Asia-Pacific Edge Computing Market Outlook to 2030

Region:Asia

Author(s):Naman Rohilla

Product Code:KROD3384

November 2024

97

About the Report

Asia-Pacific Edge Computing Market Overview

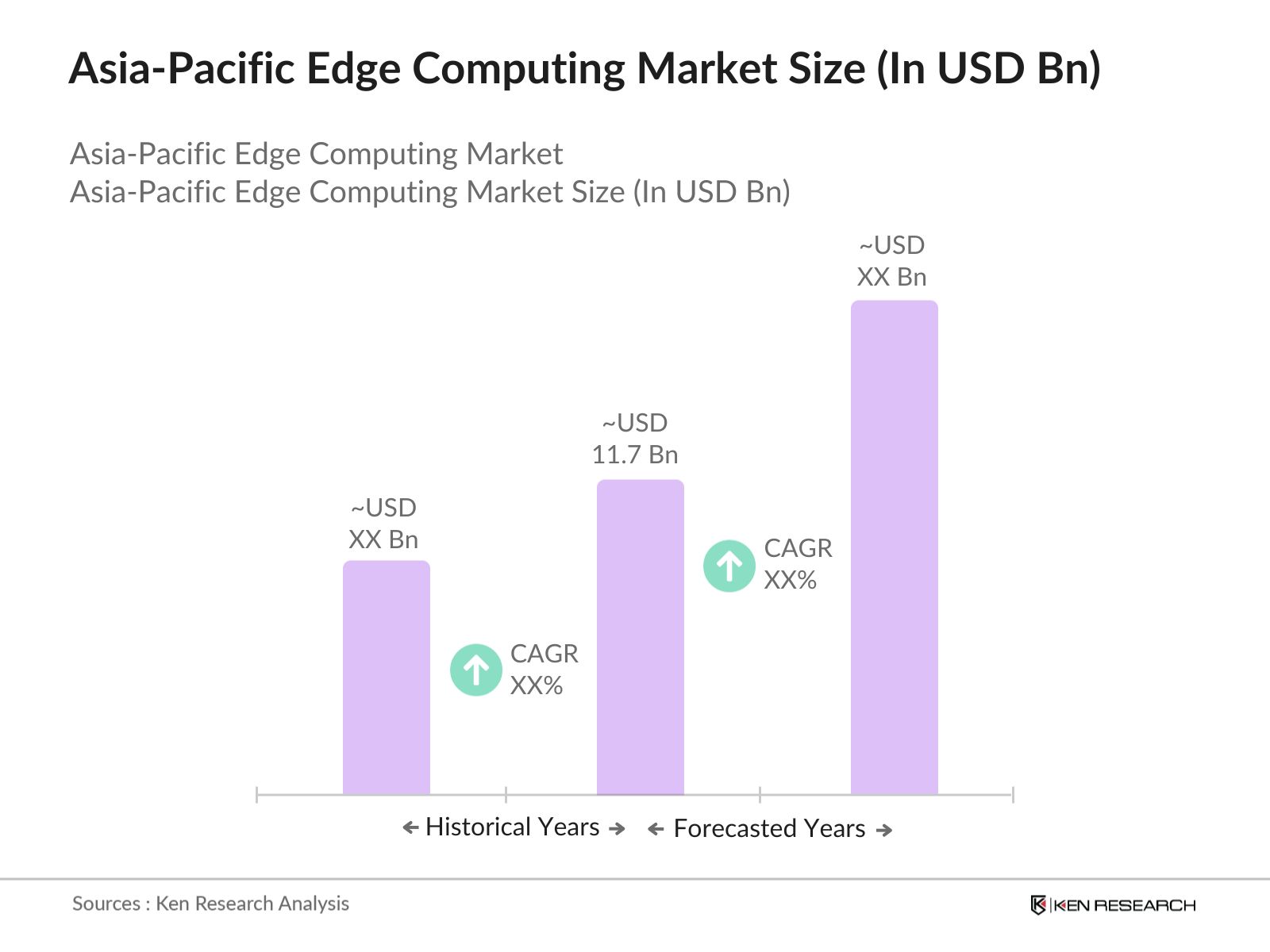

- The Asia-Pacific edge computing market is valued at USD 11.7 billion, based on a comprehensive analysis of the past five years. The market is driven by rapid advancements in 5G infrastructure, enabling faster and more efficient data processing at the network's edge. Growing demand for low-latency applications, such as real-time analytics and IoT integration, is further boosting market expansion. The regions extensive adoption of edge technology in industries like manufacturing, healthcare, and telecommunications contributes to its robust market size.

- China, Japan, and South Korea dominate the Asia-Pacific edge computing market due to their advanced technological infrastructure and substantial investments in 5G deployment and AI integration. These countries have well-established industrial sectors and high adoption rates of smart technologies, driving the growth of edge computing. Additionally, government initiatives supporting digital transformation, especially in manufacturing and smart cities, are propelling these countries to the forefront of the market.

- The rise of edge computing has prompted governments across Asia-Pacific to enhance cybersecurity frameworks. In 2024, the Association of Southeast Asian Nations (ASEAN) adopted a Regional Cybersecurity Cooperation Strategy to improve cybersecurity capabilities across member states. This framework focuses on building cross-border collaborations and standards for securing edge networks, ensuring that decentralized systems remain resilient against potential cyberattacks.

Asia-Pacific Edge Computing Market Segmentation

The Asia-Pacific Edge Computing Market is segmented by technology, MRO type, end-user industry, product type, and geographical region.

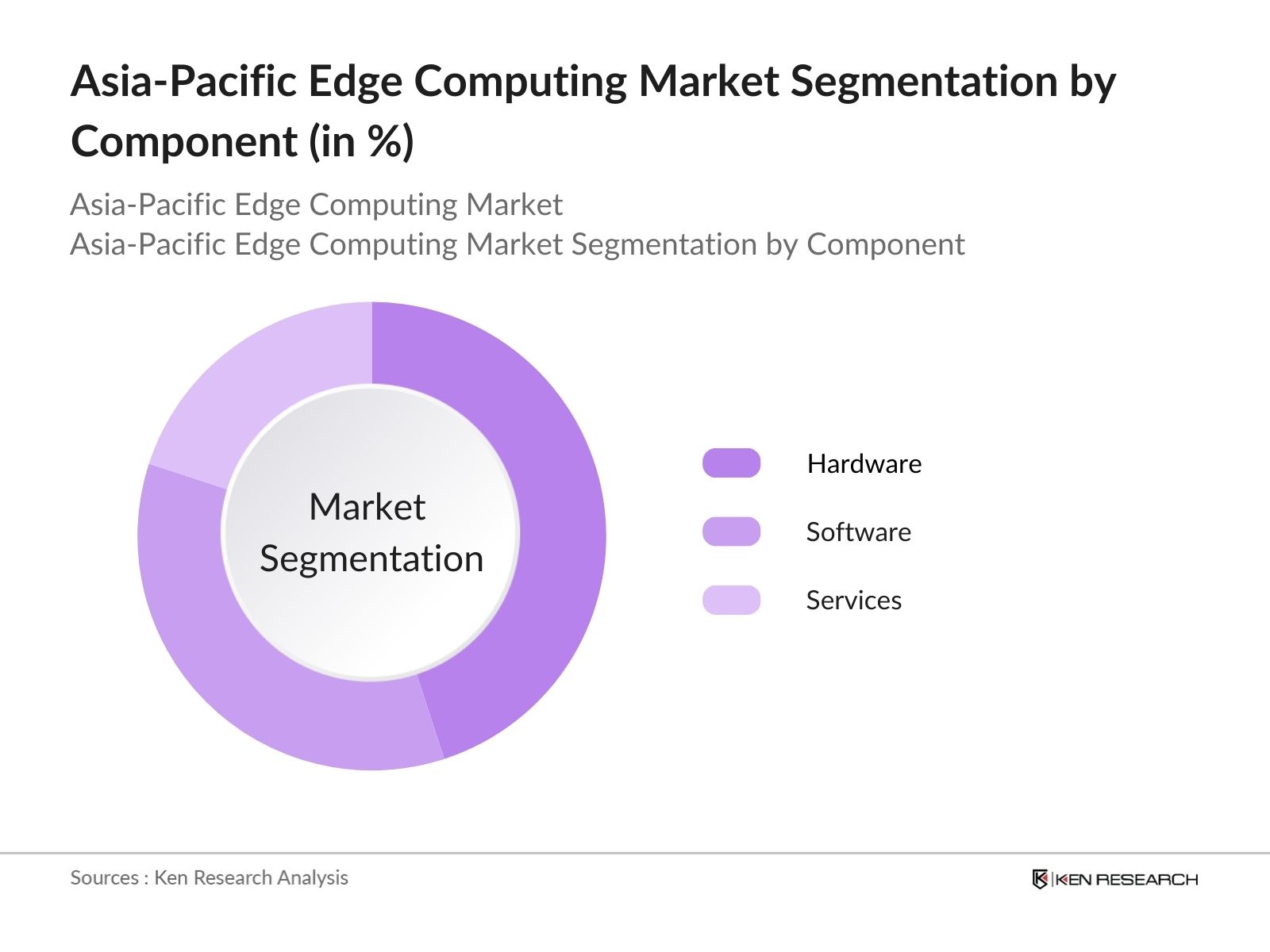

By Component: The Asia-Pacific edge computing market is segmented by component into hardware, software, and services. Hardware, including edge devices, sensors, and networking equipment, holds the dominant market share due to the necessity of physical infrastructure for edge computing. The expansion of IoT and smart applications has led to an increased demand for edge devices capable of handling real-time data processing. Companies are continually upgrading their hardware solutions to meet the growing demand for faster and more reliable edge infrastructure.

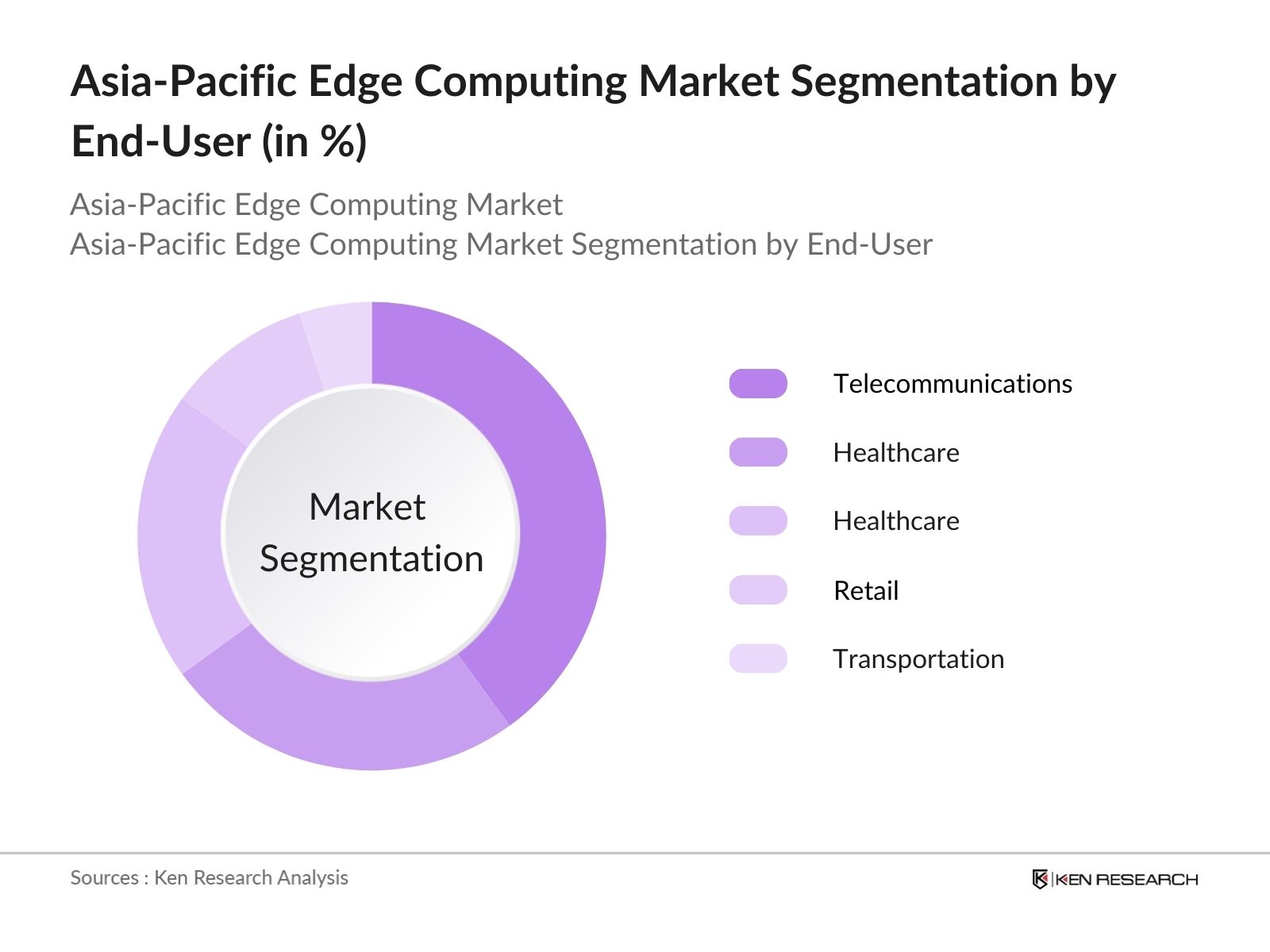

By End-User Industry: The market is segmented by end-user industries into telecommunications, healthcare, manufacturing, retail, and transportation & logistics. Telecommunications holds the largest share in this segmentation due to the ongoing 5G rollouts across Asia-Pacific, which require edge computing for efficient data management and low-latency services. Telecom operators are leveraging edge computing to support smart city projects, mobile edge computing (MEC), and advanced network services.

Asia-Pacific Edge Computing Market Competitive Landscape

The Asia-Pacific edge computing market is dominated by a few global technology giants and regional leaders. Companies like Amazon Web Services (AWS), Google Cloud, and Huawei have established their presence due to their vast resources, strong R&D capabilities, and strategic partnerships with regional telecommunications companies. These firms are leading the market with advanced edge computing solutions tailored to various industries.

|

Company |

Established |

Headquarters |

Revenue |

Edge Devices |

Data Centers |

R&D Investment |

Cloud Integration |

|

Amazon Web Services (AWS) |

2006 |

Seattle, USA |

- |

- |

- |

- |

- |

|

Google Cloud |

2008 |

Mountain View, USA |

- |

- |

- |

- |

- |

|

Huawei Technologies |

1987 |

Shenzhen, China |

- |

- |

- |

- |

- |

|

Cisco Systems |

1984 |

San Jose, USA |

- |

- |

- |

- |

- |

|

Dell Technologies |

1984 |

Round Rock, USA |

- |

- |

- |

- |

- |

Asia-Pacific Edge Computing Market Analysis

Asia-Pacific Edge Computing Market Growth Drivers:

- Increasing IoT Adoption: The Asia-Pacific region has witnessed the IoT expansion, driven by industrial automation and smart city projects. In 2024, the World Bank estimated that the number of IoT devices surpassed 6 billion in Asia-Pacific. With countries like China and Japan leading industrial IoT (IIoT) development, the manufacturing sector has increasingly relied on edge computing to handle the data influx. IoT applications in agriculture, healthcare, and logistics are expected to accelerate this trend further, enhancing data processing efficiency through edge computing.

- Demand for Low-Latency Computing: Edge computing addresses the need for real-time data processing across industries that demand minimal latency, such as autonomous vehicles and online gaming. By 2024, countries in Asia-Pacific, including South Korea, Japan, and Singapore, had invested heavily in low-latency technologies, with over $15 billion allocated for digital infrastructure improvement. Edge computing enables reduced latency for these critical applications by bringing data processing closer to users and devices, ensuring faster decision-making and real-time interactions.

- Rise in Smart City Initiatives: The push for smart city development in Asia-Pacific has boosted the demand for edge computing. Governments in China, India, and Southeast Asia have invested more than $50 billion in smart city projects aimed at enhancing urban efficiency, reducing energy consumption, and improving citizen services. These projects generate enormous amounts of data that require localized, fast, and secure processing, which edge computing solutions provide. For instance, edge computing powers smart traffic systems, enabling real-time traffic management and reducing congestion in megacities.

Asia-Pacific Edge Computing Market Challenges:

- Data Privacy and Security Concerns: The decentralized nature of edge computing raises serious data privacy and security challenges. In 2024, cybersecurity attacks cost the Asia-Pacific region an estimated $300 billion, with a major portion of these attacks targeting decentralized networks. Governments across the region have enforced stringent data protection regulations, such as India's Personal Data Protection Bill and Singapore's Cybersecurity Act, to mitigate these risks. However, ensuring data privacy in edge networks remains complex, requiring ongoing investment in cybersecurity frameworks.

- High Deployment Costs: Edge computing infrastructure, particularly at scale, can be expensive to deploy and maintain. In 2024, countries in the Asia-Pacific region, including Japan, Australia, and South Korea, reported edge computing deployment costs exceeding $500 million. This capital investment, especially in developing economies, has created barriers to widespread adoption. Moreover, edge deployments in remote areas demand robust connectivity solutions, further increasing costs for infrastructure deployment and maintenance.

Asia-Pacific Edge Computing Future Market Outlook

Over the next five years, the Asia-Pacific edge computing market is expected to exhibit growth, driven by advancements in 5G technology, the proliferation of IoT devices, and increasing demand for low-latency processing in sectors such as manufacturing and healthcare. The rise of autonomous systems, including vehicles and industrial robots, will further necessitate the adoption of edge computing. Additionally, government-backed smart city initiatives will continue to fuel the demand for edge solutions to manage real-time data processing at the edge of networks.

Asia-Pacific Edge Computing Market Opportunities:

- Integration with AI and Machine Learning: Edge computing's integration with AI and machine learning (ML) has provided a competitive advantage to businesses in various sectors like manufacturing, healthcare, and retail. As of 2024, AI solutions at the edge are projected to handle 20% of total industrial data in smart factories across Asia-Pacific, particularly in China and South Korea. This allows businesses to run advanced algorithms close to the source of data generation, reducing reliance on cloud infrastructure and enabling real-time analytics.

- Growth of Edge Data Centers: Edge data centers are expected to play a critical role in processing the surge of localized data generated by IoT devices, autonomous vehicles, and 5G networks. As of 2024, Asia-Pacific housed over 10,000 edge data centers, with countries like Singapore and South Korea emerging as leaders. These data centers offer localized data storage and processing capabilities, reducing latency and improving operational efficiency. The expansion of edge data centers aligns with growing demands for real-time data analytics in industries such as retail and telecommunications.

Scope of the Report

|

By Component |

Hardware Software Services |

|

By Deployment Model |

On-Premise Cloud-Based Hybrid |

|

By End-User Industry |

Telecommunications Healthcare Manufacturing Retail Transportation & Logistics |

|

By Application |

Industrial Automation Real-Time Data Analytics Autonomous Vehicles Smart Grid Management |

|

By Region |

China Japan South Korea Australia India |

Products

Key Target Audience Organizations and Entities Who Can Benefit by Subscribing This Report:

Government and Regulatory Bodies

Banks and Financial Institutes

Investors and Venture Capitalists

Edge Device Manufacturers

Telecommunication Providers

Data Center Operators

Cloud Service Providers

AI/ML Software Providers

Edge Data Center Service Providers

Companies

Players Mentioned in the Report:

Amazon Web Services (AWS)

Google Cloud

Huawei Technologies Co., Ltd.

Cisco Systems

Dell Technologies

HPE (Hewlett Packard Enterprise)

Microsoft Azure

Intel Corporation

Nokia Corporation

Equinix, Inc.

EdgeConneX

Schneider Electric

Vapor IO

ADLINK Technology Inc.

Lenovo Group Ltd.

Table of Contents

1. Asia-Pacific Edge Computing Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Asia-Pacific Edge Computing Market Size (in USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Asia-Pacific Edge Computing Market Analysis

3.1. Growth Drivers

3.1.1. Increasing IoT Adoption

3.1.2. Demand for Low-Latency Computing

3.1.3. Rise in Smart City Initiatives

3.1.4. Expansion of 5G Infrastructure

3.2. Market Challenges

3.2.1. Data Privacy and Security Concerns

3.2.2. High Deployment Costs

3.2.3. Interoperability Issues

3.3. Opportunities

3.3.1. Integration with AI and Machine Learning

3.3.2. Growth of Edge Data Centers

3.3.3. Edge-As-A-Service Models

3.4. Trends

3.4.1. Increasing Use of Micro Data Centers

3.4.2. Hybrid Cloud and Edge Solutions

3.4.3. AI at the Edge

3.5. Government Regulations

3.5.1. Data Sovereignty Laws

3.5.2. Regional Cybersecurity Frameworks

3.5.3. 5G Spectrum Allocations

3.6. SWOT Analysis

3.7. Stake Ecosystem

3.8. Porters Five Forces

3.9. Competition Ecosystem

4. Asia-Pacific Edge Computing Market Segmentation

4.1. By Component (In Value %)

4.1.1. Hardware (Edge Devices, Sensors, Networking Equipment)

4.1.2. Software (Edge Platforms, Cloud Integration Software)

4.1.3. Services (Edge Managed Services, System Integration)

4.2. By Deployment Model (In Value %)

4.2.1. On-Premise Edge Computing

4.2.2. Cloud-Based Edge Computing

4.2.3. Hybrid Edge

4.3. By End-User Industry (In Value %)

4.3.1. Telecommunications

4.3.2. Healthcare

4.3.3. Manufacturing

4.3.4. Retail

4.3.5. Transportation & Logistics

4.4. By Application (In Value %)

4.4.1. Industrial Automation

4.4.2. Real-Time Data Analytics

4.4.3. Autonomous Vehicles

4.4.4. Smart Grid Management

4.5. By Region (In Value %)

4.5.1. China

4.5.2. Japan

4.5.3. South Korea

4.5.4. Australia

4.5.5. India

4.5.6. Rest of APAC

5. Asia-Pacific Edge Computing Market Competitive Analysis

5.1 Detailed Profiles of Major Companies

5.1.1. Amazon Web Services

5.1.2. Microsoft Azure

5.1.3. Google Cloud

5.1.4. Huawei Technologies Co., Ltd.

5.1.5. Cisco Systems, Inc.

5.1.6. IBM Corporation

5.1.7. Dell Technologies

5.1.8. HPE (Hewlett Packard Enterprise)

5.1.9. Intel Corporation

5.1.10. Nokia Corporation

5.1.11. EdgeConneX

5.1.12. Equinix, Inc.

5.1.13. Vapor IO

5.1.14. Schneider Electric

5.1.15. ADLINK Technology Inc.

5.2 Cross Comparison Parameters (Revenue, Cloud Integration Capabilities, Geographical Reach, Number of Data Centers, AI/ML Integration, Security Solutions, IoT Partnerships, Edge Data Center Deployment)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Private Equity Investments

6. Asia-Pacific Edge Computing Market Regulatory Framework

6.1. Data Compliance Requirements

6.2. 5G Network Regulations

6.3. Edge Infrastructure Standards

7. Asia-Pacific Edge Computing Future Market Size (in USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Asia-Pacific Edge Computing Future Market Segmentation

8.1. By Component (In Value %)

8.2. By Deployment Model (In Value %)

8.3. By End-User Industry (In Value %)

8.4. By Application (In Value %)

8.5. By Region (In Value %)

9. Asia-Pacific Edge Computing Market Analysts Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Market Penetration Strategies

9.4. Innovation White Space Opportunities

Disclaimer Contact UsResearch Methodology

Step 1: Identification of Key Variables

This phase involved mapping out the ecosystem of stakeholders in the Asia-Pacific edge computing market. Desk research was conducted, using both secondary and proprietary databases, to pinpoint critical variables influencing market growth, such as 5G deployment and IoT adoption.

Step 2: Market Analysis and Construction

Historical data was collected and analyzed, covering penetration of edge devices, the relationship between cloud and edge providers, and sector-specific applications. This was followed by calculating revenue and market growth patterns for different end-user industries.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses were formulated and validated through interviews with industry experts via computer-assisted telephone interviews (CATI). Feedback from edge computing professionals provided deeper insights into operational challenges and growth drivers.

Step 4: Research Synthesis and Final Output

In the final phase, direct consultation with major edge computing solution providers and manufacturers confirmed data accuracy. This process ensured the report presents a comprehensive view of the market, validated by both top-down and bottom-up approaches.

Frequently Asked Questions

01. How big is the Asia-Pacific Edge Computing Market?

The Asia-Pacific edge computing market is valued at USD 11.7 billion, driven by the expansion of 5G infrastructure, rising IoT adoption, and demand for real-time data processing.

02. What are the challenges in the Asia-Pacific Edge Computing Market?

Key challenges of the Asia-Pacific edge computing market include data privacy concerns, high deployment costs, and interoperability issues between different systems and devices. Additionally, the complexity of managing decentralized networks poses technical barriers.

03. Who are the major players in the Asia-Pacific Edge Computing Market?

Asia-Pacific edge computing market players include Amazon Web Services (AWS), Google Cloud, Huawei Technologies, Cisco Systems, and Dell Technologies. These companies dominate due to their strong infrastructure, innovation capabilities, and strategic partnerships.

04. What are the growth drivers of the Asia-Pacific Edge Computing Market?

Asia-Pacific edge computing market growth drivers include the expansion of 5G networks, increasing demand for low-latency processing, and the rise of smart cities across the region. Additionally, advancements in AI/ML at the edge and edge data centers are further boosting the market growth.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.