Asia Pacific Eclinical Solutions Market Outlook to 2030

Region:Asia

Author(s):Meenakshi Bisht

Product Code:KROD8029

December 2024

93

About the Report

Asia Pacific Eclinical Solutions Market Overview

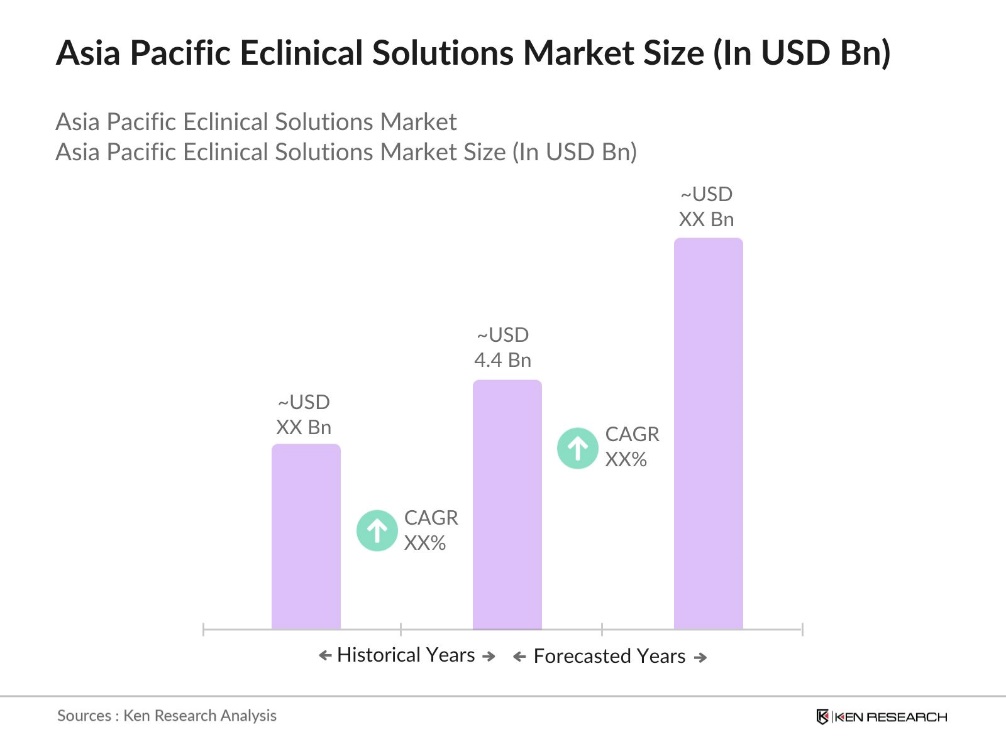

- The Asia Pacific eClinical solutions market is valued at USD 4.4 billion, based on a five-year historical analysis. The market is primarily driven by the increasing demand for advanced clinical trial management technologies and rising investment in biopharmaceutical research and development. A key driver for this market growth is the integration of eClinical solutions to streamline clinical trial processes, reduce manual data entry errors, and enhance compliance with regulatory standards.

- In the Asia Pacific region, countries such as China, India, and Japan dominate the eClinical solutions market. China leads due to its booming biopharmaceutical industry and supportive government initiatives promoting research in precision medicine and biotechnology. India and Japan also have substantial influence, with India benefiting from a growing CRO sector, while Japan boasts robust healthcare infrastructure and high investment in clinical trials.

- Governments across the Asia-Pacific region are enforcing Good Clinical Practice (GxP) standards for clinical data handling. In 2023, countries like Japan and Singapore implemented stringent guidelines to ensure that clinical data is collected, managed, and reported in compliance with international GxP standards. This regulatory push ensures the reliability and integrity of clinical trial data.

Asia Pacific Eclinical Solutions Market Segmentation

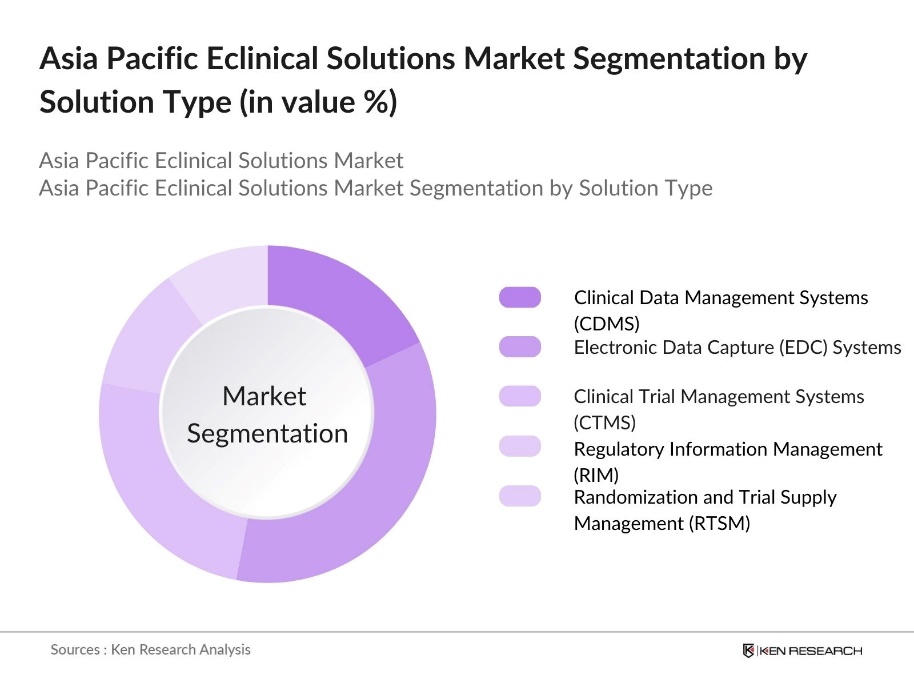

By Solution Type: The market is segmented by solution type into Clinical Data Management Systems (CDMS), Electronic Data Capture (EDC) Systems, Clinical Trial Management Systems (CTMS), Regulatory Information Management (RIM), and Randomization and Trial Supply Management (RTSM). Among these, Electronic Data Capture (EDC) systems hold a dominant market share due to their widespread adoption in clinical trials to capture, store, and manage clinical data more efficiently. EDC systems reduce the complexities of manual data entry, ensuring data accuracy, faster retrieval, and easier regulatory compliance. Major pharmaceutical companies rely heavily on these systems, making them the preferred solution.

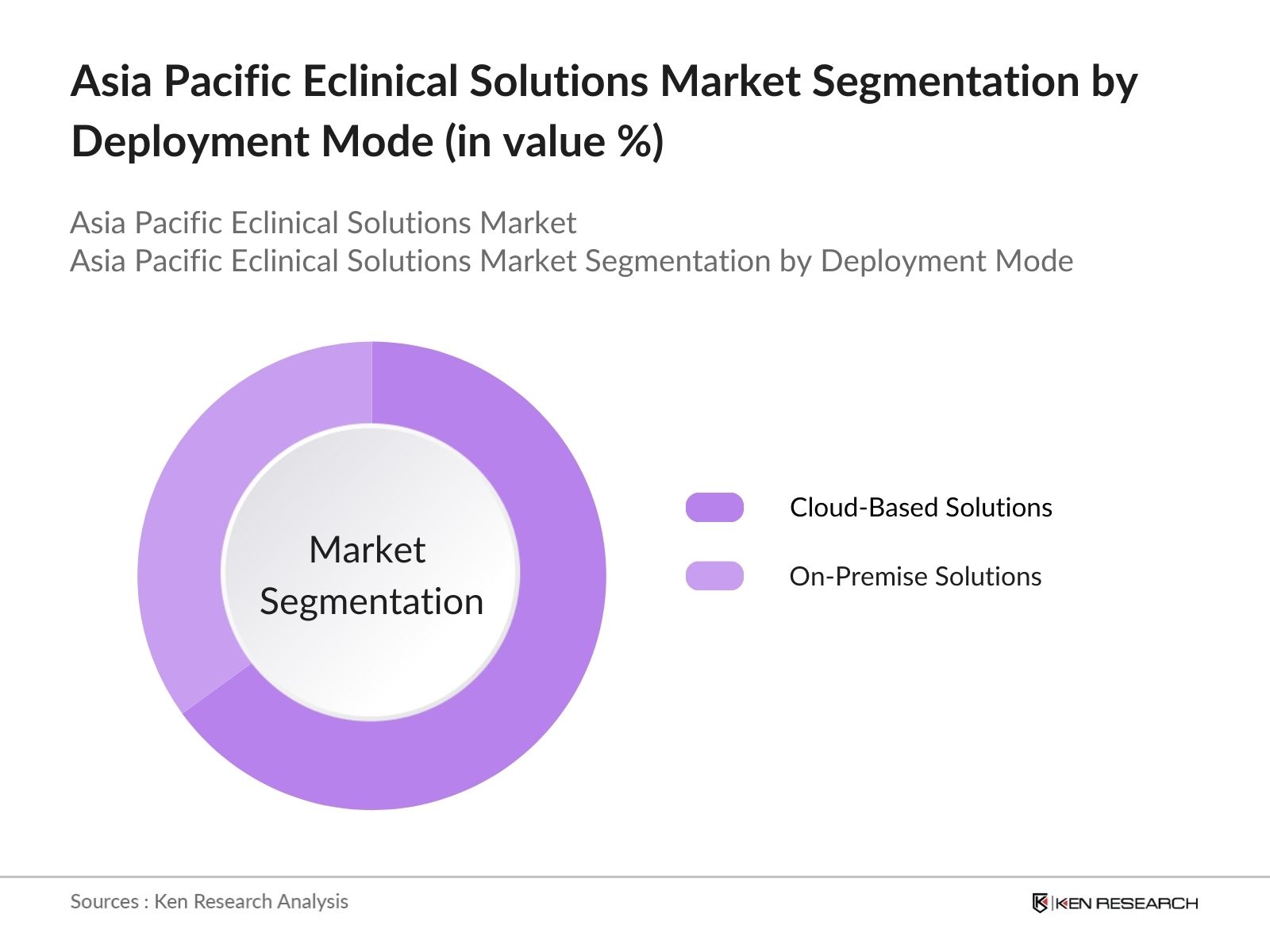

By Deployment Mode: The market is further segmented by deployment mode into Cloud-Based Solutions and On-Premise Solutions. Cloud-based solutions dominate due to their scalability, cost-effectiveness, and ease of integration with other digital systems. The cloud model allows real-time data access and collaboration across different geographic locations, which is crucial for global clinical trials. In contrast, on-premise solutions, though still in use, are limited due to higher costs and the need for extensive IT infrastructure.

Asia Pacific Eclinical Solutions Market Competitive Landscape

The Asia Pacific eClinical solutions market is dominated by a few major global and regional players who leverage their innovative solutions and expansive reach to maintain market share. Some key players include Oracle Health Sciences, Medidata Solutions, and Veeva Systems. The market shows a consolidated structure, with the top players controlling a large portion of the market. These companies often engage in strategic partnerships with pharmaceutical companies and CROs to enhance their service portfolios and reach.

Asia Pacific Eclinical Solutions Industry Analysis

Growth Drivers

- Increasing Adoption of Eclinical Solutions in Clinical Trials: The adoption of eClinical solutions is significantly rising across the Asia-Pacific region due to the increasing number of clinical trials. For instance, it was reported that over 70,000 new clinical trials were registered in the APAC region from 2017 to 2021, with China and India together accounting for approximately 40% of these trials. This growth is driven by regulatory frameworks such as the Indian Council of Medical Research's guidelines, which encourage digital clinical trial management to streamline processes.

- Regulatory Mandates for Data Standardization: Countries in the Asia-Pacific region are implementing stringent regulations to ensure the standardization of clinical data. In 2023, the International Council for Harmonisation (ICH) guidelines were widely adopted in markets like Japan, South Korea, and Australia, mandating eClinical solutions to ensure standardized data collection. Governments are pushing for the interoperability of clinical data, particularly through policies like Australias Clinical Trials Ready initiative.

- Expansion of CRO Services (Contract Research Organizations): Contract Research Organizations (CROs) are expanding their presence in the Asia-Pacific region, driven by the region's lower operational costs and large patient pool. According to the World Bank, healthcare expenditure in Southeast Asia reached $156.3 billion in 2021, boosting the demand for CRO services to manage clinical trials efficiently. This expansion fosters the use of eClinical solutions, as these organizations increasingly rely on digital tools for managing and streamlining clinical data.

Market Challenges

- Data Security and Privacy Concerns: The growing adoption of eClinical solutions raises significant concerns around data security and privacy. Countries like India and Singapore have introduced stricter data protection laws, such as Indias Personal Data Protection Bill, impacting clinical trial data handling. Compliance with these regulations requires robust encryption and access controls, adding complexity and cost for organizations, as they must balance data security with efficient clinical research processes.

- High Implementation Costs: Implementing eClinical solutions involves substantial costs, creating challenges for smaller healthcare organizations in Asia-Pacific. While larger institutions can afford advanced platforms, smaller ones struggle with financial constraints. Government healthcare budgets in many countries are often insufficient to support technological upgrades, resulting in uneven adoption of eClinical systems across the region. This cost barrier limits the widespread integration of these platforms in clinical research.

Asia Pacific Eclinical Solutions Market Future Outlook

Over the next few years, the Asia Pacific eClinical solutions market is expected to exhibit considerable growth, driven by the increasing digital transformation of healthcare services and advancements in artificial intelligence and machine learning. Additionally, the demand for cloud-based solutions will continue to surge, as companies seek cost-efficient, scalable solutions to handle vast amounts of clinical data. Regulatory agencies in the region are also expected to play a pivotal role by implementing stricter data compliance frameworks, which will further boost the demand for eClinical solutions.

Market Opportunities

- Emerging Markets for Clinical Trials: merging markets such as Vietnam, Malaysia, and Indonesia offer new opportunities for clinical trials due to lower operational costs and large patient populations. These regions are experiencing increased healthcare investment and reforms, making them attractive for clinical research. As healthcare infrastructure continues to improve, the adoption of eClinical solutions in these markets is expected to grow, supporting the expansion of clinical trials in these rapidly developing regions.

- AI and Machine Learning in Clinical Data Management: The integration of AI and machine learning in clinical data management presents significant opportunities for the eClinical solutions market in Asia-Pacific. AI-driven tools can enhance data analysis, patient monitoring, and decision-making processes in clinical trials. Governments across the region are promoting AI innovations, which are reshaping clinical data management. This technology helps streamline operations and improve trial efficiency, positioning AI as a transformative force in the clinical research landscape.

Scope of the Report

|

Solution Type |

Clinical Data Management Systems (CDMS) Electronic Data Capture (EDC) Systems Clinical Trial Management Systems (CTMS) Regulatory Information Management (RIM) Randomization and Trial Supply Management (RTSM) |

|

Deployment Mode |

Cloud-Based Solutions On-Premise Solutions |

|

End-User |

Pharmaceutical Companies CROs Academic Research Institutes Medical Device Manufacturers |

|

Phase of Clinical Trial |

Phase I Phase II Phase III Phase IV |

|

Country |

China India Japan Australia South Korea |

Products

Key Target Audience

Pharmaceutical Companies

Contract Research Organizations (CROs)

Biotechnology Companies

Healthcare Technology Companies

Medical Device Manufacturers

Government and Regulatory Bodies (e.g., FDA, TGA, CDSCO)

Investors and venture capital Firms

Banks and Financial Institutions

Companies

Players Mentioned in the Report

Oracle Health Sciences

Medidata Solutions

Veeva Systems

Parexel International

Bioclinica

Dassault Systmes (Medidata Rave)

CRF Health

IBM Watson Health

ICON plc

Clario

Table of Contents

1. Asia Pacific Eclinical Solutions Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Asia Pacific Eclinical Solutions Market Size (In USD Mn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Asia Pacific Eclinical Solutions Market Analysis

3.1. Growth Drivers

3.1.1. Increasing Adoption of Eclinical Solutions in Clinical Trials

3.1.2. Rising Demand for Automation in Clinical Research

3.1.3. Regulatory Mandates for Data Standardization

3.1.4. Expansion of CRO Services (Contract Research Organizations)

3.2. Market Challenges

3.2.1. Data Security and Privacy Concerns

3.2.2. High Implementation Costs

3.2.3. Complex Integration of Legacy Systems

3.3. Opportunities

3.3.1. Emerging Markets for Clinical Trials

3.3.2. AI and Machine Learning in Clinical Data Management

3.3.3. Cloud-Based Eclinical Solutions Adoption

3.4. Trends

3.4.1. Integration of Wearable Devices in Clinical Trials

3.4.2. Real-World Evidence (RWE) in Clinical Decision Making

3.4.3. Increased Use of Decentralized Clinical Trials

3.5. Regulatory Environment

3.5.1. Clinical Data Transparency Regulations

3.5.2. Data Standardization and Interoperability Guidelines

3.5.3. GxP Compliance for Clinical Data

3.6. SWOT Analysis

3.7. Stakeholder Ecosystem

3.8. Porters Five Forces

3.8.1. Bargaining Power of Suppliers

3.8.2. Bargaining Power of Buyers

3.8.3. Threat of New Entrants

3.8.4. Threat of Substitutes

3.8.5. Industry Rivalry

3.9. Competition Ecosystem

4. Asia Pacific Eclinical Solutions Market Segmentation

4.1. By Solution Type (In Value %)

4.1.1. Clinical Data Management Systems (CDMS)

4.1.2. Electronic Data Capture (EDC) Systems

4.1.3. Clinical Trial Management Systems (CTMS)

4.1.4. Regulatory Information Management (RIM)

4.1.5. Randomization and Trial Supply Management (RTSM)

4.2. By Deployment Mode (In Value %)

4.2.1. Cloud-Based Solutions

4.2.2. On-Premise Solutions

4.3. By End-User (In Value %)

4.3.1. Pharmaceutical Companies

4.3.2. Contract Research Organizations (CROs)

4.3.3. Academic Research Institutes

4.3.4. Medical Device Manufacturers

4.4. By Phase of Clinical Trial (In Value %)

4.4.1. Phase I

4.4.2. Phase II

4.4.3. Phase III

4.4.4. Phase IV

4.5. By Country (In Value %)

4.5.1. China

4.5.2. India

4.5.3. Japan

4.5.4. Australia

4.5.5. South Korea

5. Asia Pacific Eclinical Solutions Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. Oracle Health Sciences

5.1.2. Medidata Solutions, Inc.

5.1.3. Parexel International Corporation

5.1.4. Veeva Systems

5.1.5. CRF Health

5.1.6. Bioclinica

5.1.7. IBM Watson Health

5.1.8. Dassault Systmes (Medidata Rave)

5.1.9. ICON plc

5.1.10. Clario

5.1.11. ArisGlobal

5.1.12. Medrio

5.1.13. Castor EDC

5.1.14. Signant Health

5.1.15. eClinicalWorks

5.2. Cross Comparison Parameters (No. of Employees, Headquarters, Inception Year, Revenue, Global vs Regional Focus, Solution Portfolio, Software Usability, Market Presence)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. Asia Pacific Eclinical Solutions Market Regulatory Framework

6.1. Data Compliance and Security Regulations

6.2. Clinical Trial Reporting Requirements

6.3. Interoperability Standards

6.4. GxP Regulatory Requirements

7. Asia Pacific Eclinical Solutions Future Market Size (In USD Mn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Asia Pacific Eclinical Solutions Future Market Segmentation

8.1. By Solution Type (In Value %)

8.2. By Deployment Mode (In Value %)

8.3. By End-User (In Value %)

8.4. By Phase of Clinical Trial (In Value %)

8.5. By Country (In Value %)

9. Asia Pacific Eclinical Solutions Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

The first step involves a comprehensive analysis of the major stakeholders in the Asia Pacific eClinical Solutions Market. Through secondary research, the industry-level information was gathered to understand market dynamics and identify critical variables such as regulatory requirements, technological advancements, and market drivers.

Step 2: Market Analysis and Construction

Next, we compiled historical data to analyze key trends, adoption rates of eClinical solutions, and their revenue contribution. This process included assessing clinical trial volumes, the number of service providers, and the impact of digitalization on clinical trial management.

Step 3: Hypothesis Validation and Expert Consultation

We engaged with industry experts using CATIS and conducted interviews with clinical trial managers, pharmaceutical companies, and technology vendors. These consultations helped validate our assumptions and added valuable insights into market drivers and barriers.

Step 4: Research Synthesis and Final Output

The final step involved synthesizing the research findings and verifying the data with leading clinical solution vendors to ensure accurate market estimates. This data was then cross-referenced with publicly available reports and government publications to deliver a well-rounded analysis.

Frequently Asked Questions

01. How big is the Asia Pacific eClinical Solutions Market?

The Asia Pacific eClinical solutions market is valued at USD 4.4 billion, driven by the increasing adoption of digital clinical trial technologies, and biopharmaceutical research activities.

02. What are the challenges in the Asia Pacific eClinical Solutions Market?

Challenges in the Asia Pacific eClinical solutions market include high implementation costs, integration issues with legacy systems, and growing concerns over data security and privacy regulations.

03. Who are the major players in the Asia Pacific eClinical Solutions Market?

Key players in the Asia Pacific eClinical solutions market include Oracle Health Sciences, Medidata Solutions, Veeva Systems, Parexel International, and Bioclinica. These companies dominate due to their extensive product portfolios and strategic partnerships.

04. What are the growth drivers of the Asia Pacific eClinical Solutions Market?

The growth drivers in Asia Pacific eClinical solutions market include increased demand for automation in clinical trials, regulatory pressure for data standardization, and rising investment in biopharmaceutical research.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.