Asia-Pacific Dry Mix Mortar Market Outlook to 2030

Region:Asia

Author(s):Naman Rohilla

Product Code:KROD8677

Region:Asia

Author(s):Naman Rohilla

Product Code:KROD8677

December 2024

80

The Asia-Pacific Dry Mix Mortar Market is characterized by a blend of multinational corporations and regional manufacturers. Dominated by established names like Sika AG, Saint-Gobain Weber, and BASF SE, the market witnesses strategic positioning focused on product innovation, sustainability, and regional expansion to capture demand. These firms' stronghold in the market stems from their extensive distribution networks, continuous R&D investments, and diversified product portfolios.

In the coming years, the Asia-Pacific Dry Mix Mortar Market is anticipated to show steady growth, driven by increasing urbanization, demand for time-efficient building solutions, and a strong emphasis on sustainability. The market will benefit from advancements in formulation technology, allowing for enhanced product performance and environmental compliance. The integration of lightweight and multi-functional mortars will cater to evolving construction practices, supporting a robust demand from residential and infrastructure segments.

|

Product Type |

Cement-Based Polymer Modified Epoxy-Based Lime-Based |

|

Application |

Tiling & Flooring Wall Plastering Repairing and Restoration Waterproofing |

|

End-User |

Residential Commercial Infrastructure |

|

Distribution Channel |

Direct Sales Retail Channels Online Distribution |

|

Region |

China India Japan South Korea Southeast Asia |

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Dynamics

1.4. Market Segmentation Overview

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3.1. Growth Drivers

3.1.1. Urbanization and Real Estate Growth

3.1.2. Demand for Time-Efficient Construction

3.1.3. Regulatory Push for Sustainable Building Materials

3.1.4. Innovation in Product Formulations

3.2. Market Challenges

3.2.1. Fluctuations in Raw Material Costs

3.2.2. Transportation and Storage Constraints

3.2.3. Skilled Labor Shortages in Mortar Application

3.3. Opportunities

3.3.1. Advancements in Lightweight Mortar Mixes

3.3.2. Expansion into High-Growth Regions

3.3.3. Increasing Demand for Waterproofing Solutions

3.4. Trends

3.4.1. Rise of Sustainable and Eco-Friendly Mixes

3.4.2. Adoption of Modular Construction Practices

3.4.3. Integration of Smart and Insulated Mortar Solutions

3.5. Regulatory Framework

3.5.1. Building Codes and Green Certifications

3.5.2. Restrictions on VOC Emissions

3.5.3. Standards for Product Quality and Consistency

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

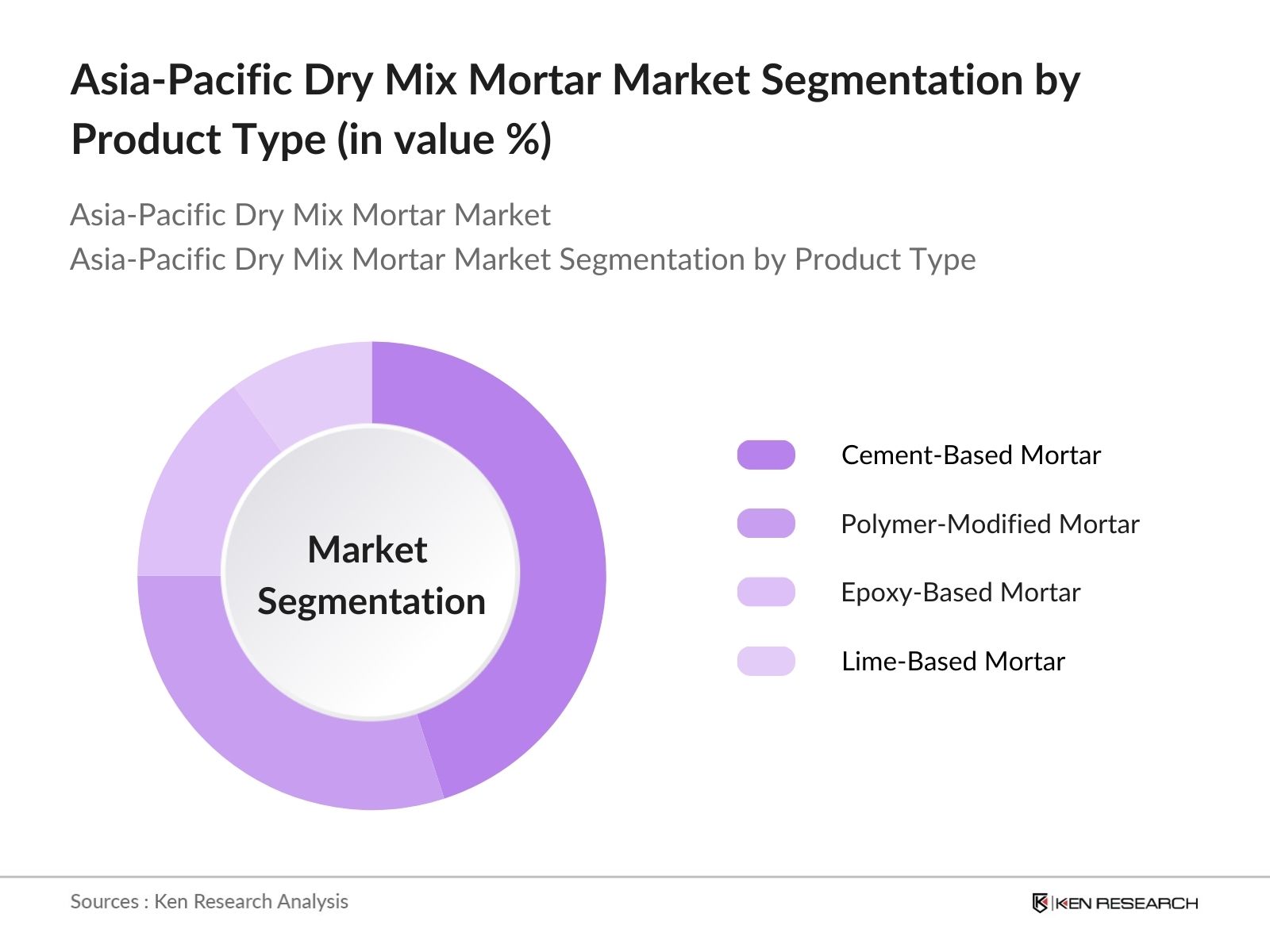

4.1. By Product Type (In Value %)

4.1.1. Cement-Based Mortar

4.1.2. Polymer Modified Mortar

4.1.3. Epoxy-Based Mortar

4.1.4. Lime-Based Mortar

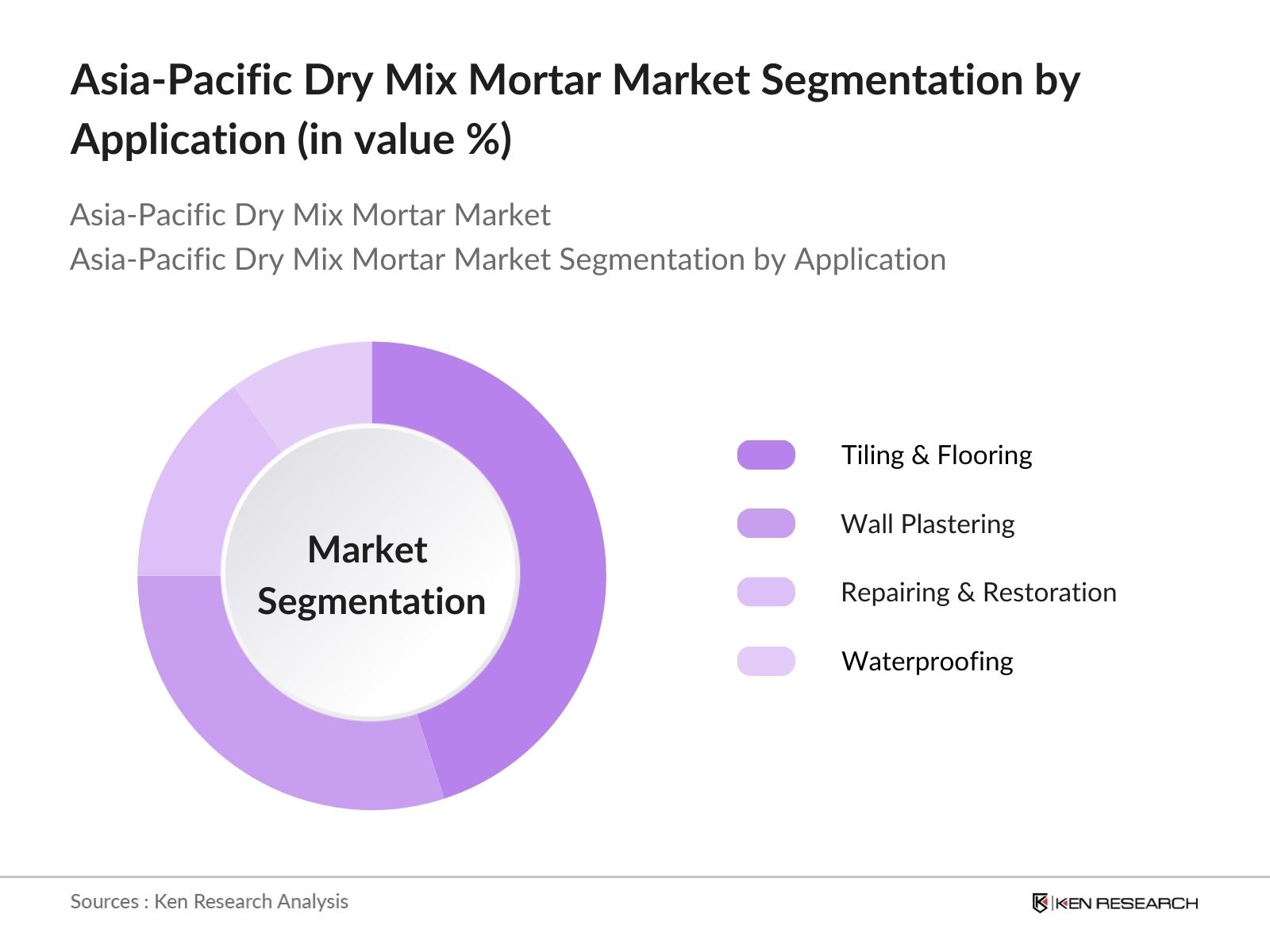

4.2. By Application (In Value %)

4.2.1. Tiling & Flooring

4.2.2. Wall Plastering

4.2.3. Repairing and Restoration

4.2.4. Waterproofing

4.3. By End-User (In Value %)

4.3.1. Residential

4.3.2. Commercial

4.3.3. Infrastructure

4.4. By Distribution Channel (In Value %)

4.4.1. Direct Sales

4.4.2. Retail Channels

4.4.3. Online Distribution

4.5. By Region (In Value %)

4.5.1. China

4.5.2. India

4.5.3. Japan

4.5.4. South Korea

4.5.5. Southeast Asia

5.1. Detailed Profiles of Major Companies

5.1.1. Sika AG

5.1.2. Saint-Gobain Weber

5.1.3. LafargeHolcim Ltd.

5.1.4. BASF SE

5.1.5. Mapei S.p.A

5.1.6. Ardex GmbH

5.1.7. CEMEX S.A.B. de C.V.

5.1.8. Dow Inc.

5.1.9. Fosroc International Ltd.

5.1.10. Parex Group

5.1.11. H.B. Fuller

5.1.12. Wacker Chemie AG

5.1.13. Knauf Group

5.1.14. Akzo Nobel N.V.

5.1.15. Adhesive Specialities

5.2. Cross Comparison Parameters (Number of Employees, Headquarters, Inception Year, Revenue, Product Portfolio, Geographical Presence, Market Share, Recent Product Innovations)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6.1. Environmental Standards and Codes

6.2. Compliance Requirements for VOC Content

6.3. Certification Processes for Sustainable Products

7.1. Market Size Projections

7.2. Key Drivers for Future Market Growth

8.1. By Product Type (In Value %)

8.2. By Application (In Value %)

8.3. By End-User (In Value %)

8.4. By Distribution Channel (In Value %)

8.5. By Region (In Value %)

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsThe initial step involves mapping the Asia-Pacific Dry Mix Mortar Market, identifying all significant stakeholders. Extensive desk research, supported by secondary databases, aids in defining the primary variables influencing market growth, such as material availability, environmental policies, and demand drivers.

A compilation of historical data assesses market penetration rates, market channels, and revenue flow within the dry mix mortar sector. Quality metrics are analyzed to ensure precise revenue estimates, giving insights into distribution networks, production capacities, and consumption patterns.

Using structured interviews with industry experts, this phase involves validating market hypotheses. Insights are gathered from professionals across companies in the mortar production, distribution, and application fields to enhance data accuracy and reflect real-time market conditions.

In the concluding stage, direct engagement with dry mix mortar manufacturers and distributors refines the analysis, covering product segmentation, demand cycles, and material sourcing. This interaction guarantees a comprehensive and validated representation of the Asia-Pacific Dry Mix Mortar Market.

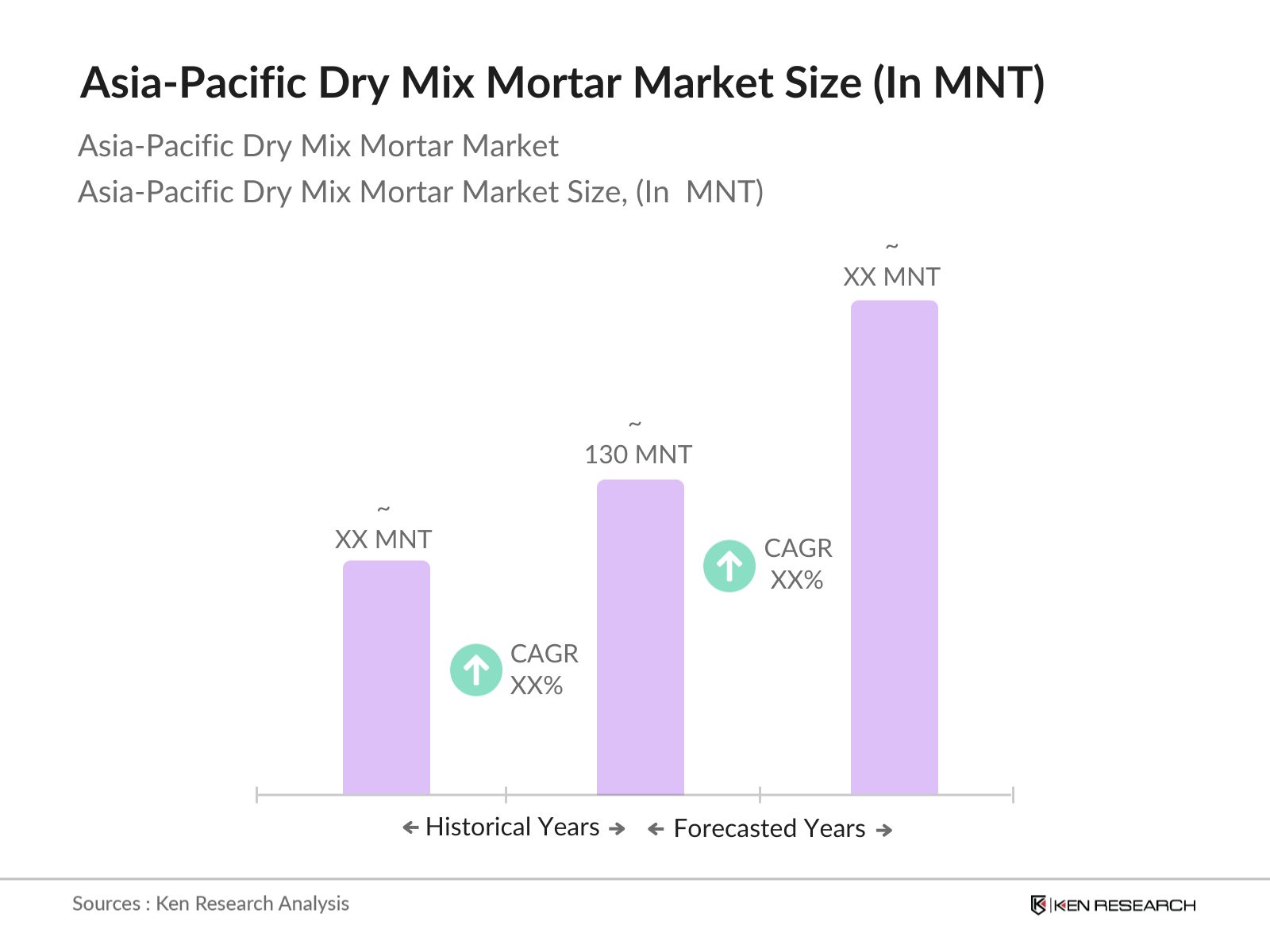

The Asia-Pacific Dry Mix Mortar Market, valued at 130 million tons, is primarily driven by the need for rapid and sustainable construction solutions in urbanizing economies.

Challenges include volatile raw material prices, high logistics costs, and the need for skilled labor in mortar applications, which impact the profitability of manufacturers.

Major players include Sika AG, Saint-Gobain Weber, BASF SE, Ardex GmbH, and Mapei S.p.A., who dominate due to established distribution networks and innovative product lines.

Key drivers include urbanization, demand for eco-friendly materials, and advances in mortar technology, fostering robust growth across residential and infrastructure sectors.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.