Asia-Pacific Electric Vehicle Battery Market Outlook to 2030

Region:Asia

Author(s):Naman Rohilla

Product Code:KROD4249

December 2024

86

About the Report

Asia-Pacific Electric Vehicle Battery Market Overview

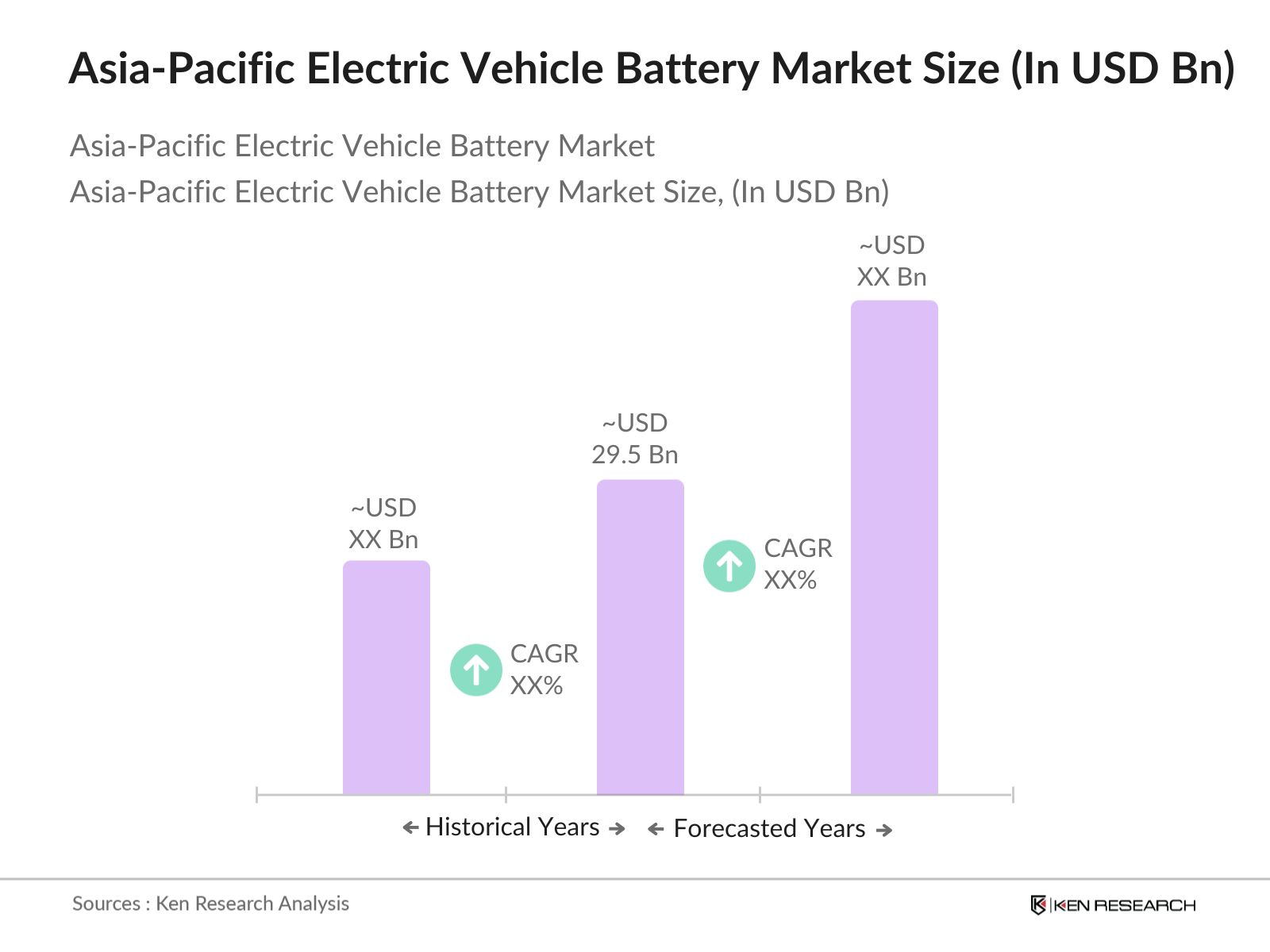

- The Asia-Pacific Electric Vehicle (EV) Battery Market is valued at USD 29.5 billion, based on a five-year historical analysis. The market has grown substantially, driven by the increasing adoption of electric vehicles across the region. The shift towards clean energy solutions, investments by governments in EV infrastructure, and the rapid advancements in battery technology, particularly in lithium-ion and solid-state batteries, are the primary drivers of market expansion. The increasing focus on sustainability and emissions reduction, alongside advancements in battery capacity and energy density, further contribute to this growth.

- Dominant countries in the Asia-Pacific region include China, Japan, and South Korea. These countries dominate due to their well-established automotive industries, advanced battery manufacturing capabilities, and government support for EV adoption. China, in particular, leads the market because of its large domestic market for EVs, coupled with aggressive government policies aimed at reducing carbon emissions. Japan and South Korea are renowned for their strong focus on research and development in battery technologies, making them global leaders in battery innovation.

- Governments in the Asia-Pacific region are indeed implementing stringent mandates for EV battery disposal and recycling. In China, the Ministry of Ecology and Environment has set regulations requiring manufacturers to recycle 80% of end-of-life batteries by 2023. Additionally, the country aims for 45% of all batteries to be recycled by the end of 2023 and 70% by 20302. Meanwhile, in India, draft battery waste management rules mandate that producers must collect and recycle 70% of battery waste by 202512. These initiatives reflect a growing commitment to sustainable practices in the EV sector across the region.

Asia-Pacific Electric Vehicle Battery Market Segmentation

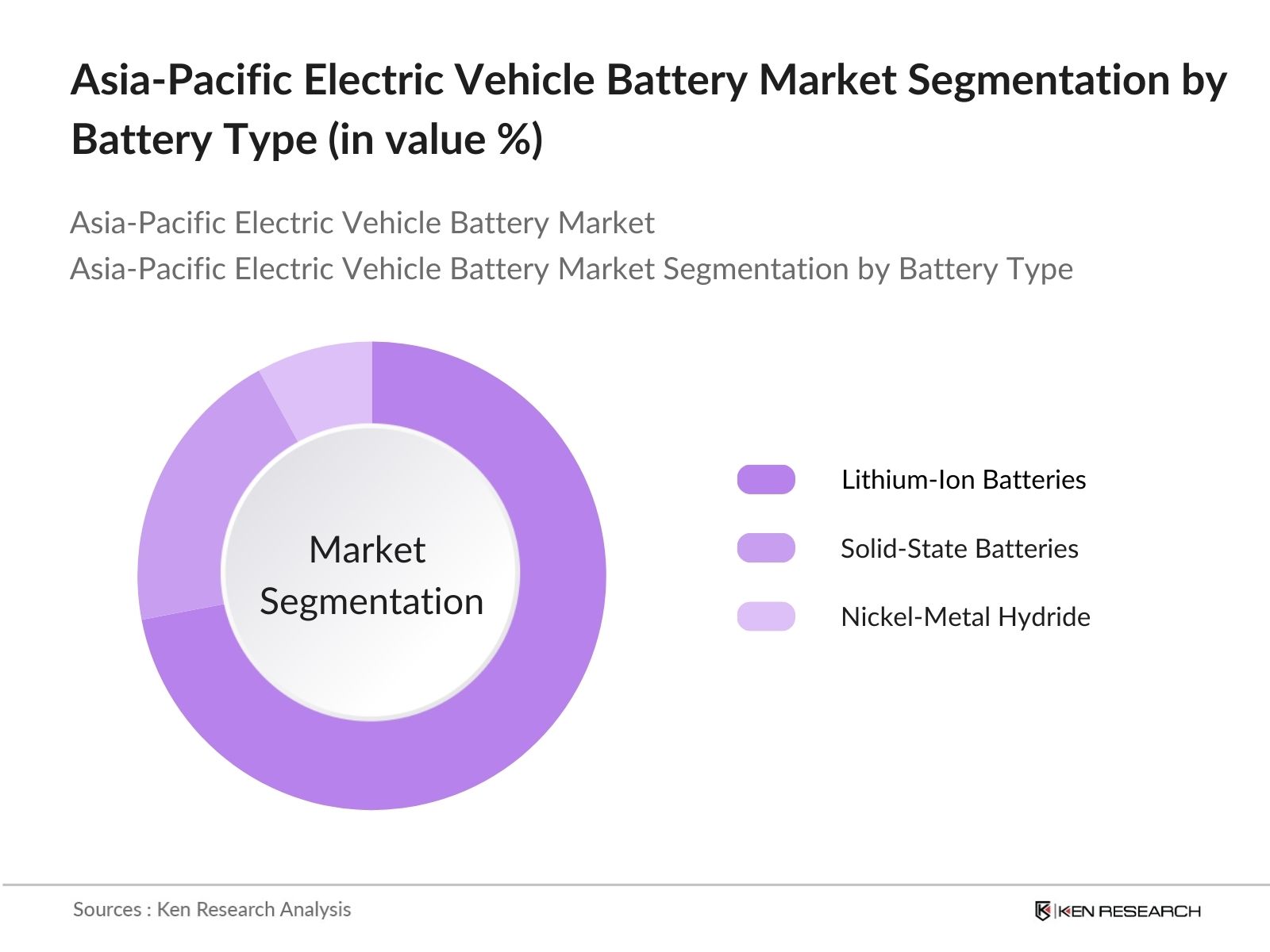

- By Battery Type: The Asia-Pacific Electric Vehicle Battery market is segmented by battery type into lithium-ion batteries, solid-state batteries, and nickel-metal hydride batteries. Recently, lithium-ion batteries hold the dominant market share in this segment due to their widespread application in electric vehicles and superior energy density. Major EV manufacturers rely heavily on lithium-ion batteries for their extended range, fast charging capabilities, and declining costs, which have resulted in their increased adoption.

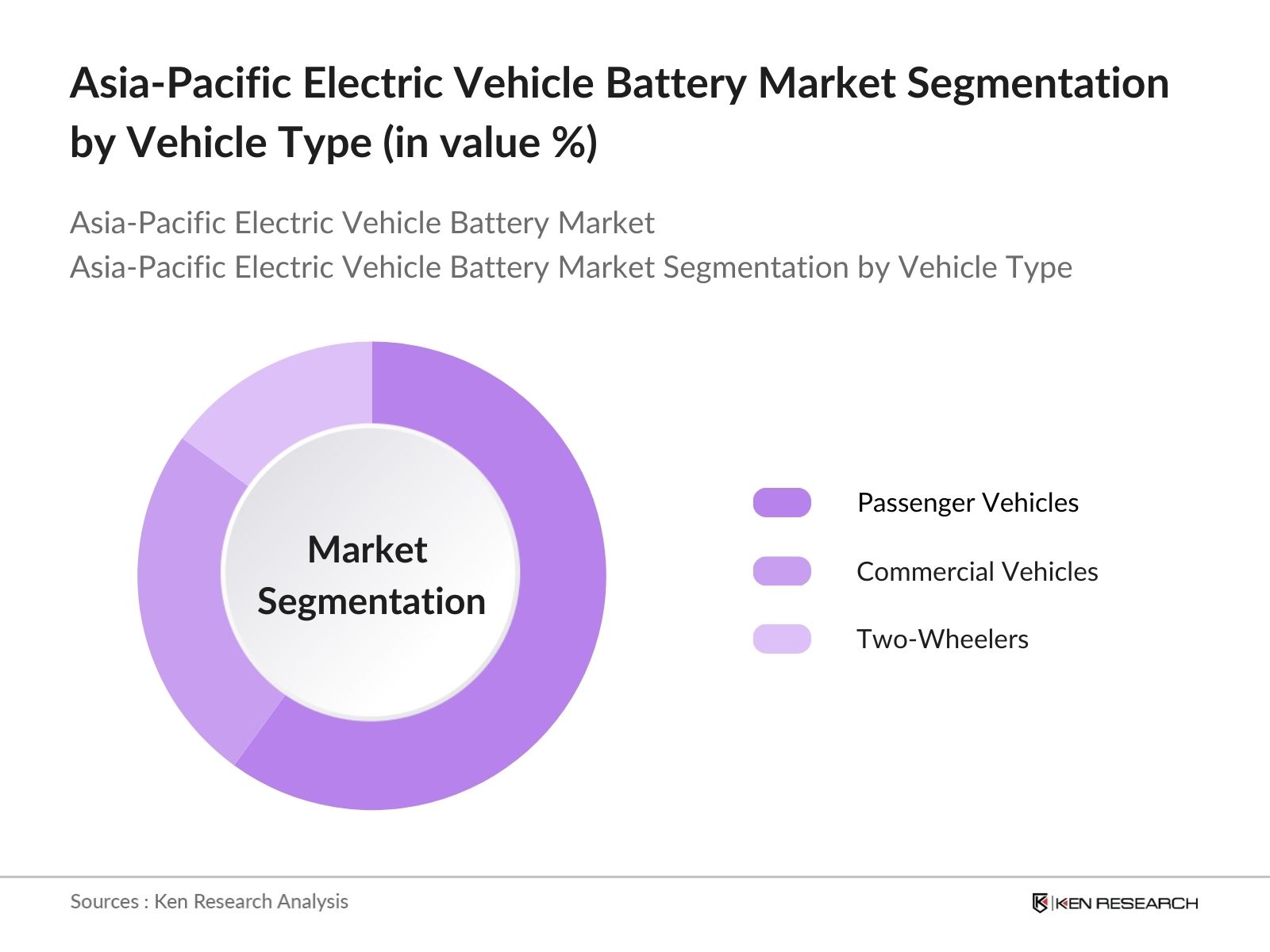

- By Vehicle Type: The Asia-Pacific Electric Vehicle Battery market is segmented by vehicle type into passenger vehicles, commercial vehicles, and two-wheelers. Passenger vehicles dominate the market under this segment, driven by the high demand for electric cars in countries like China and Japan. Government subsidies, stringent emission regulations, and growing consumer awareness about eco-friendly transportation solutions have further fueled the adoption of electric passenger vehicles, making them the most substantial contributors to battery demand.

Asia-Pacific Electric Vehicle Battery Market Competitive Landscape

The Asia-Pacific Electric Vehicle Battery market is dominated by key global and regional players, highlighting the consolidation in the industry. Companies like CATL, LG Energy Solution, and Panasonic lead due to their extensive manufacturing capacities, strong relationships with automakers, and investments in R&D. Their dominance emphasizes the strategic importance of vertical integration and long-term partnerships with automakers.

|

Company |

Established |

Headquarters |

Battery Capacity |

Revenue (2023) |

R&D Investment |

Global Market Reach |

Sustainability Initiatives |

Battery Technology Focus |

|

CATL |

2011 |

Ningde, China |

- |

- |

- |

- |

- |

- |

|

LG Energy Solution |

2020 |

Seoul, South Korea |

- |

- |

- |

- |

- |

- |

|

Panasonic Corporation |

1918 |

Osaka, Japan |

- |

- |

- |

- |

- |

- |

|

BYD Company |

1995 |

Shenzhen, China |

- |

- |

- |

- |

- |

- |

|

Samsung SDI |

1970 |

Seoul, South Korea |

- |

- |

- |

- |

- |

- |

Asia-Pacific Electric Vehicle Battery Market Analysis

Asia-Pacific Electric Vehicle Battery Market Growth Drivers

- Increasing Focus on Clean Energy: Asia-Pacific nations are prioritizing clean energy to reduce carbon emissions. Japan aims for carbon neutrality by 2050, with the Ministry of Economy, Trade, and Industry (METI) reporting an investment of over USD 19 billion in clean energy projects in 2023 to enhance the share of renewables. South Korea's Green New Deal allocated USD 61 billion for green energy and EV infrastructure development, funding advancements in EV batteries.

- Rising Investments in Battery Technology: There is a strong focus on battery technology innovation, particularly solid-state batteries and fast-charging capabilities. China allocated over USD 12 billion for battery R&D in 2023, targeting improvements in energy density and fast-charging solutions, according to the National Energy Administration (NEA). Japan's METI is also investing over USD 2.2 billion in solid-state battery technologies, bolstering the supply chain for electric vehicle batteries.

- Collaboration Between Automakers and Battery Manufacturers: Collaborations between automakers and battery manufacturers are enhancing production capacity in Asia-Pacific. For instance, BYD and Toyota have strengthened their joint venture, BYD-Toyota EV Technology Co., investing over USD 1.5 billion in battery development in 2023. Similarly, Hyundai partnered with LG Energy Solutions, injecting USD 1 billion into joint battery production facilities in South Korea to boost domestic manufacturing and reduce reliance on imports.

Asia-Pacific Electric Vehicle Battery Market Challenges

- High Battery Costs: Although battery prices have been declining, they remain a major cost barrier for EV adoption in Asia-Pacific. According to a 2023 report by the Asian Development Bank (ADB), battery production costs in the region still hover around USD 130 per kilowatt-hour (kWh), with raw material procurement accounting for nearly 50% of these costs. This hinders the mass affordability of EVs, especially in developing markets like India and Indonesia.

- Raw Material Sourcing and Supply Chain Bottlenecks: The Asia-Pacific EV battery market faces challenges in sourcing key raw materials like lithium and cobalt. The Democratic Republic of Congo (DRC) supplies 60% of the world's cobalt, leading to heavy reliance on imports. China controls 80% of global lithium refining, making supply chains vulnerable to geopolitical tensions. According to the International Energy Agency (IEA), over 70% of the global lithium supply comes from Australia, but processing bottlenecks are prevalent in 2023.

Asia-Pacific Electric Vehicle Battery Market Future Outlook

Over the next five years, the Asia-Pacific Electric Vehicle Battery market is expected to experience robust growth, fueled by continuous technological advancements, supportive government policies, and the rising demand for electric vehicles. Countries in the region, particularly China and Japan, are likely to maintain their dominant positions, driven by innovation in battery technology and expanding EV infrastructure. The market is also expected to benefit from the increasing focus on sustainable battery production and recycling technologies, alongside the development of new battery chemistries like solid-state batteries.

Asia-Pacific Electric Vehicle Battery Market Opportunities

- Expansion into Emerging Economies: Emerging economies in the ASEAN region, such as Vietnam, Thailand, and Indonesia, present untapped growth opportunities for the EV battery market. According to the World Bank, Vietnam's GDP growth reached 8.02% in 2022, driving demand for cleaner energy alternatives. Indonesia aims to have 2.5 million EVs on the road by 2030, supported by USD 1.1 billion investments in battery production. These expanding economies are expected to contribute to the region's EV battery market growth.

- Growth in Commercial Electric Fleets: Commercial EV fleets are rapidly expanding in Asia-Pacific, especially in public transport and last-mile delivery. The Indian governments target to electrify 40% of public buses by 2030 led to a 500 million USD investment in EV bus fleets in 2023, according to the Ministry of Heavy Industries. Similarly, Chinas last-mile delivery sector has adopted 400,000 electric vans by 2023, driven by state-sponsored EV initiatives.

Scope of the Report

|

By Battery Type |

Lithium-Ion (NMC, NCA, LFP) Solid-State Batteries Nickel-Metal Hydride Batteries |

|

By Vehicle Type |

Passenger Vehicles Commercial Vehicles Two-Wheelers |

|

By Battery Capacity |

Below 50 kWh 50-100 kWh Above 100 kWh |

|

By Application |

BEVs (Battery Electric Vehicles) PHEVs (Plug-in Hybrid Electric Vehicles) HEVs (Hybrid Electric Vehicles) |

|

By Region |

China Japan South Korea India Rest of Asia-Pacific |

Products

Key Target Audience

Electric Vehicle Manufacturers

Battery Manufacturers

Automotive OEMs

Investments and Venture Capitalist Firms

Banks and Financial Institutions

Government and Regulatory Bodies (Ministry of Energy, Department of Transportation)

Environmental Agencies (Asia-Pacific Environment Program)

Renewable Energy Developers

Battery Recycling Companies

Companies

Asia-Pacific Electric Vehicle Battery Market Major Players

CATL (Contemporary Amperex Technology Co. Ltd.)

LG Energy Solution

Panasonic Corporation

BYD Company

Samsung SDI

SVolt Energy Technology

CALB (China Aviation Lithium Battery)

Envision AESC

Farasis Energy

Lithium Werks

GS Yuasa Corporation

Mitsubishi Electric Corporation

PTT Group

Tata Chemicals

SK Innovation

Table of Contents

1. Asia-Pacific Electric Vehicle Battery Market Overview

1.1. Definition and Scope

1.2. Market Taxonomy

1.3. Market Growth Rate

1.4. Market Segmentation Overview

2. Asia-Pacific Electric Vehicle Battery Market Size (In USD Bn)

2.1. Historical Market Size

2.2. Year-On-Year Growth Analysis

2.3. Key Market Developments and Milestones

3. Asia-Pacific Electric Vehicle Battery Market Analysis

3.1. Growth Drivers

3.1.1. Government Incentives for EV Adoption

3.1.2. Increasing Focus on Clean Energy

3.1.3. Rising Investments in Battery Technology (Solid-State Batteries, Fast Charging Capabilities)

3.1.4. Collaboration Between Automakers and Battery Manufacturers

3.2. Market Challenges

3.2.1. High Battery Costs

3.2.2. Raw Material Sourcing and Supply Chain Bottlenecks (Lithium, Cobalt)

3.2.3. Limited Charging Infrastructure

3.2.4. Safety and Thermal Management Issues

3.3. Opportunities

3.3.1. Expansion into Emerging Economies (ASEAN Markets)

3.3.2. Technological Advancements in Battery Recycling

3.3.3. Growth in Commercial Electric Fleets (Public Transport, Last-Mile Delivery)

3.4. Trends

3.4.1. Increased Focus on Battery Energy Density Improvement

3.4.2. Development of Second-Life Batteries for Renewable Energy Storage

3.4.3. Growing Use of AI for Battery Performance Optimization

3.5. Government Regulation

3.5.1. Regional Mandates on EV Battery Disposal and Recycling

3.5.2. Subsidies for Battery Manufacturing

3.5.3. Import Duties and Tariffs on Battery Components

3.6. SWOT Analysis

3.7. Stake Ecosystem

3.8. Porters Five Forces Analysis

3.9. Competition Ecosystem

4. Asia-Pacific Electric Vehicle Battery Market Segmentation

4.1. By Battery Type (In Value %)

4.1.1. Lithium-Ion Batteries (NMC, NCA, LFP)

4.1.2. Solid-State Batteries

4.1.3. Nickel-Metal Hydride Batteries

4.2. By Vehicle Type (In Value %)

4.2.1. Passenger Vehicles

4.2.2. Commercial Vehicles

4.2.3. Two-Wheelers

4.3. By Battery Capacity (In Value %)

4.3.1. Below 50 kWh

4.3.2. 50-100 kWh

4.3.3. Above 100 kWh

4.4. By Application (In Value %)

4.4.1. BEVs (Battery Electric Vehicles)

4.4.2. PHEVs (Plug-in Hybrid Electric Vehicles)

4.4.3. HEVs (Hybrid Electric Vehicles)

4.5. By Region (In Value %)

4.5.1. China

4.5.2. Japan

4.5.3. South Korea

4.5.4. India

4.5.5. Rest of Asia-Pacific

5. Asia-Pacific Electric Vehicle Battery Market Competitive Analysis

5.1. Detailed Profiles of Major Companies

5.1.1. CATL (Contemporary Amperex Technology Co. Ltd.)

5.1.2. LG Energy Solution

5.1.3. Panasonic Corporation

5.1.4. BYD Company

5.1.5. Samsung SDI

5.1.6. SK Innovation

5.1.7. Envision AESC

5.1.8. SVolt Energy Technology

5.1.9. CALB (China Aviation Lithium Battery)

5.1.10. Tata Chemicals

5.1.11. PTT Group

5.1.12. Mitsubishi Electric Corporation

5.1.13. GS Yuasa Corporation

5.1.14. Farasis Energy

5.1.15. Lithium Werks

5.2. Cross Comparison Parameters (Battery Production Capacity, Revenue, Global Market Reach, R&D Investments, Sustainability Initiatives, Strategic Alliances, Manufacturing Footprint, Battery Chemistry Focus)

5.3. Market Share Analysis

5.4. Strategic Initiatives

5.5. Mergers and Acquisitions

5.6. Investment Analysis

5.7. Venture Capital Funding

5.8. Government Grants

5.9. Private Equity Investments

6. Asia-Pacific Electric Vehicle Battery Market Regulatory Framework

6.1. Emission Standards and Environmental Policies

6.2. Safety and Performance Regulations for Batteries

6.3. Recycling and Disposal Norms

6.4. Certification and Standardization Processes

7. Asia-Pacific Electric Vehicle Battery Future Market Size (In USD Bn)

7.1. Future Market Size Projections

7.2. Key Factors Driving Future Market Growth

8. Asia-Pacific Electric Vehicle Battery Future Market Segmentation

8.1. By Battery Type (In Value %)

8.2. By Vehicle Type (In Value %)

8.3. By Battery Capacity (In Value %)

8.4. By Application (In Value %)

8.5. By Region (In Value %)

9. Asia-Pacific Electric Vehicle Battery Market Analysts' Recommendations

9.1. TAM/SAM/SOM Analysis

9.2. Customer Cohort Analysis

9.3. Marketing Initiatives

9.4. White Space Opportunity Analysis

Research Methodology

Step 1: Identification of Key Variables

The initial phase involves constructing an ecosystem map encompassing all major stakeholders within the Asia-Pacific Electric Vehicle Battery Market. This step is underpinned by extensive desk research, utilizing a combination of secondary and proprietary databases to gather comprehensive industry-level information. The primary objective is to identify and define the critical variables that influence market dynamics.

Step 2: Market Analysis and Construction

In this phase, historical data for the Asia-Pacific Electric Vehicle Battery Market is compiled and analyzed. This includes assessing market penetration, the ratio of battery suppliers to vehicle manufacturers, and the resultant revenue generation. An evaluation of the battery manufacturing ecosystem and supply chain will be conducted to ensure the reliability and accuracy of the revenue estimates.

Step 3: Hypothesis Validation and Expert Consultation

Market hypotheses will be developed and subsequently validated through interviews with industry experts representing various segments of the electric vehicle and battery industries. These consultations will provide valuable operational and financial insights, which will help refine and corroborate the market data.

Step 4: Research Synthesis and Final Output

The final phase involves direct engagement with multiple electric vehicle and battery manufacturers to acquire detailed insights into battery segments, production capacities, consumer preferences, and other pertinent factors. This interaction will serve to verify and complement the statistics derived from the bottom-up approach, ensuring a comprehensive, accurate, and validated analysis of the Asia-Pacific Electric Vehicle Battery market.

Frequently Asked Questions

01. How big is the Asia-Pacific Electric Vehicle Battery Market?

The Asia-Pacific Electric Vehicle Battery Market is valued at USD 29.5 billion, driven by increasing demand for electric vehicles, government incentives, and investments in battery technology and infrastructure.

02. What are the challenges in the Asia-Pacific Electric Vehicle Battery Market?

Challenges in the Asia-Pacific Electric Vehicle Battery Market include high production costs, supply chain disruptions for key materials like lithium and cobalt, and safety concerns related to battery thermal management and energy density.

03. Who are the major players in the Asia-Pacific Electric Vehicle Battery Market?

Key players in the Asia-Pacific Electric Vehicle Battery Market include CATL, LG Energy Solution, Panasonic Corporation, BYD Company, and Samsung SDI, which dominate due to their large production capacities and strong relationships with automakers.

04. What are the growth drivers of the Asia-Pacific Electric Vehicle Battery Market?

Growth in the Asia-Pacific Electric Vehicle Battery Market is driven by advancements in battery technology, government initiatives to promote EV adoption, and growing consumer preference for environmentally friendly transportation options.

Why Buy From Us?

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.