Asia Pacific Electric Vehicle (EV) Market Outlook to 2030

Region:India

Author(s):Abhinav kumar

Product Code:KROD2589

Region:India

Author(s):Abhinav kumar

Product Code:KROD2589

December 2024

100

Listen to the audio summary

The Asia Pacific EV market is highly competitive, with the presence of several established global and regional players. The competitive landscape is dominated by local giants like BYD and global manufacturers such as Tesla, Hyundai, and Nissan. These companies have invested heavily in EV technology and battery production, securing strong positions in both the passenger and commercial EV sectors.

|

Company |

Established Year |

Headquarters |

No. of EV Models |

Battery Capacity (kWh) |

R&D Investment (USD) |

EV Sales (Units) |

Partnerships |

Market Share |

Global Presence |

|

Tesla Inc. |

2003 |

Palo Alto, USA |

_ |

_ |

_ |

_ |

_ |

_ |

_ |

|

BYD Auto Co. Ltd. |

1995 |

Shenzhen, China |

_ |

_ |

_ |

_ |

_ |

_ |

_ |

|

Nissan Motor Co. Ltd. |

1933 |

Yokohama, Japan |

_ |

_ |

_ |

_ |

_ |

_ |

_ |

|

Hyundai Motor Company |

1967 |

Seoul, South Korea |

_ |

_ |

_ |

_ |

_ |

_ |

_ |

|

Tata Motors Limited |

1945 |

Mumbai, India |

_ |

_ |

_ |

_ |

_ |

_ |

_ |

High Cost of EVs: Despite government incentives, the high upfront cost of electric vehicles remains a barrier in the Asia Pacific region. In 2024, the average cost of an EV is still about 1.5 times higher than a conventional internal combustion engine vehicle. This is especially problematic in emerging markets like Vietnam and Indonesia, where disposable incomes are lower. For example, in Indonesia, the average EV price is around USD 30,000, while the per capita income hovers around USD 4,000, making EVs less affordable for the majority of the population.

Limited Charging Infrastructure: One of the most significant challenges is the lack of sufficient charging infrastructure. In 2024, India, with its ambitious EV adoption targets, has only about 2,000 public charging stations, while China leads with over 1.3 million. However, most countries in Southeast Asia, such as Vietnam, Thailand, and Indonesia, have less than 500 stations each. This lack of charging points, particularly in rural and suburban areas, limits the feasibility of EV ownership, restricting market growth in these regions.

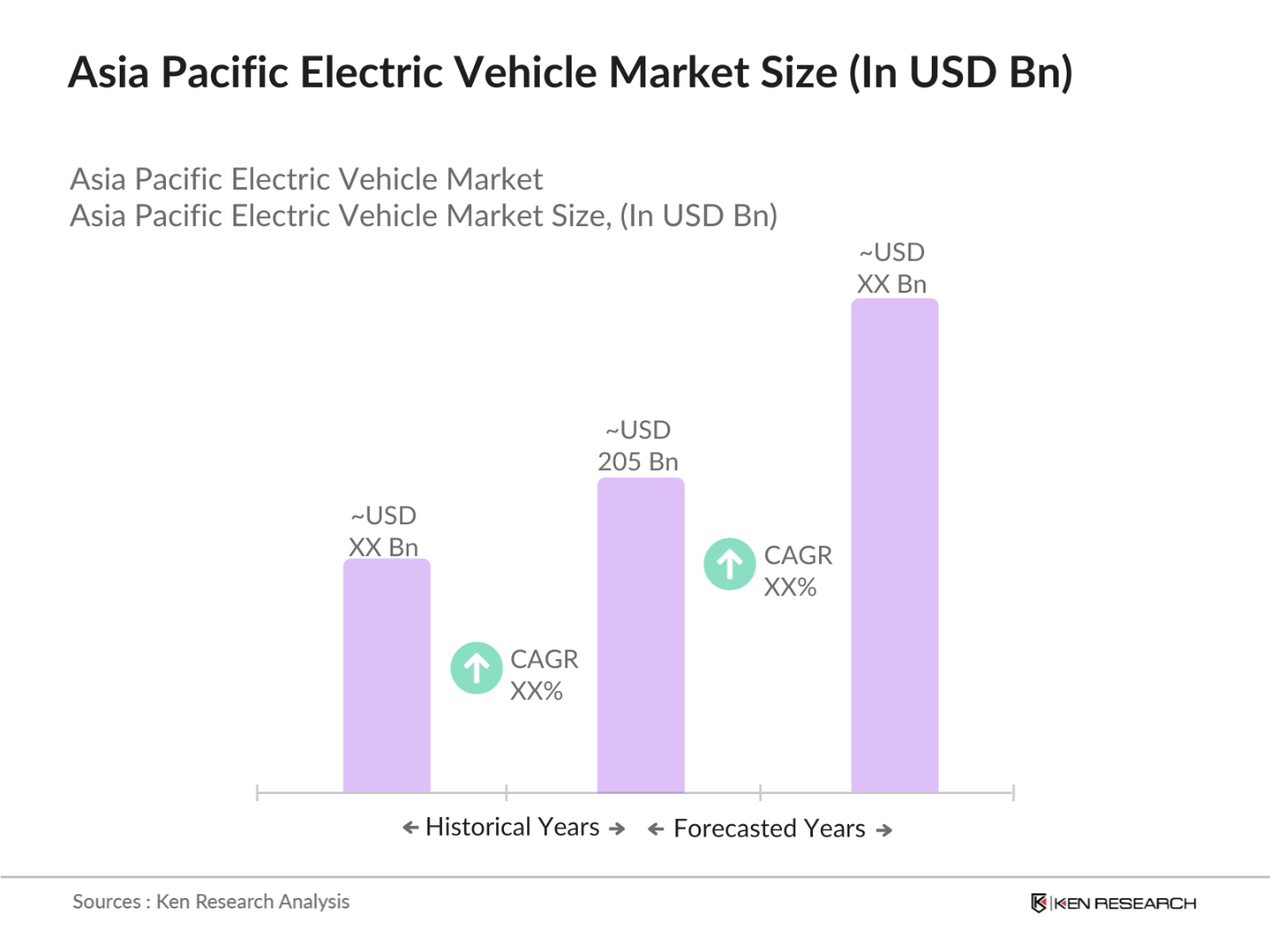

Over the next five years, the Asia Pacific EV market is expected to exhibit strong growth driven by continuous government support, advancements in EV technology, and increasing consumer demand for eco-friendly transportation solutions. The regions commitment to reducing greenhouse gas emissions and improving urban air quality is likely to boost the adoption of electric vehicles. In particular, Chinas sustained investments in battery production and charging infrastructure, combined with Indias push towards electrification in public transportation, will further fuel market expansion.

|

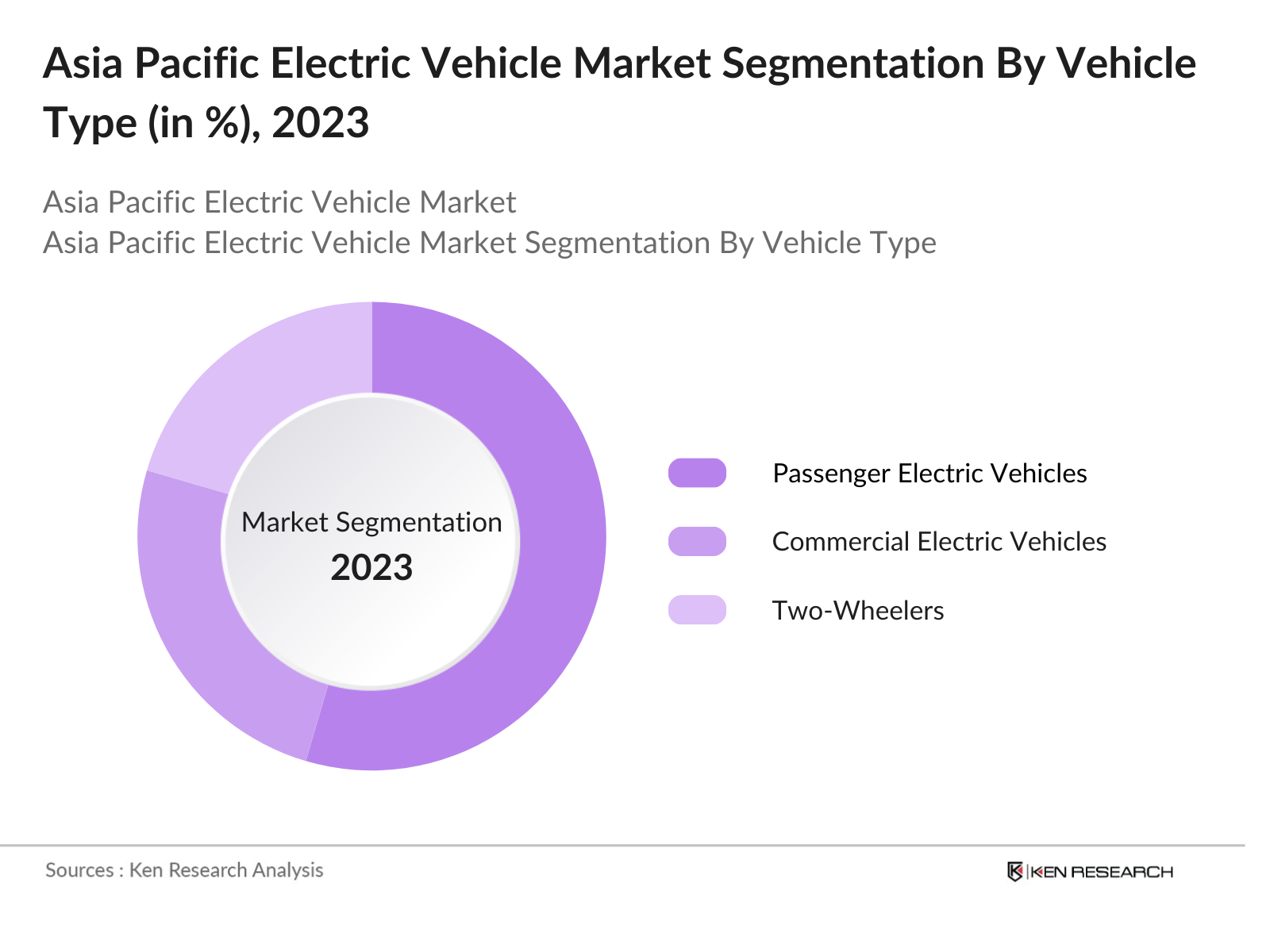

Vehicle Type |

Passenger EVs Commercial EVs Two-Wheelers E-Buses |

|

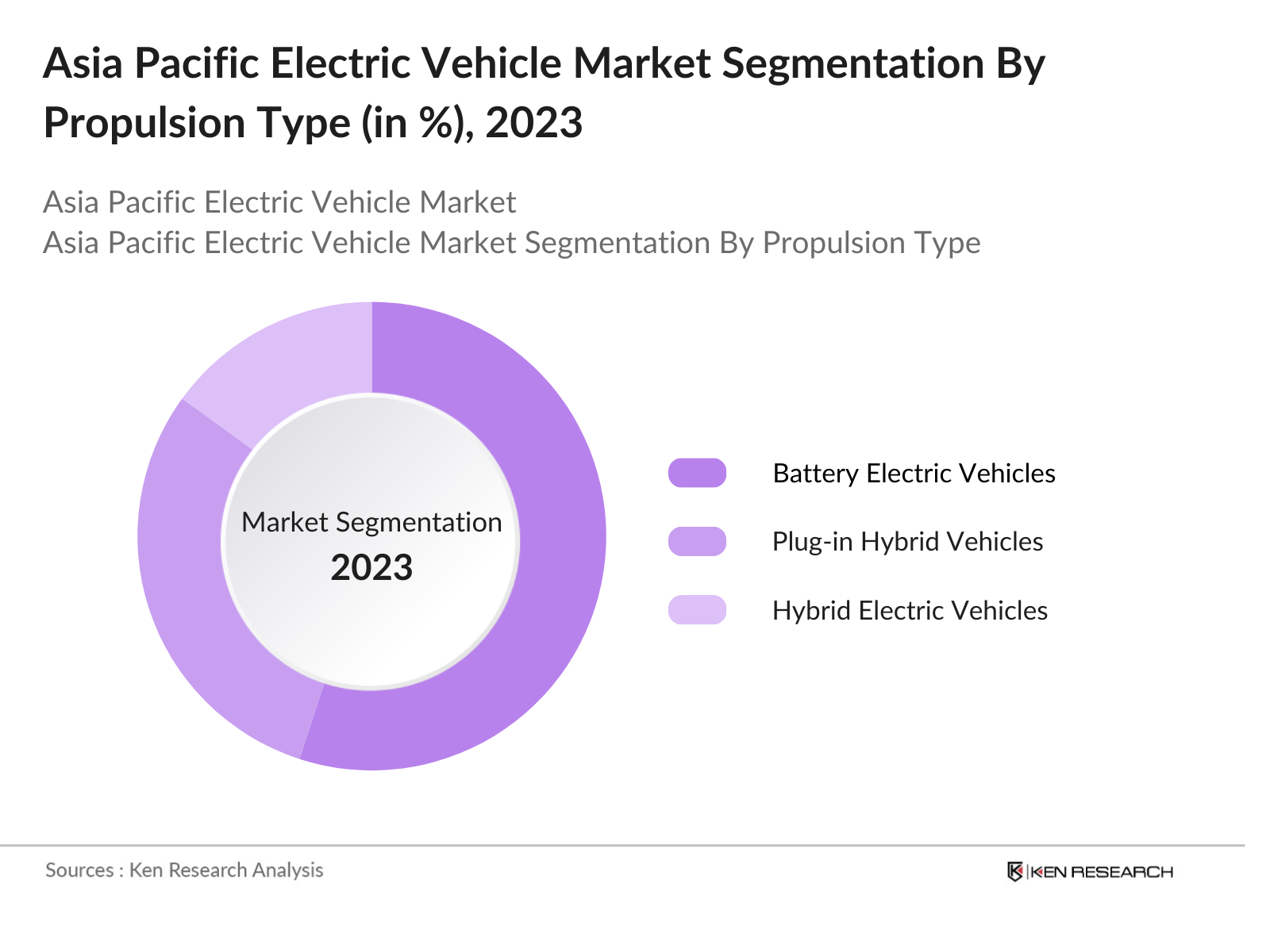

Propulsion Type |

BEV PHEV HEV |

|

Charging Type |

Fast Charging Slow Charging Wireless Charging |

|

Battery Capacity |

Below 50 kWh 50100 kWh Above 100 kWh |

|

Region |

China India Japan South Korea Southeast Asia |

1.1 Definition and Scope

1.2 Market Taxonomy

1.3 Market Growth Rate

1.4 Market Segmentation Overview

2.1 Historical Market Size

2.2 Year-On-Year Growth Analysis

2.3 Key Market Developments and Milestones

3.1 Growth Drivers

3.1.1 Government Incentives and Subsidies

3.1.2 Increasing Fuel Costs

3.1.3 Technological Advancements in Battery Technology

3.1.4 Growing Environmental Awareness

3.2 Market Challenges

3.2.1 High Cost of EVs

3.2.2 Limited Charging Infrastructure

3.2.3 Supply Chain Disruptions (Raw Material Shortages)

3.2.4 Consumer Range Anxiety

3.3 Opportunities

3.3.1 Expansion of EV Charging Networks

3.3.2 Urban Mobility Solutions

3.3.3 Integration of Renewable Energy in EV Charging

3.4 Trends

3.4.1 Rise of Battery Swapping Technology

3.4.2 Autonomous Electric Vehicles

3.4.3 Shift to Commercial EV Fleets

3.4.4 Increasing Focus on Lightweight EV Materials

3.5 Government Regulations

3.5.1 EV Adoption Targets and Policies (e.g., FAME II, New Energy Vehicle Policy)

3.5.2 Import Duty Exemptions and Tax Breaks

3.5.3 Regulations on EV Battery Recycling

3.6 SWOT Analysis

3.7 Stakeholder Ecosystem

3.8 Porters Five Forces Analysis

3.9 Competitive Ecosystem

4.1 By Vehicle Type (In Value %)

4.1.1 Passenger Electric Vehicles

4.1.2 Commercial Electric Vehicles

4.1.3 Two-Wheelers

4.1.4 E-Buses

4.2 By Propulsion Type (In Value %)

4.2.1 Battery Electric Vehicles (BEV)

4.2.2 Plug-in Hybrid Electric Vehicles (PHEV)

4.2.3 Hybrid Electric Vehicles (HEV)

4.3 By Charging Type (In Value %)

4.3.1 Fast Charging

4.3.2 Slow Charging

4.3.3 Wireless Charging

4.4 By Battery Capacity (In Value %)

4.4.1 Below 50 kWh

4.4.2 50100 kWh

4.4.3 Above 100 kWh

4.5 By Region (In Value %)

4.5.1 China

4.5.2 India

4.5.3 Japan

4.5.4 South Korea

4.5.5 Southeast Asia

5.1 Detailed Profiles of Major Companies

5.1.1 Tesla Inc.

5.1.2 BYD Auto Co. Ltd.

5.1.3 NIO Inc.

5.1.4 Hyundai Motor Company

5.1.5 Nissan Motor Co. Ltd.

5.1.6 SAIC Motor Corporation Limited

5.1.7 Tata Motors Limited

5.1.8 Honda Motor Co., Ltd.

5.1.9 Geely Auto Group

5.1.10 MG Motor

5.1.11 Xpeng Motors

5.1.12 Rivian Automotive, Inc.

5.1.13 Mahindra Electric Mobility Ltd.

5.1.14 KIA Corporation

5.1.15 Lucid Motors

5.2 Cross Comparison Parameters (No. of EV Models, Battery Range, Pricing, Headquarters, Revenue, Partnerships, Technology Patents, Market Share)

5.3 Market Share Analysis

5.4 Strategic Initiatives

5.5 Mergers and Acquisitions

5.6 Investment Analysis

5.7 Venture Capital Funding

5.8 Government Grants

5.9 Private Equity Investments

6.1 EV Policies and Targets in Major Countries

6.2 Import and Export Regulations for EV Components

6.3 EV Infrastructure Standards

6.4 Battery Recycling and Disposal Policies

6.5 Certification Processes for EV Safety and Efficiency

7.1 Future Market Size Projections

7.2 Key Factors Driving Future Market Growth

8.1 By Vehicle Type (In Value %)

8.2 By Propulsion Type (In Value %)

8.3 By Charging Type (In Value %)

8.4 By Battery Capacity (In Value %)

8.5 By Region (In Value %)

9.1 TAM/SAM/SOM Analysis

9.2 Customer Cohort Analysis

9.3 Marketing Initiatives

9.4 White Space Opportunity Analysis

The first step involves constructing an ecosystem map of key stakeholders within the Asia Pacific EV market. Extensive desk research and secondary databases were used to identify critical market variables that influence overall demand.

In this phase, historical market data on EV adoption rates, production capacities, and government policies were compiled. A thorough analysis of these variables was conducted to ensure reliable revenue estimates.

Market assumptions were validated via interviews with industry experts, including EV manufacturers and charging infrastructure providers. This process helped refine the accuracy of market projections.

Finally, insights were synthesized from direct discussions with key industry players. This final stage ensures a comprehensive and validated understanding of the Asia Pacific EV market.

The Asia Pacific Electric Vehicle market is valued at USD 205 billion, driven by government incentives, technological advancements, and increasing consumer interest in sustainable transportation solutions.

Challenges include the high cost of electric vehicles, insufficient charging infrastructure, supply chain disruptions, and consumer concerns about battery range.

Key players include Tesla, BYD Auto Co. Ltd., Hyundai Motor Company, Nissan Motor Co. Ltd., and Tata Motors Limited.

Growth is driven by government incentives, advancements in battery technology, increased environmental awareness, and rising fuel prices, especially in major cities like Beijing, Tokyo, and Seoul.

The Asia Pacific Electric Vehicle market is poised for significant growth due to technological innovations, policy support, and increasing consumer demand for eco-friendly transportation options.

Framework")

What makes us stand out is that our consultants follows Robust, Refine and Result (RRR) methodology. i.e. Robust for clear definitions, approaches and sanity checking, Refine for differentiating respondents facts and opinions and Result for presenting data with story

We have set a benchmark in the industry by offering our clients with syndicated and customized market research reports featuring coverage of entire market as well as meticulous research and analyst insights.

While we don't replace traditional research, we flip the method upside down. Our dual approach of Top Bottom & Bottom Top ensures quality deliverable by not just verifying company fundamentals but also looking at the sector and macroeconomic factors.

With one step in the future, our research team constantly tries to show you the bigger picture. We help with some of the tough questions you may encounter along the way: How is the industry positioned? Best marketing channel? KPI's of competitors? By aligning every element, we help maximize success.

Our report gives you instant access to the answers and sources that other companies might choose to hide. We elaborate each steps of research methodology we have used and showcase you the sample size to earn your trust.

If you need any support, we are here! We pride ourselves on universe strength, data quality, and quick, friendly, and professional service.