Compliance

3.5.3. Fuel Economy Regulations

3.5.4. Environmental Policies Impacting Automotive ECU Design

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem (OEMs, Suppliers, End-Users)

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

4. Asia Pacific Automotive ECU Market Segmentation

4.1. By Vehicle Type (In Value %)

4.1.1. Passenger Vehicles

4.1.2. Commercial Vehicles

4.1.3. Electric Vehicles

4.1.4. Heavy-Duty Trucks

4.1.5. Autonomous Vehicles

4.2. By ECU Type (In Value %)

4.2.1. Engine Control Units

4.2.2. Transmission Control Units

4.2.3. ADAS Control Units

4.2.4. Infotainment Control Units

4.2.5. Body Control Modules

4.3. By Application (In Value %)

4.3.1. Powertrain

4.3.2. Chassis Electronics

4.3.3. Safety and Security

4.3.4. Communication and Infotainment

4.3.5. Autonomous Driving

4.4. By Technology (In Value %)

4.4.1. Traditional ECUs

4.4.2. Hybrid ECUs

4.4.3. Domain Control ECUs

4.4.4. Centralized ECUs

4.5. By Region (In Value %)

4.5.1. China

4.5.2. Japan

4.5.3. South Korea

4.5.4. India

4.5.5. ASEAN Countries

5. Asia Pacific Automotive ECU Market Competitive Analysis

5.1 Detailed Profiles of Major Competitors

5.1.1. Robert Bosch GmbH

5.1.2. Continental AG

5.1.3. Denso Corporation

5.1.4. Aptiv PLC

5.1.5. Mitsubishi Electric Corporation

5.1.6. NXP Semiconductors

5.1.7. ZF Friedrichshafen AG

5.1.8. Valeo

5.1.9. Marelli

5.1.10. Hitachi Astemo

5.1.11. Renesas Electronics Corporation

5.1.12. Infineon Technologies AG

5.1.13. Hella GmbH & Co. KGaA

5.1.14. Panasonic Automotive Systems

5.1.15. Hyundai Mobis

5.2 Cross Comparison Parameters (Headquarters, Revenue, Product Specialization, R&D Spending, Market Presence, Strategic Initiatives, Partnerships, Mergers & Acquisitions)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers And Acquisitions

5.6. Investment Analysis

5.7 Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. Asia Pacific Automotive ECU Market Regulatory Framework

6.1. Compliance Requirements

6.2. Certification Processes

6.3. Environmental Standards

6.4. Regional Safety Regulations

7. Asia Pacific Automotive ECU Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Asia Pacific Automotive ECU Future Market Segmentation

8.1. By Vehicle Type (In Value %)

8.2. By ECU Type (In Value %)

8.3. By Application (In Value %)

8.4. By Technology (In Value %)

8.5. By Region (In Value %)

9. Asia Pacific Automotive ECU Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The first step involves creating a comprehensive ecosystem map that identifies all major stakeholders within the Asia Pacific Automotive ECU market. This process relies on extensive secondary research to collect industry-level data, including technological trends, regulatory impacts, and market dynamics.

Step 2: Market Analysis and Construction

In this step, we compile and analyze historical market data, focusing on key aspects such as ECU penetration in vehicles, sales performance, and revenue generation. This data is cross-verified with information from primary interviews and secondary sources to ensure accuracy.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses are developed based on data trends and are validated through interviews with industry experts. These consultations provide crucial insights into operational and financial aspects, aiding in refining market forecasts.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with industry players to verify data on ECU integration, product demand, and technological developments. This information is synthesized into a cohesive market report that accurately reflects the current and future dynamics of the Asia Pacific Automotive ECU market.

Frequently Asked Questions

How big is the Asia Pacific Automotive ECU Market?

The Asia Pacific Automotive ECU market is valued at USD 15 billion, driven by increasing demand for electric vehicles, ADAS technologies, and stringent emission regulations.

What are the challenges in the Asia Pacific Automotive ECU Market?

Challenges in the Asia Pacific Automotive ECU market include the ongoing semiconductor shortage, high R&D costs, and cybersecurity risks associated with connected vehicles, all of which impact ECU production and deployment.

Who are the major players in the Asia Pacific Automotive ECU Market?

Key players in the Asia Pacific Automotive ECU market include Robert Bosch GmbH, Continental AG, Denso Corporation, Aptiv PLC, and Mitsubishi Electric Corporation, all of which dominate due to their extensive R&D capabilities and OEM partnerships.

What are the growth drivers of the Asia Pacific Automotive ECU Market?

The Asia Pacific Automotive ECU market is driven by factors such as the rise of electric vehicles, the growing adoption of ADAS, and the trend toward vehicle electrification, particularly in China, Japan, and South Korea.

What role does government regulation play in the Asia Pacific Automotive ECU Market?

Government regulations in the Asia Pacific Automotive ECU market mandating stricter safety and emission standards are major drivers of ECU adoption, as automakers must comply with rules aimed at reducing vehicle emissions and enhancing passenger safety.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.