Asia-Pacific CAR T-Cell Therapy Market Outlook to 2030

Region:Afganistan

Author(s):Naman Rohilla

Product Code:KROD3527

Region:Afganistan

Author(s):Naman Rohilla

Product Code:KROD3527

November 2024

81

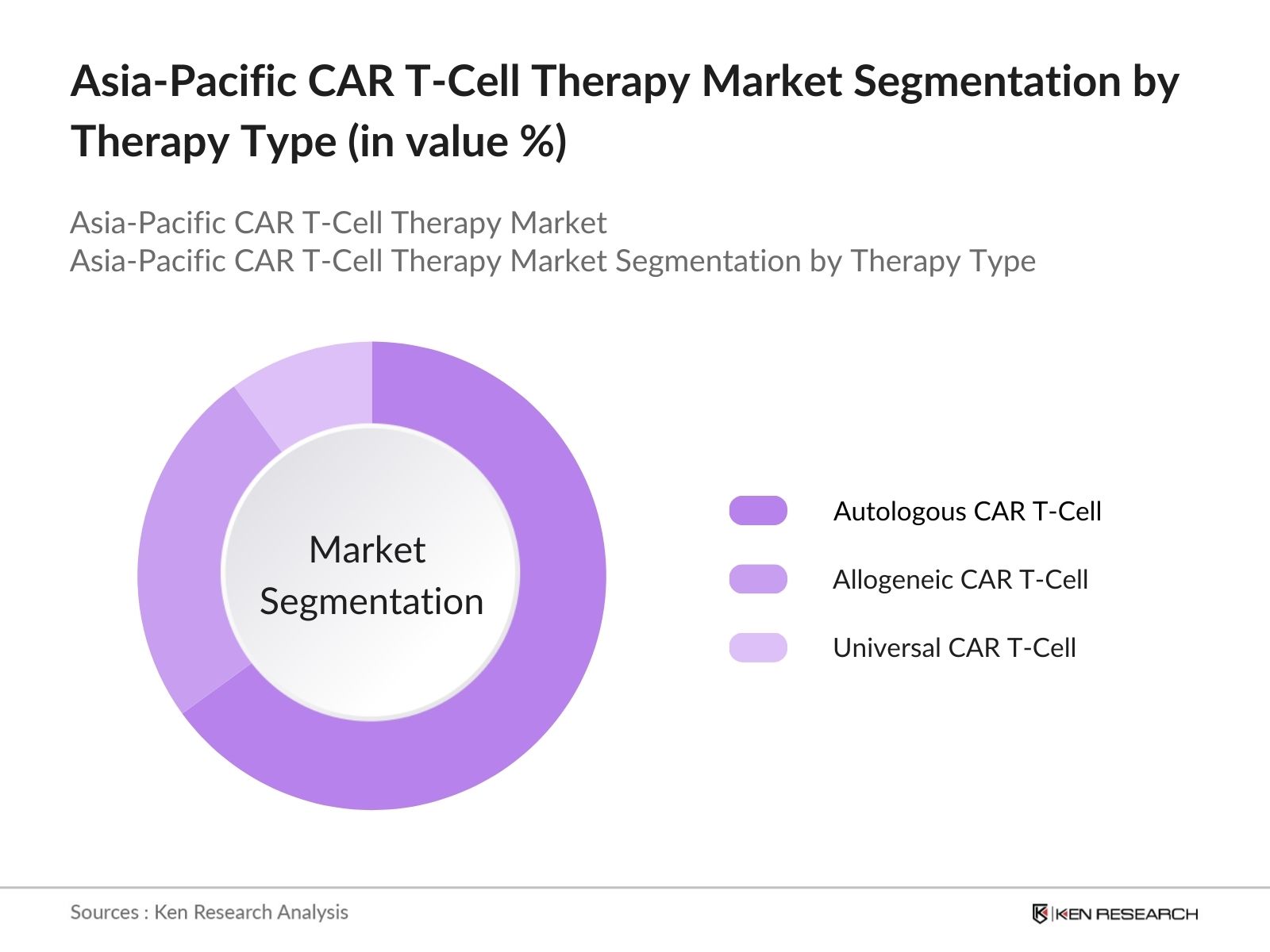

By Therapy Type: The Asia-Pacific CAR T-Cell Therapy market is segmented by therapy type into autologous CAR T-cell therapy, allogeneic CAR T-cell therapy, and universal CAR T-cell therapy. Autologous CAR T-cell therapy holds a dominant market share in this segmentation due to its high success rates in treating blood cancers like leukemia and lymphoma. The ability to tailor this therapy to individual patients by using their own cells has resulted in better efficacy and minimal immune rejection, making it the preferred choice in clinical applications.

By Target Antigen: The market is also segmented by target antigen into CD19, BCMA, CD22, and others. CD19-targeted CAR T-cell therapies hold the largest market share, largely due to their effectiveness in treating B-cell malignancies such as leukemia and lymphoma. This antigen has been widely studied and shows consistent success across multiple clinical trials, solidifying its position as the most widely used target for CAR T-cell therapy in the region.

The Asia-Pacific CAR T-Cell Therapy market is dominated by major global and regional players who have established strong R&D pipelines and clinical partnerships with healthcare institutions. The competitive landscape highlights the importance of strategic collaborations, especially between biotech firms and academic research centers, for the development of next-generation CAR T-cell therapies.

|

Company |

Establishment Year |

Headquarters |

Revenue (2023, USD Bn) |

No. of Employees |

R&D Expenditure |

Product Portfolio |

Global Presence |

Key Clients |

Strategic Alliances |

|

ABB Ltd. |

1988 |

Zurich, Switzerland |

- |

- |

- |

- |

- |

- |

- |

|

Fanuc Corporation |

1972 |

Oshino, Japan |

- |

- |

- |

- |

- |

- |

- |

|

KUKA Robotics |

1995 |

Augsburg, Germany |

- |

- |

- |

- |

- |

- |

- |

|

Yaskawa Electric Corp |

1915 |

Kitakyushu, Japan |

- |

- |

- |

- |

- |

- |

- |

|

Bharat Fritz Werner Ltd. (BFW) |

1961 |

Bengaluru, India |

- |

- |

- |

- |

- |

- |

- |

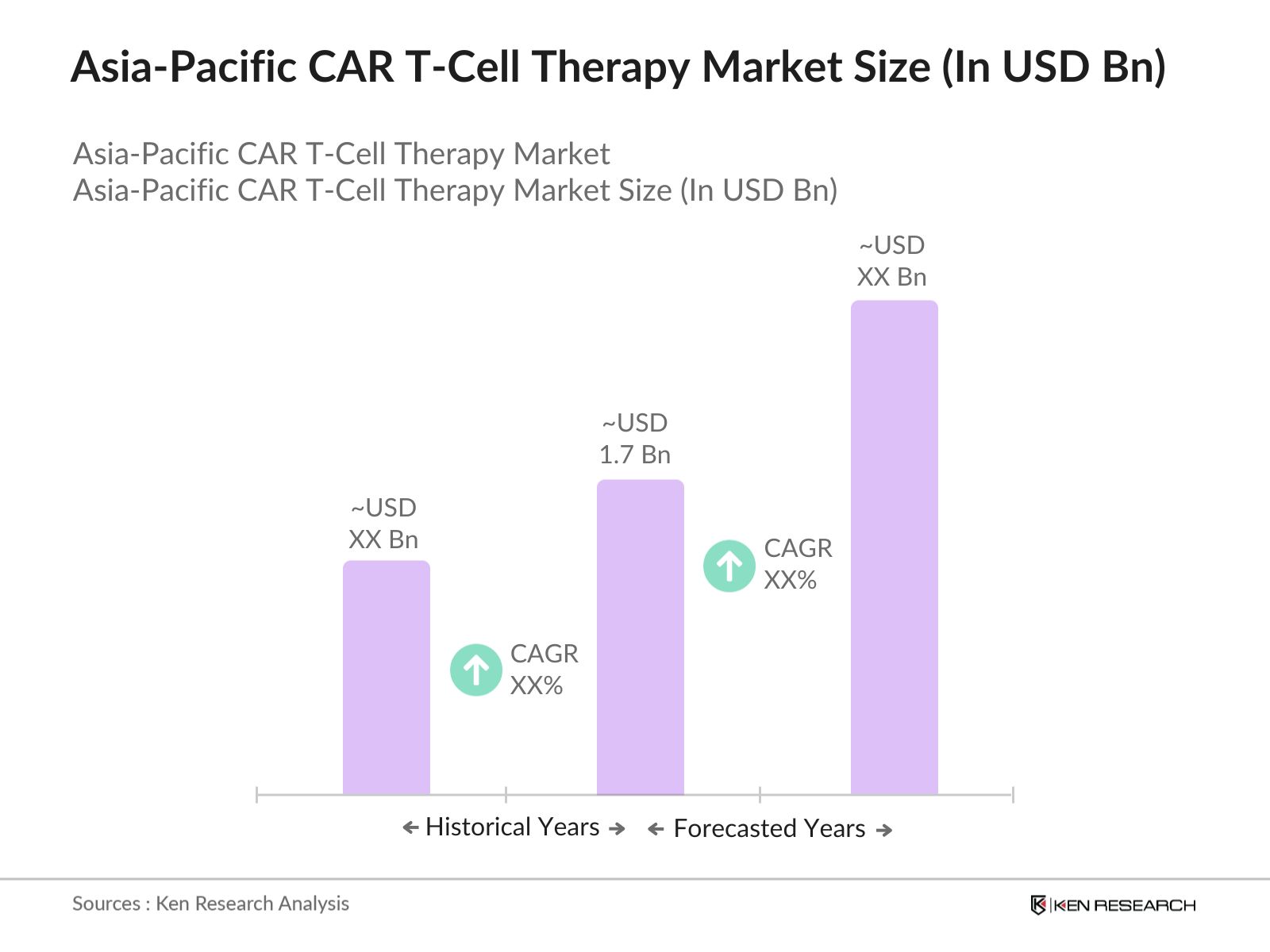

Over the next five years, the Asia-Pacific CAR T-Cell Therapy market is expected to experience growth due to continuous advancements in genetic engineering, increased clinical adoption, and expanding indications beyond hematologic cancers. Governments across the region are providing funding and fast-track approval processes, which will accelerate market expansion. With the ongoing development of allogeneic and off-the-shelf CAR-T therapies, cost reduction and accessibility are likely to improve, making these treatments more widely available.

|

By Type of Therapy |

Autologous CAR T-Cell Therapy Allogeneic CAR T-Cell Therapy Universal CAR T-Cell Therapy |

|

By Target Antigen |

CD19 BCMA CD22 Others |

|

By Therapeutic Area |

Hematologic Cancers (Leukemia, Lymphoma, Multiple Myeloma) Solid Tumors Autoimmune Diseases Others |

|

By End User |

Hospitals Cancer Research Centers Academic & Research Institutes |

|

By Region |

China Japan South Korea India Australia & New Zealand Rest of Asia-Pacific |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Rise in Hematologic Cancer Cases

3.1.2. Increasing Approval for CAR-T Therapies

3.1.3. Advancements in Gene Editing Technologies

3.1.4. Favorable Reimbursement Policies (Regulatory/Financial Incentives)

3.2. Market Challenges

3.2.1. High Manufacturing Costs

3.2.2. Stringent Regulatory Approvals (FDA/EMA Guidelines)

3.2.3. Limited Healthcare Infrastructure in Developing Nations

3.2.4. Supply Chain Disruptions in Cell Therapies

3.3. Opportunities

3.3.1. Strategic Partnerships and Collaborations (Pharma-Biotech Alliances)

3.3.2. Expansion of CAR T-Cell Applications (Solid Tumors and Autoimmune Diseases)

3.3.3. Technological Innovations in Cell Therapy Manufacturing

3.3.4. Clinical Trials and Product Launches in Emerging Markets

3.4. Trends

3.4.1. Development of Next-Generation CAR T-Cells (Allogeneic and Off-the-Shelf Therapies)

3.4.2. Integration of Artificial Intelligence in Therapy Design

3.4.3. Personalized and Precision Medicine Approach in Oncology

3.4.4. Use of Digital Health Platforms for Patient Monitoring and Follow-Up

3.5. Government Regulations and Policies

3.5.1. FDA and EMA CAR T-Cell Therapy Guidelines

3.5.2. National Oncology Programs and Initiatives

3.5.3. Financial Support and Incentives for Cancer Treatment

3.6. SWOT Analysis

3.7. Stake Ecosystem (Pharmaceutical Manufacturers, Biotech Startups, Hospitals, R&D Centers)

3.8. Porters Five Forces Analysis

3.9. Competitive Landscape Overview

4.1. By Type of Therapy (In Value %)

4.1.1. Autologous CAR T-Cell Therapy

4.1.2. Allogeneic CAR T-Cell Therapy

4.1.3. Universal CAR T-Cell Therapy

4.2. By Target Antigen (In Value %)

4.2.1. CD19

4.2.2. BCMA

4.2.3. CD22

4.2.4. Others

4.3. By Therapeutic Area (In Value %)

4.3.1. Hematologic Cancers (Leukemia, Lymphoma, Multiple Myeloma)

4.3.2. Solid Tumors

4.3.3. Autoimmune Diseases

4.3.4. Others

4.4. By End User (In Value %)

4.4.1. Hospitals

4.4.2. Cancer Research Centers

4.4.3. Academic & Research Institutes

4.5. By Region (In Value %)

4.5.1. China

4.5.2. Japan

4.5.3. South Korea

4.5.4. India

4.5.5. Australia & New Zealand

4.5.6. Rest of Asia-Pacific

5.1. Detailed Profiles of Major Competitors

5.1.1. Novartis AG

5.1.2. Gilead Sciences Inc.

5.1.3. Bristol-Myers Squibb Company

5.1.4. Johnson & Johnson

5.1.5. Pfizer Inc.

5.1.6. Amgen Inc.

5.1.7. Celgene Corporation

5.1.8. Bluebird Bio Inc.

5.1.9. Celyad Oncology

5.1.10. Kite Pharma

5.1.11. Legend Biotech

5.1.12. Autolus Therapeutics

5.1.13. Fate Therapeutics

5.1.14. CARsgen Therapeutics

5.1.15. Gracell Biotechnologies

5.2. Cross Comparison Parameters

5.2.1. Number of Employees

5.2.2. Headquarters

5.2.3. Inception Year

5.2.4. Revenue

5.2.5. Number of Approved Therapies

5.2.6. Number of Ongoing Clinical Trials

5.2.7. Manufacturing Capabilities (Cell Processing Units)

5.2.8. Research and Development Investments

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants and Funding Programs

5.9. Private Equity Investments

6.1. Regulatory Authorities (FDA, EMA, PMDA)

6.2. Compliance and Approval Processes

6.3. Clinical Trial Regulations

6.4. Manufacturing and Supply Chain Standards

6.5. Therapy Reimbursement Policies

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8.1. By Type of Therapy (In Value %)

8.2. By Target Antigen (In Value %)

8.3. By Therapeutic Area (In Value %)

8.4. By End User (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

The initial phase involved mapping the key stakeholders in the Asia-Pacific CAR T-Cell Therapy Market, leveraging proprietary databases and secondary sources. This helped identify critical variables like market drivers, challenges, and segmentation dynamics.

This phase involved analyzing historical data for the CAR T-Cell Therapy market. The data included market penetration rates, therapy adoption statistics, and regional revenue figures, compiled through secondary research.

Hypotheses about market trends and growth drivers were validated through consultations with CAR T-cell therapy experts. These consultations were conducted through CATIs with senior managers from pharmaceutical companies.

The final phase synthesized research insights from multiple stakeholders, including pharmaceutical companies and clinical trial investigators, to provide a complete market analysis.

The Asia-Pacific CAR T-Cell Therapy market was valued at USD 1.7 billion, driven by advancements in gene editing technologies and growing investment in cancer research.

Challenges include high manufacturing costs, supply chain bottlenecks, and stringent regulatory approvals that delay product commercialization.

Key players in the market include Novartis AG, Gilead Sciences Inc., Bristol-Myers Squibb, Johnson & Johnson, and Pfizer Inc. These companies dominate due to their extensive clinical pipelines and strong R&D investments.

Growth is driven by increased approvals of CAR T-cell therapies, government funding for cancer treatments, and technological advancements in genetic engineering.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.