Asia Pacific Barley Tea Market Outlook to 2030

Region:Afganistan

Author(s):Paribhasha Tiwari

Product Code:KROD9651

Region:Afganistan

Author(s):Paribhasha Tiwari

Product Code:KROD9651

November 2024

88

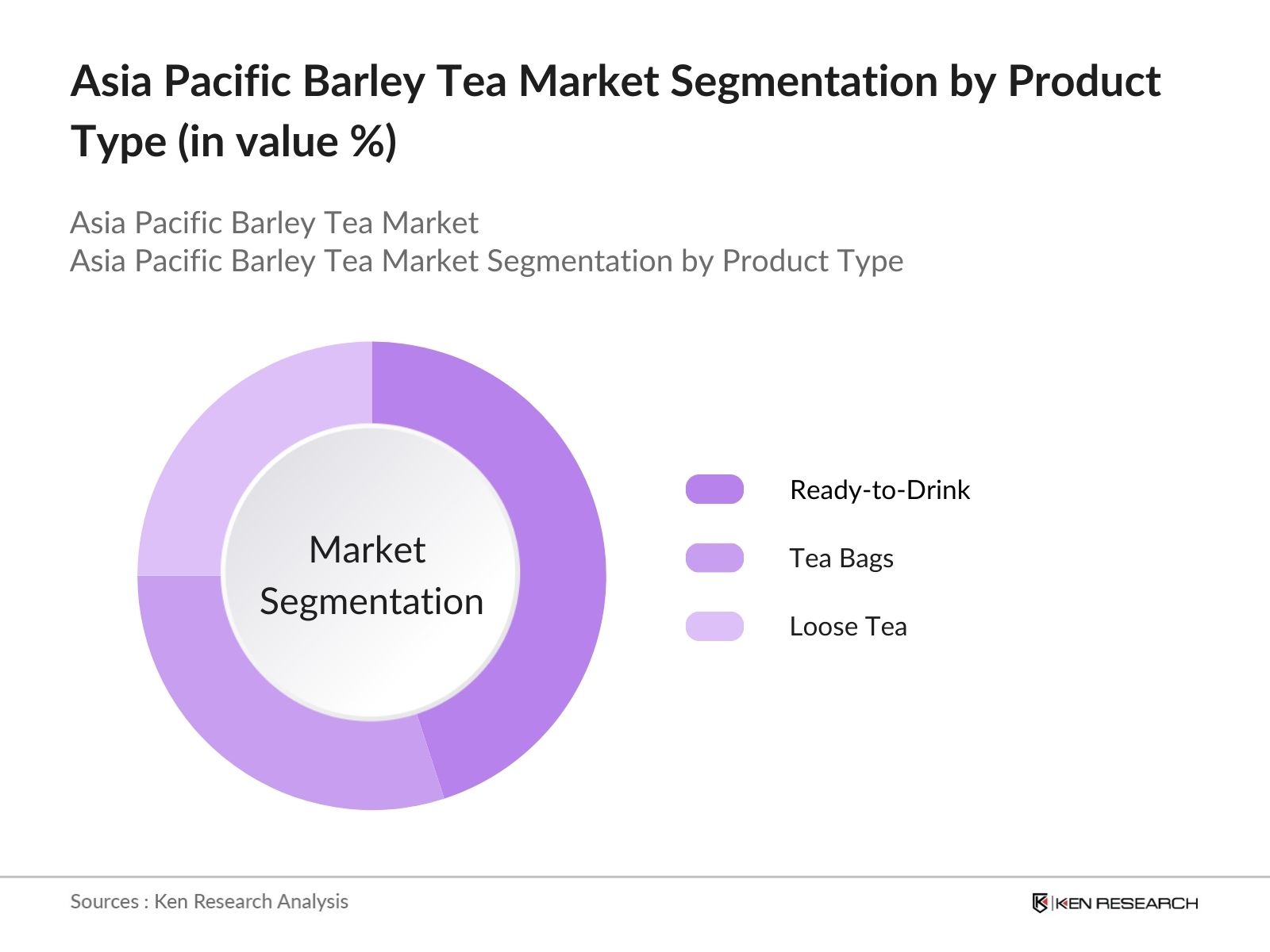

By Product Type: The Asia Pacific Barley Tea Market is segmented by product type into loose tea, tea bags, and ready-to-drink formats. Recently, ready-to-drink barley tea holds a significant share, attributed to the convenience it offers to on-the-go consumers, especially urban dwellers. The growth of ready-to-drink formats aligns with increasing demand for instant beverages in countries like Japan and South Korea, where such products are a regular part of daily routines.

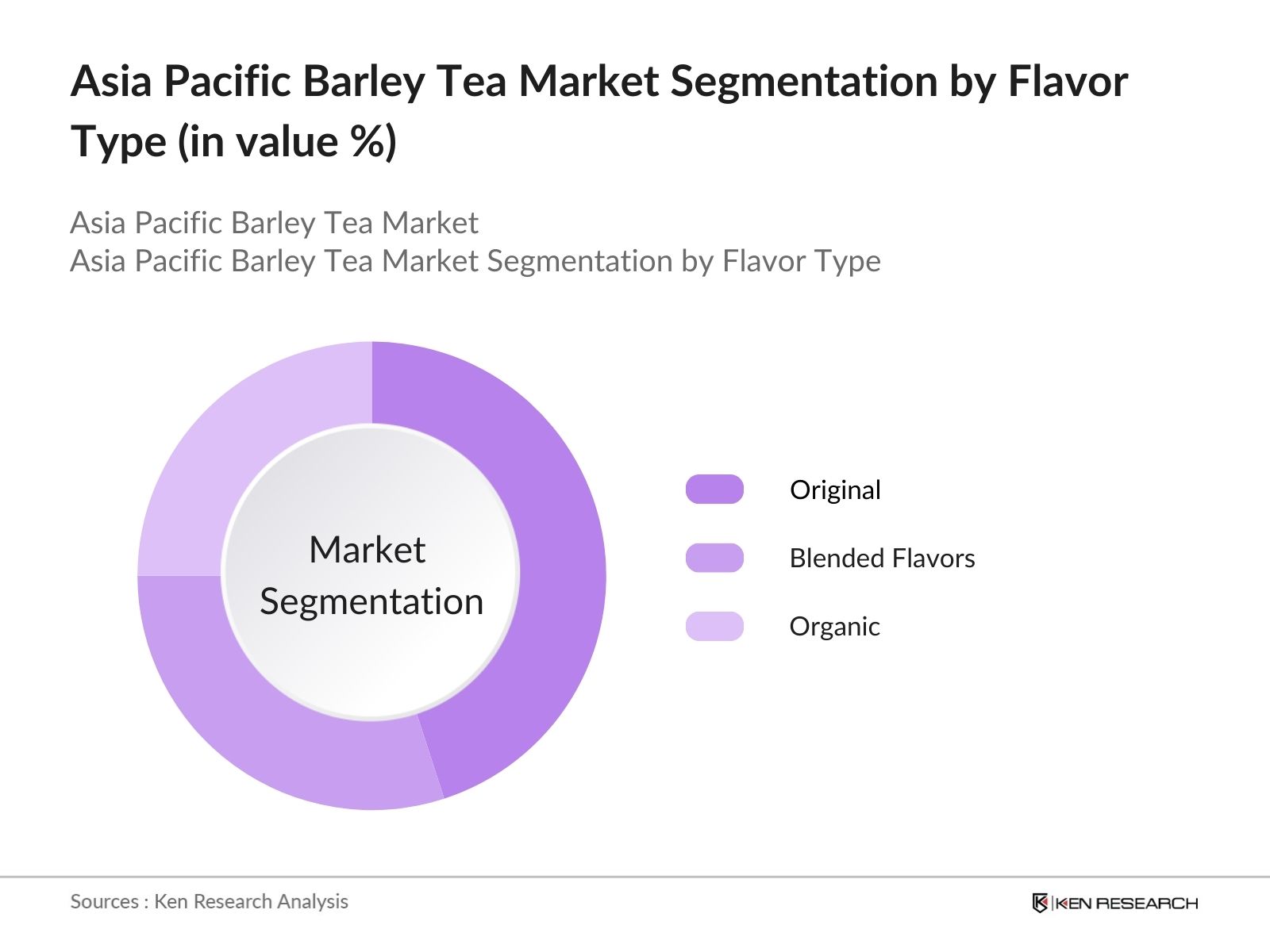

By Flavor Type: The market is also segmented by flavor type, including original, blended flavors (such as lemon and mint), and organic variants. Original flavors dominate, largely due to their longstanding cultural acceptance and simplicity in traditional diets across the Asia Pacific. Additionally, the preference for authentic, unaltered flavors in Japan and China has reinforced the market position of original-flavored barley tea.

The Asia Pacific Barley Tea Market is characterized by the presence of several key players, both domestic and international. Major companies dominate through strong distribution networks and focus on product innovation tailored to regional tastes.

The Asia Pacific Barley Tea Market is poised for sustained growth, driven by consumer health trends and expanding retail channels across urban and rural areas. Efforts toward sustainable packaging and increasing consumer awareness about barley tea's health benefits are expected to influence product preferences and expand market reach.

|

By Product Type |

Loose Tea Tea Bags Ready-to-Drink |

|

By Flavor Type |

Original Blended Flavors (e.g., Lemon, Mint) Organic |

|

By Distribution Channel |

Supermarkets & Hypermarkets Online Retail Specialty Stores Convenience Stores |

|

By End-User |

Household Food Service Sector (Hotels, Cafes) |

|

By Region |

China Japan South Korea Southeast Asia Oceania |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Rising Health Awareness

3.1.2. Increasing Adoption of Functional Beverages

3.1.3. Cultural Acceptance and Preferences

3.1.4. Growing Demand for Non-Caffeinated Beverages

3.2. Market Challenges

3.2.1. Limited Shelf Stability

3.2.2. Lack of Consumer Awareness in Rural Areas

3.2.3. Competition from Established Herbal Teas

3.3. Opportunities

3.3.1. Expansion of Online Retail Channels

3.3.2. Product Diversification (e.g., Flavored Barley Tea)

3.3.3. Increased Penetration into Emerging Economies

3.4. Trends

3.4.1. Organic and Natural Labeling

3.4.2. Enhanced Packaging Solutions

3.4.3. Adoption of Ready-to-Drink (RTD) Formats

3.5. Government Regulation

3.5.1. Food Safety Standards

3.5.2. Import and Export Regulations

3.5.3. Labeling Requirements for Health Beverages

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4.1. By Product Type (In Value %)

4.1.1. Loose Tea

4.1.2. Tea Bags

4.1.3. Ready-to-Drink

4.2. By Flavor Type (In Value %)

4.2.1. Original

4.2.2. Blended Flavors (e.g., Mint, Lemon)

4.2.3. Organic

4.3. By Distribution Channel (In Value %)

4.3.1. Supermarkets & Hypermarkets

4.3.2. Online Retail

4.3.3. Specialty Stores

4.3.4. Convenience Stores

4.4. By End-User (In Value %)

4.4.1. Household

4.4.2. Food Service Sector (Hotels, Cafes)

4.5. By Region (In Value %)

4.5.1. China

4.5.2. Japan

4.5.3. South Korea

4.5.4. Southeast Asia

4.5.5. Oceania

5.1. Detailed Profiles of Major Companies

5.1.1. Ito En, Ltd.

5.1.2. Harada Tea Processing Co., Ltd.

5.1.3. Suntory Holdings Limited

5.1.4. Oi Ocha

5.1.5. UCC Ueshima Coffee Co., Ltd.

5.1.6. Asahi Group Holdings, Ltd.

5.1.7. Daiohs Corporation

5.1.8. Marubeni Corporation

5.1.9. Kirin Beverage Company

5.1.10. Coca-Cola Bottlers Japan Inc.

5.1.11. Pokka Sapporo Food & Beverage Ltd.

5.1.12. Sanyo Foods Co., Ltd.

5.1.13. Tassei Co., Ltd.

5.1.14. Yamamotoyama Tea Company

5.1.15. Marutomo Co., Ltd.

5.2. Cross Comparison Parameters (Product Range, Market Presence, Distribution Networks, Revenue, Product Pricing, Innovation Rate, Sustainability Initiatives, Market Share)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Government Subsidies for Export

5.8. Partnership with Local Distributors

5.9. Private Equity Investments

6.1. Quality Standards Compliance

6.2. Certification Requirements for Organic Labeling

6.3. Import Tariffs and Trade Agreements

7.1. Future Market Size Projections

7.2. Key Factors Influencing Future Market Expansion

8.1. By Product Type (In Value %)

8.2. By Flavor Type (In Value %)

8.3. By Distribution Channel (In Value %)

8.4. By End-User (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Product Portfolio Enhancement

9.3. Regional Expansion Strategy

9.4. Consumer Engagement Strategies

Disclaimer Contact UsAn initial ecosystem map was created to identify all major stakeholders, including industry players and regulatory authorities, in the Asia Pacific Barley Tea Market. This step involved extensive desk research using proprietary and public databases to determine critical variables affecting the market.

Historical data was analyzed to construct a comprehensive market view, focusing on consumer demand and distribution networks. Data from these analyses were instrumental in understanding the current market dynamics and consumer trends.

Preliminary findings were validated through consultations with key industry experts via computer-assisted telephone interviews (CATIs), providing insights on competitive positioning, challenges, and growth opportunities.

The final phase incorporated feedback from major barley tea manufacturers, consolidating findings to ensure an accurate, data-backed market report aligned with industry insights.

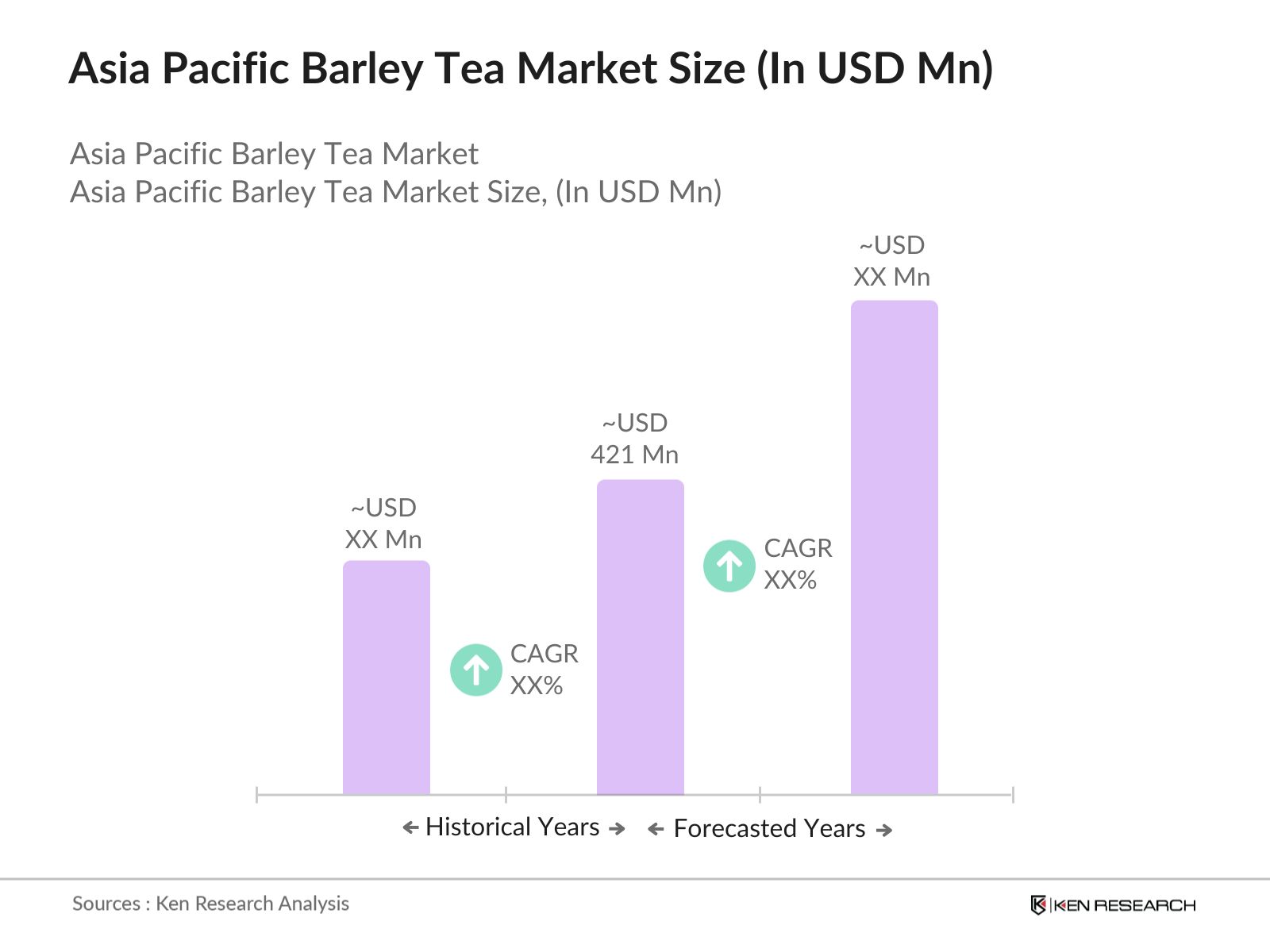

The Asia Pacific Barley Tea Market, valued at USD 421 million based on the latest data, is driven by rising health awareness and an increase in demand for non-caffeinated beverages.

Key challenges include limited shelf stability and the low awareness in certain rural regions, posing barriers to widespread adoption.

Major players include Ito En, Ltd., Suntory Holdings Ltd., and Asahi Group Holdings, which dominate due to extensive distribution networks and strong brand recognition.

The market is primarily driven by increasing demand for functional beverages, consumer health consciousness, and the popularity of barley tea as a staple drink in East Asian countries.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.