Asia Pacific Coal to Liquid Market

Region:Asia

Author(s):Sanjna Verma

Product Code:KROD2197

October 2024

99

About the Report

Asia Pacific Coal to Liquid Market Overview

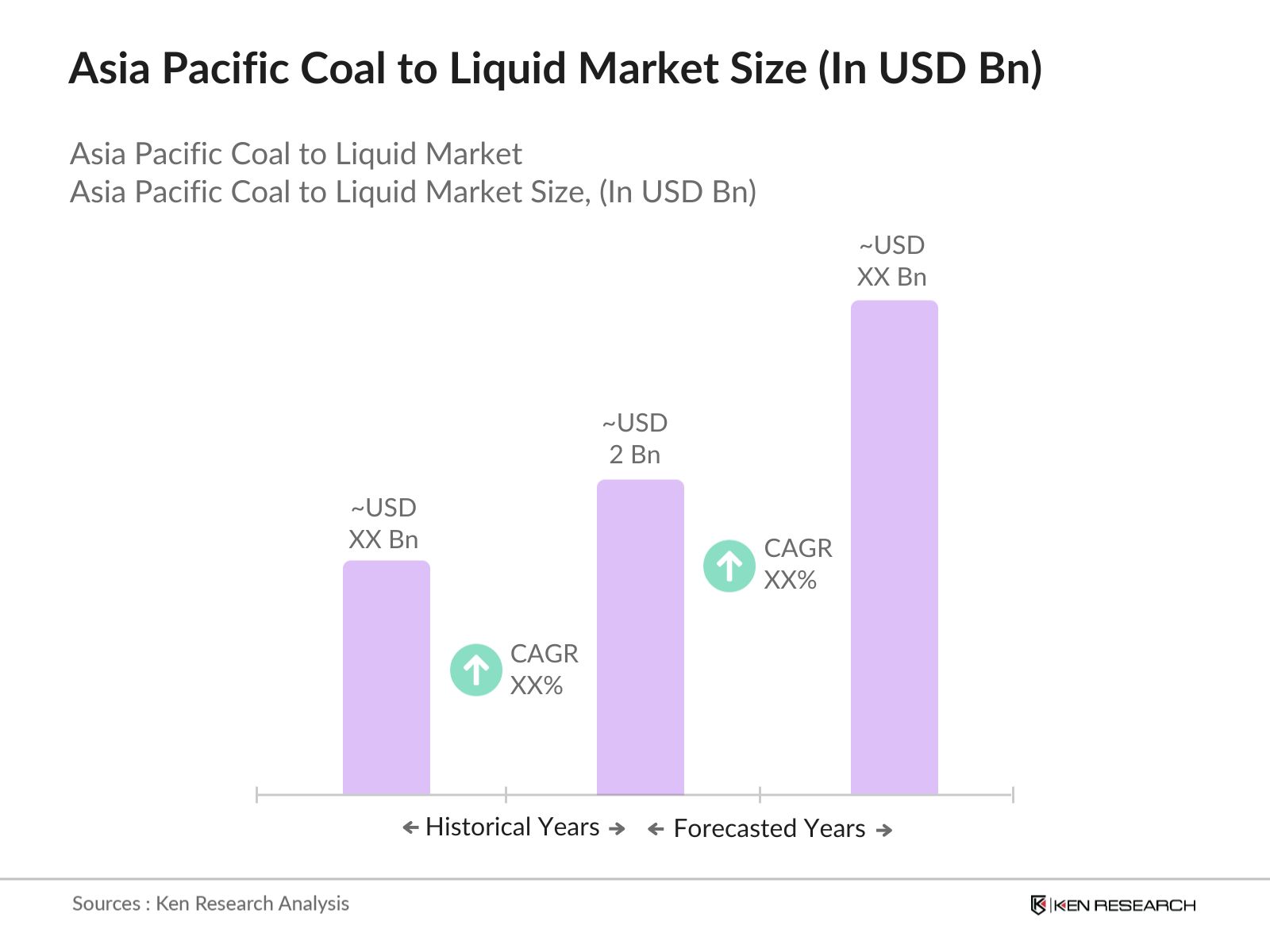

- In 2023, the Asia Pacific Coal to Liquid (CTL) market reached a size of USD 2 billion, driven by the region's increasing reliance on alternative fuels amid concerns over crude oil prices and energy security. Key players in the region are investing in coal liquefaction technologies to meet the growing demand for liquid fuels.

- Major players in the Asia Pacific CTL market include Shenhua Group (China), Sasol Limited (South Africa, but with strong operations in APAC), Yankuang Group (China), and Indian Oil Corporation (India). These companies are at the forefront of developing advanced coal liquefaction technologies to meet rising fuel demands

- In 2024, China Shenhua Energy Company Limited, a subsidiary of Shenhua Group, announced plans to acquire coal assets that will increase its coal production capacity by 20.7 million tonnes per year, including capacity from a mine under construction. The acquisition will expand Shenhua's coal production capabilities, allowing them to meet growing energy demands.

- Regions like Inner Mongolia in China, due to their coal-rich reserves, dominate CTL production. The proximity to major coal mines in these regions provides logistical advantages, significantly reducing transportation costs and supporting the development of CTL plants. This geographical advantage is crucial for the market’s dominance.

Asia Pacific Coal to Liquid Market Segmentation

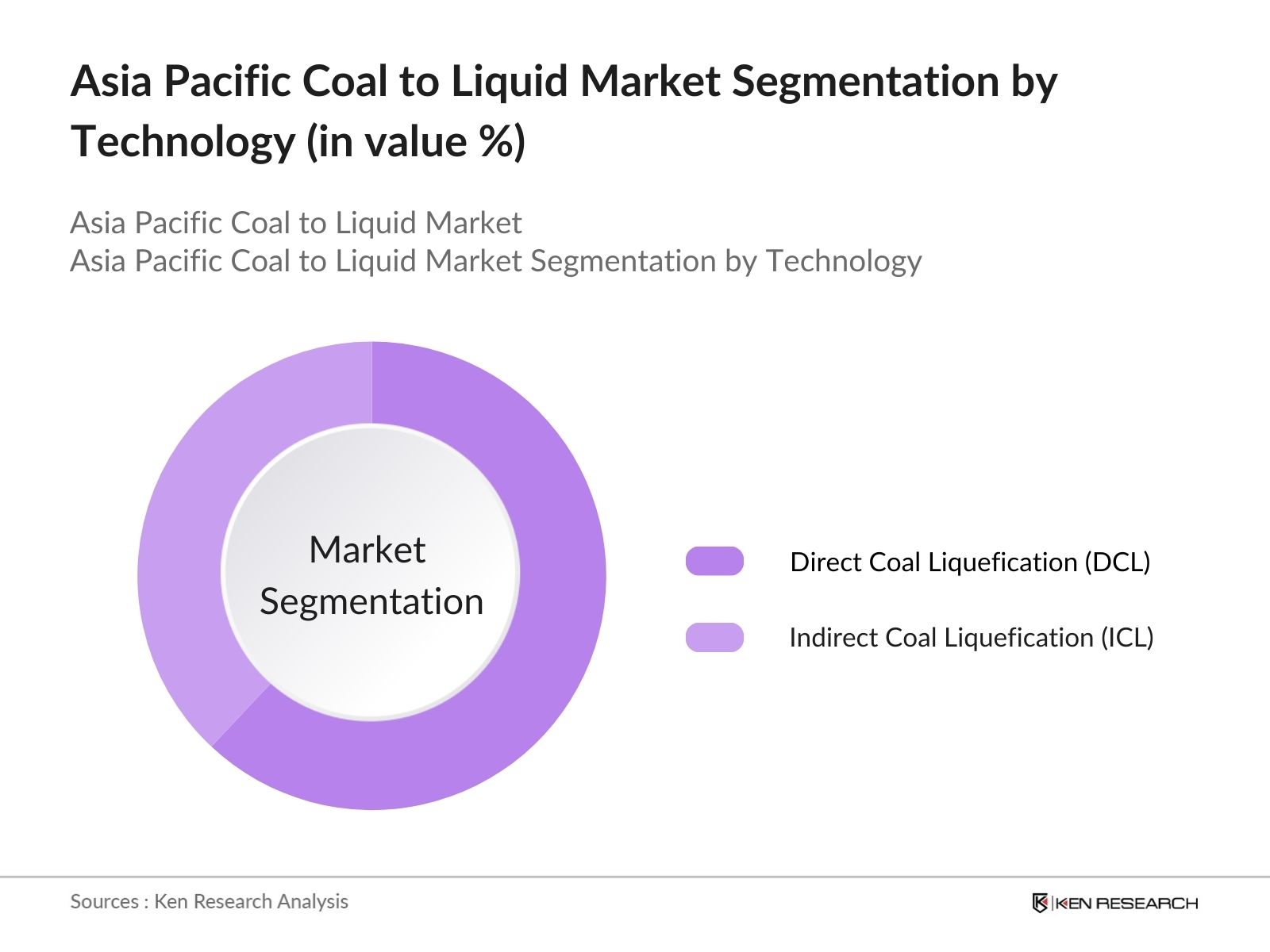

By Technology: The Asia Pacific Coal to Liquid Market is segmented by technology into direct coal liquefaction (DCL) and indirect coal liquefaction (ICL). In 2023, direct coal liquefaction led the market due to its higher efficiency in converting coal into liquid hydrocarbons. This method is particularly prominent in China, where the technology has been refined for industrial-scale applications. Indirect coal liquefaction, while less dominant, is gaining ground due to its flexibility in producing various fuel types.

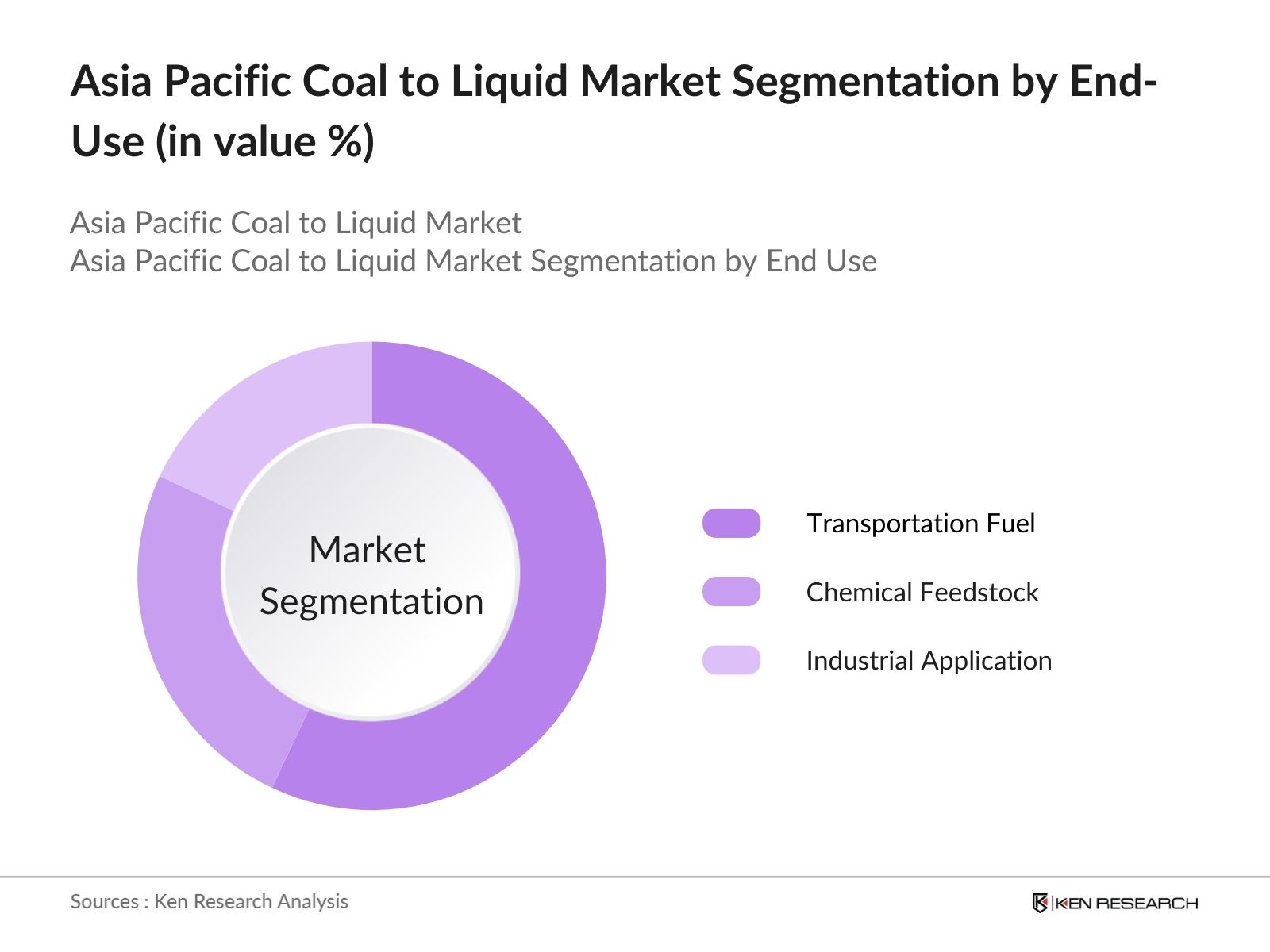

By End-Use: The CTL market is segmented into transportation fuel, chemical feedstock, and industrial applications. Transportation fuel holds the largest market share in 2023, driven by rising fuel demands across APAC economies like China, India, and South Korea. Coal-derived liquids are being used as an alternative to conventional petroleum fuels in regions where crude oil imports are costly. Chemical feedstock, while smaller, is growing due to the application of CTL in producing key chemicals like methanol.

By Region: The Asia Pacific CTL market is regionally segmented into China, India, South Korea, Japan, Australia, and the rest of the APAC region. In 2023, China emerged as the dominant market due to its significant coal reserves, extensive government support for CTL projects, and a focus on reducing crude oil dependence. India follows, with its government actively promoting coal-based energy technologies to reduce oil imports.

Asia Pacific Coal to Liquid Market Competitive Landscape

|

Company Name |

Establishment Year |

Headquarters |

|

Shenhua Group |

1995 |

Beijing, China |

|

Sasol Limited |

1950 |

Johannesburg, South Africa |

|

Yankuang Group |

1976 |

Shandong, China |

|

Indian Oil Corporation |

1959 |

New Delhi, India |

|

Sinopec Group |

1983 |

Beijing, China |

- Yankuang Group: In 2024, Yankuang Energy Group became the new strategic core shareholder of SMT Scharf AG, acquiring approximately 52.66% of the company at a price of EUR 11.10 per share. This acquisition is expected to create synergies between Yankuang, a leading manufacturer in the coal mining equipment sector, and SMT Scharf, which specializes in transportation solutions for underground mining.

- Indian Oil Corporation: In 2023, IOCL received approval from the National Company Law Tribunal (NCLT) for the acquisition of a 100% stake in Mercator Petroleum Limited (MPL) through the Corporate Insolvency Resolution Process (CIRP) for ?148 crore. MPL possesses an oil and gas exploration block in the Cambay Basin, Gujarat, which is located about 60 kilometers from IOCL's Koyali refinery.

Asia Pacific Coal to Liquid Industry Analysis

Growth Drivers:

- Abundant Coal Reserves: Asia Pacific countries like China and India have vast coal reserves that provide the raw material necessary for coal-to-liquid conversion. India's coal production rose to 893.19 million tonnes in 2022-23. The all-India Production of coal during 2023-24 was 997.83 MT with a positive growth of 11.71%. These reserves drive the CTL market as countries in the region seek to convert this resource into liquid fuels, supporting both transportation and industrial sectors.

- Rising Energy Demand in Emerging Economies: Rapid industrialization and urbanization across Asia Pacific have caused energy demand to surge, particularly in India, China, and Indonesia. As of 2022, India's total installed solar capacity exceeded 63 gigawatts (GW), having more than tripled over the past five years. This rising demand is pushing these countries to explore alternative energy sources like coal-to-liquid technology to reduce dependence on crude oil imports, making CTL a strategic energy solution for the future.

- Support from National Energy Policies: The Chinese government has prioritized coal-to-liquid technology under its 14th Five-Year Plan (2021-2025). The plan outlines objectives for technological advancements in coal synthesis and supports the construction of demonstration projects to improve efficiency and environmental practices in coal-to-chemicals, coal-to-oil, and coal-to-gas sectors.

Challenges:

- High Production Costs: Coal-to-liquid technology is capital-intensive, with high upfront costs for setting up plants and operating them. In 2023, it cost approximately $87,500 per barrel of daily capacity for a CTL plant in China. This expense makes the technology less attractive to smaller energy companies, especially when global oil prices drop, putting profitability under pressure.

- Technological Limitations: Although CTL technology has seen advancements, certain operational inefficiencies remain. Indirect coal liquefaction process suffers from a conversion efficiency. Half of the energy from coal is lost during processing. This makes the technology less efficient compared to other alternatives, such as renewable energy sources or natural gas. Additionally, the high carbon emissions and water consumption associated with CTL further exacerbate environmental concerns.

Government Initiatives:

- China’s National Energy Administration: The NEA was officially established in 2008. Under the 14th Five-Year Plan (2021-2025), the NEA aims to enhance the capacity of renewable energy to reach 1,200 gigawatts (GW) by 2030. This ambitious target reflects China's commitment to reducing carbon emissions and transitioning to a more sustainable energy system. This initiative aims to reduce crude oil imports by utilizing coal reserves for liquid fuel production, aligning with China’s goal of energy.

- India’s Ministry of Coal Initiative: The Indian Ministry of Coal announced the "National Coal Gasification Mission” which was launched in 2020, this mission aims to gasify 100 million tonnes of coal by 2030. It focuses on converting coal into synthesis gas (syngas) for cleaner energy production and reducing reliance on imported fuels. The mission includes financial incentives and policy support to promote coal gasification projects across the country.

Asia Pacific Coal to Liquid Future Market Outlook

Asia Pacific Coal to Liquid market is expected to continue expanding over the next five years, driven by growing demand for energy security and the utilization of abundant coal reserves. The market is projected to benefit from technological advancements that increase the efficiency of coal liquefaction processes while reducing environmental impacts.

Future Trends

- Adoption of Carbon Capture Technologies: In the future, the Asia Pacific CTL market will witness widespread adoption of carbon capture and storage (CCS) technologies. Governments will enforce stricter environmental regulations, and companies will invest heavily in CCS to mitigate the environmental impact of coal liquefaction. This will play a crucial role in aligning the CTL industry with sustainability goals.

- Increasing Investment in Cleaner CTL Technologies: The market will see significant investments aimed at improving the efficiency and environmental sustainability of CTL processes. Cleaner technologies will be developed, allowing for a reduction in carbon emissions during the liquefaction process.

Scope of the Report

|

By Technology |

Direct Coal Liquefaction (DCL) Indirect Coal Liquefaction (ICL) |

|

By End Use |

Transportation Fuel Chemical Feedstock Industrial Applications |

|

By Region |

China South Korea India Japan Australia Rest of APAC |

Products

Key Target Audience – Organizations and Entities Who Can Benefit by Subscribing This Report:

- Energy Corporations

- Fuel Distributors

- Coal Producers

- Chemical Manufacturers

- Logistics and Supply Chain Companies

- Investors and Venture Capitalists

- Government and Regulatory Bodies (e.g., China’s National Development and Reform Commission, India’s Ministry of Coal)

Time Period Captured in the Report:

- Historical Period: 2018-2023

- Base Year: 2023

- Forecast Period: 2023-2028

Companies

- Shenhua Group

- Sasol Limited

- Yankuang Group

- Indian Oil Corporation

- Sinopec Group

- China Coal Energy Company

- Adani Group

- Jindal Steel & Power

- Reliance Industries

- Bharat Petroleum Corporation

- Coal India Ltd

- Hyundai Oilbank

- Kawasaki Heavy Industries

- Posco Energy

- Itochu Corporation

Table of Contents

1. Asia Pacific Coal to Liquid Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Asia Pacific Coal to Liquid Market Size (in USD Billion)

2.1. Historical Market Size

2.2. Year-on-Year Growth Analysis

2.3. Market Forecast and Projections

2.4. Key Market Developments and Milestones

3. Asia Pacific Coal to Liquid Market Dynamics

3.1. Growth Drivers

3.1.1. Abundant Coal Reserves (China, India, Australia, Indonesia)

3.1.2. Rising Energy Demand (India, China, Southeast Asia)

3.1.3. Supportive Government Policies (14th Five-Year Plan, India’s Coal Gasification Mission)

3.1.4. Increasing Adoption of Alternative Fuels

3.2. Restraints

3.2.1. High Production Costs (Capital-Intensive CTL Projects)

3.2.2. Technological Challenges (Conversion Efficiency, Carbon Emissions)

3.2.3. Environmental Concerns (Water Consumption, Pollution)

3.3. Opportunities

3.3.1. Technological Innovations (Carbon Capture and Storage (CCS))

3.3.2. Expansion of Industrial Applications (Chemical Feedstock, Methanol Production)

3.3.3. Public-Private Collaborations

3.4. Trends

3.4.1. Development of Cleaner CTL Technologies

3.4.2. Increasing Investment in R&D (Efficiency Improvements, Environmental Sustainability)

3.4.3. Integration of Renewable Energy with CTL Processes

3.5. Government Regulation

3.5.1. China’s National Energy Administration Policies

3.5.2. India’s Ministry of Coal Initiatives

3.5.3. Environmental Standards and Certifications

3.6. SWOT Analysis (Strengths, Weaknesses, Opportunities, Threats)

3.7. Stakeholder Ecosystem (Governments, Energy Companies, Technology Providers, Financial Institutions)

3.8. Competition Ecosystem (Market Share Distribution, Competitive Positioning)

4. Asia Pacific Coal to Liquid Market Segmentation

4.1. By Technology

4.1.1. Direct Coal Liquefaction (DCL)

4.1.2. Indirect Coal Liquefaction (ICL)

4.2. By End-Use

4.2.1. Transportation Fuel

4.2.2. Chemical Feedstock

4.2.3. Industrial Applications

4.3. By Region

4.3.1. China (Dominance Due to Coal Reserves and Government Support)

4.3.2. India (Government Policies, Reducing Oil Import Dependence)

4.3.3. South Korea (Technological Advancements, Energy Security Goals)

4.3.4. Japan (Innovation in Cleaner CTL Technologies)

4.3.5. Australia (Coal Export and CTL Expansion)

4.3.6. Rest of APAC (Growth Prospects in Southeast Asia, Regional Coal Production)

5. Asia Pacific Coal to Liquid Market Competitive Landscape

5.1. Detailed Profiles of Major Competitors

5.1.1. Shenhua Group

5.1.2. Sasol Limited

5.1.3. Yankuang Group

5.1.4. Indian Oil Corporation

5.1.5. Sinopec Group

5.1.6. China Coal Energy Company

5.1.7. Adani Group

5.1.8. Jindal Steel & Power

5.1.9. Reliance Industries

5.1.10. Bharat Petroleum Corporation

5.1.11. Coal India Ltd

5.1.12. Hyundai Oilbank

5.1.13. Kawasaki Heavy Industries

5.1.14. Posco Energy

5.1.15. Itochu Corporation

5.2. Cross-Comparison Parameters (Company Inception, Headquarters, Revenue, Market Focus, Employee Strength)

6. Asia Pacific Coal to Liquid Market Competitive Analysis

6.1. Market Share Analysis

6.2. Strategic Initiatives

6.3. Investment Analysis

6.4. Technological Advancements

6.5. Company Profiles – Financial and Operational Analysis (Revenue, Profit Margins, Market Capitalization, Key Operations)

7. Asia Pacific Coal to Liquid Market Regulatory Framework

7.1. National Energy Policies (China, India, South Korea, Japan, Australia)

7.2. Compliance Requirements (Environmental Regulations, Safety Standards)

7.3. Certification Processes (Emission Standards, CTL Plant Certification)

8. Asia Pacific Coal to Liquid Future Market Size (in USD Billion)

8.1. Future Market Size Projections

8.2. Factors Driving Future Market Growth (Energy Demand, Technological Innovations, Regulatory Support)

9. Asia Pacific Coal to Liquid Future Market Segmentation

9.1. By Technology

9.1.1. Direct Coal Liquefaction (DCL)

9.1.2. Indirect Coal Liquefaction (ICL)

9.2. By End-Use

9.2.1. Transportation Fuel

9.2.2. Chemical Feedstock

9.2.3. Industrial Applications

9.3. By Region

9.3.1. China

9.3.2. India

9.3.3. South Korea

9.3.4. Australia

9.3.5. Rest of APAC

10. Asia Pacific Coal to Liquid Market Analysts' Recommendations

10.1. TAM/SAM/SOM Analysis (Total Addressable Market, Serviceable Addressable Market, Serviceable Obtainable Market)

10.2. Customer Cohort Analysis

10.3. White Space Opportunity Analysis

10.4. Strategic Recommendations for Market Entry/Expansion

Disclaimer

Contact Us

Research Methodology

Step 1: Identifying Key Variables:

Ecosystem creation for all the major entities and referring to multiple secondary and proprietary databases to perform desk research around market to collate industry level information.

Step 2: Market Building:

Collating statistics on Asia Pacific Coal to Liquid Market over the years, penetration of marketplaces and service providers ratio to compute revenue generated for Asia Pacific Coal to Liquid Market. We will also review service quality statistics to understand revenue generated which can ensure accuracy behind the data points shared.

Step 3: Validating and Finalizing:

Building market hypothesis and conducting CATIs with industry exerts belonging to different companies to validate statistics and seek operational and financial information from company representatives.

Step 4: Research output:

Our team will approach multiple Coal to Liquid suppliers and distributors companies and understand nature of product segments and sales, consumer preference and other parameters, which will support us validate statistics derived through bottom to top approach from Coal to Liquid suppliers and distributors companies.

Frequently Asked Questions

01 How big is Asia Pacific Coal to Liquid Market?

In 2023, the Asia Pacific Coal to Liquid (CTL) market reached a size of USD 2 billion, driven by the region's increasing reliance on alternative fuels amid concerns over crude oil prices and energy security. Key players in the region are investing in coal liquefaction technologies to meet the growing demand for liquid fuels.

02 What are the challenges in the Asia Pacific Coal to Liquid market?

Key challenges of Asia Pacific Coal to Liquid Market include high production costs, significant carbon emissions during the liquefaction process, and technological inefficiencies. These factors complicate the widespread adoption of CTL technology, particularly amid rising environmental concerns.

03 What are the growth drivers of Asia Pacific Coal to Liquid Market?

Growth drivers of Asia Pacific Coal to Liquid Market include the region's vast coal reserves, rising energy demand in rapidly industrializing nations like China and India, and supportive government initiatives aimed at reducing crude oil imports and enhancing energy security.

04 Who are the major players in the Asia Pacific Coal to Liquid Market?

Major players in the market include Shenhua Group, Sasol Limited, Yankuang Group, Indian Oil Corporation, and Sinopec Group. These companies lead the market due to their large-scale operations, strong government support, and access to extensive coal reserves.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.